What is the Bacon Market Overview – definition, scope, and significance?

The Bacon Market encompasses the production, processing, distribution, and consumption of cured pork and alternative‑source bacon products worldwide. It includes all major curing methods—dry cured, immersion cured, and pumped bacon—as well as variations by nature (organic versus conventional) and source (pork, beef, turkey, chicken). The market serves multiple channels, from supermarkets and hypermarkets to independent retailers and food‑service establishments. Bacon remains a staple protein in many cuisines, contributing to dietary protein intake and generating substantial revenue; its 2026 market size of $36.77 billion underscores its economic importance and the breadth of consumer demand across regions.

What are the Bacon Market Drivers, Restraints, Challenges, and Opportunities?

Key drivers include rising consumer preference for convenient, ready‑to‑cook protein, expanding food‑service channels, and growing demand for organic and specialty bacon varieties. Health‑conscious trends create opportunities for low‑sodium and nitrate‑free products. Restraints stem from health concerns over processed meat consumption, regulatory scrutiny on additives, and price volatility of raw meat supplies. Challenges involve supply‑chain disruptions, especially for pork, and competition from plant‑based alternatives. Opportunities arise from product innovation (flavor infusions, hybrid meat‑plant blends), geographic expansion into emerging markets, and premiumization of organic and sustainably sourced bacon.

What are the current Bacon Market Growth Trends?

Recent trends show a shift toward premium and organic bacon, driven by consumer willingness to pay more for perceived health and sustainability benefits. Flavor experimentation—such as smoked maple, pepper‑crusted, and spice‑rubbed varieties—is gaining traction. The food‑service sector is increasingly incorporating bacon into menu items beyond breakfast, including salads, burgers, and desserts, boosting overall demand. Additionally, manufacturers are adopting advanced curing technologies that enhance shelf life while reducing sodium and nitrite content, aligning with health‑focused market expectations.

How has COVID‑19 impacted the Bacon Market and what is the recovery trajectory?

The pandemic caused short‑term disruptions in supply chains and reduced food‑service sales due to lockdowns, leading to a temporary dip in volume. However, home‑cooking surged, offsetting losses as consumers stocked up on convenient protein options, including bacon. Post‑pandemic, the market has rebounded strongly, with retail channels stabilizing and food‑service demand resurging. The recovery is supported by continued consumer interest in comfort foods and the market’s projected CAGR of 4.26 % through 2033, indicating sustained growth beyond the pandemic period.

