What is the North America Touch Panel Market Overview including definition, scope, and significance?

The North America Touch Panel Market encompasses the development, manufacturing, and deployment of interactive display technologies across the United States, Canada, and Mexico. Touch panels serve as critical human-machine interfaces enabling direct interaction with digital content through touch gestures. The market scope includes resistive, capacitive, and infrared technologies serving consumer electronics, medical devices, retail systems, and industrial automation applications. With a market size of $30.02 billion in 2026, this sector represents a significant component of the broader display technology ecosystem. The significance lies in touch panels' role as essential interfaces for smartphones, tablets, kiosks, point-of-sale systems, medical equipment, and industrial control panels. As digital transformation accelerates across industries, touch interfaces have become fundamental to user experience design, operational efficiency, and competitive differentiation for businesses throughout North America.

What are the key drivers, restraints, challenges, and opportunities in the North America Touch Panel Market?

Key drivers include increasing adoption of touch-enabled devices across consumer electronics, growing demand for interactive displays in retail and healthcare sectors, and rising industrial automation requiring intuitive human-machine interfaces. The projected CAGR of 10.80% from 2027 to 2033 reflects strong growth momentum. Major restraints involve high manufacturing costs for advanced capacitive technologies, supply chain vulnerabilities for critical components, and technical limitations in extreme environmental conditions. Challenges include intense price competition among established players like Samsung, LG Display, and 3M, rapid technology obsolescence, and stringent regulatory requirements for medical and automotive applications. Opportunities emerge from expanding applications in automotive displays, growing demand for large-format interactive displays in education and corporate environments, increasing integration of touch technology in IoT devices, and the rising trend of contactless interfaces post-pandemic. The forecasted market value of $61.54 billion by 2033 underscores substantial expansion potential.

What are the current and emerging growth trends shaping the North America Touch Panel Market?

Current trends include the dominant shift toward capacitive technology due to superior multi-touch capabilities and durability, increasing adoption of in-cell and on-cell touch integration for thinner device profiles, and growing demand for large-format displays exceeding 55 inches in commercial applications. Emerging trends feature the development of flexible and foldable touch panels for next-generation devices, integration of haptic feedback for enhanced user experience, and advancement of infrared technology for large-scale interactive walls and outdoor kiosks. The market sees rising penetration in automotive applications including center stack displays and rear-seat entertainment systems. Medical applications expand with touch-enabled diagnostic equipment and patient monitoring systems. Retail transformation drives demand for self-service kiosks and interactive signage. Industrial Sector 4.0 initiatives accelerate adoption of ruggedized touch panels for factory automation. These trends collectively support the projected growth trajectory from $30.02 billion in 2026 to $61.54 billion by 2033.

How has COVID-19 impacted the North America Touch Panel Market and what is the recovery trajectory?

The COVID-19 pandemic initially disrupted the North America Touch Panel Market through supply chain interruptions, manufacturing facility shutdowns, and reduced consumer spending on discretionary electronics. However, the crisis accelerated digital transformation across multiple sectors, creating new demand drivers. Remote work and learning fueled unprecedented demand for laptops, tablets, and monitors with touch capabilities. Healthcare sector urgency drove rapid deployment of touch-enabled medical devices, telemedicine kiosks, and patient check-in systems. Retail and hospitality industries accelerated adoption of contactless self-service kiosks and touchless payment terminals. The market demonstrated resilience with recovery supported by pent-up demand and structural shifts toward touch interfaces. The projected CAGR of 10.80% from 2027 to 2033 reflects strong post-pandemic recovery momentum. Companies like Innolux Corporation, Planar, and Xenarc Technologies adapted production strategies to meet evolving demand patterns, positioning the market for sustained expansion toward the $61.54 billion forecast by 2033.

What is the competitive landscape of the North America Touch Panel Market including major competitors and market consolidation?

The North America Touch Panel Market features a competitive landscape with ten key players: 3M, Advantech Co. Ltd., FUJITSU LIMITED, Hitachi Ltd, Innolux Corporation, LG Display Co. Ltd., Planar, Renesas Electronics Corporation, Samsung, and Xenarc Technologies Corporation. These companies compete across technology segments including resistive, capacitive, and infrared touch solutions. Market consolidation trends show larger display manufacturers like Samsung and LG Display leveraging vertical integration advantages, while specialized players like 3M and Planar focus on niche commercial and industrial applications. Advantech and Renesas strengthen positions in industrial and automotive segments respectively. Innolux Corporation and FUJITSU LIMITED compete in medical and enterprise-grade solutions. Xenarc Technologies specializes in ruggedized displays for demanding environments. The competitive dynamics are shaped by R&D investments in next-generation touch technologies, strategic partnerships for component supply, and geographic expansion strategies. The market's growth trajectory toward $61.54 billion by 2033 intensifies competition for market share across consumer, commercial, and industrial product types.

