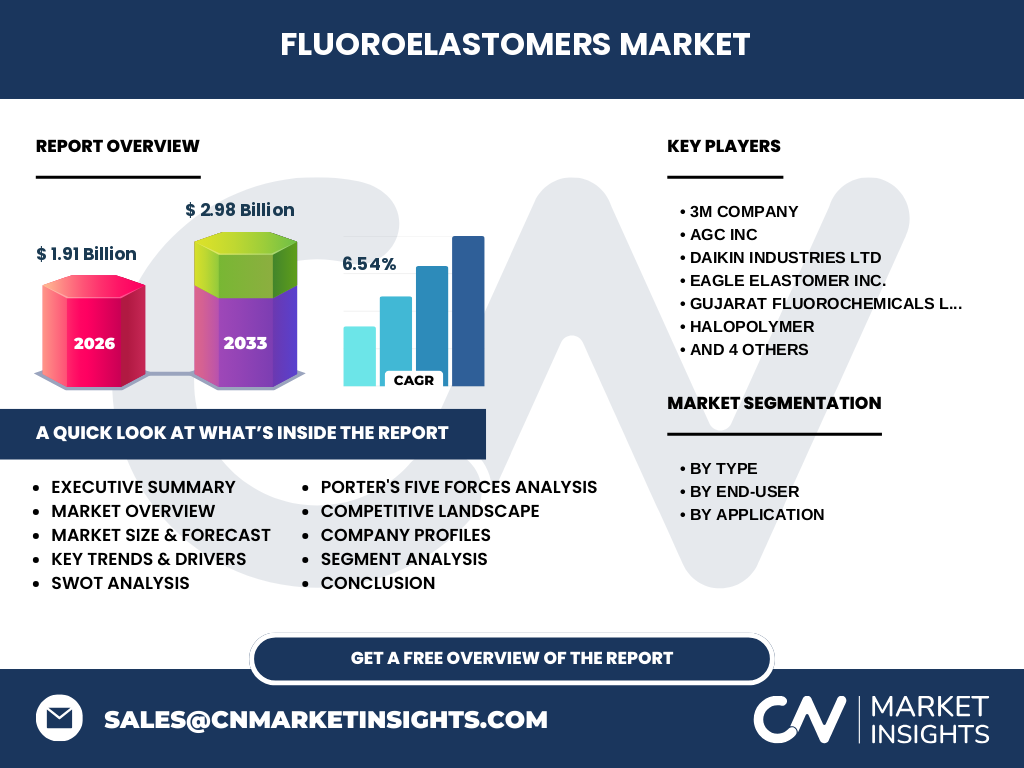

What is the Fluoroelastomers Market Overview, including its definition, scope, and significance?

The fluoroelastomers market encompasses high-performance synthetic rubbers characterized by exceptional heat, chemical, and oil resistance. These fluorinated polymers serve critical sealing and component roles across demanding industries. The market scope covers fluorocarbon elastomers, fluorosilicone elastomers, and perfluorocarbon elastomers, with applications spanning O-rings, seals, gaskets, hoses, and molded parts. Significance stems from irreplaceability in extreme environments — automotive fuel systems, aerospace hydraulics, oil & gas downhole tools, semiconductor processing, and energy infrastructure — where conventional elastomers fail. Market size reached 1.91 Billion in 2026, reflecting strong industrial demand.

What are the key drivers, restraints, challenges, and opportunities in the Fluoroelastomers Market?

Key drivers include stringent emissions regulations mandating advanced sealing in automotive and aerospace, expanding semiconductor fabrication requiring ultra-clean perfluorocarbon elastomers, and growing oil & gas exploration in harsh environments. Restraints involve high raw material costs (fluorine chemistry), complex manufacturing, and limited supplier base. Challenges encompass PFAS regulatory scrutiny potentially restricting certain grades, recycling difficulties, and substitute development. Opportunities lie in next-generation low-friction formulations, hydrogen economy sealing solutions, electric vehicle thermal management, and emerging economies' industrialization. The 6.54% CAGR through 2033 reflects these dynamics balancing growth against regulatory headwinds.

What current and emerging trends are shaping the Fluoroelastomers Market growth trajectory?

Current trends feature shifting demand toward perfluorocarbon elastomers for semiconductor plasma resistance, increasing fluorosilicone adoption in aerospace fuel systems for low-temperature flexibility, and automotive transition to FKM grades compatible with biofuels and electric drivetrain fluids. Emerging trends include development of PFAS-compliant fluorine-free alternatives, nano-reinforced composites for extended seal life, additive manufacturing of custom fluoroelastomer parts, and circular economy initiatives for post-industrial recycling. Regional production localization in Asia-Pacific, particularly China and India, is reshaping supply chains as Gujarat Fluorochemicals and Shandong Huaxia expand capacity.