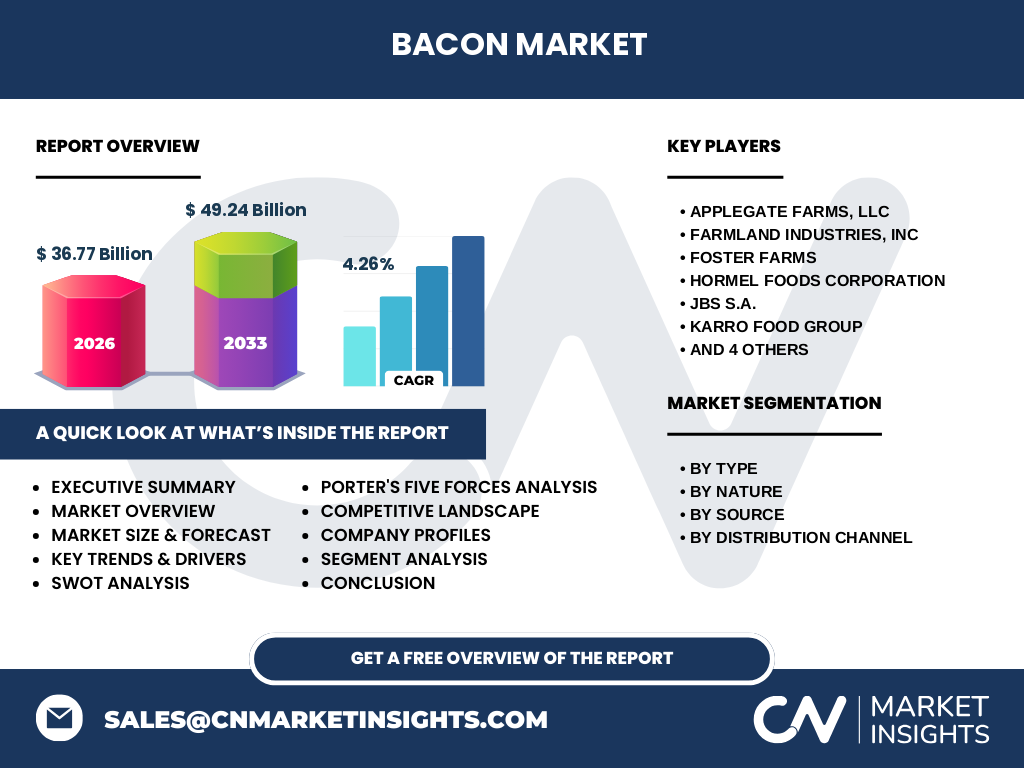

Who are the major competitors in the Bacon Market and what is the level of market consolidation?

Key competitors include Applegate Farms, LLC; Farmland Industries, Inc; Foster Farms; Hormone Foods Corporation; JBS S.A.; Karro Food Group; OSI Group; Organic Prairie; Smithfield Foods, Inc; and True Story Foods. The market exhibits moderate consolidation, with several large integrated meat processors holding significant production capacity, while niche players focus on organic and specialty segments. Strategic partnerships and acquisitions are common as firms aim to broaden product portfolios and expand distribution reach.

What does the Executive Summary reveal about the Bacon Market?

The Bacon Market is valued at $36.77 billion in 2026 and is projected to reach $49.24 billion by 2033, reflecting a robust CAGR of 4.26 %. Growth is driven by consumer demand for convenience, premium and organic offerings, and expanding food‑service applications. While health concerns and raw material price volatility present challenges, innovative curing techniques and product diversification create substantial opportunities. The competitive landscape is characterized by a mix of large processors and specialty brands, with ongoing consolidation through strategic alliances.

What are the forecast expectations for the Bacon Market from 2025 to 2032?

Based on the stated CAGR of 4.26 %, the market is expected to maintain steady expansion, moving from the 2026 base of $36.77 billion to approximately $49.24 billion by the end of the forecast horizon in 2033. This trajectory suggests consistent annual growth, driven by rising consumption across retail and food‑service channels, and increasing market penetration of organic and alternative‑source bacon products.

How is the Bacon Market sized and shared by segmentation?

Segmentation occurs across four primary dimensions:

By Type: Dry cured, immersion cured, and pumped bacon each address distinct processing preferences, with dry cured maintaining traditional flavor profiles, immersion cured offering rapid production cycles, and pumped bacon delivering uniform salt distribution.

By Nature: Organic bacon commands a premium niche, appealing to health‑conscious consumers, while conventional bacon dominates the mainstream volume market.

By Source: Pork remains the core source, but beef, turkey, and chicken bacon provide alternative options for dietary restrictions and flavor diversity.

By Distribution Channel: Supermarkets and hypermarkets capture the majority of retail sales; independent retailers serve localized markets; and the food‑service channel drives bulk and specialty usage.

What is the global Bacon Market size and share by region?

The global market totals $36.77 billion in 2026, with sales distributed across North America, Europe, Asia‑Pacific, Latin America, and the Middle East & Africa. While exact regional monetary shares are not disclosed, each region contributes to the aggregate size through its unique consumption patterns, regulatory environments, and distribution networks.

What does the regional analysis of the Bacon Market reveal?

North America leads consumption due to strong breakfast traditions and extensive retail infrastructure. Europe follows, with growing interest in organic and specialty bacon. Asia‑Pacific presents emerging growth opportunities as Western dietary habits spread and local producers adopt curing technologies. Latin America shows steady demand driven by pork production capacity, whereas the Middle East & Africa exhibit niche growth linked to expatriate communities and evolving retail formats.

What are the leading company profiles in the Bacon Market and their strategies?