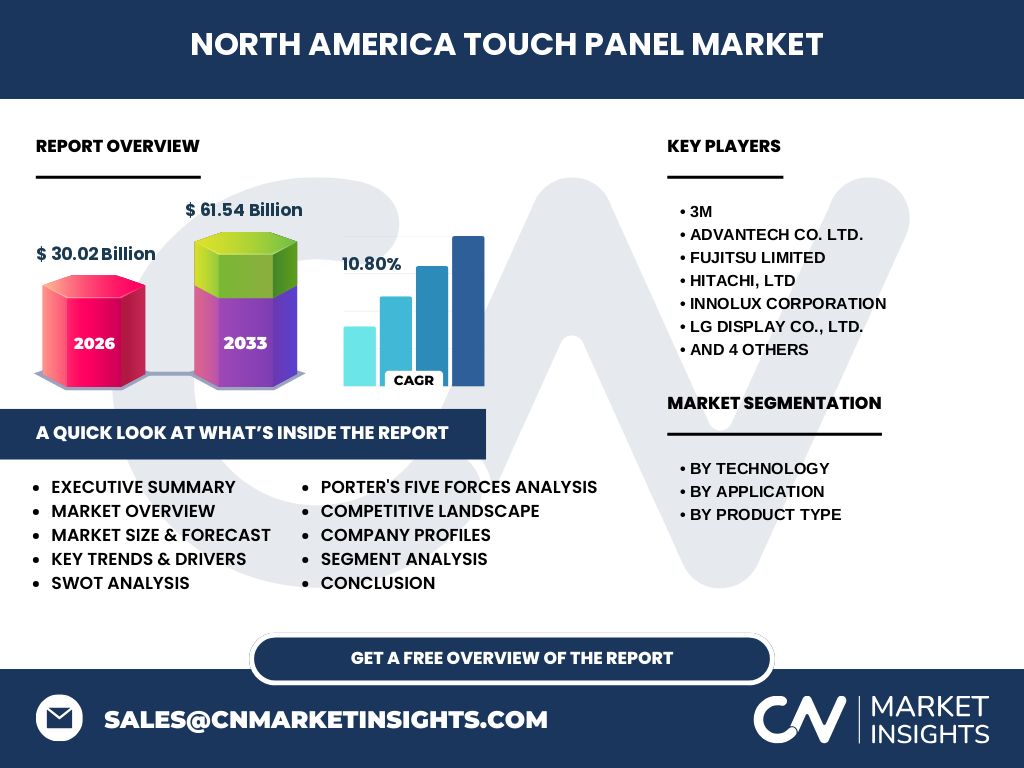

What are the key findings and high-level overview of the North America Touch Panel Market in the Executive Summary?

The North America Touch Panel Market demonstrates robust growth fundamentals with a 2026 market size of $30.02 billion projected to reach $61.54 billion by 2033, representing a 10.80% CAGR. The market encompasses three primary technologies: resistive, capacitive, and infrared, serving diverse applications across consumer electronics, medical devices, retail systems, and industrial automation. Product segmentation includes consumer and commercial/industrial categories. Key players including Samsung, LG Display, 3M, and Innolux Corporation drive innovation through R&D investments and strategic partnerships. Growth drivers include digital transformation across industries, automotive display proliferation, healthcare technology adoption, and retail automation. The market recovered strongly from COVID-19 disruptions, with pandemic-induced behavioral changes accelerating touch interface adoption. Competitive intensity remains high with both consolidated display giants and specialized technology providers. The forecast period 2027-2033 presents significant opportunities in flexible displays, haptic integration, large-format commercial applications, and industrial IoT implementations.

What are the market projections and forecast for the North America Touch Panel Market for the 2025-2032 period?

The North America Touch Panel Market forecast indicates substantial growth from the 2026 baseline of $30.02 billion to $61.54 billion by 2033, reflecting a compound annual growth rate of 10.80% during the 2027-2033 forecast period. This projection encompasses all technology segments including resistive, capacitive, and infrared touch panels across consumer, medical, retail, and industrial applications. The growth trajectory assumes continued digital transformation across North American economies, sustained demand for touch-enabled consumer electronics, expanding automotive display applications, and accelerating adoption of interactive solutions in healthcare and retail sectors. The commercial and industrial product segment is expected to outpace consumer segment growth driven by Sector 4.0 initiatives and enterprise digitalization. Regional dynamics within North America show the United States maintaining dominant market share followed by Canada and Mexico. The forecast considers macroeconomic factors, technology adoption curves, competitive landscape evolution, and regulatory environments impacting market development through 2033.