How did COVID-19 impact the Fluoroelastomers Market and what is the recovery trajectory?

COVID-19 caused acute disruption in 2020 — automotive shutdowns slashed O-ring and seal demand, aerospace order cancellations reduced fluorosilicone consumption, and oil & gas capital expenditure cuts deferred projects. Semiconductor demand proved resilient, supporting perfluorocarbon grades. Recovery followed a K-shape: semiconductor and energy sectors rebounded rapidly by late 2020, automotive recovered through 2021 with pent-up demand, while aerospace lagged until 2022-2023. Supply chain reorganization post-pandemic accelerated dual-sourcing strategies, benefiting established players like Chemours, Daikin, and Solvay with qualified supply chains. The market has surpassed pre-pandemic levels, tracking toward the 2.98 Billion forecast for 2033.

What defines the competitive landscape and market consolidation in the Fluoroelastomers Market?

The fluoroelastomers market exhibits high consolidation among top-tier fluorine chemistry specialists. Ten major companies dominate: 3M Company, AGC Inc, Daikin Industries Ltd, Eagle Elastomer Inc., Gujarat Fluorochemicals Ltd, HaloPolymer, Shandong Huaxia Shenzhou New Material Co Ltd, Shin-Etsu Chemical Co Ltd, Solvay SA, and The Chemours Co. These firms control proprietary monomer synthesis, polymer production, and compounding — creating high entry barriers. Consolidation trends include vertical integration (Daikin, Chemours), geographic expansion (AGC, Solvay in Asia), and strategic partnerships for next-gen formulations. Regional players like Gujarat Fluorochemicals and Shandong Huaxia are gaining share through cost-competitive perfluorocarbon and fluorocarbon grades.

What are the key findings and high-level overview from the Fluoroelastomers Market Executive Summary?

The fluoroelastomers market demonstrates robust fundamentals with 1.91 Billion valuation in 2026, projected to reach 2.98 Billion by 2033 at 6.54% CAGR. Three-type segmentation — fluorocarbon, fluorosilicone, perfluorocarbon — serves five end-users: automotive, aerospace, oil & gas, semiconductors, energy & power. Applications concentrate in O-rings, seals/gaskets, hoses, and molded parts. Asia-Pacific leads growth driven by semiconductor fabs, automotive production, and chemical industry expansion. Regulatory pressure on PFAS compounds creates both risk and innovation catalyst. Top ten companies maintain technology moats through integrated fluorine value chains. Investment thesis centers on irreplaceable performance in extreme environments and secular demand from electrification and advanced manufacturing.

What are the Fluoroelastomers Market projections for the 2025-2032 forecast period?

Market forecast projects growth from 1.91 Billion in 2026 to 2.98 Billion by 2033, representing 6.54% compound annual growth rate. The 2025-2032 period captures accelerating demand from semiconductor capacity expansions (perfluorocarbon elastomers), electric vehicle platform launches requiring specialized FKM grades (fluorocarbon elastomers), and hydrogen infrastructure development (fluorosilicone elastomers). Regional growth differentials favor Asia-Pacific at above-average CAGR, while North America and Europe track near global average with premium-grade concentration. Oil & gas cyclical recovery adds upside potential. Forecast assumes continued PFAS regulatory adaptation rather than blanket restrictions, allowing product portfolio evolution.

How does the Fluoroelastomers Market break down by segmentation including type, end-user, and application?

Market segmentation by type comprises fluorocarbon elastomers (largest volume, automotive/aerospace seals), fluorosilicone elastomers (aerospace fuel systems, low-temp flexibility), and perfluorocarbon elastomers (highest value, semiconductor/chemical processing). By end-user: automotive leads volume (fuel systems, transmissions), aerospace demands highest specifications (fluorosilicone/perfluorocarbon), oil & gas requires sour-gas resistance, semiconductors drive perfluorocarbon growth, energy & power includes nuclear and hydrogen applications. By application: O-rings dominate unit volume across all sectors, seals and gaskets represent largest revenue share, hoses critical for automotive/aerospace fluid transfer, molded parts growing with custom engineering solutions. Each segment exhibits distinct pricing, regulation, and growth dynamics.

What is the global Fluoroelastomers Market size and share distribution by geographic region?

