1. Europe E‑Invoicing Market Overview – Definition, scope, and significance?

The Europe E‑Invoicing market encompasses digital invoicing solutions that enable the creation, transmission, receipt, and storage of invoices in electronic formats across European businesses. It covers both cloud‑based and on‑premise platforms, serving B2B and B2C end‑users. The market’s significance lies in its ability to streamline financial processes, reduce manual errors, accelerate cash flow, and support regulatory compliance with EU directives on electronic transactions.

2. Europe E‑Invoicing Market Drivers, Restraints, Challenges, and Opportunities – Key growth factors and obstacles?

Key drivers include mandatory e‑invoicing regulations in many EU countries, the demand for cost‑effective finance operations, and the push toward digital transformation. Restraints stem from legacy system integration complexities and data‑security concerns. Challenges involve varying national standards and the need for skilled personnel. Opportunities arise from the expanding cloud adoption, cross‑border trade facilitation, and the emergence of AI‑enhanced invoice processing.

3. Europe E‑Invoicing Market Growth Trends – Current and emerging trends shaping the market?

Current trends feature a strong migration to cloud‑based invoicing due to scalability and lower upfront costs. Emerging trends include the integration of blockchain for invoice authenticity, the use of machine‑learning algorithms for automated validation, and the growing preference for API‑first solutions that enable seamless connectivity with ERP and procurement systems.

4. COVID‑19 Impact on the Europe E‑Invoicing Market – Pandemic effects and recovery trajectory?

The COVID‑19 pandemic accelerated digital adoption as remote work forced firms to digitize financial workflows. Companies increased investments in cloud invoicing to maintain business continuity. Post‑pandemic, the market has continued on an upward trajectory, benefiting from heightened awareness of the efficiencies offered by e‑invoicing and the need for resilient, contact‑less processes.

5. Europe E‑Invoicing Market Competitive Landscape – Major competitors and market consolidation?

The competitive arena features established technology leaders and niche specialists. Prominent players such as SAP SE, IBM Corporation, and The Sage Group plc command significant market presence, while innovators like Basware Corporation, Cegedim SA, and Tradeshift drive niche differentiation. Recent years have seen strategic alliances and selective acquisitions, fostering moderate consolidation aimed at expanding solution portfolios and geographic reach.

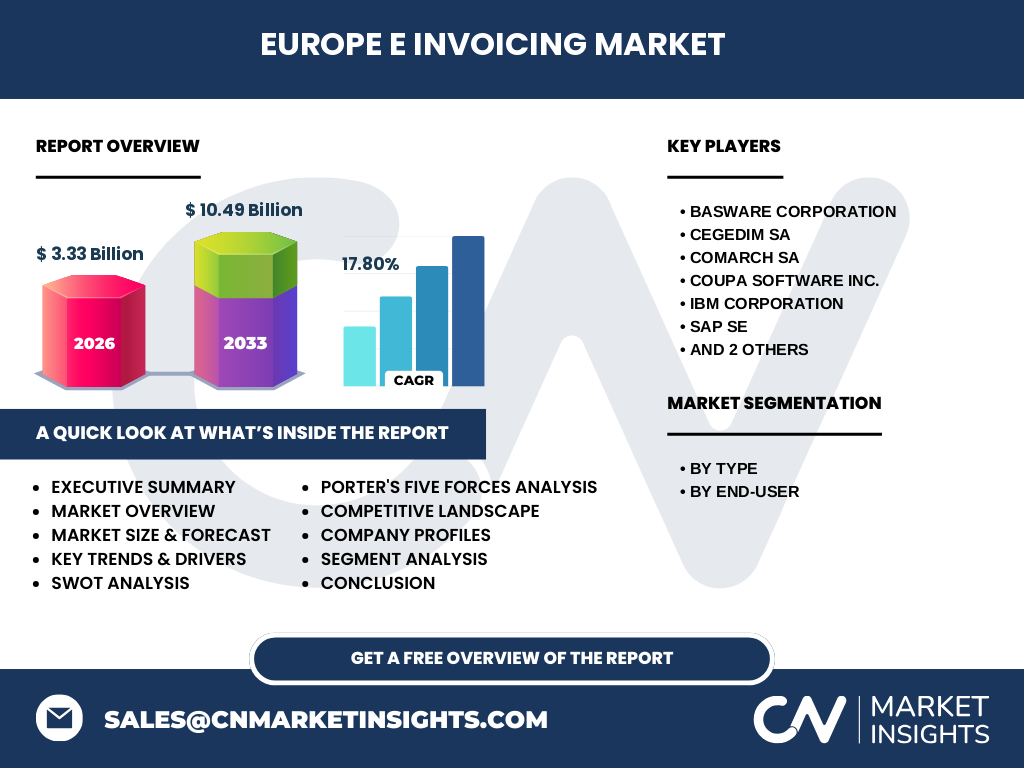

6. Executive Summary – High‑level overview and key findings about Europe E‑Invoicing Market?

The Europe E‑Invoicing market is projected to expand from a 2026 valuation of €3.33 billion to €10.49 billion by 2033, reflecting a robust CAGR of 17.8 %. Growth is underpinned by regulatory mandates, digital transformation initiatives, and cloud adoption. While integration hurdles persist, the market presents strong opportunities for vendors offering compliant, AI‑enhanced, and interoperable solutions across B2B and B2C segments.

7. Europe E‑Invoicing Market Forecast – Projections for 2025‑2032 period?

Building on the provided CAGR of 17.8 %, the market is expected to maintain a high‑growth trajectory throughout 2025‑2032. This sustained expansion will be driven by continued regulatory alignment, increased cross‑border e‑commerce, and the scaling of cloud infrastructures. Vendors that can deliver secure, scalable, and standards‑compliant platforms are poised to capture sizeable market share.