What is the market size and share breakdown by segmentation for the North America Touch Panel Market?

The North America Touch Panel Market segmentation analysis reveals three primary classification frameworks. By technology, the market divides into resistive, capacitive, and infrared touch panels, with capacitive technology leading adoption in consumer electronics due to multi-touch capability and optical clarity. By application, four key segments emerge: consumer electronics representing the largest volume segment, medical devices requiring high reliability and regulatory compliance, retail systems including point-of-sale and interactive kiosks, and industrial automation demanding ruggedized solutions. By product type, the market separates into consumer-grade panels for personal devices and commercial/industrial-grade panels for enterprise applications. The overall market valued at $30.02 billion in 2026 distributes across these segments with varying growth rates. The commercial and industrial product segment demonstrates stronger growth momentum aligned with digital transformation initiatives. Each segment exhibits distinct competitive dynamics, technology requirements, and customer purchasing behaviors that influence market share distribution among the ten key players including 3M, Samsung, LG Display, and specialized providers like Planar and Xenarc Technologies.

What is the global market size and share by region for the North America Touch Panel Market?

The North America Touch Panel Market represents a significant regional segment within the global touch panel industry, with a market size of $30.02 billion in 2026 projected to reach $61.54 billion by 2033 at a 10.80% CAGR. Within the North American region, the United States constitutes the largest country market driven by high consumer electronics penetration, advanced healthcare infrastructure, robust retail automation, and strong industrial manufacturing base. Canada follows with growing adoption in commercial applications and public sector digitalization initiatives. Mexico benefits from manufacturing proximity and expanding automotive production driving demand for touch-enabled vehicle displays. The regional market benefits from presence of major global players including Samsung, LG Display, and 3M alongside North American specialists like Planar, Xenarc Technologies, and Advantech. Regional growth is supported by strong R&D ecosystems, early technology adoption culture, and high per-capita spending on electronic devices. The forecast period 2027-2033 expects sustained regional leadership in touch technology innovation and application development.

What is the detailed regional analysis of the North America Touch Panel Market performance?

The North America Touch Panel Market regional analysis reveals distinct performance characteristics across the United States, Canada, and Mexico. The United States dominates with the largest market share driven by Silicon Valley innovation ecosystem, high consumer electronics adoption rates, extensive healthcare technology deployment, and advanced retail automation. Major technology hubs concentrate R&D activities for next-generation touch solutions. Canada shows strong growth in commercial and industrial segments, particularly in financial services self-service banking, transportation infrastructure, and public sector digital services. The Canadian market benefits from government digital initiatives and high enterprise technology spending. Mexico emerges as a manufacturing hub with growing domestic demand, leveraging automotive production clusters requiring touch-enabled instrument clusters and infotainment systems. Cross-border supply chain integration supports regional competitiveness. All three countries contribute to the aggregate $30.02 billion market size in 2026 with the 10.80% CAGR reflecting region-wide digital transformation momentum. Regulatory harmonization under USMCA facilitates technology deployment and market access across the region.

Who are the leading company profiles in the North America Touch Panel Market and what are their strategies?

The North America Touch Panel Market features ten prominent companies with distinct strategic positioning. Samsung and LG Display leverage vertical integration from panel manufacturing to touch module assembly, targeting high-volume consumer and automotive segments. 3M focuses on specialized films and coatings for capacitive touch sensors, serving premium commercial applications. Innolux Corporation emphasizes large-format displays for commercial signage and industrial applications. FUJITSU LIMITED targets enterprise and medical-grade touch solutions with high reliability requirements. Hitachi Ltd concentrates on industrial automation and transportation systems. Advantech Co. Ltd. specializes in ruggedized industrial touch panels for Sector 4.0 deployments. Planar, a Leyard company, leads in large-format collaborative displays and control room solutions. Renesas Electronics Corporation provides touch controller ICs enabling advanced touch functionality. Xenarc Technologies Corporation focuses on extreme environment rugged displays for military, marine, and industrial applications. Strategies include R&D investment in flexible and foldable technologies, strategic partnerships for supply chain resilience, geographic expansion within North America, and application-specific product development aligned with the market's projected growth to $61.54 billion by 2033.

