What is the Operational Technology Market and why is it significant?

The Operational Technology (OT) Market encompasses hardware, software, and services that monitor, control, and automate industrial processes across critical infrastructure sectors. Unlike Information Technology (IT) which manages data, OT directly interacts with physical equipment and processes in real-time. The market's significance lies in its role as the backbone of industrial operations, enabling efficiency, safety, and reliability in sectors such as energy, manufacturing, transportation, and building automation. With a projected market size of 178.65 Billion in 2026 growing to 337.91 Billion by 2033 at a 9.53% CAGR, OT represents a critical investment area for industrial digital transformation and Industry 4.0 initiatives.

What are the key drivers, restraints, challenges, and opportunities in the Operational Technology Market?

Key drivers include accelerating Industry 4.0 adoption, increasing demand for operational efficiency, and growing convergence of IT and OT systems. The 9.53% CAGR reflects strong momentum from predictive maintenance, real-time monitoring, and automation needs across verticals. Restraints involve legacy system integration complexities, cybersecurity vulnerabilities in connected environments, and high initial capital expenditure. Challenges include skilled workforce shortages, regulatory compliance variations across regions, and interoperability standards gaps. Opportunities emerge from edge computing adoption, AI-driven analytics, cloud-OT integration, and expanding applications in building automation and transportation sectors where digital twin technology and remote operations capabilities are gaining traction.

What current and emerging trends are shaping the Operational Technology Market growth?

The market is experiencing transformative trends including IT-OT convergence enabling unified data analytics, edge computing deployment for low-latency decision making, and AI/ML integration for predictive maintenance and process optimization. Cybersecurity mesh architectures are becoming essential as attack surfaces expand. Digital twin technology adoption accelerates across manufacturing and energy verticals. The 9.53% CAGR through 2033 reflects growing demand for wireless sensor networks, 5G-enabled industrial connectivity, and software-defined automation. Sustainability-driven investments in energy efficiency and emissions monitoring create new OT application areas. Vendor consolidation and platform-based solutions are reshaping competitive dynamics as end-users seek integrated rather than point solutions.

How did COVID-19 impact the Operational Technology Market and what is the recovery trajectory?

COVID-19 initially disrupted OT supply chains and delayed capital projects across energy, manufacturing, and transportation sectors. However, the pandemic accelerated digital transformation urgency, driving remote monitoring and operations capabilities adoption. Companies prioritized OT investments enabling workforce reduction on-site while maintaining operational continuity. The recovery trajectory shows strong V-shaped rebound with accelerated IT-OT convergence projects. The forecast of 337.91 Billion by 2033 at 9.53% CAGR reflects post-pandemic resilience investment cycles. Key recovery drivers include supply chain resilience requirements, contactless operations mandates, and government infrastructure stimulus packages prioritizing industrial modernization and critical infrastructure security.

What defines the competitive landscape of the Operational Technology Market?

