Automotive Composite Market Overview - Definition, scope, and significance

The Automotive Composite Market represents a specialized segment within the automotive industry focused on advanced composite materials used in vehicle manufacturing. These composites combine two or more constituent materials with significantly different physical or chemical properties, creating components that exhibit characteristics superior to individual materials. The market encompasses various composite types including carbon fiber composites, glass fiber composites, and other fiber-reinforced materials, along with different resin systems such as thermoset and thermoplastic formulations. The significance of this market lies in its ability to address critical automotive industry challenges including weight reduction, fuel efficiency improvement, enhanced performance, and sustainability goals. As automotive manufacturers worldwide strive to meet increasingly stringent emissions regulations and consumer demands for higher performance vehicles, composite materials have emerged as essential solutions that enable innovation in vehicle design and manufacturing processes.

Automotive Composite Market Drivers, Restraints, Challenges, and Opportunities - Key growth factors and obstacles

The Automotive Composite Market experiences multiple drivers propelling its growth, including stringent government regulations on vehicle emissions, increasing consumer demand for fuel-efficient vehicles, and the automotive industry's shift toward lightweight materials. The rising adoption of electric vehicles presents significant opportunities, as composites help offset battery weight while providing structural integrity. Additionally, technological advancements in manufacturing processes and material science continue to reduce production costs and improve material properties. However, the market faces several restraints and challenges, including high initial costs of composite materials compared to traditional alternatives, complex manufacturing processes requiring specialized equipment and skilled labor, and recycling difficulties associated with certain composite types. The market also encounters challenges related to supply chain disruptions, raw material price volatility, and the need for standardization across different applications. Opportunities exist in emerging markets, particularly in Asia-Pacific regions where automotive production is expanding rapidly, and in the development of sustainable and recyclable composite materials that align with circular economy principles.

Automotive Composite Market Growth Trends - Current and emerging trends shaping the market

The Automotive Composite Market is experiencing several transformative growth trends that are reshaping the industry landscape. One prominent trend is the increasing integration of advanced manufacturing technologies such as automated fiber placement, resin transfer molding, and 3D printing, which are improving production efficiency and reducing costs. Another significant trend is the growing focus on sustainable and recyclable composite materials, driven by environmental regulations and corporate sustainability initiatives. The market is also witnessing a shift toward thermoplastic composites, which offer advantages in terms of recyclability, faster processing times, and improved damage tolerance compared to traditional thermoset materials. Additionally, the rise of electric and autonomous vehicles is creating new demand patterns, as these vehicles require specialized composite solutions for battery enclosures, structural components, and sensor housings. The trend toward vehicle lightweighting continues to accelerate, with manufacturers increasingly adopting multi-material strategies that combine composites with metals and other materials to optimize performance characteristics. Furthermore, the development of hybrid composite systems that combine different fiber types and resin systems is gaining traction, offering enhanced material properties tailored to specific automotive applications.

COVID-19 Impact on the Automotive Composite Market - Pandemic effects and recovery trajectory

The COVID-19 pandemic significantly impacted the Automotive Composite Market through multiple channels, creating both immediate disruptions and longer-term structural changes. During the initial outbreak phases, the market experienced severe supply chain disruptions, manufacturing facility closures, and sharp declines in automotive production volumes as lockdowns and social distancing measures were implemented globally. Many composite material suppliers faced raw material shortages and transportation bottlenecks, while automotive manufacturers reduced or suspended production, directly affecting composite component demand. However, the market has demonstrated resilience and is following a recovery trajectory characterized by several key developments. The pandemic accelerated digital transformation initiatives, with increased adoption of virtual design tools, simulation software, and remote collaboration platforms in composite material development and testing. Additionally, the crisis highlighted the importance of supply chain resilience, leading to increased regionalization of manufacturing and diversification of supplier bases. The recovery has been supported by government stimulus packages focused on green technologies and electric vehicle adoption, which typically incorporate higher composite material content. As automotive production volumes return to pre-pandemic levels and beyond, the composite market is experiencing renewed growth momentum, with many manufacturers accelerating their lightweighting and sustainability initiatives that were temporarily paused during the crisis.

