Logistics Service Market Overview - Definition, scope, and significance

The logistics service market encompasses the comprehensive management of the flow of goods, services, and information between the point of origin and the point of consumption to meet customer requirements. This market includes transportation, warehousing, inventory management, packaging, and freight forwarding services across multiple transportation modes including roadways, waterways, rail, and airways. The scope extends from first-party logistics (1PL) through fifth-party logistics (5PL), covering everything from basic transportation to fully integrated supply chain solutions. The market's significance lies in its critical role as the backbone of global trade, enabling businesses to operate efficiently across borders, manage inventory effectively, and deliver products to consumers worldwide. As globalization continues to expand and e-commerce grows exponentially, logistics services have become increasingly vital for economic development and international commerce.

Logistics Service Market Drivers, Restraints, Challenges, and Opportunities - Key growth factors and obstacles

The logistics service market is primarily driven by the rapid growth of e-commerce, globalization of trade, and increasing consumer demand for faster delivery times. The expansion of manufacturing sectors in emerging economies and the rise of just-in-time inventory management practices further accelerate market growth. However, the market faces significant restraints including high operational costs, complex regulatory environments across different countries, and the need for substantial infrastructure investment. Challenges such as supply chain disruptions, capacity constraints, and the shortage of skilled workforce continue to impact the industry. Despite these obstacles, numerous opportunities exist, including the integration of advanced technologies like artificial intelligence and blockchain for enhanced supply chain visibility, the growing demand for sustainable logistics solutions, and the potential for market expansion in developing regions with improving infrastructure.

Logistics Service Market Growth Trends - Current and emerging trends shaping the market

The logistics service market is experiencing several transformative trends that are reshaping the industry landscape. Digital transformation through automation, IoT integration, and real-time tracking systems is becoming increasingly prevalent, enabling greater efficiency and transparency in supply chain operations. The adoption of green logistics practices and sustainable transportation methods is gaining momentum as companies prioritize environmental responsibility. Last-mile delivery innovations, including drone deliveries and autonomous vehicles, are revolutionizing the final stage of product delivery. Additionally, the market is witnessing a shift toward integrated logistics solutions that combine multiple services under one provider, offering customers end-to-end supply chain management. The COVID-19 pandemic has accelerated the adoption of contactless delivery and digital documentation processes, while also highlighting the importance of resilient and flexible supply chain networks.

COVID-19 Impact on the Logistics Service Market - Pandemic effects and recovery trajectory

The COVID-19 pandemic significantly disrupted the logistics service market, creating both immediate challenges and long-term structural changes. Initial lockdowns and border closures led to severe supply chain disruptions, port congestions, and transportation delays across the globe. However, the pandemic also accelerated digital transformation within the industry, with increased adoption of contactless delivery, real-time tracking systems, and automated warehouse operations. E-commerce experienced unprecedented growth during this period, driving demand for last-mile delivery services and warehousing capacity. The recovery trajectory shows a gradual return to pre-pandemic operations, but with lasting changes including enhanced supply chain resilience, greater emphasis on regional manufacturing, and increased investment in technology for supply chain visibility. The industry has emerged more adaptable and technology-driven, with companies now prioritizing flexibility and risk management in their logistics strategies.

Logistics Service Market Competitive Landscape - Major competitors and market consolidation