What is the Porter's Five Forces analysis of the North America Touch Panel Market competitive forces?

The Porter's Five Forces analysis for the North America Touch Panel Market reveals moderate to high competitive intensity. Threat of new entrants remains moderate due to high capital requirements for manufacturing facilities, established intellectual property portfolios held by incumbents like Samsung and LG Display, and stringent quality certifications for medical and automotive applications. Bargaining power of suppliers is moderate, with specialized material providers for indium tin oxide, cover glass, and controller ICs holding leverage, though large buyers like 3M and Innolux Corporation mitigate this through volume purchasing. Bargaining power of buyers is high, particularly from large OEMs in consumer electronics and automotive sectors who demand cost reductions and customization. Threat of substitutes exists from alternative interface technologies including voice control, gesture recognition, and stylus-based systems, though touch remains dominant for direct manipulation tasks. Competitive rivalry is intense among the ten key players including FUJITSU LIMITED, Hitachi Ltd, Advantech, Planar, Renesas Electronics, and Xenarc Technologies, driving continuous innovation and price pressure across the $30.02 billion market expanding to $61.54 billion by 2033.

What is the SWOT analysis of the North America Touch Panel Market including strengths, weaknesses, opportunities, and threats?

The SWOT analysis for the North America Touch Panel Market identifies key strategic factors. Strengths include strong R&D infrastructure with innovation hubs across the region, established supply chain networks, high technology adoption rates among consumers and enterprises, and presence of global leaders like Samsung, LG Display, and 3M. The 10.80% CAGR reflects fundamental market strength. Weaknesses involve dependence on Asian component supply chains for critical materials, high manufacturing costs compared to offshore alternatives, skilled labor shortages in advanced manufacturing, and technology fragmentation across resistive, capacitive, and infrared standards. Opportunities encompass expanding automotive display applications, growing demand for large-format collaborative displays, healthcare digital transformation, retail automation acceleration, and emerging flexible/foldable form factors. The forecast to $61.54 billion by 2033 quantifies this potential. Threats include geopolitical trade tensions affecting component sourcing, intense price competition eroding margins, rapid technology obsolescence cycles, regulatory compliance complexity across medical and automotive sectors, and potential disruption from alternative interface technologies like voice and gesture control.

What is the value chain analysis of the North America Touch Panel Market industry structure and value flow?

The North America Touch Panel Market value chain encompasses five primary stages. Upstream raw material suppliers provide indium tin oxide for transparent conductors, cover glass substrates, adhesives, and specialized films. Component manufacturers produce touch sensors (capacitive, resistive, infrared), controller ICs from companies like Renesas Electronics Corporation, and driver circuits. Module integrators including 3M, Planar, and Xenarc Technologies assemble touch sensors with display panels, optical bonding, and protective layers. System integrators and OEMs such as Advantech, FUJITSU LIMITED, and Hitachi Ltd incorporate touch modules into finished products spanning consumer devices, medical equipment, retail kiosks, and industrial control panels. End users across consumer, medical, retail, and industrial sectors drive demand for the $30.02 billion market. Value flows from material suppliers (lower margin) through component and module stages (moderate margin) to system integration (higher margin) where application-specific customization creates differentiation. Key players like Samsung and LG Display operate across multiple stages capturing more value. The projected growth to $61.54 billion by 2033 expands value creation opportunities across all chain stages.

What are the key investment insights and strategic recommendations for the North America Touch Panel Market?

Key investment insights for the North America Touch Panel Market highlight several strategic opportunities aligned with the 10.80% CAGR and $61.54 billion forecast by 2033. Priority investment areas include capacitive touch technology R&D for automotive-grade displays meeting AEC-Q100 standards, large-format interactive displays exceeding 65 inches for enterprise collaboration, and ruggedized industrial touch panels for Sector 4.0 factory automation. Medical-grade touch solutions with antimicrobial coatings and regulatory compliance represent high-margin niches. Supply chain localization investments reduce geopolitical risk for critical components like controller ICs and specialized films. Strategic partnerships with companies like Innolux Corporation, Planar, and Xenarc Technologies provide access to specialized application expertise. Emerging opportunities in flexible and foldable touch panels warrant early-stage R&D allocation. Retail automation and contactless self-service kiosks driven by post-pandemic behavioral changes offer near-term revenue growth. Investors should monitor technology standardization efforts, regulatory developments in healthcare and automotive, and competitive dynamics among the ten key market players for optimal portfolio positioning.

What is the conclusion and key takeaways for the North America Touch Panel Market?

