What is the definition, scope, and significance of the Europe Automated Compounding Systems Market?

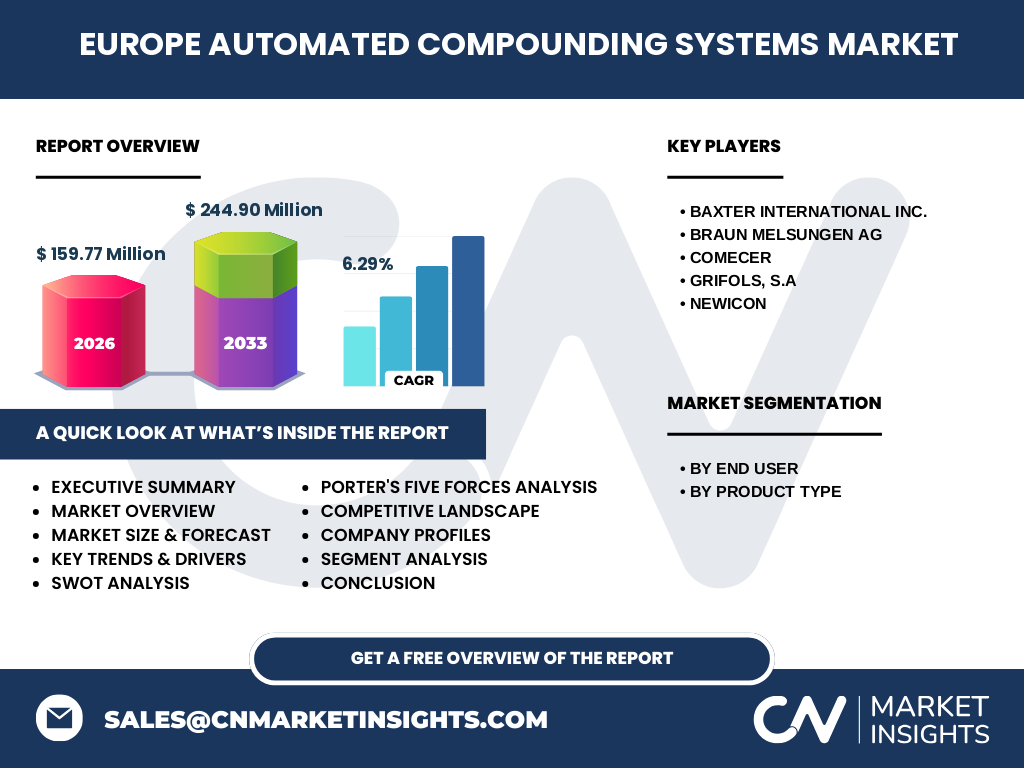

The Europe Automated Compounding Systems Market encompasses advanced robotic and software-driven platforms designed to automate the preparation of sterile and non-sterile intravenous medications, including chemotherapy, parenteral nutrition, and antibiotics. These systems enhance dosing accuracy, reduce contamination risk, improve workflow efficiency, and ensure regulatory compliance across hospital pharmacies and specialized oncology centers. The market scope includes gravimetric and volumetric technologies deployed in hospitals and chemotherapy centers. With a 2026 market size of 159.77 million and projected growth to 244.90 million by 2033 at a 6.29% CAGR, this market represents a critical infrastructure investment for European healthcare systems prioritizing patient safety and operational excellence.

What are the key drivers, restraints, challenges, and opportunities shaping the Europe Automated Compounding Systems Market?

Key drivers include stringent EU GMP regulations mandating sterile compounding standards, rising cancer incidence fueling chemotherapy demand, and hospital pharmacy labor shortages accelerating automation adoption. The 6.29% CAGR reflects strong momentum from patient safety initiatives and compounding error reduction mandates. Restraints involve high capital expenditure, integration complexity with legacy pharmacy IT systems, and reimbursement variability across European countries. Challenges include technical validation requirements, staff training needs, and maintenance costs. Opportunities lie in expanding gravimetric system adoption for higher precision, growing outpatient chemotherapy centers, and emerging markets in Eastern Europe where pharmacy modernization is accelerating.

What current and emerging trends are shaping the Europe Automated Compounding Systems Market?