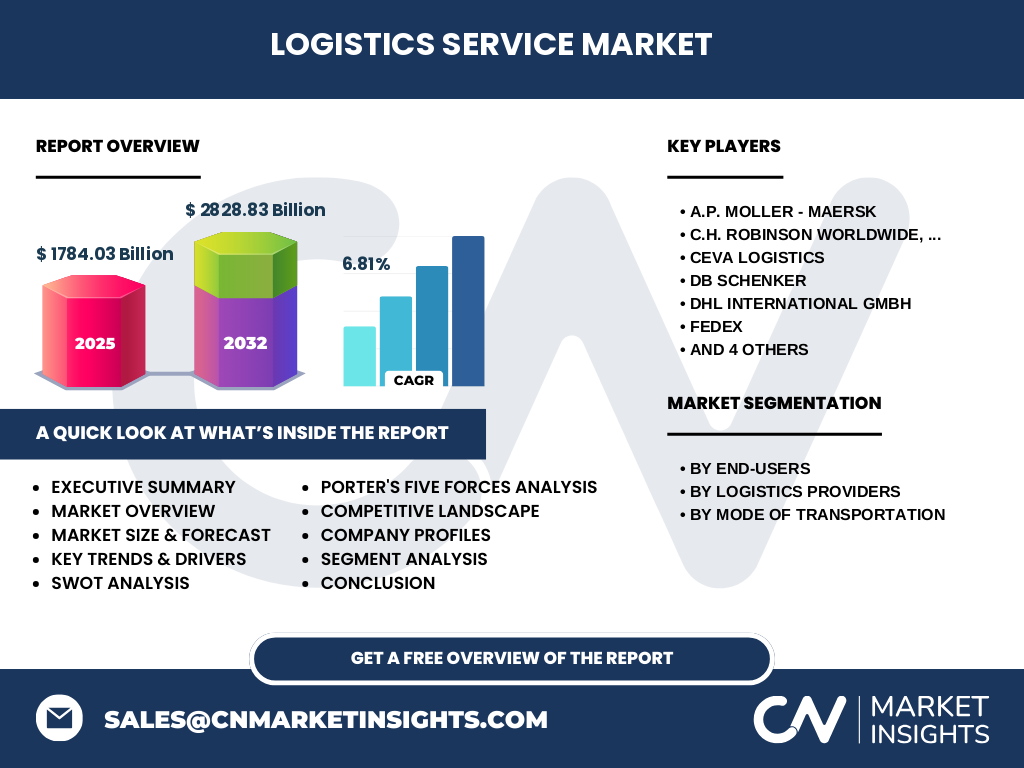

The logistics service market features a highly competitive landscape characterized by the presence of both global giants and specialized regional players. Major competitors include A.P. MOLLER - MAERSK, DHL International GmbH, FedEx, United Parcel Service (UPS), and KUEHNE + NAGEL, which dominate through their extensive global networks and comprehensive service offerings. The market is witnessing increasing consolidation through mergers and acquisitions as companies seek to expand their geographic reach and service capabilities. Competition is intensifying particularly in the e-commerce logistics segment, with companies investing heavily in last-mile delivery solutions and warehousing infrastructure. The competitive dynamics are also shaped by the entry of technology companies into the logistics space, creating new competitive pressures and driving innovation in supply chain solutions. Market players are increasingly focusing on developing integrated logistics platforms that combine multiple services to offer differentiated value propositions to customers.

Executive Summary - High-level overview and key findings about Logistics Service Market

The logistics service market is experiencing robust growth, driven by increasing globalization, e-commerce expansion, and technological advancements in supply chain management. The market is projected to grow from 1784.03 Billion in 2026 to 2828.83 Billion by 2033, representing a CAGR of 6.81% during the forecast period. This growth is fueled by rising demand across key end-user segments including healthcare, retail & consumer goods, and industrial manufacturing. The market is characterized by diverse service providers ranging from first-party to fifth-party logistics, offering solutions across multiple transportation modes. Digital transformation remains a key trend, with companies investing in automation, IoT, and AI to enhance operational efficiency. The competitive landscape is dominated by global players who are increasingly focusing on integrated solutions and sustainable practices to maintain their market positions. Regional markets are showing varied growth patterns, with emerging economies presenting significant opportunities for expansion.

