What is the Europe Delivery Management Software Market Overview, including definition, scope, and significance?

The Europe Delivery Management Software Market refers to the suite of digital platforms that enable businesses to plan, execute, and monitor last‑mile delivery operations across the continent. Its scope covers cloud‑based and on‑premises solutions serving restaurants, logistics firms, and courier businesses of all enterprise sizes. The market is significant because it drives operational efficiency, reduces delivery costs, and improves customer satisfaction in a region with dense urban centers and strict regulatory environments.

What are the key drivers, restraints, challenges, and opportunities shaping the Europe Delivery Management Software Market?

Key drivers include the surge in e‑commerce, rising consumer expectations for real‑time tracking, and the push for contactless deliveries accelerated by the pandemic. Restraints involve high implementation costs for on‑premises deployments and data‑privacy compliance across EU member states. Challenges comprise integration with legacy logistics systems and talent shortages for advanced analytics. Opportunities lie in expanding cloud adoption among small and medium enterprises and leveraging AI‑based route optimization.

What are the current and emerging growth trends in the Europe Delivery Management Software Market?

Current trends show a rapid shift toward cloud‑native platforms that offer scalability and lower upfront investment. Artificial intelligence and machine learning are being embedded for predictive ETAs, dynamic routing, and automated dispatch. Sustainability pressures drive adoption of electric‑vehicle‑friendly routing and carbon‑footprint reporting. Additionally, API‑first architectures enable seamless integration with third‑party marketplaces and warehouse management systems across Europe.

How did COVID‑19 impact the Europe Delivery Management Software Market and what is the recovery trajectory?

COVID‑19 acted as a catalyst, compressing digital transformation timelines by several years. Lockdowns forced restaurants and retailers to adopt delivery management tools almost overnight, boosting demand for cloud solutions. The pandemic also highlighted the need for contactless proof‑of‑delivery and real‑time customer communication. Post‑pandemic, the market maintains elevated growth as businesses retain digital capabilities and invest in resilience against future disruptions.

What does the competitive landscape look like for the Europe Delivery Management Software Market?