Automotive Composite Market Competitive Landscape - Major competitors and market consolidation

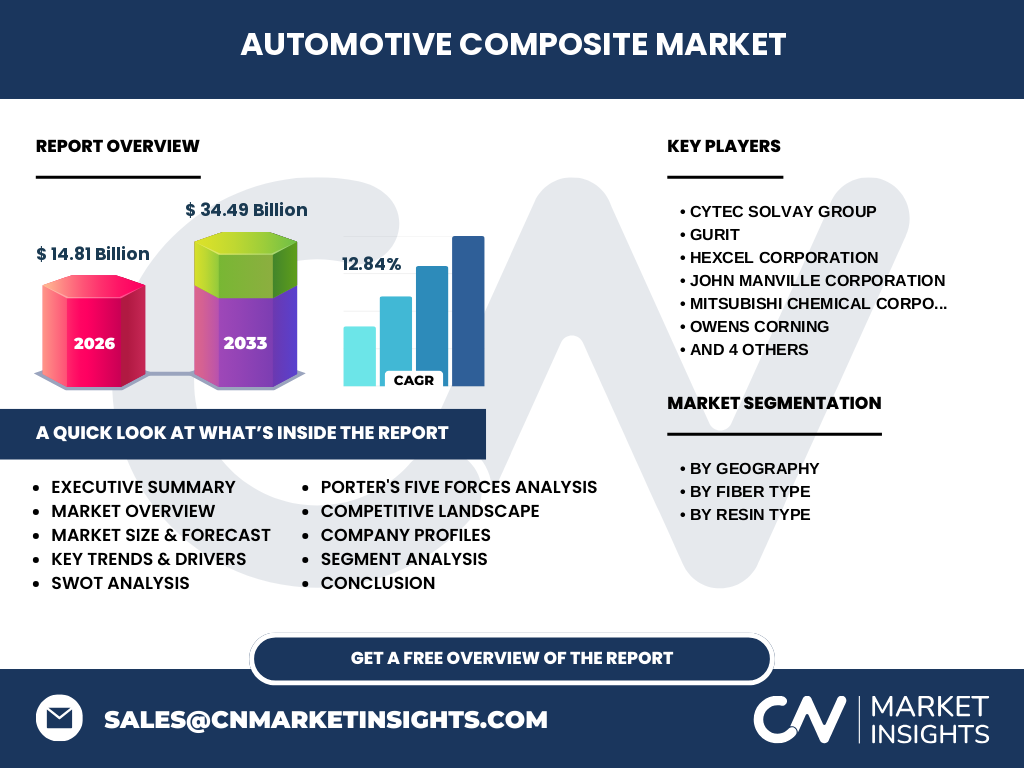

The Automotive Composite Market features a competitive landscape characterized by a mix of established multinational corporations and specialized composite material manufacturers competing for market share. The market demonstrates moderate consolidation, with several key players holding significant positions while allowing space for niche specialists and regional competitors. Major competitors in this space include companies such as Cytec Solvay Group, Gurit, Hexcel Corporation, John Manville Corporation, Mitsubishi Chemical Corporation, Owens Corning, SGL Carbon, TEIJIN LIMITED, Toray Industries Inc., and Zoltek Carbon Fiber. These companies compete based on factors including product quality, technological innovation, manufacturing capabilities, global presence, and customer relationships. The competitive dynamics are influenced by ongoing research and development investments, strategic partnerships with automotive OEMs, and vertical integration strategies. Market consolidation is occurring through mergers, acquisitions, and strategic alliances as companies seek to expand their technological capabilities, geographic reach, and product portfolios. The competitive intensity is further heightened by the entry of new players, particularly from emerging markets, and the increasing demand for customized composite solutions tailored to specific automotive applications. Companies are also competing on sustainability credentials, with those offering recyclable and environmentally friendly composite materials gaining competitive advantages in markets with stringent environmental regulations.