Logistics Service Market Forecast - Projections for 2025-2032 period

The logistics service market is poised for substantial growth between 2025 and 2032, with projections indicating a significant expansion in market size and scope. Starting from a base of 1784.03 Billion in 2026, the market is expected to reach 2828.83 Billion by 2033, reflecting a compound annual growth rate (CAGR) of 6.81%. This growth trajectory is supported by several factors including the continued expansion of e-commerce, increasing adoption of advanced logistics technologies, and growing demand for integrated supply chain solutions. The forecast period will likely see accelerated investment in sustainable logistics practices and digital transformation initiatives across the industry. Regional markets are expected to show varying growth rates, with emerging economies potentially outpacing developed markets due to infrastructure development and increasing trade volumes. The market will also witness continued consolidation as larger players seek to enhance their capabilities and geographic reach through strategic acquisitions and partnerships.

Logistics Service Market Size and Share by Segmentation - Breakdown by {segmentData}

The logistics service market demonstrates diverse segmentation across end-users, logistics providers, and transportation modes. By end-user segments, retail & consumer goods represents a significant portion of the market, driven by e-commerce growth and changing consumer expectations. Industrial manufacturing follows closely, supported by global manufacturing trends and supply chain complexities. Healthcare logistics is experiencing rapid growth due to increased demand for medical supplies and pharmaceutical distribution. In terms of logistics providers, third-party logistics (3PL) services dominate the market, offering comprehensive solutions to businesses seeking to outsource their supply chain operations. Fourth-party logistics (4PL) and fifth-party logistics (5PL) are gaining traction as companies seek more integrated and technology-driven solutions. Regarding transportation modes, roadways maintain the largest share due to their flexibility and cost-effectiveness, while waterways continue to dominate long-haul international shipping. Air transportation, though representing a smaller share, is crucial for time-sensitive deliveries and high-value goods.

Global Logistics Service Market Size and Share by Region - Geographic distribution

The global logistics service market exhibits distinct regional characteristics and growth patterns across different geographic areas. North America and Europe represent mature markets with sophisticated logistics infrastructure and high technology adoption rates. These regions are characterized by strong e-commerce penetration and advanced supply chain management practices. The Asia-Pacific region is emerging as a key growth driver, fueled by rapid industrialization, expanding manufacturing sectors, and increasing international trade volumes, particularly in countries like China and India. Latin America presents opportunities for market expansion, though challenges include infrastructure development and regulatory complexities. The Middle East and Africa region, while currently representing a smaller market share, shows potential for growth driven by economic diversification efforts and increasing trade activities. Regional market dynamics are influenced by factors such as trade agreements, infrastructure development, and technological adoption rates, with emerging markets potentially outpacing developed regions in terms of growth rate.

Regional Analysis of the Logistics Service Market - Detailed regional market performance

Regional analysis of the logistics service market reveals distinct performance patterns and growth opportunities across different geographic areas. North America demonstrates strong market performance driven by advanced infrastructure, high e-commerce penetration, and technological innovation in supply chain management. The region's focus on last-mile delivery solutions and sustainable logistics practices continues to shape market dynamics. Europe maintains a significant market presence, characterized by sophisticated logistics networks and strict regulatory frameworks promoting sustainable transportation. The region's emphasis on green logistics and cross-border trade facilitation supports steady market growth. Asia-Pacific emerges as the fastest-growing region, propelled by rapid industrialization, expanding manufacturing capabilities, and increasing international trade volumes. Countries like China and India are investing heavily in logistics infrastructure to support their growing economies. Latin America presents a mixed picture, with Brazil and Mexico leading market development, though challenges persist in terms of infrastructure and regulatory environments. The Middle East and Africa region shows potential for growth, particularly in countries investing in economic diversification and trade infrastructure development.

