What is the Europe Dairy Flavor Market Overview – Definition, scope, and significance?

The Europe Dairy Flavor Market encompasses all flavor solutions that replicate or enhance dairy‑derived tastes such as butter, cheese, cream, yogurt, and milk across various food and beverage categories. The market scope includes liquid, powder, and paste forms of flavors and serves applications ranging from bakery and confectionery to soups, sauces, beverages, and dairy products themselves. This segment is significant because dairy flavors drive consumer acceptance of novel and clean‑label products, enable manufacturers to meet changing taste preferences, and support the growth of value‑added processed foods throughout the European region.

What are the Europe Dairy Flavor Market Drivers, Restraints, Challenges, and Opportunities?

Key drivers include rising consumer demand for premium and natural‑tasting dairy‑based products, expanding clean‑label trends, and the growth of functional foods that rely on authentic dairy notes. Opportunities arise from the increasing popularity of plant‑based alternatives that require dairy‑flavor replication, and from innovative delivery formats such as micro‑encapsulated liquid flavors. Restraints involve stringent EU food‑safety regulations and heightened price sensitivity among bulk manufacturers. Challenges stem from fluctuating raw‑material costs for natural dairy extracts and the need for rapid product development cycles to keep pace with fast‑moving consumer trends.

What are the Europe Dairy Flavor Market Growth Trends?

Current trends highlight a shift toward clean‑label, non‑GMO, and sustainably sourced dairy flavors. Manufacturers are adopting high‑purity natural extracts and exploring fermentation‑derived flavor compounds to meet consumer expectations. Emerging trends include the use of dairy‑flavor blends that combine traditional butter or cheese notes with exotic fruit or spice accents, catering to adventurous palettes. Additionally, the growth of ready‑to‑drink coffee and tea beverages in Europe fuels demand for liquid dairy flavors that dissolve instantly without affecting product stability.

How has COVID‑19 impacted the Europe Dairy Flavor Market and what is the recovery trajectory?

The pandemic initially disrupted supply chains for natural dairy extracts, causing temporary shortages and price spikes. However, the surge in home cooking and increased consumption of packaged foods accelerated demand for convenient flavor solutions, especially in powder and paste formats suitable for food‑service and ready‑meal producers. Recovery has been steady, with market confidence returning as manufacturers diversify sourcing and invest in digital forecasting tools. The post‑COVID landscape shows a stronger emphasis on resilience and local sourcing within the European dairy flavor ecosystem.

What does the Europe Dairy Flavor Market Competitive Landscape look like?

The competitive environment is characterized by a mix of global flavor houses and specialized regional players. Major competitors such as Kerry Group, CP Ingredients, and Ornua Co‑operative Limited dominate through extensive R&D portfolios and integrated supply chains. Smaller innovators like Synergy Flavors and The Edlong Corporation focus on niche applications and customized flavor blends. Recent consolidation activity includes strategic alliances and joint ventures aimed at expanding natural‑flavor capabilities and broadening geographic reach across Europe.