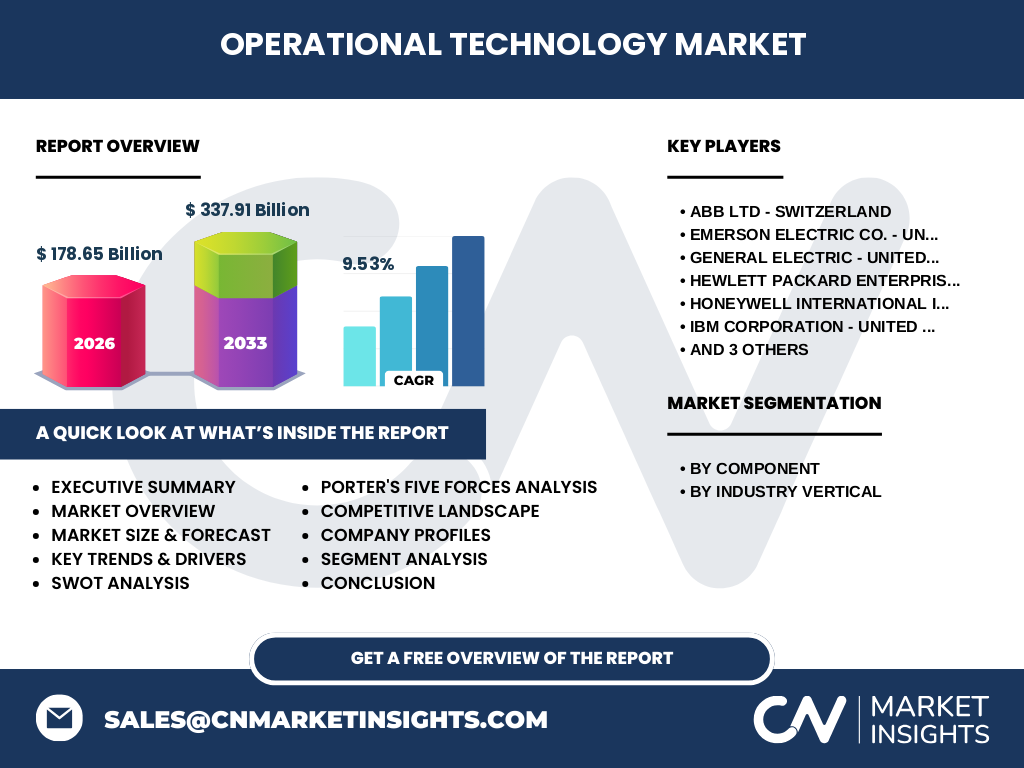

The competitive landscape features established industrial conglomerates and technology specialists. Major players include ABB Ltd (Switzerland), Emerson Electric Co. (US), General Electric (US), Hewlett Packard Enterprise (US), Honeywell International (US), IBM Corporation (US), NextNine Ltd. (Israel, a Honeywell Company), Siemens AG (Germany), and Wipro Limited (India). Market consolidation is evident through strategic acquisitions expanding portfolio breadth across hardware, software, and services segments. Competition centers on platform integration capabilities, cybersecurity offerings, vertical-specific domain expertise, and global service delivery networks. The 9.53% CAGR attracts new entrants in niche areas like edge analytics and OT security, while incumbents strengthen ecosystem partnerships to deliver end-to-end industrial digital transformation solutions.

What are the key findings and high-level overview of the Operational Technology Market?

The Operational Technology Market demonstrates robust growth trajectory from 178.65 Billion in 2026 to 337.91 Billion by 2033, driven by a 9.53% CAGR. Key findings reveal accelerating IT-OT convergence as the primary growth catalyst across all segments: Hardware, Software, and Services components, and Energy and Utilities, Manufacturing, Transportation, Building Automation, and Others verticals. Geographic expansion shows strong adoption in developed economies with emerging markets accelerating investments. Competitive dynamics favor integrated platform providers offering cybersecurity, edge computing, and vertical-specific applications. Strategic imperatives include addressing legacy modernization, workforce upskilling, and regulatory compliance while capturing sustainability-driven opportunities in energy efficiency and emissions monitoring.

What are the market projections for the Operational Technology Market from 2025 to 2032?

The Operational Technology Market is projected to grow from 178.65 Billion in 2026 to 337.91 Billion by 2033, representing a compound annual growth rate of 9.53%. This forecast period (2027-2033) reflects sustained demand across all component segments: Hardware investments in sensors, controllers, and edge devices; Software growth in SCADA, MES, historian, and analytics platforms; Services expansion in system integration, managed services, and cybersecurity consulting. Vertical growth drivers include Energy and Utilities grid modernization, Manufacturing smart factory initiatives, Transportation fleet and infrastructure monitoring, and Building Automation energy optimization. Regional variations will reflect industrial base maturity, digital infrastructure readiness, and government policy support for critical infrastructure modernization.

How is the Operational Technology Market segmented by component and industry vertical?

The market segmentation reveals distinct growth dynamics across components and verticals. By Component: Hardware encompasses industrial controllers, sensors, actuators, and network infrastructure; Software includes SCADA, DCS, MES, historian, and advanced analytics platforms; Services cover system integration, managed services, consulting, and cybersecurity. By Industry Vertical: Energy and Utilities drives demand through grid modernization and renewable integration; Manufacturing leads in smart factory and predictive maintenance adoption; Transportation invests in fleet management and infrastructure monitoring; Building Automation grows through energy efficiency and occupant safety systems; Others includes water/wastewater, oil/gas midstream, and discrete manufacturing. The 9.53% CAGR reflects balanced growth across segments with software and services outpacing hardware.

What is the geographic distribution of the Operational Technology Market globally?