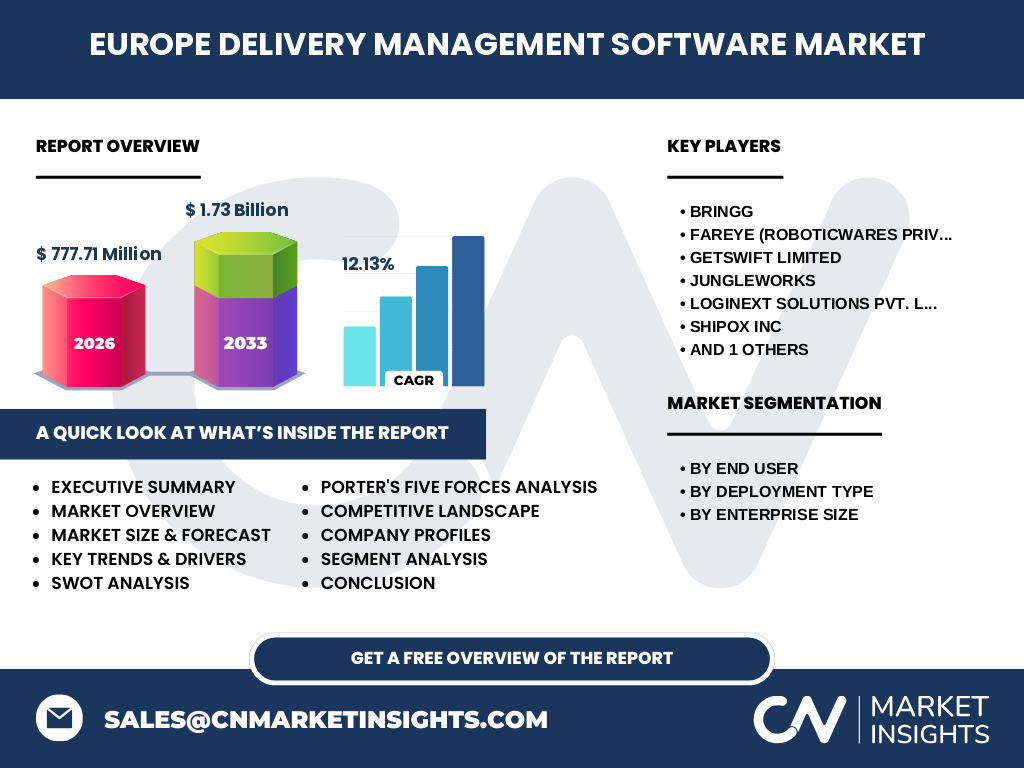

The competitive landscape is fragmented yet consolidating, with major players such as Bringg, FarEye (RoboticWares Private Limited), GetSwift Limited, JungleWorks, Loginext Solutions Pvt. Ltd, Shipox Inc, and WorkWave LLC commanding significant market share. These firms differentiate through AI‑driven routing, multi‑tenant cloud platforms, and industry‑specific modules for restaurant, logistics, and courier segments. Strategic partnerships and acquisitions are common as vendors seek to broaden geographic coverage and enhance functionality.

What are the key findings and high‑level overview from the executive summary of the Europe Delivery Management Software Market?

The executive summary highlights that the Europe Delivery Management Software Market was valued at 777.71 million in 2026 and is projected to reach 1.73 billion by 2033, reflecting a CAGR of 12.13 percent. Growth is fueled by e‑commerce expansion, cloud adoption, and regulatory pressure for transparency. The market serves restaurant delivery, logistics, and courier businesses across cloud and on‑premises deployments, with small and medium enterprises representing a fast‑growing user base.

What are the market forecast projections for the Europe Delivery Management Software Market for the 2025‑2032 period?

Market forecasts indicate continued double‑digit growth from 2027 through 2033, driven by the 12.13 percent CAGR. By 2033 the market is expected to surpass 1.73 billion, with cloud deployments outpacing on‑premises due to lower total cost of ownership. The restaurant delivery segment will lead revenue, followed by logistics and courier businesses, while large enterprises will maintain higher per‑account spend than small and medium enterprises.

How is the Europe Delivery Management Software Market size and share broken down by segmentation?

Segmentation analysis breaks the market by end user, deployment type, and enterprise size. End‑user categories include restaurant delivery, logistics, and courier business. Deployment is split between cloud and on‑premises solutions. Enterprise size distinguishes small and medium enterprises from large enterprises. The 777.71 million valuation in 2026 is distributed across these dimensions, with cloud‑based restaurant delivery for small and medium enterprises showing the fastest adoption rate.

What is the global Europe Delivery Management Software Market size and share by region?

Geographically, the report focuses on the European region, where the market size stood at 777.71 million in 2026 and is forecast to reach 1.73 billion by 2033. While the data does not provide a country‑level breakdown, Western Europe’s mature e‑commerce infrastructure and Eastern Europe’s rapid digitalization both contribute to the aggregate growth. The region’s unified regulatory framework further supports cross‑border solution deployment.

What does the regional analysis reveal about the Europe Delivery Management Software Market performance?

Regional analysis reveals that Western European markets such as Germany, France, and the United Kingdom lead in cloud adoption and AI‑enabled routing, generating the highest per‑capita spend. Southern Europe shows strong growth in restaurant delivery platforms driven by tourism‑linked food services. Northern Europe emphasizes sustainability, pushing electric‑vehicle routing features. Eastern Europe, while smaller in absolute terms, exhibits the steepest CAGR as local logistics firms modernize legacy systems.

Who are the leading companies in the Europe Delivery Management Software Market and what are their strategies?

Leading company profiles highlight each vendor’s strategic focus. Bringg emphasizes enterprise‑grade orchestration and real‑time visibility. FarEye leverages robotic process automation for last‑mile optimization. GetSwift Limited targets on‑demand delivery marketplaces with a low‑code platform. JungleWorks offers modular SaaS for food‑ordering ecosystems. Loginext Solutions provides AI‑driven route planning for large logistics fleets. Shipox Inc specializes in courier‑centric dispatch automation. WorkWave LLC delivers integrated field‑service and delivery management for service‑oriented businesses.