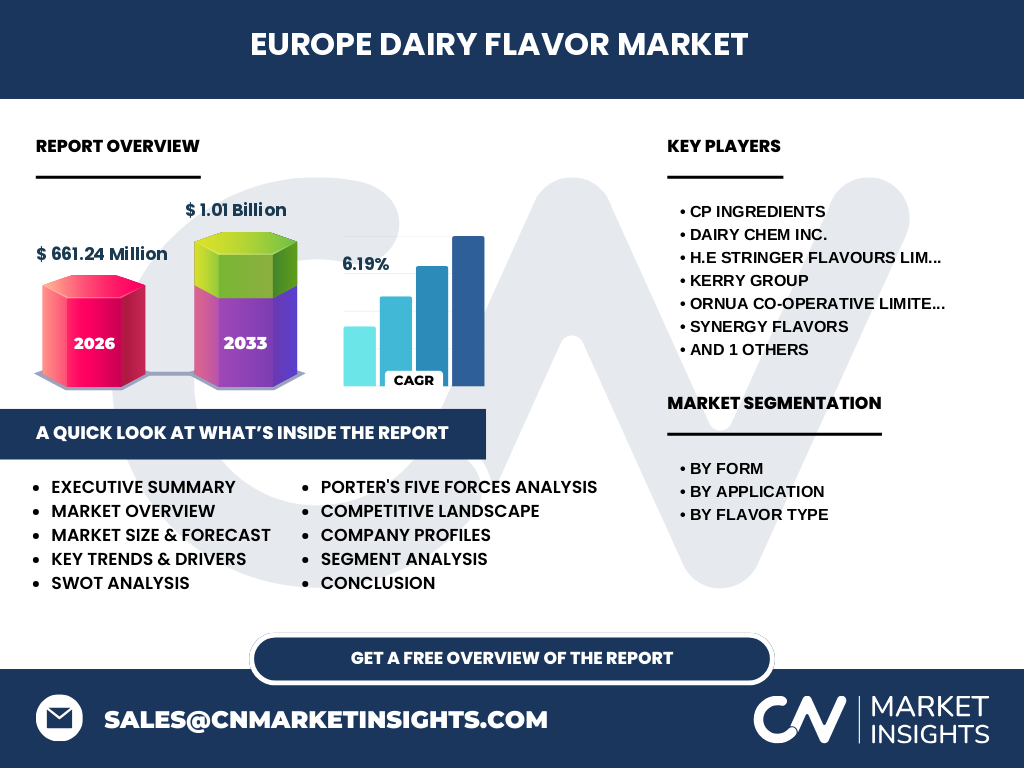

What are the key findings in the Executive Summary of the Europe Dairy Flavor Market?

The Europe Dairy Flavor Market is projected to grow from a 2026 valuation of €661.24 million to €1.01 billion by 2033, representing a robust CAGR of 6.19 %. Growth is propelled by demand for natural, clean‑label dairy flavors, the expansion of plant‑based products requiring dairy‑flavor mimicry, and the rise of premium dairy‑flavored beverages. Competitive dynamics are intensifying, with leading firms investing in sustainable sourcing and innovative delivery formats. The market presents significant opportunities for entrants that can offer high‑purity, low‑cost natural extracts and flexible supply solutions.

What is the Europe Dairy Flavor Market Forecast for 2025‑2032?

Guided by the stated CAGR of 6.19 %, the market is expected to maintain steady expansion throughout the 2025‑2032 horizon. The forecast indicates continued traction in the liquid flavor segment, driven by beverage applications, while powder forms retain strong demand in bakery and confectionery. Paste flavors are anticipated to grow modestly, supporting niche applications such as dairy‑enhanced sauces. The overall market size is projected to approach €1 billion by the early 2030s, underscoring sustained investor interest.

What is the Europe Dairy Flavor Market Size and Share by Segmentation?

By form, the market is divided into liquid, powder, and paste flavors. Liquid flavors command the largest share due to their versatility in beverage and high‑volume food manufacturing. Powder flavors hold a solid position, especially in bakery and confectionery where ease of handling and stability are essential. Paste flavors serve specialized applications such as dairy‑enhanced sauces. By application, bakery and confectionery together represent a substantial portion of demand, followed by beverages, dairy products, and soups & sauces. Flavor type segmentation shows butter and cheese flavors leading the portfolio, with cream, yogurt, and milk flavors growing alongside consumer interest in richer, authentic dairy experiences.

What is the Global Europe Dairy Flavor Market Size and Share by Region?

Europe remains a core hub for dairy flavor innovation, accounting for the majority of the €661.24 million market in 2026. While the report focuses on Europe, the region’s share reflects its advanced food‑processing industry, robust regulatory framework, and high consumer expectations for flavor quality. The market’s growth contributes significantly to the global dairy flavor landscape, positioning Europe as a trendsetter for flavor development worldwide.

What does the Regional Analysis of the Europe Dairy Flavor Market reveal?

Western Europe, led by Germany, France, and the United Kingdom, drives the largest share, benefiting from mature food‑processing sectors and strong R&D investment. Northern Europe, particularly Scandinavia, shows rapid adoption of natural and sustainable flavor solutions. Southern Europe, with Italy and Spain, emphasizes artisanal and premium dairy flavors, especially in cheese and yogurt applications. Central and Eastern European markets are emerging, with increasing demand for cost‑effective powder flavors as local food manufacturers expand.

Who are the leading company profiles in the Europe Dairy Flavor Market?

Kerry Group leads with an expansive portfolio of natural dairy extracts and strong sustainability commitments. CP Ingredients specializes in high‑purity liquid dairy flavors and operates a network of regional production sites. Ornua Co‑operative Limited leverages its dairy cooperatives to source authentic milk‑based flavors. Dairy Chem Inc. provides a broad range of powder and paste dairy flavors, targeting bakery and confectionery. Synergy Flavors and The Edlong Corporation focus on customized flavor blends and niche market segments, offering agility and rapid turnaround for specialty clients.