Global fluoroelastomers market size reached 1.91 Billion in 2026, with geographic distribution reflecting industrial concentration. Asia-Pacific commands largest share driven by China's semiconductor fabrication expansion, automotive manufacturing hub, and growing fluorochemical production (Gujarat Fluorochemicals, Shandong Huaxia). North America holds significant share through established aerospace, oil & gas, and semiconductor sectors with Chemours, 3M, and Daikin manufacturing presence. Europe maintains strong position via automotive OEM demand, chemical processing, and stringent emissions standards served by Solvay and AGC. Rest of World includes emerging Middle East oil & gas demand and Latin America automotive growth. Regional shares shift toward Asia-Pacific through 2033 forecast period.

How does regional analysis detail the Fluoroelastomers Market performance across key geographies?

North America: mature market with high perfluorocarbon penetration in semiconductors, aerospace MRO demand, and PFAS regulatory leadership shaping product roadmaps. Europe: automotive-driven fluorocarbon demand, REACH compliance accelerating sustainable formulations, strong Solvay/AGC production base. Asia-Pacific: fastest growth from China's semiconductor self-sufficiency push, India's chemical industry expansion (Gujarat Fluorochemicals), Japan's advanced materials innovation (Daikin, Shin-Etsu), South Korea's chip fabrication. Middle East: oil & gas downstream investment drives sour-service elastomer demand. Latin America: automotive assembly growth in Mexico/Brazil supports fluorocarbon consumption. Each region exhibits distinct regulatory, supply chain, and end-user dynamics affecting grade selection and pricing.

Who are the leading company profiles in the Fluoroelastomers Market and what are their strategies?

Top ten companies define competitive strategy: Chemours (Viton™ portfolio, vertical integration, PFAS transition leadership), Daikin Industries (Dai-El™, integrated fluorine monomer-to-polymer, Asia-Pacific expansion), Solvay (Tecnoflon®, specialty grades, European stronghold), 3M (Dyneon™, broad fluoropolymer platform, divestiture focus), AGC (Aflas®, unique TFE/propylene grades, automotive focus), Shin-Etsu (semiconductor-grade perfluorocarbon, high-purity specialization), Gujarat Fluorochemicals (cost-competitive fluorocarbon/perfluorocarbon, backward integration), HaloPolymer (Russian fluorochemical leader, export-oriented), Eagle Elastomer (Viton™ licensee, North American compounding), Shandong Huaxia (emerging Chinese scale player, government-supported capacity). Strategies center on specialty grade differentiation, supply chain security, and regulatory adaptation.

What does Porter's Five Forces Analysis reveal about the Fluoroelastomers Market competitive forces?

Threat of new entrants: Very high barriers — fluorine chemistry complexity, capital intensity, regulatory qualifications, and established customer qualifications protect incumbents. Bargaining power of suppliers: Moderate — fluorspar and HF supply concentrated but major producers vertically integrated. Bargaining power of buyers: Moderate to high — large OEMs (automotive, aerospace, semiconductor) qualify specific grades but face switching costs. Threat of substitutes: Low for extreme environments — silicone, EPDM, HNBR fail at temperature/chemical extremes; emerging fluorine-free alternatives target niche applications only. Competitive rivalry: High among top ten — differentiated by grade portfolio, technical service, geographic reach, and regulatory readiness rather than price alone. Industry structure favors established integrated players.

What are the Strengths, Weaknesses, Opportunities, and Threats in the Fluoroelastomers Market SWOT Analysis?

Strengths: Irreplaceable performance in extreme conditions, high customer switching costs, integrated value chains of major players, growing semiconductor/energy demand. Weaknesses: High production costs, PFAS regulatory exposure, limited recycling infrastructure, concentrated supplier base. Opportunities: Electric vehicle thermal management seals, hydrogen economy infrastructure, PFAS-compliant next-gen formulations, additive manufacturing enablement, Asia-Pacific capacity localization. Threats: Expanding PFAS restrictions (EU, US EPA), economic cyclicality in oil & gas/auto, substitute development for moderate environments, geopolitical supply chain risks (fluorspar concentration), raw material cost volatility. Strategic imperative: innovate toward sustainable fluorine chemistry while defending core extreme-environment franchises.

How does the Fluoroelastomers Market Value Chain Analysis describe industry structure and value flow?

Value chain flows from fluorspar mining → hydrogen fluoride (HF) production → fluorinated monomers (VF2, TFE, PMVE) → polymer synthesis (fluorocarbon, fluorosilicone, perfluorocarbon) → compounding (curatives, fillers, process aids) → molding/extrusion → OEM integration. Major players (Chemours, Daikin, Solvay, AGC, 3M, Shin-Etsu) integrate backward to monomer/polymer stages, capturing disproportionate value. Compounding and molding represent fragmented midstream with specialized processors. End-users (automotive Tier 1s, aerospace OEMs, semiconductor fabs) drive specifications and qualifications. Value concentration upstream creates pricing power for integrated producers; downstream fragmentation enables technical service differentiation. Emerging Asian integration (Gujarat, Shandong Huaxia) reshapes geographic value distribution.