Applegate Farms, LLC focuses on organic and natural bacon, leveraging clean‑label positioning. Farmland Industries, Inc emphasizes scale and vertical integration to control costs. Foster Farms expands its poultry‑based bacon line to capture alternative‑source demand. Hormel Foods Corporation invests in flavor innovation and convenient packaging. JBS S.A. utilizes global sourcing to optimize supply. Karro Food Group targets niche markets with artisanal products. OSI Group serves food‑service customers with bulk solutions. Organic Prairie concentrates on certified organic offerings. Smithfield Foods, Inc leverages its pork dominance for volume leadership. True Story Foods explores plant‑forward bacon alternatives.

How does Porter’s Five Forces analysis apply to the Bacon Market?

Threat of new entrants is moderate; high capital requirements and strict food safety regulations create barriers, though niche organic brands can enter more easily.

Bargaining power of suppliers is relatively high due to reliance on pork and alternative meats, which are subject to price fluctuations.

Bargaining power of buyers is moderate; large retailers negotiate pricing, but consumer brand loyalty to premium or organic bacon can reduce price sensitivity.

Threat of substitutes is growing, with plant‑based bacon and other processed meats offering alternatives.

Industry rivalry is intense, driven by product differentiation, price competition, and marketing of health‑focused attributes.

What are the SWOT insights for the Bacon Market?

Strengths: Established consumer base, versatile product applications, and strong profitability of premium segments.

Weaknesses: Perceived health risks, dependency on pork supply, and limited differentiation for conventional products.

Opportunities: Expansion of organic and alternative‑source bacon, flavor innovation, and penetration into emerging markets.

Threats: Rising regulatory scrutiny, competition from plant‑based proteins, and raw material price volatility.

What does the Bacon Market value chain look like?

The value chain starts with animal farming (pork, beef, turkey, chicken), proceeds to meat processing where curing methods (dry, immersion, pumped) are applied, followed by packaging and labeling (including organic certification). Distribution follows through wholesalers to retail channels—supermarkets, independent stores, and food‑service providers. End consumers purchase the product for home cooking or dining‑out consumption. Supporting activities include R&D for curing technology, quality assurance, and marketing.

What key investment insights can be drawn for the Bacon Market?

Investors should consider companies with strong organic or specialty portfolios, as these segments command higher margins and exhibit robust growth. Firms that own integrated supply chains can mitigate raw‑material cost risks, enhancing profitability. Partnerships with food‑service distributors expand volume sales. Monitoring regulatory developments and consumer health trends will be critical for risk assessment. Overall, the projected CAGR of 4.26 % and a sizable market base present attractive long‑term opportunities.

What is the conclusion of the Bacon Market report?

The Bacon Market demonstrates solid growth potential, anchored by a $36.77 billion base in 2026 and a forecasted rise to $49.24 billion by 2033. Consumer demand for convenience, premium, and organic options fuels expansion, while health concerns and raw material volatility pose challenges. Strategic innovation, supply‑chain integration, and geographic diversification emerge as key levers for sustained success.

What research methodology was used for this report?

The analysis combines primary interviews with industry executives, secondary data from trade publications, company financials, and market databases. Quantitative data were validated through cross‑referencing, and qualitative insights were derived from trend monitoring and expert opinion. Forecast modeling applied a compound annual growth rate of 4.26 % to project future market size.

What is the scope of the research?

The study covers global bacon production, processing, and distribution across all major regions, examining product types, nature, source, and channel segmentation. It includes competitive profiling of leading firms, market dynamics, and forecasts through 2033. The scope excludes detailed pricing analysis and country‑level market shares beyond the provided aggregate figures.

Which key companies and recent developments are highlighted in the Bacon Market?

Leading firms—Applegate Farms, Farmland Industries, Foster Farms, Hormel Foods, JBS S.A., Karro Food Group, OSI Group, Organic Prairie, Smithfield Foods, and True Story Foods—have launched new organic lines, expanded plant‑based bacon alternatives, and formed strategic partnerships with retail and food‑service distributors. Recent developments include product launches focusing on low‑sodium cured bacon, investment in sustainable packaging, and acquisitions aimed at strengthening presence in the premium and alternative‑source segments.