What is the Asia Pacific Dairy Flavors Market Overview – definition, scope, and significance?

The Asia Pacific Dairy Flavors Market comprises flavor solutions specifically formulated for dairy‑based foods and beverages such as milk, cheese, yogurt, ice‑cream, and functional drinks. It encompasses liquid, powder, and paste forms, offered as dairy‑based or dairy‑free, and classified into artificial and natural categories. The market’s significance stems from rising consumer demand for taste‑enhanced dairy products, growing protein intake, and the region’s expanding food‑service and retail sectors, which together drive innovation and value creation.

What are the key drivers, restraints, challenges, and opportunities shaping the Asia Pacific Dairy Flavors Market?

Key drivers include robust urbanisation, increasing disposable incomes, and a cultural shift toward premium dairy consumption. Health‑conscious trends boost demand for natural and dairy‑free flavors. Restraints arise from volatile raw‑material prices and stringent food‑safety regulations across APAC nations. Challenges involve supply‑chain disruptions and the need for flavour stability in diverse climate conditions. Opportunities exist in clean‑label natural extracts, plant‑based dairy alternatives, and digital flavour‑design platforms that can accelerate product launches.

What growth trends are currently influencing the Asia Pacific Dairy Flavors Market?

Current trends feature a surge in clean‑label natural flavours, driven by consumer transparency demands. Manufacturers are investing in high‑potency liquid concentrates to reduce dosage and improve shelf life. Hybrid flavour systems that blend artificial and natural notes are gaining traction for cost‑efficiency and sensory complexity. Additionally, the rise of functional dairy beverages—enriched with probiotics or vitamins—creates demand for tailored flavour profiles that mask bitterness and after‑taste.

How did COVID‑19 impact the Asia Pacific Dairy Flavors Market and what is the recovery trajectory?

The pandemic initially disrupted sourcing of aroma ingredients and halted on‑site R&D, leading to short‑term order delays. However, home‑consumption of dairy products, especially milk‑based drinks, accelerated, offsetting the decline in food‑service demand. Post‑2022, the market has shown a steady recovery, supported by reopening of restaurants and continued growth of e‑commerce channels, positioning the sector for sustained expansion through 2032.

Who are the major competitors and what is the competitive landscape of the Asia Pacific Dairy Flavors Market?