Executive Summary - High-level overview and key findings about Automotive Composite Market

The Automotive Composite Market represents a dynamic and rapidly evolving segment within the global automotive industry, driven by the critical need for lightweight materials that enhance vehicle performance, fuel efficiency, and sustainability. The market is experiencing robust growth, with projections indicating expansion from 14.81 Billion in 2026 to 34.49 Billion by 2033, representing a compound annual growth rate of 12.84%. This growth is fueled by increasing automotive production, particularly in emerging markets, the accelerating adoption of electric vehicles, and stringent government regulations on vehicle emissions and fuel efficiency. The market segmentation reveals diverse opportunities across different fiber types, including carbon fiber composites and glass fiber composites, as well as various resin systems such as thermoset and thermoplastic formulations. Geographically, the market spans North America, Europe, Asia-Pacific, South and Central America, and the Middle East and Africa, with each region presenting unique growth dynamics and competitive landscapes. Key industry players are actively investing in research and development, strategic partnerships, and capacity expansions to capitalize on emerging opportunities. The market faces challenges including high material costs, complex manufacturing processes, and recycling concerns, but these are being addressed through technological innovations and sustainability initiatives. Overall, the Automotive Composite Market presents significant growth potential for stakeholders who can navigate the evolving technological, regulatory, and competitive landscape effectively.

Automotive Composite Market Forecast - Projections for 2025-2032 period

The Automotive Composite Market is projected to experience substantial growth throughout the 2025-2032 period, with market size expanding from 14.81 Billion to 34.49 Billion, representing a compound annual growth rate of 12.84%. This forecast reflects the increasing adoption of composite materials across various automotive applications, driven by the industry's ongoing transformation toward electrification, lightweighting, and sustainability. The growth trajectory is expected to be particularly strong in segments related to electric vehicle components, where composites play crucial roles in battery enclosures, structural reinforcements, and weight reduction strategies. Regional forecasts indicate varying growth rates across different geographic markets, with Asia-Pacific likely to demonstrate the highest growth due to expanding automotive production and increasing adoption of advanced materials. The forecast period will also see continued technological advancements that reduce production costs and expand the applicability of composite materials to new automotive components. Market dynamics during this period will be influenced by factors including raw material price fluctuations, technological innovations in manufacturing processes, evolving environmental regulations, and changing consumer preferences for vehicle performance and sustainability. The forecast assumes continued recovery from COVID-19 related disruptions and sustained investment in automotive innovation, particularly in electric and autonomous vehicle technologies that heavily rely on advanced composite materials.

Automotive Composite Market Size and Share by Segmentation - Breakdown by {segmentData}

The Automotive Composite Market exhibits diverse segmentation patterns across multiple dimensions, with each segment contributing uniquely to the overall market dynamics and growth trajectory. By fiber type, the market is segmented into carbon fiber composites, glass fiber composites, and other fiber types, with carbon fiber composites commanding premium positioning due to their superior strength-to-weight ratios and performance characteristics, while glass fiber composites maintain larger volume shares due to their cost-effectiveness and versatility. The resin type segmentation divides the market into thermoset and thermoplastic categories, with thermoset composites traditionally dominating due to their established manufacturing processes and material properties, while thermoplastic composites are experiencing rapid growth driven by their recyclability advantages and faster processing capabilities. By geography, the market spans North America, Europe, Asia-Pacific, South and Central America, and Middle East and Africa, with Asia-Pacific emerging as the largest and fastest-growing region due to expanding automotive production and increasing adoption of advanced materials. Each geographic segment demonstrates distinct growth patterns influenced by local automotive manufacturing trends, regulatory environments, and economic conditions. The segmentation analysis reveals that while premium segments like carbon fiber composites represent higher value opportunities, volume-driven segments such as glass fiber composites continue to provide substantial market opportunities, particularly in emerging economies where cost considerations remain paramount.