Leading Company Profiles in the Logistics Service Market - Industry players and strategies

The logistics service market is dominated by several key players who have established strong global presence through comprehensive service offerings and extensive networks. A.P. MOLLER - MAERSK leads the market with its integrated shipping and logistics solutions, focusing on end-to-end supply chain management and digital transformation initiatives. DHL International GmbH maintains its competitive edge through diverse service portfolio spanning express delivery, freight transportation, and supply chain solutions. FedEx continues to innovate in last-mile delivery and e-commerce logistics, while United Parcel Service (UPS) leverages its extensive ground network and technology investments. KUEHNE + NAGEL distinguishes itself through specialized logistics services and strong presence in air and sea freight. C.H. Robinson Worldwide, Inc. excels in third-party logistics with its technology-driven platform approach. These companies are increasingly focusing on sustainability initiatives, digital transformation, and strategic partnerships to enhance their market positions and address evolving customer needs.

Porter's Five Forces Analysis of the Logistics Service Market - Competitive forces assessment

Porter's Five Forces analysis reveals the competitive dynamics shaping the logistics service market. The threat of new entrants remains moderate due to high capital requirements, complex regulatory environments, and the need for established networks and relationships. However, technological advancements are lowering barriers to entry in certain segments, particularly in digital freight brokerage and last-mile delivery services. The bargaining power of buyers is increasing as customers demand more integrated solutions, transparency, and competitive pricing, particularly in the e-commerce sector. Suppliers, including transportation providers and technology vendors, maintain moderate bargaining power, though this varies by region and service type. The threat of substitutes exists through alternative transportation modes and in-house logistics capabilities, though comprehensive logistics services remain difficult to replace. Competitive rivalry is intense, characterized by price competition, service differentiation, and technological innovation among major players seeking to expand their market share and geographic presence.

SWOT Analysis of the Logistics Service Market - Strengths, weaknesses, opportunities, threats

The logistics service market exhibits distinct strengths, weaknesses, opportunities, and threats that shape its competitive landscape. Strengths include the industry's critical role in global trade, extensive established networks, and increasing technological capabilities for supply chain optimization. The market benefits from growing e-commerce demand and the essential nature of logistics services across all economic sectors. However, weaknesses persist in the form of high operational costs, complex regulatory environments, and vulnerability to economic fluctuations and geopolitical tensions. Opportunities abound in digital transformation, sustainable logistics solutions, and emerging markets with growing trade volumes. The industry can capitalize on technological advancements in automation, IoT, and AI to enhance efficiency and service offerings. Threats include intense competition, potential supply chain disruptions, and the risk of technological obsolescence. Additionally, environmental regulations and the need for sustainable practices present both challenges and opportunities for market participants.

Logistics Service Market Value Chain Analysis - Industry structure and value flow

The logistics service market value chain encompasses a complex network of activities that create and deliver value to end customers. At the foundation lie raw material suppliers and component manufacturers who initiate the supply chain process. Primary activities include inbound logistics, operations, outbound logistics, marketing and sales, and service delivery. Support activities comprise infrastructure development, human resource management, technology development, and procurement. Key intermediaries in the value chain include freight forwarders, warehousing providers, and transportation companies who facilitate the movement of goods across different modes. Technology providers play an increasingly crucial role, offering solutions for supply chain visibility, route optimization, and warehouse management. The value chain is characterized by growing integration and collaboration among participants, driven by the need for end-to-end supply chain solutions. Digital platforms are transforming traditional value chain structures, enabling more efficient matching of supply and demand while reducing intermediaries and enhancing transparency.

Key Investment Insights in the Logistics Service Market - Strategic investment recommendations

Strategic investment insights for the logistics service market highlight several key areas for potential growth and value creation. Investment in digital infrastructure and technology platforms represents a critical opportunity, particularly in areas such as real-time tracking systems, predictive analytics, and automated warehouse solutions. The market is witnessing increased investment in sustainable logistics solutions, including electric vehicles and green warehousing, driven by environmental regulations and corporate sustainability goals. Emerging markets present significant investment potential, particularly in regions with growing manufacturing sectors and improving infrastructure. Strategic partnerships and acquisitions are recommended for companies seeking to expand their geographic presence or enhance service capabilities. Investment in last-mile delivery solutions and cold chain logistics is particularly attractive given the growth of e-commerce and healthcare distribution. Companies should also consider investing in workforce development and training to address the industry's skills gap and prepare for technological advancements.