What does Porter’s Five Forces Analysis reveal about the Europe Dairy Flavor Market?

• Threat of new entrants is moderate; high R&D costs and regulatory compliance create barriers, yet niche specialization offers entry points.

• Bargaining power of suppliers is moderate; dependence on natural dairy extracts gives raw‑material providers some leverage, but diversified sourcing mitigates risk.

• Bargaining power of buyers is high; large food manufacturers demand competitive pricing and consistent quality, driving suppliers to innovate.

• Threat of substitutes is low; while plant‑based flavor technologies exist, authentic dairy notes remain unmatched for many applications.

• Competitive rivalry is intense, with major players investing in product differentiation, sustainability, and strategic partnerships to protect market share.

What are the SWOT Analysis insights for the Europe Dairy Flavor Market?

Strengths: Established supply chains, advanced R&D capabilities, and strong consumer demand for authentic dairy flavors.

Weaknesses: Sensitivity to raw‑material price volatility and strict regulatory requirements.

Opportunities: Expansion into plant‑based dairy‑flavor replication, development of clean‑label natural extracts, and growth in premium beverage segments.

Threats: Potential trade restrictions affecting dairy ingredient imports and increasing competition from bio‑engineered flavor alternatives.

How is the Europe Dairy Flavor Market Value Chain structured?

The value chain begins with raw‑material procurement (milk, butter, cheese cultures), followed by extraction and purification processes to create flavor concentrates. These concentrates are then formulated into liquid, powder, or paste forms, packaged, and distributed to food manufacturers. End‑users—bakery, confectionery, beverage, dairy, and sauce producers—integrate the flavors into finished products. Supporting activities include quality assurance, regulatory compliance, and post‑sale technical support.

What are the key investment insights in the Europe Dairy Flavor Market?

Investors should target companies with strong natural‑flavor pipelines and demonstrated sustainability credentials, as these align with consumer trends and regulatory expectations. Strategic acquisitions of niche flavor innovators can accelerate portfolio diversification. Additionally, funding R&D projects focused on fermentation‑derived dairy flavors offers a pathway to lower cost, high‑purity solutions that reduce dependence on traditional dairy sourcing.

What conclusions can be drawn about the Europe Dairy Flavor Market?

The Europe Dairy Flavor Market is on a clear growth trajectory, underpinned by a 6.19 % CAGR and a projected valuation exceeding €1 billion by 2033. Demand for authentic, natural dairy flavors across multiple food categories is resilient, and the market’s competitive landscape encourages continuous innovation. Companies that prioritize sustainable sourcing, expand liquid‑flavor capabilities, and address plant‑based flavor needs are well positioned to capture future value.

What research methodology was employed for this market study?

The analysis combines primary interviews with industry experts, secondary data from company reports, trade publications, and regulatory databases. Quantitative projections are based on the supplied market size (€661.24 million in 2026) and CAGR (6.19 %). Qualitative insights derive from trend monitoring, competitive benchmarking, and scenario planning to assess drivers, restraints, and opportunities.

What is the scope of this research?

The study covers the European region, focusing on dairy‑flavor forms (liquid, powder, paste), applications (bakery, confectionery, soups & sauces, beverages, dairy products), and flavor types (butter, cheese, cream, yogurt, milk). It includes major market participants, growth forecasts through 2033, and strategic analyses such as Porter’s Five Forces and SWOT. Geographic granularity extends to Western, Northern, Southern, and Central/Eastern Europe.

Which key companies and recent developments are shaping the Europe Dairy Flavor Market?

Kerry Group announced a new sustainable sourcing initiative for natural butter flavor extracts, aiming to reduce carbon footprint by 15 % by 2025. CP Ingredients launched a micro‑encapsulated liquid dairy flavor designed for high‑temperature beverage processing. Ornua Co‑operative Limited introduced a line of organic milk‑based flavor concentrates targeting premium dairy product manufacturers. Dairy Chem Inc. reported a partnership with a leading bakery chain to supply powder cheese flavors for frozen pastry lines. Synergy Flavors unveiled a rapid‑prototype platform for custom dairy‑flavor blends, and The Edlong Corporation expanded its European manufacturing footprint with a new paste‑flavor facility in the Netherlands.