Global Automotive Composite Market Size and Share by Region - Geographic distribution

The global Automotive Composite Market demonstrates distinct regional characteristics and growth patterns across different geographic territories, reflecting variations in automotive manufacturing intensity, regulatory environments, and technological adoption rates. North America represents a mature market with significant adoption of advanced composite materials, driven by stringent fuel efficiency regulations, strong automotive manufacturing presence, and early adoption of electric vehicle technologies. Europe maintains a substantial market share characterized by aggressive emissions reduction targets, established automotive OEMs, and leadership in sustainable material development, with countries like Germany, France, and Italy serving as key hubs for composite innovation and application. The Asia-Pacific region emerges as the largest and fastest-growing market segment, propelled by expanding automotive production in China, Japan, South Korea, and India, along with increasing investments in electric vehicle manufacturing and infrastructure development. South and Central America presents a developing market with growth potential tied to automotive industry expansion and gradual adoption of advanced materials, while the Middle East and Africa region shows nascent but promising growth opportunities linked to diversification of automotive manufacturing capabilities and increasing focus on sustainable transportation solutions. The regional distribution reflects not only current market sizes but also varying growth trajectories, with emerging markets demonstrating higher growth rates as they modernize automotive manufacturing capabilities and adopt advanced material technologies.

Regional Analysis of the Automotive Composite Market - Detailed regional market performance

The regional analysis of the Automotive Composite Market reveals nuanced performance patterns and growth dynamics across different geographic territories. In North America, the market demonstrates steady growth driven by the presence of major automotive manufacturers, stringent Corporate Average Fuel Economy (CAFE) standards, and increasing electric vehicle production. The region benefits from advanced manufacturing infrastructure, strong research and development capabilities, and significant investments in lightweighting technologies. Europe presents a sophisticated market characterized by aggressive carbon reduction targets, established composite material expertise, and leadership in sustainable automotive technologies. Countries such as Germany, France, and Italy serve as innovation centers, with strong collaborations between automotive OEMs and composite material suppliers driving technological advancement. The Asia-Pacific region exhibits the most dynamic growth patterns, with China emerging as both a massive production hub and a significant consumer market for automotive composites. Japan and South Korea contribute advanced technological capabilities, while emerging markets in Southeast Asia present new growth opportunities. South and Central America shows gradual market development, with Brazil and Mexico leading automotive production and composite adoption, though growth remains constrained by economic volatility and infrastructure limitations. The Middle East and Africa region, while currently representing a smaller market share, demonstrates potential for growth through diversification initiatives and increasing focus on automotive manufacturing capabilities, particularly in countries like Morocco and South Africa that are developing as regional automotive production centers.

Leading Company Profiles in the Automotive Composite Market - Industry players and strategies

The Automotive Composite Market features several prominent industry players who have established significant market positions through strategic investments, technological innovation, and strong customer relationships. Cytec Solvay Group has positioned itself as a leader in advanced composite materials, focusing on high-performance solutions for automotive applications and leveraging its expertise in carbon fiber technologies. Gurit specializes in composite material manufacturing with a strong emphasis on sustainable solutions and has developed comprehensive product portfolios serving various automotive segments. Hexcel Corporation brings extensive experience in carbon fiber production and composite manufacturing, with particular strengths in aerospace-grade materials adapted for automotive applications. John Manville Corporation offers a diverse range of composite solutions with focus on glass fiber technologies and cost-effective manufacturing processes. Mitsubishi Chemical Corporation represents a major Japanese player with integrated capabilities across the composite value chain, from raw material production to finished components. Owens Corning maintains a strong presence in glass fiber composites with global manufacturing capabilities and extensive automotive industry experience. SGL Carbon specializes in carbon-based solutions with particular expertise in battery enclosure materials for electric vehicles. TEIJIN LIMITED brings Japanese technological excellence in advanced fiber technologies and composite material development. Toray Industries Inc. stands as a global leader in carbon fiber production with comprehensive automotive application capabilities. Zoltek Carbon Fiber focuses on providing cost-effective carbon fiber solutions for automotive mass production applications. These companies employ various strategic approaches including vertical integration, strategic partnerships with automotive OEMs, research and development investments, and geographic expansion to maintain and enhance their market positions.

