5G Chipset Market Overview - Definition, scope, and significance

5G chipsets are specialized integrated circuits designed to enable devices to connect to 5G networks, facilitating high-speed data transmission, low latency, and massive device connectivity. These chipsets are fundamental components in smartphones, tablets, laptops, IoT devices, and infrastructure equipment, serving as the backbone of the 5G ecosystem. The 5G chipset market encompasses the design, manufacturing, and distribution of these critical components across various frequency bands and process nodes, supporting the global transition to next-generation wireless communication standards.

5G Chipset Market Drivers, Restraints, Challenges, and Opportunities - Key growth factors and obstacles

The primary drivers of the 5G chipset market include the accelerating global deployment of 5G infrastructure, increasing consumer demand for high-speed connectivity, and the proliferation of 5G-enabled devices across multiple sectors. The growing adoption of IoT applications, autonomous vehicles, and smart city initiatives further propels market growth. However, challenges such as high development costs, complex manufacturing processes, and supply chain disruptions pose significant restraints. The market also faces challenges related to spectrum allocation, regulatory compliance, and the need for continuous innovation to meet evolving 5G standards. Despite these obstacles, opportunities abound in emerging markets, enterprise applications, and the development of advanced chipset technologies supporting higher frequencies and improved energy efficiency.

5G Chipset Market Growth Trends - Current and emerging trends shaping the market

Current growth trends in the 5G chipset market are characterized by the rapid advancement of semiconductor process technologies, with manufacturers focusing on developing chipsets using less than 10nm process nodes for enhanced performance and power efficiency. The market is witnessing a shift towards integrated solutions that combine modem and RF capabilities, reducing device complexity and improving energy consumption. Another significant trend is the increasing demand for chipsets supporting multiple frequency bands, including sub-6 GHz and mmWave frequencies, to ensure comprehensive 5G coverage. The emergence of standalone 5G networks and the evolution towards 5G Advanced (5.5G) standards are driving innovation in chipset design, with manufacturers focusing on AI-enabled capabilities and enhanced security features.

COVID-19 Impact on the 5G Chipset Market - Pandemic effects and recovery trajectory

The COVID-19 pandemic initially disrupted the 5G chipset market through supply chain interruptions, manufacturing delays, and reduced consumer spending on electronic devices. However, the pandemic ultimately accelerated digital transformation across industries, creating renewed demand for 5G connectivity to support remote work, telemedicine, and online education. The recovery trajectory has been marked by increased investments in 5G infrastructure, particularly in emerging markets, and a surge in demand for 5G-enabled devices as economies reopened. The pandemic also highlighted the importance of resilient supply chains, prompting manufacturers to diversify their supplier base and invest in localized production capabilities.

5G Chipset Market Competitive Landscape - Major competitors and market consolidation

The 5G chipset market features a competitive landscape dominated by established semiconductor giants and specialized 5G technology providers. Key players include Qualcomm Technologies, Inc., MediaTek Inc., Samsung, Intel Corporation, and Huawei Device Co., Ltd., each competing for market share through technological innovation and strategic partnerships. The market has witnessed significant consolidation activities, with companies acquiring specialized firms to enhance their 5G capabilities and expand their product portfolios. Competition is intensifying as new entrants emerge, particularly from China and other Asian markets, challenging the dominance of traditional players and driving innovation in areas such as power efficiency, integration, and support for emerging 5G use cases.

