1. What is the Asia Pacific Antibiotics Market Overview – definition, scope, and significance?

The Asia Pacific antibiotics market encompasses the production, distribution, and consumption of antibacterial pharmaceutical products across the Asia‑Pacific region, including countries such as China, India, Japan, South Korea, Australia, and Southeast Asian nations. The market scope covers all drug classes—sulfonamides, aminoglycosides, carbapenems, macrolides, fluoroquinolones, penicillins, and cephalosporins—as well as diverse mechanisms of action ranging from mycolic acid inhibition to protein synthesis inhibition. Its significance lies in the region’s rapidly growing population, rising healthcare expenditure, and increasing incidence of bacterial infections, all of which drive demand for effective antimicrobial therapies.

2. What are the key drivers, restraints, challenges, and opportunities shaping the Asia Pacific antibiotics market?

Key drivers include expanding middle‑class populations, heightened awareness of infectious diseases, and strong governmental support for antimicrobial stewardship programs. Economic growth fuels hospital infrastructure expansion, thereby boosting antibiotic consumption. Restraints arise from growing antimicrobial resistance (AMR) concerns, which prompt stricter regulations and limit unrestricted sales. Challenges involve complex regulatory pathways across multiple jurisdictions and supply‑chain disruptions that can affect raw‑material availability. Opportunities are evident in the development of novel drug classes, biotech‑derived antibiotics, and partnerships that leverage advanced drug‑delivery platforms to address resistant strains.

3. What are the current growth trends in the Asia Pacific antibiotics market?

Current trends feature a shift towards broad‑spectrum agents that address multidrug‑resistant pathogens, alongside a steady rise in demand for narrow‑spectrum agents for targeted therapy. There is also a noticeable increase in outpatient antibiotic prescriptions driven by telemedicine adoption. Emerging trends include the integration of digital health tools for prescription monitoring and the use of real‑world evidence to support new drug approvals. Additionally, several regional manufacturers are scaling up biosimilar antibiotic production to meet cost‑sensitive market segments.

4. How has COVID‑19 impacted the Asia Pacific antibiotics market and what is the recovery trajectory?

The COVID‑19 pandemic initially suppressed routine antibiotic consumption due to reduced elective procedures and lower hospital admissions. However, secondary bacterial infections in COVID‑19 patients temporarily heightened the use of broad‑spectrum antibiotics. Post‑pandemic, the market is recovering as healthcare services normalize, and antimicrobial stewardship initiatives are being reinforced to curb inappropriate use. The recovery trajectory is positive, with demand returning to pre‑pandemic levels and expected to accelerate as vaccination drives reduce viral burden, freeing resources for bacterial infection management.