The market is witnessing a shift from volumetric to gravimetric automated compounding systems due to superior weight-based accuracy for high-risk drugs. Integration with pharmacy management software and electronic health records is becoming standard, enabling closed-loop medication management. There's growing adoption in satellite pharmacies and outpatient chemotherapy centers beyond traditional hospital settings. Telepharmacy-enabled remote verification workflows are emerging post-COVID. Sustainability initiatives are driving demand for systems reducing drug waste and single-use plastic consumption. The 2026 market size of 159.77 million reflects early-stage adoption with significant expansion potential through 2033 as European hospitals modernize compounding infrastructure to meet evolving EU pharmacopeia standards.

How did COVID-19 impact the Europe Automated Compounding Systems Market and what is the recovery trajectory?

COVID-19 initially disrupted supply chains and delayed capital equipment installations across European hospitals in 2020-2021. However, the pandemic accelerated recognition of automation's value in reducing staff exposure during hazardous drug preparation and maintaining compounding continuity during workforce shortages. Post-pandemic, the market has rebounded strongly with the 6.29% CAGR reflecting pent-up demand and renewed investment in pharmacy resilience. Hospitals are prioritizing automated systems that enable social distancing, remote monitoring, and surge capacity for antiviral and critical care medication compounding. The forecast to 244.90 million by 2033 incorporates this structural shift toward automation as a permanent healthcare infrastructure upgrade rather than a temporary pandemic response.

What is the competitive landscape and market consolidation status in the Europe Automated Compounding Systems Market?

The Europe Automated Compounding Systems Market features a concentrated competitive landscape with five key players dominating: Baxter International Inc., B. Braun Melsungen AG, Comecer, Grifols S.A., and NewIcon. These companies compete across gravimetric and volumetric system portfolios, with differentiation in software integration, regulatory compliance features, and service networks. Market consolidation is moderate, with established medical technology leaders leveraging existing hospital relationships while specialized compounding automation firms like Comecer and NewIcon focus on technological innovation. Strategic partnerships with pharmacy software vendors and hospital groups are common. The competitive dynamics favor companies offering comprehensive installation, validation, training, and maintenance support across diverse European regulatory environments.

What are the key findings and high-level overview of the Europe Automated Compounding Systems Market?

The Europe Automated Compounding Systems Market is poised for robust growth from 159.77 million in 2026 to 244.90 million by 2033, driven by a 6.29% CAGR. Key findings include accelerating adoption of gravimetric over volumetric systems for chemotherapy and high-alert medications, strong demand from hospital pharmacies and dedicated chemotherapy centers, and regulatory pressure as the primary growth catalyst. The market is characterized by technological sophistication requirements, high entry barriers, and a concentrated vendor landscape led by Baxter, B. Braun, Comecer, Grifols, and NewIcon. Geographic adoption varies with Western Europe leading, while Eastern Europe represents untapped potential. Investment in automation is increasingly viewed as essential for patient safety, regulatory compliance, and operational efficiency.

What are the market projections and forecast for the Europe Automated Compounding Systems Market for 2025-2032?

The Europe Automated Compounding Systems Market is projected to grow from 159.77 million in 2026 to 244.90 million by 2033, representing a compound annual growth rate of 6.29%. This forecast encompasses both gravimetric and volumetric automated compounding systems across hospital and chemotherapy center end-user segments. The growth trajectory reflects sustained capital investment in pharmacy automation across European healthcare systems, driven by evolving EU GMP Annex 1 requirements, increasing chemotherapy volumes, and pharmacist shortage mitigation. The forecast period captures the transition from early adoption to mainstream deployment, with gravimetric systems expected to capture increasing market share due to superior accuracy for cytotoxic and high-cost biologics compounding.

What is the market size and share breakdown by segmentation for the Europe Automated Compounding Systems Market?

The Europe Automated Compounding Systems Market is segmented by product type into gravimetric automated compounding systems and volumetric automated compounding systems, and by end user into hospitals and chemotherapy centers. Gravimetric systems are gaining share due to weight-based precision requirements for chemotherapy and biologics. Hospitals represent the larger end-user segment given centralized pharmacy operations, while chemotherapy centers show faster growth as outpatient oncology expands. The total market size of 159.77 million in 2026 reflects combined revenues across both product types and end-user categories. Segmentation dynamics vary by country based on healthcare delivery models, with some markets favoring hospital-based compounding and others developing specialized ambulatory chemotherapy networks.

What is the geographic distribution and regional market size for the Europe Automated Compounding Systems Market?