The North America Touch Panel Market concludes as a dynamic, high-growth sector with robust fundamentals supporting expansion from $30.02 billion in 2026 to $61.54 billion by 2033 at a 10.80% CAGR. Key takeaways include the market's resilience demonstrated through COVID-19 recovery and acceleration of digital transformation trends. Technology evolution favors capacitive solutions for consumer and automotive applications while infrared maintains relevance in large-format commercial deployments. The competitive landscape balances global display giants Samsung and LG Display with specialized North American players including 3M, Planar, Xenarc Technologies, and Advantech Co. Ltd. Application diversification across consumer, medical, retail, and industrial sectors provides revenue stability. Regional strengths in innovation, early adoption, and advanced manufacturing create sustainable competitive advantages. Critical success factors include supply chain resilience, application-specific customization capabilities, regulatory compliance expertise, and strategic partnerships across the value chain. The forecast period presents significant opportunities for stakeholders who align investments with automotive displays, healthcare technology, industrial automation, and next-generation form factor development.

What research methodology was used to conduct this North America Touch Panel Market analysis?

The research methodology for this North America Touch Panel Market analysis employs a comprehensive multi-phase approach combining primary and secondary research techniques. Primary research includes structured interviews with industry executives from key companies including 3M, Advantech Co. Ltd., FUJITSU LIMITED, Hitachi Ltd, Innolux Corporation, LG Display Co. Ltd., Planar, Renesas Electronics Corporation, Samsung, and Xenarc Technologies Corporation. Secondary research encompasses extensive review of company financial reports, SEC filings, investor presentations, patent databases, technical publications, and industry association data. Market sizing utilizes bottom-up approaches aggregating company revenues by technology segment (resistive, capacitive, infrared) and application verticals (consumer, medical, retail, industrial). Top-down validation cross-references with macroeconomic indicators, display industry trends, and technology adoption curves. Forecast modeling incorporates driver-based assumptions for the 2027-2033 period yielding the 10.80% CAGR projection. Competitive analysis applies Porter's Five Forces and SWOT frameworks. Regional analysis examines United States, Canada, and Mexico market dynamics. Data triangulation ensures accuracy of the $30.02 billion 2026 baseline and $61.54 billion 2033 forecast.

What is the research scope and coverage limitations for this North America Touch Panel Market report?

The research scope for this North America Touch Panel Market report encompasses comprehensive analysis of the United States, Canada, and Mexico markets across the 2026-2033 period. Coverage includes all three primary technology segments: resistive, capacitive, and infrared touch panels. Application analysis spans four verticals: consumer electronics, medical devices, retail systems, and industrial automation. Product type segmentation covers consumer-grade and commercial/industrial-grade panels. The report profiles ten key companies: 3M, Advantech Co. Ltd., FUJITSU LIMITED, Hitachi Ltd, Innolux Corporation, LG Display Co. Ltd., Planar, Renesas Electronics Corporation, Samsung, and Xenarc Technologies Corporation. Financial projections anchor on the $30.02 billion 2026 market size and $61.54 billion 2033 forecast with 10.80% CAGR. Analytical frameworks include Porter's Five Forces, SWOT analysis, value chain mapping, and competitive landscape assessment. Scope excludes South American markets, individual company market share percentages, quarterly financial projections, and component-level pricing analysis. The research focuses on strategic insights supporting investment and business decisions rather than operational tactical guidance.

Who are the key companies and what are their recent developments in the North America Touch Panel Market?

The North America Touch Panel Market features ten key companies driving innovation and competitive dynamics. Samsung and LG Display lead with advanced OLED and LCD touch integration for consumer electronics and automotive displays. 3M continues developing next-generation capacitive touch films with enhanced optical clarity and durability for commercial applications. Innolux Corporation expands large-format touch panel production for digital signage and collaborative displays. FUJITSU LIMITED advances medical-grade touch solutions with antimicrobial surfaces and regulatory certifications. Hitachi Ltd focuses on industrial touch panels for transportation and factory automation. Advantech Co. Ltd. introduces ruggedized edge computing touch terminals for Sector 4.0 deployments. Planar, under Leyard ownership, launches fine-pitch LED touch walls for control rooms and experiential installations. Renesas Electronics Corporation releases new touch controller ICs supporting higher refresh rates and lower power consumption. Xenarc Technologies Corporation develops sunlight-readable, wide-temperature touch monitors for defense and marine applications. These developments align with the market's growth trajectory from $30.02 billion in 2026 to $61.54 billion by 2033 at 10.80% CAGR.