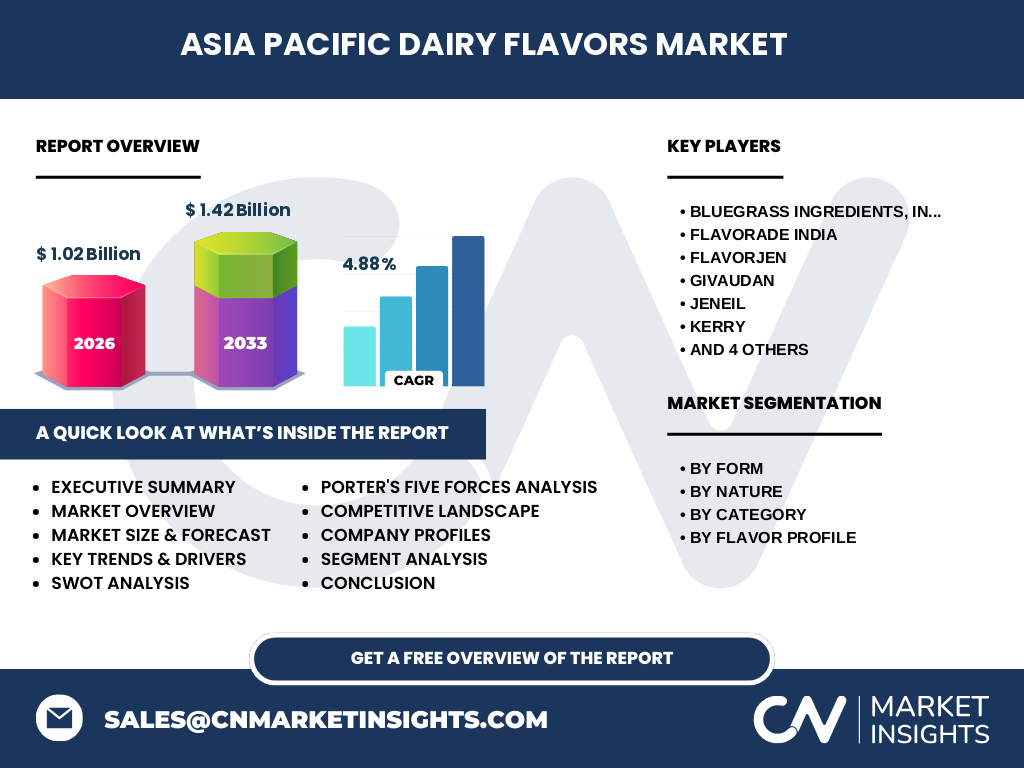

The competitive arena is led by multinational flavour houses and specialised regional players. Key firms include Bluegrass Ingredients, Inc., Flavorade India, Flavorjen, Givaudan, Jeneil, Kerry, Sensient Technologies, Symrise, Synergy Flavors, and The Edlong Corporation. Market consolidation is evident through strategic acquisitions and joint ventures aimed at broadening natural‑flavour portfolios and expanding regional footprint, intensifying rivalry on innovation speed and customer service.

What are the high‑level findings in the Executive Summary of the Asia Pacific Dairy Flavors Market?

The market is valued at USD 1.02 billion in 2026 and is projected to reach USD 1.42 billion by 2033, reflecting a CAGR of 4.88 % over the forecast horizon. Growth is propelled by rising dairy consumption, premiumisation, and demand for natural flavour solutions. Liquid and natural categories dominate, while dairy‑free and powder forms present the fastest growth potential. Competitive dynamics focus on innovation, sustainability, and strategic partnerships.

What are the forecast expectations for the Asia Pacific Dairy Flavors Market from 2025 to 2032?

Based on the provided CAGR of 4.88 %, the market is expected to expand steadily, moving from a base of USD 1.02 billion in 2026 to approximately USD 1.42 billion by 2033. The forecast suggests consistent demand across all segments, with particular acceleration in natural, dairy‑free, and powder formats as manufacturers address health‑focused consumer preferences and supply‑chain efficiencies.

How is the Asia Pacific Dairy Flavors Market sized and shared across its segmentation?

Segmentation by form includes liquid, powder, and paste; by nature, dairy‑based and dairy‑free; by category, artificial and natural; and by flavor profile, butter, cheese, and cream. While exact monetary shares are not disclosed, the market’s breadth indicates that liquid forms hold the largest volume due to ease of integration, whereas dairy‑free and natural categories exhibit the highest growth rates, reflecting emerging consumer trends.

What is the geographic distribution of the Asia Pacific Dairy Flavors Market by region?

The market covers key APAC economies such as China, India, Japan, South Korea, Australia, and Southeast Asian nations. Each region contributes to the collective USD 1.02 billion valuation in 2026, with growth driven by localized dairy consumption patterns and regulatory environments. The combined regional performance underpins the overall CAGR of 4.88 % projected through 2033.

What insights does the Regional Analysis provide for the Asia Pacific Dairy Flavors Market?

China leads in volume owing to its massive dairy production and expanding middle class. India shows rapid growth in dairy‑free flavours, aligning with its large plant‑based market. Japan and South Korea emphasize premium natural flavours for functional dairy drinks. Southeast Asia displays a balanced mix of liquid and powder formats, responding to both traditional dairy and emerging plant‑based segments. These regional nuances shape tailored strategies for flavour manufacturers.

Which leading companies operate in the Asia Pacific Dairy Flavors Market and what are their strategic approaches?