Logistics Service Market Conclusion - Summary and key takeaways

The logistics service market presents a dynamic and evolving landscape characterized by robust growth, technological innovation, and changing customer expectations. With a projected CAGR of 6.81% from 2026 to 2033, the market is set to expand significantly, driven by e-commerce growth, globalization, and increasing demand for integrated supply chain solutions. The industry is undergoing a digital transformation, with investments in automation, IoT, and AI reshaping traditional logistics operations. Sustainability has emerged as a key focus area, influencing both operational practices and strategic decisions. The competitive landscape remains intense, with major players focusing on technological advancement, geographic expansion, and service diversification to maintain their market positions. Regional markets show varied growth patterns, with emerging economies presenting significant opportunities for expansion. Success in this market will increasingly depend on companies' ability to offer integrated, technology-driven solutions while maintaining operational efficiency and sustainability.

Research Methodology - How this research was conducted

The research methodology employed for this market analysis combines multiple approaches to ensure comprehensive and accurate insights. Primary research involved interviews with industry experts, logistics service providers, and end-users to gather firsthand information about market trends, challenges, and opportunities. Secondary research encompassed analysis of industry reports, company annual reports, regulatory documents, and trade publications to validate findings and provide historical context. Market size and growth projections were derived using both top-down and bottom-up approaches, considering various factors including end-user demand, technological adoption rates, and economic indicators. Data triangulation was employed to cross-verify information from multiple sources, ensuring reliability of the findings. The research also incorporated Porter's Five Forces analysis and SWOT analysis to provide strategic insights into market dynamics. Geographic analysis considered regional economic conditions, trade patterns, and infrastructure development to assess market potential across different areas.

Research Scope - Coverage and limitations

The research scope encompasses a comprehensive analysis of the global logistics service market, covering key segments including end-users, logistics providers, and transportation modes. The study examines market dynamics from 2026 to 2033, with particular focus on growth trends, competitive landscape, and regional variations. Coverage includes major market players, emerging technologies, and strategic developments shaping the industry. However, the research has certain limitations, including the exclusion of highly specialized niche logistics services and micro-regional variations in market conditions. The analysis primarily focuses on commercial logistics services and does not extensively cover military or government-specific logistics operations. Additionally, while the research provides broad geographic coverage, some developing regions may have limited available data due to reporting constraints. The study's projections are based on current market conditions and assumptions about future economic and technological developments, which may be subject to change based on unforeseen global events or market disruptions.

Key Companies and Recent Developments in the Logistics Service Market - Introduction to top companies and their recent announcements, product launches, partnerships, and strategic developments

The logistics service market features several prominent companies driving innovation and market growth through strategic initiatives. A.P. MOLLER - MAERSK has recently announced significant investments in digital supply chain solutions and sustainable shipping technologies, including partnerships with technology companies to enhance real-time visibility. DHL International GmbH continues to expand its e-commerce logistics capabilities, launching new automated sorting facilities and last-mile delivery solutions in key markets. FedEx has introduced advanced robotics in its warehouses and expanded its cold chain logistics network to meet growing healthcare distribution needs. United Parcel Service (UPS) has announced strategic partnerships for drone delivery testing and investments in alternative fuel vehicles for its ground fleet. KUEHNE + NAGEL has strengthened its position through acquisitions of specialized logistics providers and investments in digital freight platforms. C.H. Robinson Worldwide, Inc. has launched new AI-powered supply chain analytics tools and expanded its network of carrier partners. These companies are increasingly focusing on sustainability initiatives, with many announcing carbon neutrality goals and investments in electric vehicle fleets. Recent developments also include strategic alliances between traditional logistics providers and technology companies to create integrated supply chain solutions, reflecting the industry's shift toward digital transformation and end-to-end service offerings.