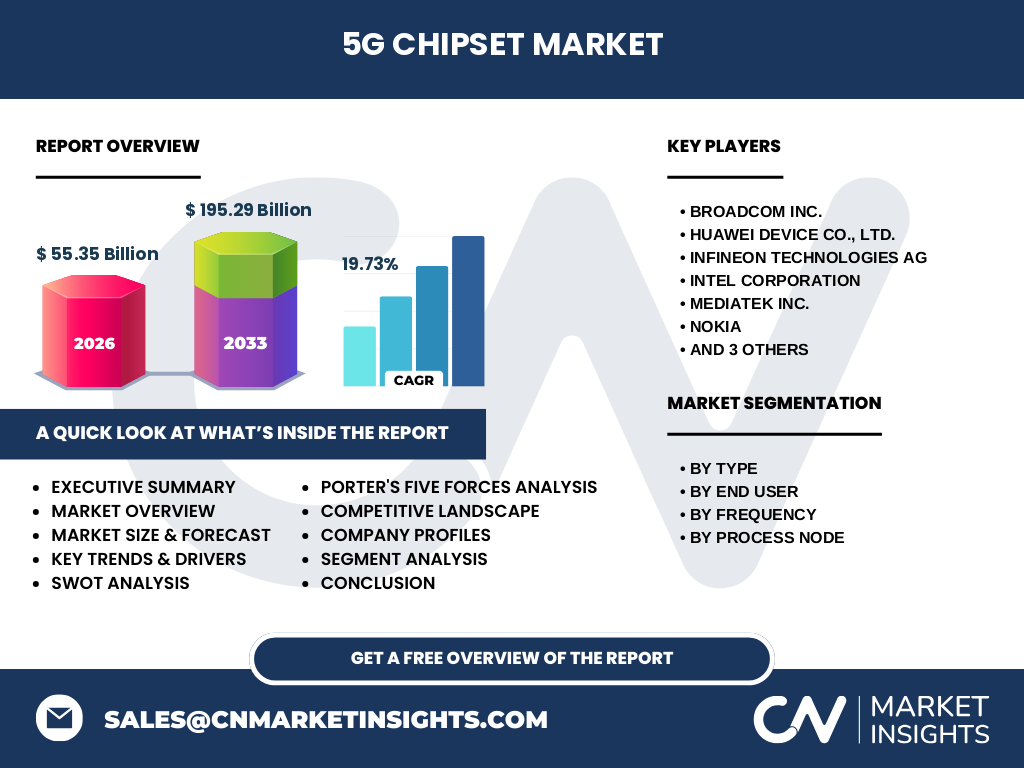

Executive Summary - High-level overview and key findings about 5G Chipset Market

The 5G chipset market is experiencing robust growth, driven by the global rollout of 5G networks and increasing demand for high-speed connectivity across consumer and enterprise applications. The market is projected to grow from $55.35 billion in 2026 to $195.29 billion by 2033, representing a CAGR of 19.73%. This growth is supported by technological advancements in semiconductor manufacturing, expanding 5G infrastructure, and the proliferation of 5G-enabled devices across various end-user segments. The market's evolution is characterized by increasing integration, support for multiple frequency bands, and the development of energy-efficient solutions to meet the diverse needs of the 5G ecosystem.

5G Chipset Market Forecast - Projections for 2025-2032 period

The 5G chipset market is poised for substantial growth between 2025 and 2032, with projections indicating a market size of $195.29 billion by 2033, up from $55.35 billion in 2026. This represents a compound annual growth rate (CAGR) of 19.73% over the forecast period. The growth trajectory is supported by continued investments in 5G infrastructure, increasing adoption of 5G-enabled devices, and the expansion of 5G applications across various industries. The forecast period will likely see accelerated innovation in chipset technologies, with a focus on supporting advanced 5G features, improving energy efficiency, and enabling new use cases in areas such as IoT, autonomous vehicles, and industrial automation.

5G Chipset Market Size and Share by Segmentation - Breakdown by {segmentData}

The 5G chipset market is segmented by type, end user, frequency, and process node, each contributing differently to the overall market size and share. By type, the market includes modem and RFIC chipsets, with modems dominating due to their essential role in 5G connectivity. The end-user segmentation spans IT & Telecom, Manufacturing, Media & Entertainment, Healthcare, and Energy & Utilities, with IT & Telecom holding the largest share due to the primary deployment of 5G in communication networks and devices. Frequency segmentation includes sub-6 GHz, 24-29 GHz, and above 39 GHz bands, with sub-6 GHz chipsets commanding a significant market share due to their widespread coverage capabilities. Process node segmentation ranges from less than 10nm to above 28nm, with chipsets using less than 10nm process nodes gaining traction for their superior performance and power efficiency.