What are the key investment insights and strategic recommendations for the Fluoroelastomers Market?

Priority investment areas: perfluorocarbon elastomer capacity for semiconductor node scaling (highest margin, stickiest demand), PFAS-compliant fluorocarbon platform development (regulatory hedge, automotive retention), fluorosilicone expansion for aerospace/hydrogen (growth niche, technical barriers), Asia-Pacific production localization (cost advantage, supply security). M&A targets: specialty compounders with OEM qualifications, fluorine monomer producers for vertical integration, recycling technology startups. Risk mitigation: diversify fluorspar sourcing, invest in fluorine-free alternative R&D, engage proactively in PFAS regulatory frameworks. Financial metrics support premium valuations for integrated specialty players vs. commodity fluorocarbon producers. Long-term thesis: irreplaceability in decarbonization technologies (EVs, hydrogen, nuclear) sustains pricing power.

What are the summary conclusions and key takeaways from the Fluoroelastomers Market analysis?

The fluoroelastomers market exhibits resilient 6.54% CAGR growth from 1.91 Billion (2026) to 2.98 Billion (2033), driven by structural demand from semiconductors, electrification, and energy transition. Three-type segmentation serves distinct performance-economics tiers. Competitive landscape favors ten integrated fluorine chemistry leaders with high entry barriers. Critical inflection point: PFAS regulation will reshape product portfolios but not eliminate extreme-environment demand. Asia-Pacific production shift accelerates. Investment winners will combine regulatory agility, technical service depth, and geographic balance. Market requires monitoring of fluorochemical expertise — not a commodity play. Stakeholders should prioritize perfluorocarbon exposure, PFAS transition readiness, and Asian supply chain positioning.

What research methodology was employed to conduct this Fluoroelastomers Market analysis?

Research methodology combines primary and secondary approaches. Primary research includes structured interviews with fluoroelastomer producers (Chemours, Daikin, Solvay, AGC, Gujarat Fluorochemicals), compounders, OEM procurement managers (automotive, aerospace, semiconductor), and regulatory experts. Secondary research encompasses company financial filings, patent landscapes, trade association data (ASTM D1418, ISO 1629), government regulatory dockets (EPA PFAS roadmap, ECHA restriction proposals), customs import/export statistics, and technical literature. Market sizing employs bottom-up capacity modeling cross-referenced with top-down demand estimation by end-user sector. Forecasting incorporates scenario analysis for PFAS regulatory outcomes. Data triangulation ensures consistency across sources. Analysis period covers 2020-2033 with 2026 base year.

What is the research scope and coverage limitations for this Fluoroelastomers Market report?

Research scope covers global fluoroelastomers market across three type segments (fluorocarbon, fluorosilicone, perfluorocarbon elastomers), five end-user sectors (automotive, aerospace, oil & gas, semiconductors, energy & power), and four application categories (O-rings, seals/gaskets, hoses, molded parts). Geographic coverage includes North America, Europe, Asia-Pacific, Middle East, Latin America. Ten key companies profiled. Time horizon: 2020-2033 with 2026 base year and 2027-2033 forecast. Limitations: excludes fluoropolymer thermoplastics (PTFE, PFA, FEP), fluoroelastomer adhesives/coatings, and non-sealing applications. Does not quantify PFAS regulatory impact scenarios. Regional shares estimated from production capacity and trade data. Company financials limited to public disclosures.

Who are the key companies and what recent developments shape the Fluoroelastomers Market landscape?

Ten key companies drive market developments: Chemours advancing Viton™ FreeFlow™ extrusion grades and PFAS transition roadmap; Daikin expanding Dai-El™ production in China and developing low-friction FKM for EV thermal management; Solvay launching Tecnoflon® peroxide-curable grades for hydrogen sealing; 3M progressing PFAS exit timeline while maintaining Dyneon™ supply; AGC commercializing Aflas® TFE/propylene for sour gas; Shin-Etsu qualifying ultra-high-purity perfluorocarbon for sub-3nm semiconductor nodes; Gujarat Fluorochemicals commissioning integrated fluorocarbon/perfluorocarbon capacity in India; HaloPolymer modernizing Russian fluorochemical assets for export; Eagle Elastomer expanding North American compounding for aerospace MRO; Shandong Huaxia scaling Chinese fluorocarbon output with government support. Recent partnerships focus on recycling pilots and fluorine-free alternative co-development.