The Operational Technology Market exhibits varied geographic adoption patterns aligned with industrial maturity and digital infrastructure development. Developed economies in North America and Europe lead in IT-OT convergence investments, driven by advanced manufacturing bases, stringent regulatory frameworks, and established vendor ecosystems. Asia-Pacific demonstrates accelerating growth through massive industrial modernization programs, smart city initiatives, and expanding manufacturing footprints. The Middle East and Africa show increasing investments in oil & gas digitalization and infrastructure development. Latin America exhibits growing adoption in mining, energy, and manufacturing sectors. The global forecast of 337.91 Billion by 2033 at 9.53% CAGR reflects broad-based geographic expansion with regional growth rates varying by industrial policy and digital readiness.

How does the Operational Technology Market perform across different regions?

Regional performance varies significantly based on industrial composition, regulatory environment, and digital maturity. North America leads in cybersecurity integration and cloud-OT platform adoption, driven by critical infrastructure protection mandates. Europe excels in sustainability-driven OT investments for energy transition and circular manufacturing. Asia-Pacific shows highest growth rates through government-led Industry 4.0 programs in China, Japan, South Korea, and India's manufacturing corridor development. Middle East focuses on oil & gas digital twin and remote operations capabilities. Each region's contribution to the 337.91 Billion forecast reflects local vertical strengths: Energy and Utilities dominance in Middle East, Manufacturing leadership in Asia-Pacific, Transportation innovation in Europe, and Building Automation growth in North America.

Who are the leading companies in the Operational Technology Market and what are their strategies?

The competitive landscape is anchored by nine major players pursuing distinct strategic positioning. ABB Ltd (Switzerland) focuses on robotics-electrification-OT integration. Emerson Electric (US) emphasizes measurement analytics and software portfolio expansion. General Electric (US) leverages Predix platform and aviation-power domain expertise. Hewlett Packard Enterprise (US) targets edge-to-cloud OT solutions. Honeywell International (US) combines building automation, process solutions, and cybersecurity through Forge platform. IBM Corporation (US) delivers Maximo asset management and hybrid cloud OT integration. NextNine Ltd. (Israel, Honeywell subsidiary) specializes in secure remote operations. Siemens AG (Germany) leads with Digital Industries portfolio and MindSphere IoT OS. Wipro Limited (India) provides system integration and managed services for global OT transformations.

What does Porter's Five Forces analysis reveal about the Operational Technology Market?

Porter's Five Forces analysis indicates moderate-to-high competitive intensity. Threat of new entrants is moderated by high domain expertise barriers, certification requirements, and established customer relationships, though niche software and cybersecurity startups find entry points. Supplier power remains balanced with multiple component providers but concentrated in specialized semiconductors and industrial software. Buyer power increases as large industrial enterprises demand integrated platforms over point solutions and leverage multi-vendor strategies. Threat of substitutes emerges from IT-centric cloud platforms extending to edge, though OT's real-time deterministic requirements create protective moats. Competitive rivalry is intense among the nine major players driving innovation in platform capabilities, vertical solutions, and service delivery models to capture the 9.53% CAGR growth.

What are the strengths, weaknesses, opportunities, and threats in the Operational Technology Market SWOT analysis?

Strengths include essential role in critical infrastructure, high switching costs creating customer retention, and expanding addressable market through IT-OT convergence. The 9.53% CAGR through 2033 reflects structural growth drivers. Weaknesses involve legacy system technical debt, cybersecurity vulnerabilities in brownfield environments, and skilled workforce shortages across OT domains. Opportunities encompass edge AI analytics, digital twin proliferation, sustainability-driven energy management, and 5G-enabled industrial connectivity. Emerging verticals like building automation and transportation offer greenfield deployment advantages. Threats include ransomware targeting industrial systems, geopolitical supply chain disruptions, regulatory fragmentation across jurisdictions, and potential economic cyclicality impacting capital expenditure cycles in energy and manufacturing verticals.

How does the Operational Technology Market value chain function and where is value created?

The OT value chain spans component suppliers (semiconductors, sensors, communication chips), hardware manufacturers (controllers, gateways, edge devices), software vendors (SCADA, MES, analytics platforms), system integrators (design, implementation, commissioning), managed service providers (monitoring, maintenance, optimization), and end-users across verticals. Value creation shifts toward software and services layers as hardware commoditizes. The 178.65 Billion to 337.91 Billion growth reflects increasing value capture in analytics, cybersecurity, and outcome-based service models. System integrators like Wipro and platform vendors like Siemens, Honeywell, and IBM orchestrate multi-vendor ecosystems. Strategic control points emerge at data aggregation layers where operational intelligence transforms into business outcomes across Energy, Manufacturing, Transportation, and Building Automation verticals.