Global 5G Chipset Market Size and Share by Region - Geographic distribution

The global 5G chipset market exhibits distinct regional characteristics, with Asia-Pacific leading in terms of market size and growth potential, followed by North America and Europe. Asia-Pacific's dominance is attributed to the presence of major semiconductor manufacturers, rapid 5G infrastructure deployment, and large consumer markets in countries like China, South Korea, and Japan. North America follows with significant market share, driven by early 5G adoption, technological innovation, and substantial investments in 5G infrastructure. Europe represents a mature market with steady growth, supported by regulatory initiatives promoting 5G deployment and digital transformation across industries. Emerging markets in Latin America, Middle East, and Africa are also showing promising growth potential as 5G networks expand and device affordability improves.

Regional Analysis of the 5G Chipset Market - Detailed regional market performance

Regional analysis of the 5G chipset market reveals distinct growth patterns and market dynamics across different geographical areas. Asia-Pacific leads the market, driven by aggressive 5G deployment strategies in China, South Korea, and Japan, coupled with the presence of major chipset manufacturers like Samsung and MediaTek. North America follows closely, with the United States spearheading 5G adoption through substantial investments in infrastructure and a competitive device market dominated by Qualcomm and Intel. Europe shows steady growth, with countries like Germany, the UK, and France focusing on industrial 5G applications and smart city initiatives. Emerging regions such as Latin America and Africa are experiencing increasing demand for 5G chipsets as network coverage expands and device costs decrease, presenting significant growth opportunities for market players.

Leading Company Profiles in the 5G Chipset Market - Industry players and strategies

The 5G chipset market is characterized by the presence of several key players, each employing distinct strategies to maintain and expand their market positions. Qualcomm Technologies, Inc. leads with its Snapdragon series, focusing on premium smartphone and IoT applications. MediaTek Inc. has gained significant market share by offering cost-effective solutions for mid-range devices and expanding into automotive and IoT segments. Samsung leverages its integrated device and chipset capabilities to provide comprehensive 5G solutions. Intel Corporation focuses on infrastructure and enterprise applications, while Huawei Device Co., Ltd. maintains a strong presence in the Chinese market and emerging economies. These companies are investing heavily in R&D, forming strategic partnerships, and pursuing vertical integration to strengthen their competitive positions in the rapidly evolving 5G chipset landscape.

Porter's Five Forces Analysis of the 5G Chipset Market - Competitive forces assessment

Porter's Five Forces analysis of the 5G chipset market reveals a highly competitive environment with significant barriers to entry due to high capital requirements and complex technological expertise. The bargaining power of buyers is moderate, as device manufacturers have multiple chipset options but face switching costs and compatibility issues. Suppliers of raw materials and manufacturing equipment wield considerable power due to the specialized nature of semiconductor production. The threat of new entrants is relatively low, given the substantial investments required in R&D and manufacturing infrastructure. However, the threat of substitutes is minimal as 5G chipsets are essential for 5G connectivity, and competitive rivalry among existing players is intense, driving continuous innovation and price competition.

SWOT Analysis of the 5G Chipset Market - Strengths, weaknesses, opportunities, threats

The 5G chipset market exhibits several strengths, including rapid technological advancements, increasing global 5G adoption, and the essential nature of chipsets in enabling 5G connectivity. However, weaknesses such as high development costs, complex manufacturing processes, and supply chain vulnerabilities pose challenges to market growth. Opportunities abound in emerging markets, enterprise applications, and the development of advanced chipset technologies supporting higher frequencies and improved energy efficiency. Threats to the market include geopolitical tensions affecting supply chains, regulatory challenges, and the potential for technological disruptions that could render current solutions obsolete. The market's ability to navigate these factors will determine its long-term success and growth trajectory.

5G Chipset Market Value Chain Analysis - Industry structure and value flow

The 5G chipset value chain encompasses several key stages, from semiconductor design and manufacturing to distribution and end-user applications. The chain begins with semiconductor design houses and IP providers, who create the foundational technologies for 5G chipsets. This is followed by chip fabrication, testing, and packaging, primarily carried out by specialized foundries and OSAT (Outsourced Semiconductor Assembly and Test) companies. The finished chipsets are then distributed to device manufacturers, who integrate them into smartphones, tablets, IoT devices, and infrastructure equipment. The value chain also includes software developers who create drivers and optimization tools, as well as network operators who deploy 5G infrastructure. Each stage of the value chain contributes to the overall market dynamics, with opportunities for value creation and potential bottlenecks that can impact market growth.