Porter's Five Forces Analysis of the Automotive Composite Market - Competitive forces assessment

Porter's Five Forces analysis provides valuable insights into the competitive dynamics shaping the Automotive Composite Market. The threat of new entrants remains moderate to high due to significant capital requirements for manufacturing facilities, the need for specialized technical expertise, and established relationships between existing suppliers and automotive OEMs. However, technological advancements and the growing importance of sustainable materials create opportunities for innovative new players. The bargaining power of suppliers is relatively high, particularly for raw materials such as carbon fiber precursors and specialized resins, which are often produced by a limited number of suppliers with significant market influence. The bargaining power of buyers, primarily automotive manufacturers, is substantial due to their large purchase volumes, ability to switch suppliers, and increasing focus on cost reduction and supply chain optimization. The threat of substitute products exists through alternative lightweighting technologies such as advanced high-strength steels, aluminum alloys, and magnesium components, though composites often provide unique performance advantages that limit substitution potential. Competitive rivalry within the market is intense, characterized by price competition, technological innovation races, and efforts to secure long-term supply agreements with major automotive customers. The overall competitive intensity is further influenced by factors including market consolidation trends, the entry of new players from adjacent industries, and the increasing importance of sustainability credentials in supplier selection processes.

SWOT Analysis of the Automotive Composite Market - Strengths, weaknesses, opportunities, threats

A comprehensive SWOT analysis of the Automotive Composite Market reveals multiple internal and external factors influencing market dynamics and future prospects. Strengths of the market include the superior performance characteristics of composite materials, including exceptional strength-to-weight ratios, design flexibility, and corrosion resistance, which align well with automotive industry needs for lightweighting and performance enhancement. The market also benefits from strong technological foundations, established manufacturing capabilities, and growing expertise in composite material development and application. However, weaknesses include high material and processing costs compared to traditional alternatives, complex manufacturing processes requiring specialized equipment and skilled labor, and challenges associated with composite material recycling and end-of-life disposal. Opportunities abound in the growing electric vehicle market, where composites can help offset battery weight while providing structural benefits, and in the development of sustainable and recyclable composite materials that address environmental concerns. The market also benefits from increasing regulatory pressure for fuel efficiency and emissions reduction, which drives demand for lightweight materials. Threats include raw material price volatility, competition from alternative lightweighting technologies, potential supply chain disruptions, and the risk of technological obsolescence as new materials and manufacturing processes emerge. Additionally, the market faces challenges from economic uncertainties, trade tensions, and potential shifts in automotive manufacturing locations that could impact regional demand patterns.

Automotive Composite Market Value Chain Analysis - Industry structure and value flow

The Automotive Composite Market value chain encompasses multiple interconnected stages, each contributing distinct value and facing unique challenges and opportunities. The chain begins with raw material suppliers who provide essential inputs such as carbon fiber precursors, glass fibers, resins, and additives. These suppliers range from large chemical companies producing basic materials to specialized manufacturers focusing on high-performance fibers and advanced resin systems. The next stage involves composite material manufacturers who transform raw materials into usable forms through processes such as fiber production, weaving, resin formulation, and pre-impregnation. These manufacturers add significant value through material engineering, quality control, and customization for specific automotive applications. Component manufacturers then utilize these materials to produce finished composite parts through various manufacturing processes including compression molding, injection molding, and automated fiber placement. This stage involves substantial value addition through design optimization, tooling development, and quality assurance processes. Automotive OEMs represent the next critical link, integrating composite components into vehicle platforms while managing complex supply chain relationships and ensuring compliance with performance and safety standards. Supporting services throughout the value chain include research and development, testing and certification, logistics, and aftermarket support. The value chain is characterized by increasing collaboration and integration among participants, with trends toward vertical integration, strategic partnerships, and shared innovation initiatives aimed at reducing costs and accelerating technology development.