What are the key investment insights for the Operational Technology Market?

Strategic investment priorities should target software platforms enabling IT-OT convergence, cybersecurity solutions for industrial control systems, and edge analytics capabilities. The 9.53% CAGR through 2033 supports sustained capital deployment. High-growth segments include cloud-OT integration platforms, digital twin software, and managed security services. Vertical-specific opportunities: Energy and Utilities grid modernization (DERMS, ADMS), Manufacturing MES and quality analytics, Transportation predictive maintenance, Building Automation energy optimization. Geographic allocation should weight Asia-Pacific growth capacity, North America cybersecurity maturity, Europe sustainability mandates. Risk mitigation requires addressing legacy integration complexity, talent acquisition, and regulatory compliance. M&A opportunities exist in niche OT security, edge AI, and vertical application vendors complementing platform strategies.

What are the key conclusions and takeaways from the Operational Technology Market analysis?

The Operational Technology Market represents a fundamental industrial transformation opportunity, growing from 178.65 Billion in 2026 to 337.91 Billion by 2033 at 9.53% CAGR. Critical takeaways: IT-OT convergence is the primary value driver across all segments and verticals. Cybersecurity becomes a differentiator, not just a requirement. Software and services outpace hardware in value capture. Vertical-specific domain expertise determines competitive success. Geographic strategies must align with regional industrial policies and digital maturity. Workforce development and legacy modernization remain persistent challenges. Sustainability mandates create new OT application domains. Platform ecosystems will consolidate around vendors offering integrated hardware-software-services stacks. Early movers in edge AI, digital twins, and outcome-based models capture disproportionate value.

What research methodology was used to analyze the Operational Technology Market?

The research methodology employs a multi-source triangulation approach combining primary and secondary research. Primary research includes interviews with OT vendors, system integrators, end-user enterprises across Energy and Utilities, Manufacturing, Transportation, and Building Automation verticals, and industry analysts. Secondary research encompasses company financial reports, regulatory filings, industry association publications, government infrastructure investment data, and technology adoption surveys. Market sizing utilizes bottom-up modeling from component-level shipments and top-down validation from vendor revenue analysis. The 9.53% CAGR projection incorporates scenario analysis for macroeconomic variables, technology adoption curves, and vertical-specific investment cycles. Forecast models account for IT-OT convergence acceleration, cybersecurity investment mandates, and sustainability-driven modernization across all geographic regions.

What is the scope and coverage limitations of this Operational Technology Market research?

The research scope covers the global Operational Technology Market segmented by Component (Hardware, Software, Services) and Industry Vertical (Energy and Utilities, Manufacturing, Transportation, Building Automation, Others). Geographic coverage includes all major industrial economies with regional analysis depth varying by data availability. The forecast period spans 2027-2033 with 2026 baseline of 178.65 Billion projecting to 337.91 Billion at 9.53% CAGR. Company coverage focuses on nine key players: ABB Ltd, Emerson Electric Co., General Electric, Hewlett Packard Enterprise, Honeywell International, IBM Corporation, NextNine Ltd., Siemens AG, and Wipro Limited. Limitations include exclusion of pure-play IT vendors without OT-specific offerings, consumer IoT segments, and detailed country-level forecasts. Emerging technologies like quantum sensing and neuromorphic computing are monitored but not quantified.

Which key companies operate in the Operational Technology Market and what are their recent developments?

The Operational Technology Market features nine prominent companies driving innovation through strategic developments. ABB Ltd (Switzerland) advances robotics-automation integration and energy management platforms. Emerson Electric Co. (US) expands measurement analytics portfolio and DeltaV automation software. General Electric (US) enhances Predix platform and digital twin capabilities across aviation and power. Hewlett Packard Enterprise (US) strengthens edge-to-cloud OT solutions with GreenLake. Honeywell International (US) integrates Forge platform across building automation, process solutions, and cybersecurity through NextNine Ltd. (Israel subsidiary) for secure remote operations. IBM Corporation (US) advances Maximo asset management and hybrid cloud OT integration. Siemens AG (Germany) leads with Digital Industries portfolio, MindSphere IoT OS, and Xcelerator platform. Wipro Limited (India) expands system integration and managed services for global industrial digital transformations across Energy, Manufacturing, Transportation, and Building Automation verticals.