Key Investment Insights in the 5G Chipset Market - Strategic investment recommendations

Strategic investment insights for the 5G chipset market highlight several key areas for potential growth and returns. Investors should focus on companies developing advanced process node technologies (less than 10nm) that offer superior performance and power efficiency. The growing demand for integrated modem-RF solutions presents investment opportunities in companies that can deliver comprehensive, energy-efficient chipsets. Emerging markets in Asia-Pacific and Latin America offer significant growth potential as 5G networks expand and device affordability improves. Additionally, investments in companies developing chipsets for specific vertical applications, such as automotive, industrial IoT, and smart cities, could yield substantial returns as these sectors increasingly adopt 5G technology. Strategic partnerships and vertical integration within the value chain are also key areas to watch for investment opportunities.

5G Chipset Market Conclusion - Summary and key takeaways

The 5G chipset market is positioned for substantial growth, driven by the global expansion of 5G networks and increasing demand for high-speed connectivity across various applications. With a projected market size of $195.29 billion by 2033 and a CAGR of 19.73%, the market presents significant opportunities for innovation and investment. Key trends include the development of advanced process node technologies, integration of modem and RF capabilities, and support for multiple frequency bands. While challenges such as high development costs and supply chain complexities exist, the market's strengths and opportunities outweigh these obstacles. As 5G technology continues to evolve and new use cases emerge, the chipset market will play a crucial role in enabling the next generation of wireless communication and digital transformation across industries.

Research Methodology - How this research was conducted

This market research was conducted using a comprehensive methodology that combines primary and secondary research techniques. Primary research involved interviews with industry experts, semiconductor manufacturers, and end-users to gather firsthand insights into market trends, challenges, and opportunities. Secondary research included analysis of industry reports, company financial statements, patent filings, and regulatory documents to validate and supplement primary findings. Market size and growth projections were derived using a combination of top-down and bottom-up approaches, considering factors such as 5G infrastructure deployment rates, device shipment forecasts, and technological advancements in semiconductor manufacturing. The research also incorporated Porter's Five Forces analysis and SWOT analysis to provide a holistic view of the market dynamics and competitive landscape.

Research Scope - Coverage and limitations

The research scope for this 5G chipset market analysis encompasses a comprehensive examination of the global market, including detailed segmentation by type, end user, frequency, and process node. The study covers major geographical regions, with a focus on key markets in North America, Europe, Asia-Pacific, and emerging economies. The research timeframe extends from 2025 to 2032, with historical data and future projections provided to offer a complete market perspective. However, it's important to note that the research is limited by the availability of public data on certain market segments and regional performances. Additionally, the rapidly evolving nature of 5G technology and potential geopolitical factors may impact future market dynamics in ways that are difficult to predict with complete accuracy.

Key Companies and Recent Developments in the 5G Chipset Market - Introduction to top companies and their recent announcements, product launches, partnerships, and strategic developments

The 5G chipset market is dominated by several key players who are driving innovation and shaping the industry's future. Broadcom Inc. has been focusing on developing advanced RF solutions for 5G infrastructure, with recent announcements highlighting their progress in 5G baseband processors. Huawei Device Co., Ltd. continues to strengthen its position in the Chinese market and emerging economies, despite facing international challenges. Infineon Technologies AG has been expanding its portfolio of power management solutions for 5G devices, with recent product launches emphasizing energy efficiency. Intel Corporation has refocused its 5G strategy on infrastructure and edge computing applications, forming strategic partnerships to enhance its market presence. MediaTek Inc. has gained significant market share with its Dimensity series, targeting mid-range smartphones and expanding into automotive and IoT segments. Nokia has been strengthening its position in 5G infrastructure, with recent developments focusing on Open RAN solutions. Qualcomm Technologies, Inc. continues to lead in premium smartphone chipsets with its Snapdragon series, while also expanding into automotive and IoT markets. Samsung leverages its integrated device and chipset capabilities to provide comprehensive 5G solutions, with recent announcements highlighting advancements in mmWave technology. Unisoc (Shanghai) Technologies Co., Ltd. has been gaining traction in emerging markets with cost-effective 5G solutions, forming partnerships to expand its global presence. These companies' recent developments underscore the dynamic nature of the 5G chipset market and the ongoing efforts to address evolving technological and market demands.