5. Who are the major competitors and what is the consolidation landscape in the Asia Pacific antibiotics market?

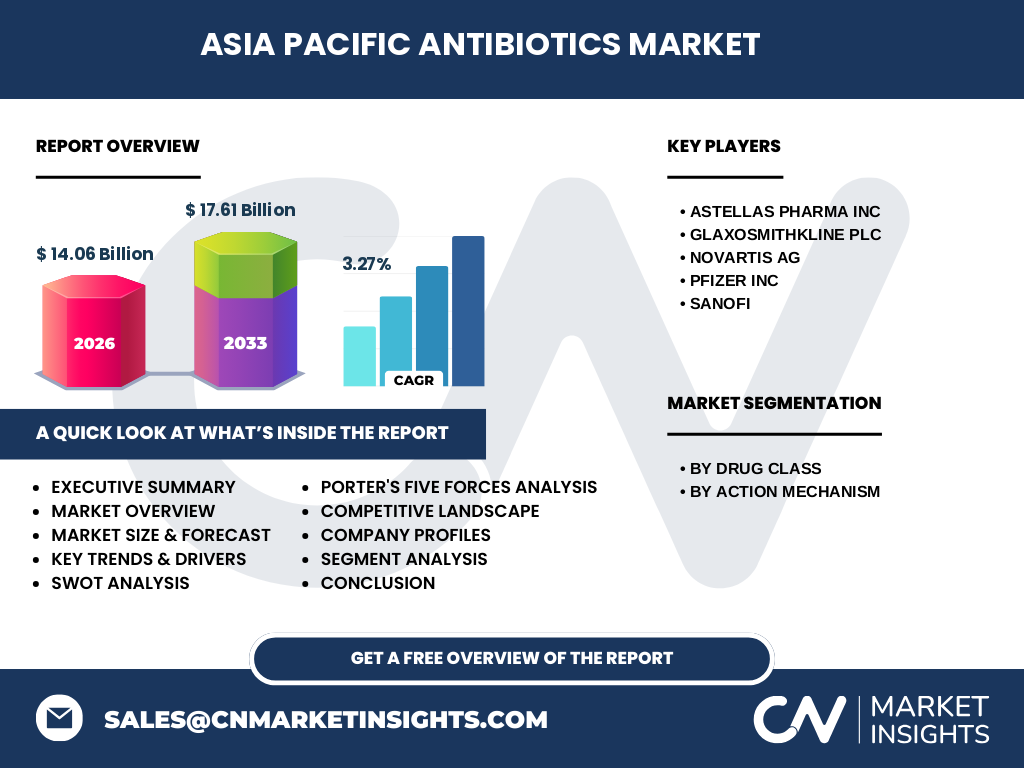

Major competitors include Astellas Pharma Inc, GlaxoSmithKline plc, Novartis AG, Pfizer Inc, and Sanofi. These multinational firms dominate through extensive product portfolios, robust R&D pipelines, and strategic alliances with local manufacturers. Consolidation is occurring via mergers, acquisitions, and joint ventures aimed at expanding geographic reach and enriching pipeline assets. Recent activity features cross‑border collaborations that combine global expertise with regional market knowledge, strengthening competitive positioning.

6. What are the high‑level findings and key takeaways in the Executive Summary?

The Asia Pacific antibiotics market is valued at USD 14.06 billion in 2026 and is projected to reach USD 17.61 billion by 2033, reflecting a compound annual growth rate (CAGR) of 3.27 %. Growth is underpinned by expanding healthcare infrastructure, rising awareness of bacterial infections, and continued investment in novel antimicrobial agents. Nonetheless, AMR remains a critical concern, prompting regulatory scrutiny and encouraging innovation. The market is fragmented yet increasingly consolidated as leading global firms pursue strategic partnerships and acquisitions to secure market share.

7. What are the forecast expectations for the Asia Pacific antibiotics market from 2025 to 2032?

Based on the provided CAGR of 3.27 %, the market is expected to maintain steady expansion through 2032. The forecast anticipates incremental annual increases that will cumulatively push market value from the 2026 baseline of USD 14.06 billion to approximately USD 17.61 billion by 2033. This trajectory suggests a robust demand environment, reinforced by ongoing healthcare reforms, rising infection rates, and sustained R&D investment in newer antibiotic classes.

8. How is the Asia Pacific antibiotics market sized and shared by drug class and mechanism of action?

Segmentation by drug class includes sulfonamides, aminoglycosides, carbapenems, macrolides, fluoroquinolones, penicillins, and cephalosporins. Each class contributes to the overall market value, with broad‑spectrum agents such as carbapenems and fluoroquinolones typically commanding higher price points due to their critical role in treating resistant infections. Mechanism‑of‑action segmentation comprises mycolic acid inhibitors, RNA synthesis inhibitors, DNA synthesis inhibitors, protein synthesis inhibitors, and cell wall synthesis inhibitors. The diversity of mechanisms reflects the market’s response to evolving bacterial resistance patterns, ensuring therapeutic options across multiple pathways.

9. What is the geographic distribution of the Asia Pacific antibiotics market by region?

The market is spread across key sub‑regions: East Asia (China, Japan, South Korea), South Asia (India, Bangladesh, Pakistan), and Southeast Asia (Indonesia, Thailand, Vietnam, Philippines, Malaysia). Each sub‑region contributes to the aggregate market value of USD 14.06 billion in 2026, with growth driven by localized healthcare policies, population density, and disease prevalence. While exact regional share percentages are not disclosed, the overall regional mix reflects a balanced contribution from both high‑income (Japan, South Korea, Australia) and emerging economies (China, India, Indonesia).

10. What are the detailed regional performance insights for the Asia Pacific antibiotics market?

East Asia remains a major consumer due to advanced hospital networks and higher per‑capita pharmaceutical spending. China’s rapid urbanization and expanding insurance coverage have accelerated antibiotic uptake, particularly for high‑value carbapenems and fluoroquinolones. South Asia, led by India, shows strong growth in generic antibiotic production, positioning the region as both a supplier and a large consumer. Southeast Asia experiences steady demand growth, propelled by government initiatives to improve infectious‑disease surveillance and expand primary‑care access.

11. Which companies lead the Asia Pacific antibiotics market and what are their current strategies?

Key players—Astellas Pharma Inc, GlaxoSmithKline plc, Novartis AG, Pfizer Inc, and Sanofi—focus on expanding product pipelines, leveraging biosimilar platforms, and forming strategic alliances with regional manufacturers. Astellas emphasizes renal‑targeted antibiotics, whereas GSK invests in pediatric formulations. Novartis pursues next‑generation beta‑lactams, Pfizer advances its fluoroquinolone portfolio, and Sanofi concentrates on integrating antimicrobial stewardship tools with its commercial offerings. Across the board, companies are prioritizing R&D, regulatory alignment, and market‑access initiatives.