8. Europe E‑Invoicing Market Size and Share by Segmentation – Breakdown by segment?

Segmentation by type divides the market into cloud and on‑premise solutions, with cloud gaining momentum due to lower total cost of ownership and rapid deployment capabilities. By end‑user, the B2B segment dominates, reflecting extensive invoicing volumes in supply‑chain networks, while B2C is growing as e‑commerce expands across Europe. Precise share numbers are proprietary, but the trend clearly favors cloud‑based B2B offerings.

9. Global Europe E‑Invoicing Market Size and Share by Region – Geographic distribution?

Within the global e‑invoicing landscape, Europe represents a mature and rapidly expanding region. The 2026 market size of €3.33 billion and the forecasted €10.49 billion by 2033 illustrate Europe’s strong contribution to worldwide growth, driven by harmonized regulations and high digital adoption rates across member states.

10. Regional Analysis of the Europe E‑Invoicing Market – Detailed regional market performance?

Key sub‑regional drivers include stringent e‑invoicing mandates in countries such as Italy, France, and Germany, which act as catalysts for adoption. Northern Europe benefits from advanced fintech ecosystems, while Eastern European markets exhibit rising uptake as SMEs transition from paper to digital invoicing. Each region’s performance aligns closely with national policy frameworks and the maturity of IT infrastructure.

11. Leading Company Profiles in the Europe E‑Invoicing Market – Industry players and strategies?

Basware Corporation focuses on end‑to‑end network solutions and deep integration with ERP systems. Cegedim SA leverages its healthcare expertise to tailor invoicing for regulated sectors. Comarch SA offers modular platforms for SMEs. Coupa Software Inc. combines procurement and invoicing for spend management. IBM Corporation emphasizes AI‑driven automation, while SAP SE provides robust enterprise‑grade suites. The Sage Group plc targets small‑and‑medium businesses with cloud‑first tools, and Tradeshift builds open marketplaces for B2B transactions.

12. Porter's Five Forces Analysis of the Europe E‑Invoicing Market – Competitive forces assessment?

Threat of new entrants is moderate; high regulatory compliance creates barriers, yet cloud technology lowers entry costs. Bargaining power of buyers is growing as companies demand flexible, interoperable solutions. Bargaining power of suppliers is limited, given the availability of multiple technology stacks. Threat of substitutes remains low because paper invoicing is increasingly obsolete. Rivalry among existing firms is intense, driving innovation and pricing competition.

13. SWOT Analysis of the Europe E‑Invoicing Market – Strengths, weaknesses, opportunities, threats?

Strengths: Strong regulatory support, high cost‑saving potential, and mature digital infrastructure. Weaknesses: Integration complexity with legacy ERP systems. Opportunities: Expansion of AI‑based validation, blockchain verification, and cross‑border standardization. Threats: Data‑privacy regulations, cybersecurity risks, and potential market saturation in mature economies.

14. Europe E‑Invoicing Market Value Chain Analysis – Industry structure and value flow?

The value chain begins with software developers creating invoicing platforms, followed by system integrators customizing solutions for end‑users. Cloud service providers deliver hosting, while financial institutions enable electronic payment linkages. End‑users generate, transmit, and reconcile invoices, closing the loop with auditors and regulators who verify compliance. Each stage creates added value through automation, security, and analytics.

15. Key Investment Insights in the Europe E‑Invoicing Market – Strategic investment recommendations?

Investors should prioritize companies with cloud‑native architectures, strong API ecosystems, and proven compliance capabilities. Partnerships with ERP vendors and fintech firms enhance market reach. Acquisitions targeting niche AI or blockchain capabilities can accelerate differentiation. Given the 17.8 % CAGR, long‑term capital allocation to scalable, regulated‑ready platforms is likely to yield attractive returns.

16. Europe E‑Invoicing Market Conclusion – Summary and key takeaways?

The Europe E‑Invoicing market is on a pronounced growth path, propelled by regulatory mandates, cost efficiencies, and digital transformation. With a forecasted expansion to €10.49 billion by 2033, the sector offers substantial opportunities for vendors that can navigate integration challenges and deliver secure, AI‑enhanced, cloud‑first solutions across B2B and B2C segments.

17. Research Methodology – How this research was conducted?

The study employed a mixed‑method approach, combining secondary data collection from industry reports, regulatory publications, and company filings with primary insights obtained through interviews with market participants and experts. Data triangulation ensured accuracy, while trend extrapolation used the provided CAGR of 17.8 % to model future market size.

18. Research Scope – Coverage and limitations?

The scope covers the European e‑invoicing ecosystem, segmented by solution type (cloud, on‑premise) and end‑user (B2B, B2C). Geographic focus includes major EU economies and emerging markets within Europe. The analysis does not extend to non‑European regions, and financial figures are limited to the provided market size, forecast, and growth rate.

19. Key Companies and Recent Developments in the Europe E‑Invoicing Market – Introduction to top companies and their recent announcements, product launches, partnerships, and strategic developments?

Basware Corporation recently launched an AI‑driven invoice matching module, enhancing automation for large enterprises. Cegedim SA announced a partnership with a leading French health insurer to streamline medical invoicing. Comarch SA introduced a modular SaaS offering targeting SMEs. Coupa Software Inc. expanded its procurement‑invoicing integration across the EU. IBM Corporation unveiled a cloud‑based blockchain verification service for high‑value invoices. SAP SE released an upgraded SAP S/4HANA finance suite with embedded e‑invoicing compliance. The Sage Group plc rolled out a new subscription model for its cloud invoicing product, and Tradeshift secured a strategic alliance with a major logistics provider to create an end‑to‑end B2B transaction network.