Key Investment Insights in the Automotive Composite Market - Strategic investment recommendations

The Automotive Composite Market presents compelling investment opportunities driven by strong growth projections, technological advancements, and shifting automotive industry dynamics. Strategic investment recommendations focus on several key areas that offer the highest potential returns and strategic value. First, investments in advanced manufacturing technologies such as automated fiber placement, resin transfer molding, and 3D printing represent critical opportunities to reduce production costs and improve manufacturing efficiency. These technologies can significantly enhance competitiveness by addressing one of the market's primary challenges: high production costs. Second, investments in sustainable and recyclable composite materials align with growing environmental regulations and consumer preferences, offering long-term growth potential as the industry transitions toward circular economy principles. Third, capacity expansions in high-growth regions, particularly Asia-Pacific, provide opportunities to capture emerging market demand and establish strong regional presence. Fourth, strategic partnerships and joint ventures with automotive OEMs can provide stable revenue streams and insights into future material requirements, while also facilitating technology transfer and market access. Fifth, investments in research and development focused on next-generation composite materials, including hybrid systems and bio-based materials, can create competitive advantages and open new market segments. Additionally, investments in digital technologies for design optimization, supply chain management, and quality control can improve operational efficiency and customer responsiveness. The most successful investment strategies will likely combine multiple approaches, focusing on technological leadership, geographic diversification, and strong customer relationships to capture the market's growth potential while managing associated risks.

Automotive Composite Market Conclusion - Summary and key takeaways

The Automotive Composite Market represents a dynamic and rapidly evolving sector within the broader automotive industry, characterized by strong growth projections, technological innovation, and shifting market dynamics. The market is poised for substantial expansion, with projections indicating growth from 14.81 Billion to 34.49 Billion by 2033, driven by a compound annual growth rate of 12.84%. This growth is fueled by the automotive industry's ongoing transformation toward electrification, lightweighting, and sustainability, with composite materials playing increasingly critical roles in addressing these challenges. The market segmentation reveals diverse opportunities across different fiber types, resin systems, and geographic regions, with Asia-Pacific emerging as the primary growth engine while established markets in North America and Europe continue to drive technological innovation. Key industry players are actively investing in research and development, strategic partnerships, and capacity expansions to capitalize on emerging opportunities and address market challenges. Despite facing obstacles including high costs, complex manufacturing processes, and recycling concerns, the market benefits from strong drivers such as stringent emissions regulations, electric vehicle adoption, and continuous technological advancements. The future outlook remains positive, with continued growth expected across all market segments and regions, supported by ongoing innovations in material science, manufacturing processes, and sustainable technologies. Success in this market will require companies to balance technological leadership with cost competitiveness, sustainability initiatives with performance requirements, and global expansion with regional customization.

Research Methodology - How this research was conducted

The research methodology employed for this Automotive Composite Market analysis combines multiple approaches to ensure comprehensive and accurate market insights. The primary research component involved extensive interviews and discussions with industry experts, composite material manufacturers, automotive OEMs, and supply chain participants to gather firsthand insights into market trends, challenges, and opportunities. These interactions provided valuable qualitative data on market dynamics, technological developments, and strategic initiatives. Secondary research encompassed a thorough review of industry reports, company publications, technical journals, patent filings, and regulatory documents to validate and supplement primary findings. Market size and growth projections were derived through a combination of top-down and bottom-up approaches, analyzing data from multiple sources including production volumes, material consumption patterns, and regional automotive manufacturing statistics. The segmentation analysis utilized both quantitative data on market shares and qualitative assessments of market positioning and competitive dynamics. Geographic analysis incorporated economic indicators, automotive production data, and regional regulatory frameworks to understand market variations across different territories. The research also employed analytical frameworks including Porter's Five Forces and SWOT analysis to provide structured assessments of market competitiveness and strategic positioning. Data triangulation techniques were applied throughout the research process to ensure accuracy and reliability of findings, with particular attention paid to reconciling discrepancies between different data sources and methodologies.