12. How does Porter’s Five Forces framework evaluate the competitive dynamics of the Asia Pacific antibiotics market?

• Threat of new entrants: Moderate – high R&D costs and stringent regulatory requirements create barriers, yet emerging biotech firms and generic manufacturers pose a selective threat.

• Bargaining power of suppliers: Low to moderate – raw‑material suppliers are numerous, but specialized active pharmaceutical ingredients (APIs) for newer classes can command higher leverage.

• Bargaining power of buyers: Growing – hospitals and national health systems increasingly demand price transparency and value‑based contracts, boosting buyer influence.

• Threat of substitutes: Low – limited therapeutic alternatives to antibiotics for bacterial infections, though vaccine development is a peripheral substitute.

• Industry rivalry: High – intense competition among multinational and regional firms drives innovation, pricing pressure, and strategic collaborations.

13. What are the SWOT highlights for the Asia Pacific antibiotics market?

Strengths: Large and growing patient base, diversified drug‑class portfolio, strong R&D pipelines.

Weaknesses: High susceptibility to AMR regulations, dependence on a few high‑margin broad‑spectrum agents.

Opportunities: Development of novel mechanisms, expansion of biosimilar antibiotic lines, digital stewardship platforms.

Threats: Escalating resistance, potential pricing controls, and supply‑chain disruptions for critical APIs.

14. How is the value chain of the Asia Pacific antibiotics market structured?

The value chain begins with discovery and pre‑clinical research, progresses through clinical trials and regulatory approval, then moves to manufacturing (including API synthesis and formulation), followed by distribution via wholesalers and pharmacy networks. End‑users are hospitals, clinics, and retail pharmacies. Supporting services—including pharmacovigilance, antimicrobial‑stewardship consulting, and digital prescription‑tracking—add value throughout the chain, especially in mature markets where compliance and data‑driven decision‑making are emphasized.

15. What investment insights are most relevant for stakeholders in the Asia Pacific antibiotics market?

Investors should prioritize companies with diversified pipelines across multiple drug classes and mechanisms, as this mitigates AMR‑related risk. Strategic allocation toward firms that have secured regional partnerships or joint ventures can accelerate market entry and scale production. Funding opportunities exist in digital health solutions that enable antibiotic stewardship, as well as in contract manufacturing organizations (CMOs) that specialize in API production for high‑potency antibiotics. Finally, monitoring regulatory developments will help anticipate pricing and reimbursement shifts.

16. What are the concluding observations from this market research?

The Asia Pacific antibiotics market is on a steady growth path, driven by demographic dynamics, rising infection rates, and sustained investment in drug development. While AMR presents a persistent challenge, it also fuels innovation and creates opportunities for next‑generation agents. Market leaders are consolidating through strategic alliances, and emerging players are gaining ground via biosimilar production. Overall, the market’s projected CAGR of 3.27 % underscores a resilient outlook, encouraging continued investment and strategic focus.

17. What methodology was employed to conduct this research?

The study combined primary interviews with industry experts, secondary data extraction from reputable pharmaceutical databases, and trend analysis using historical sales figures. Forecast modeling applied a compound annual growth rate (CAGR) of 3.27 % based on the 2026 market size of USD 14.06 billion and the 2033 projected value of USD 17.61 billion. Segmentation analysis utilized the defined drug‑class and mechanism‑of‑action categories, while competitive mapping incorporated publicly disclosed financials and pipeline information of the key companies.

18. What is the scope and coverage of this research?

The research covers the entire Asia Pacific region, encompassing all major economies and sub‑regions. It evaluates market size, segmentation, competitive dynamics, and forecasts through 2033. Limitations are confined to publicly available data; proprietary company‑specific sales figures and undisclosed pipeline details are not included. Nonetheless, the analysis provides a comprehensive view of market drivers, trends, and strategic opportunities.

19. Which key companies have recent developments in the Asia Pacific antibiotics market?

Recent highlights include Astellas Pharma Inc’s launch of a new renal‑targeted carbapenem in Japan, GlaxoSmithKline plc’s partnership with an Indian generic manufacturer to expand sulfonamide production, Novartis AG’s acquisition of a biotech firm specializing in RNA synthesis inhibitors, Pfizer Inc’s rollout of a digital stewardship platform across Southeast Asian hospitals, and Sanofi’s entry into the cephalosporin biosimilar segment through a joint venture in South Korea. These initiatives reflect a focus on pipeline expansion, market access, and innovative delivery solutions.