The Europe Automated Compounding Systems Market encompasses all European countries with the 2026 market size of 159.77 million representing aggregate regional demand. Western European markets including Germany, France, UK, Italy, and Spain dominate current adoption due to advanced hospital infrastructure, stringent regulatory enforcement, and higher healthcare spending. Northern European countries show strong gravimetric system penetration. Eastern European markets represent emerging opportunities with pharmacy modernization programs underway. The forecast to 244.90 million by 2033 assumes broad-based growth across regions, with varying adoption curves based on national health policies, reimbursement frameworks, and cancer care network development. Regional distribution reflects Europe's diverse healthcare systems unified by EU pharmaceutical regulations.

What is the detailed regional performance analysis for the Europe Automated Compounding Systems Market?

Regional performance varies significantly across Europe. DACH region (Germany, Austria, Switzerland) leads in technology adoption with strong gravimetric system preference and established compounding regulations. France and Benelux countries show robust hospital pharmacy automation driven by national patient safety mandates. UK market growth is propelled by NHS pharmacy transformation programs. Southern Europe (Italy, Spain, Portugal) demonstrates accelerating adoption as chemotherapy volumes rise. Nordic countries exhibit high per-capita penetration with advanced telepharmacy integration. Eastern Europe (Poland, Czech Republic, Hungary) represents the fastest growth potential as EU structural funds support hospital modernization. The 6.29% CAGR aggregates these diverse regional trajectories toward the 244.90 million forecast.

Who are the leading companies in the Europe Automated Compounding Systems Market and what are their strategies?

The five leading companies are Baxter International Inc., B. Braun Melsungen AG, Comecer, Grifols S.A., and NewIcon. Baxter leverages its broad infusion therapy portfolio and global service network. B. Braun emphasizes integration with its pharmaceutical compounding and infusion pump ecosystems. Comecer specializes in radiopharmacy and cytotoxic compounding isolators with strong European regulatory expertise. Grifols focuses on plasma-derived medicines and hospital pharmacy automation synergies. NewIcon differentiates through robotic precision and software innovation for high-throughput environments. Common strategies include partnerships with pharmacy information system vendors, expansion of gravimetric technology portfolios, regulatory consulting services, and geographic expansion into Eastern European markets. All invest heavily in EU GMP Annex 1 compliance features.

What does the Porter's Five Forces analysis reveal about the Europe Automated Compounding Systems Market?

Porter's Five Forces analysis indicates moderate-to-high competitive intensity. Threat of new entrants is low due to high R&D barriers, regulatory validation requirements, and established hospital relationships. Supplier power is moderate with specialized component providers for robotics, gravimetric sensors, and sterile consumables. Buyer power is increasing as large hospital groups and purchasing consortia consolidate procurement. Threat of substitutes remains low as manual compounding cannot meet modern safety standards, though outsourcing to centralized compounding facilities presents an alternative model. Competitive rivalry is high among the five established players differentiating on technology precision, software integration, service quality, and regulatory support. The 6.29% CAGR reflects a growing pie that tempers direct rivalry.

What are the strengths, weaknesses, opportunities, and threats in the SWOT analysis of the Europe Automated Compounding Systems Market?

Strengths: Strong regulatory tailwinds (EU GMP Annex 1), proven error reduction, established vendor ecosystem with deep hospital relationships. Weaknesses: High capital costs, complex validation, specialized training requirements, integration challenges with legacy systems. Opportunities: Gravimetric technology expansion, Eastern European market penetration, outpatient chemotherapy center growth, telepharmacy-enabled remote verification, sustainability-driven waste reduction. Threats: Budget constraints in public healthcare systems, reimbursement policy changes, potential regulatory harmonization delays, cybersecurity risks in connected systems, competition from centralized compounding outsourcing models. The 159.77 million to 244.90 million growth trajectory reflects net positive SWOT dynamics with opportunities outweighing threats.

What is the value chain structure and value flow in the Europe Automated Compounding Systems Market?

The value chain comprises component suppliers (precision robotics, gravimetric load cells, sterile fluid path components), system integrators (the five key manufacturers), software providers (pharmacy management, compounding workflow, EHR integration), installation and validation services, distributors and direct sales channels, hospital pharmacy and chemotherapy center end-users, and ongoing service/maintenance/calibration providers. Value flows from component innovation through system design, regulatory validation (critical value-add), clinical implementation, and recurring revenue from consumables, software licenses, and service contracts. The 6.29% CAGR reflects value creation at each stage, with highest margins in gravimetric system sales, validation services, and long-term maintenance agreements. Regulatory compliance expertise represents a key value chain differentiator.