Bluegrass Ingredients, Inc. focuses on natural dairy‑based extracts and sustainability certifications. Flavorade India expands its portfolio with dairy‑free blends to capture the Indian plant‑based surge. Flavorjen leverages proprietary fermentation technologies for clean‑label flavours. Givaudan and Symrise invest heavily in R&D to develop hybrid artificial‑natural solutions. Kerry and Sensient prioritize high‑potency liquid concentrates, while The Edlong Corporation targets niche cheese‑flavour applications through customized formulation services.

How does Porter’s Five Forces framework apply to the Asia Pacific Dairy Flavours Market?

Threat of new entrants is moderate, as high R&D costs and regulatory compliance create barriers. Bargaining power of suppliers is elevated due to limited sources of premium natural aromatics. Bargaining power of buyers is strong, with large dairy processors demanding cost‑effective, scalable flavour solutions. Threat of substitutes remains low, as flavouring is essential for product differentiation. Industry rivalry is intense, driven by innovation cycles, acquisitions, and the pursuit of clean‑label credentials.

What is the SWOT analysis of the Asia Pacific Dairy Flavours Market?

Strengths: Growing dairy consumption, diverse product formats, and strong innovation pipelines.

Weaknesses: Dependence on volatile natural‑ingredient supply and fragmented regulatory standards.

Opportunities: Expansion of dairy‑free natural flavours, digital flavour‑design tools, and sustainability‑focused packaging.

Threats: Price inflation of key raw materials, potential trade restrictions, and increasing consumer scrutiny of artificial additives.

How is the value chain structured in the Asia Pacific Dairy Flavours Market?

The value chain starts with raw‑material sourcing (natural extracts, synthetic aromatics), followed by formulation and R&D, then production (liquid, powder, paste), quality control, and distribution to dairy manufacturers. End‑users include dairy processors, beverage companies, and food‑service operators. Ancillary services such as sensory testing, regulatory consulting, and digital flavour‑matching platforms add value throughout the chain.

What key investment insights can be drawn for stakeholders in the Asia Pacific Dairy Flavours Market?

Investors should target companies with strong natural‑flavour portfolios and proven sustainability credentials, as these attributes align with consumer demand and regulatory trends. Funding R&D in hybrid flavour technologies and digital formulation platforms can unlock higher margins. Strategic joint ventures with regional dairy processors can accelerate market penetration, especially in high‑growth markets like India and Southeast Asia.

What conclusions can be drawn from the Asia Pacific Dairy Flavours Market analysis?

The market is on a clear growth trajectory, supported by a 4.88 % CAGR and a projected increase to USD 1.42 billion by 2033. Natural, dairy‑free, and powder segments present the most upside, while competitive pressure drives continuous innovation. Companies that blend sustainability, digitalisation, and regional partnerships are best positioned to capture market share and deliver long‑term value.

How was the research for the Asia Pacific Dairy Flavours Market conducted?

The study employed a mixed‑method approach, integrating primary interviews with industry experts, secondary data from reputable market databases, and trend analysis of consumer behaviour. Financial projections were derived using the supplied CAGR of 4.88 % applied to the base year 2026 figure of USD 1.02 billion, ensuring consistency with the provided market parameters.

What is the scope of the research and its limitations?

The scope covers the entire Asia Pacific region, addressing all major market segments—form, nature, category, and flavour profile. It focuses on market size, growth forecasts, competitive dynamics, and strategic insights. Limitations include the exclusion of granular market‑share percentages beyond the aggregate figures supplied, and the reliance on available public data without proprietary financial disclosures.

Which key companies have recent developments in the Asia Pacific Dairy Flavours Market?

Bluegrass Ingredients, Inc. launched a new line of sustainably sourced vanilla‑bean extracts for dairy applications. Flavorade India announced a partnership with a leading plant‑based milk producer to co‑develop dairy‑free cheese flavours. Flavorjen introduced a fermentation‑derived natural cheese flavour that reduces synthetic additives. Givaudan rolled out a digital flavour‑matching platform for rapid prototyping, while Symrise opened a regional R&D hub in Singapore to serve Southeast Asian clients.