What is the Porter’s Five Forces analysis for the Europe Delivery Management Software Market?

Porter’s Five Forces analysis shows moderate threat of new entrants due to high technology barriers and established customer relationships. Supplier power is low because cloud infrastructure providers are abundant. Buyer power is rising as enterprises demand flexible pricing and interoperability. Threat of substitutes remains limited; traditional manual dispatch cannot match real‑time analytics. Competitive rivalry is intense among the seven key players, driving continuous innovation and pricing pressure.

What is the SWOT analysis for the Europe Delivery Management Software Market?

SWOT analysis identifies strengths such as robust AI routing engines, scalable cloud architectures, and strong compliance with GDPR. Weaknesses include high upfront cost for on‑premises deployments and reliance on third‑party map data. Opportunities encompass expanding into emerging Eastern European markets, integrating sustainability metrics, and offering API marketplaces. Threats involve regulatory changes, cybersecurity risks, and potential price wars as competitors consolidate.

What does the value chain analysis show for the Europe Delivery Management Software Market?

Value chain analysis maps the flow from raw data acquisition (GPS, order feeds) through platform development, integration services, and end‑user deployment. Core value is created in the software layer where routing algorithms, real‑time tracking, and analytics reside. Service providers add value via implementation, customization, and support. Distribution channels include direct sales, system integrators, and cloud marketplaces. Revenue is captured through subscription licenses, transaction fees, and professional services.

What are the key investment insights for the Europe Delivery Management Software Market?

Key investment insights recommend allocating capital toward cloud‑native vendors with proven AI routing and strong GDPR compliance. Prioritize companies expanding API ecosystems to capture the growing SME segment. Consider strategic stakes in firms targeting Eastern Europe’s high CAGR. Monitor M&A activity among the seven major players, as consolidation can create scale advantages. Diversify across deployment models to hedge against on‑premises demand fluctuations.

What is the conclusion and key takeaway for the Europe Delivery Management Software Market?

The conclusion underscores that the Europe Delivery Management Software Market is on a robust growth trajectory, anchored by a 12.13 percent CAGR and a projected valuation of 1.73 billion by 2033. Cloud adoption, AI‑driven optimization, and regulatory compliance are the primary levers. Stakeholders should focus on scalable, interoperable solutions that address the distinct needs of restaurant, logistics, and courier segments across enterprise sizes.

What research methodology was used to produce this Europe Delivery Management Software Market report?

Research methodology combines primary interviews with product managers, CTOs, and end‑users across the seven key vendors, supplemented by secondary sources such as financial filings, industry white papers, and market databases. Quantitative modeling uses the reported 777.71 million 2026 base and 12.13 percent CAGR to extrapolate the 2027‑2033 forecast. Qualitative insights are validated through triangulation across multiple expert opinions.

What is the research scope and coverage limitations for the Europe Delivery Management Software Market study?

Research scope covers the Europe Delivery Management Software Market from 2026 through 2033, segmented by end user (restaurant delivery, logistics, courier business), deployment type (cloud, on‑premises), and enterprise size (small and medium enterprises, large enterprises). The study includes the seven identified vendors and excludes adjacent markets such as warehouse management or fleet telematics. Geographic coverage is limited to the European region without country‑level granularity.

Which key companies are featured and what recent developments have they announced in the Europe Delivery Management Software Market?

Key companies and recent developments feature Bringg’s launch of a unified orchestration hub, FarEye’s acquisition of a robotic process automation startup, GetSwift Limited’s partnership with a major European food‑delivery marketplace, JungleWorks’ release of a low‑code API toolkit, Loginext Solutions’ AI‑enhanced route optimizer for electric fleets, Shipox Inc’s integration with a leading courier network, and WorkWave LLC’s expansion of field‑service modules for service‑oriented delivery. These moves signal accelerated innovation and market consolidation.