What are the key investment insights and strategic recommendations for the Europe Automated Compounding Systems Market?

Strategic investment should prioritize gravimetric technology platforms given superior accuracy requirements for expanding biologics and chemotherapy pipelines. Geographic focus on Western Europe for immediate revenue and Eastern Europe for growth capture. Partnership with pharmacy software vendors accelerates integration value. Service network investment is critical for retention and recurring revenue. Regulatory consulting capabilities create competitive moats. The 6.29% CAGR and 159.77 million to 244.90 million expansion supports acquisitions of specialized automation firms. R&D should target reduced footprint systems for satellite pharmacies, AI-driven compounding optimization, and sustainability features reducing drug waste. Investment timing favors early movers in gravimetric conversion cycles as volumetric systems reach replacement age.

What are the summary conclusions and key takeaways for the Europe Automated Compounding Systems Market?

The Europe Automated Compounding Systems Market represents a high-growth, regulation-driven sector expanding from 159.77 million in 2026 to 244.90 million by 2033 at 6.29% CAGR. Key takeaways: gravimetric systems are displacing volumetric technology for high-risk compounding; hospital pharmacies and chemotherapy centers are dual growth engines; five established vendors dominate but face evolving competitive dynamics; regulatory compliance (EU GMP Annex 1) is the primary market catalyst; Eastern Europe offers significant untapped potential; service and software integration capabilities determine long-term competitive position. The market's trajectory reflects healthcare's structural shift toward automation for patient safety, efficiency, and resilience. Stakeholders should monitor regulatory evolution, reimbursement policies, and technology convergence with pharmacy informatics.

What research methodology was used to analyze the Europe Automated Compounding Systems Market?

The research methodology combines primary and secondary research approaches. Primary research includes interviews with hospital pharmacy directors, oncology pharmacists, compounding technology specialists, and vendor executives across major European markets. Secondary research encompasses EU regulatory databases, national health ministry publications, hospital procurement records, company financial reports, industry association data (EAHP, ESH, ISOPP), and peer-reviewed literature on compounding automation outcomes. Market sizing employs bottom-up modeling from installed base data, procedure volumes, and average selling prices, validated through top-down cross-referencing with public company disclosures. Forecast modeling incorporates regulatory implementation timelines, healthcare capital expenditure trends, cancer incidence projections, and technology adoption curves. The 6.29% CAGR reflects consensus across multiple analytical frameworks.

What is the research scope and coverage limitations for the Europe Automated Compounding Systems Market analysis?

The research scope covers the Europe Automated Compounding Systems Market for gravimetric and volumetric automated compounding systems used in hospital pharmacies and chemotherapy centers across European countries. The analysis includes market size (159.77 million in 2026), forecast (244.90 million by 2033), CAGR (6.29%), segmentation by product type and end user, competitive landscape of five key companies (Baxter, B. Braun, Comecer, Grifols, NewIcon), and strategic analysis frameworks. Coverage focuses on sterile IV compounding automation excluding oral solid dose automation, non-sterile compounding, and manual compounding equipment. The scope encompasses EU and non-EU European countries with developed hospital pharmacy infrastructure. Market data reflects manufacturer revenue for systems, installation, validation, software, consumables, and service contracts.

What are the key companies and their recent developments in the Europe Automated Compounding Systems Market?

The five key companies driving the Europe Automated Compounding Systems Market are Baxter International Inc., B. Braun Melsungen AG, Comecer, Grifols S.A., and NewIcon. Baxter continues expanding its ExactaMix gravimetric platform with enhanced EHR connectivity. B. Braun has advanced its APOTECAchemo and APOTECAunits portfolio with improved robotic kinematics. Comecer focuses on isolator-integrated compounding systems meeting latest EU GMP Annex 1 requirements. Grifols leverages its hospital pharmacy automation division for integrated compounding workflow solutions. NewIcon develops high-throughput robotic systems with advanced gravimetric verification. Recent industry developments include strategic partnerships with pharmacy software vendors, expansion of service networks in Eastern Europe, new gravimetric sensor technologies reducing compounding cycle times, and sustainability initiatives addressing single-use plastic reduction in sterile fluid paths.