Research Scope - Coverage and limitations

The research scope for this Automotive Composite Market analysis encompasses a comprehensive examination of market dynamics, trends, and opportunities across multiple dimensions. The geographic coverage includes major automotive markets across North America, Europe, Asia-Pacific, South and Central America, and the Middle East and Africa, providing a global perspective on market developments and regional variations. The market segmentation analysis covers key categories including fiber types (carbon fiber composites, glass fiber composites, and others) and resin types (thermoset and thermoplastic), along with application areas and end-use segments. The research timeframe extends from historical data through current market conditions to future projections spanning 2025-2032, enabling both retrospective analysis and forward-looking insights. However, the research scope also acknowledges certain limitations, including the challenge of obtaining precise market data for certain emerging applications and regional markets where composite adoption is still developing. Additionally, the rapidly evolving nature of composite technologies and manufacturing processes means that some specific technical details may become outdated as new innovations emerge. The research focuses primarily on structural and semi-structural automotive applications, with limited coverage of non-structural uses such as interior components and aesthetic applications. Market size figures and growth projections are based on available data and analytical models, with inherent uncertainties associated with forecasting in a dynamic industry environment. Despite these limitations, the research provides a robust framework for understanding market dynamics and identifying key opportunities and challenges in the Automotive Composite Market.

Key Companies and Recent Developments in the Automotive Composite Market - Introduction to top companies and their recent announcements, product launches, partnerships, and strategic developments

The Automotive Composite Market features several key companies that have demonstrated leadership through strategic initiatives, technological innovations, and market expansion efforts. Cytec Solvay Group has recently announced advancements in high-performance composite materials specifically designed for electric vehicle applications, including new formulations that offer improved thermal management and structural integrity. The company has also expanded its manufacturing capabilities through strategic investments in production facilities to meet growing demand. Gurit has introduced innovative sustainable composite solutions, including bio-based resin systems and recyclable material formulations, aligning with increasing environmental regulations and customer sustainability requirements. The company has formed strategic partnerships with automotive OEMs to co-develop next-generation lightweighting solutions. Hexcel Corporation has launched new carbon fiber products with enhanced properties for automotive crash structures and battery enclosures, while also expanding its global manufacturing footprint to better serve key automotive markets. John Manville Corporation has announced new glass fiber composite technologies offering improved cost-performance ratios for mass-market vehicle applications, along with investments in automated manufacturing processes to increase production efficiency. Mitsubishi Chemical Corporation has unveiled advanced thermoplastic composite materials with superior recyclability characteristics, supported by new production capacity investments in key automotive regions. Owens Corning has introduced innovative hybrid composite systems combining different fiber types to optimize performance characteristics for specific automotive applications, while also strengthening its distribution network. SGL Carbon has launched specialized composite solutions for electric vehicle battery enclosures, addressing critical safety and performance requirements in the rapidly growing EV market. TEIJIN LIMITED has announced new aramid fiber composite technologies for automotive safety applications, complemented by strategic R&D investments in material innovation. Toray Industries Inc. has unveiled next-generation carbon fiber materials with improved manufacturing economics for automotive mass production, supported by capacity expansion projects. Zoltek Carbon Fiber has introduced cost-effective carbon fiber solutions targeting broader automotive market segments, along with strategic partnerships to enhance market penetration. These developments reflect the industry's focus on innovation, sustainability, and strategic growth initiatives to capitalize on emerging market opportunities.