Redistribution Layer Material Market Overview - Definition, scope, and significance

The Redistribution Layer (RDL) Material Market encompasses specialized materials used in semiconductor packaging to redistribute electrical connections and enhance device performance. RDL materials, including polyimide, polybenzoxazole, and benzocyclobutene, serve as dielectric and conductive layers that enable advanced packaging technologies such as fan-out wafer level packaging and 2.5D/3D IC packaging. These materials play a crucial role in modern electronics by facilitating miniaturization, improving electrical performance, and enabling the integration of multiple components in compact form factors. The market's significance lies in its support of emerging technologies like artificial intelligence, 5G communications, and Internet of Things (IoT) devices, where advanced packaging solutions are essential for meeting performance and size requirements.

Redistribution Layer Material Market Drivers, Restraints, Challenges, and Opportunities - Key growth factors and obstacles

The primary drivers of the Redistribution Layer Material Market include the increasing demand for advanced semiconductor packaging solutions, driven by the proliferation of smartphones, wearables, and other compact electronic devices. The growing adoption of 5G technology and artificial intelligence applications further fuels the need for sophisticated packaging materials that can handle higher frequencies and power densities. However, the market faces restraints such as the high cost of advanced RDL materials and the complexity of manufacturing processes. Challenges include the need for continuous innovation to meet evolving performance requirements and the potential supply chain disruptions affecting raw material availability. Opportunities exist in the development of next-generation materials with enhanced properties, such as improved thermal stability and lower dielectric constants, as well as expansion into emerging applications like automotive electronics and medical devices.

Redistribution Layer Material Market Growth Trends - Current and emerging trends shaping the market

Current growth trends in the Redistribution Layer Material Market are characterized by the increasing adoption of fan-out wafer level packaging (FOWLP) and 2.5D/3D IC packaging technologies. These advanced packaging methods are gaining traction due to their ability to improve device performance, reduce form factor, and enable heterogeneous integration of different components. Emerging trends include the development of ultra-thin and flexible RDL materials to support the growing demand for wearable devices and flexible electronics. Additionally, there is a focus on materials with enhanced thermal management properties to address the heat dissipation challenges in high-performance computing applications. The market is also witnessing a trend towards the integration of RDL materials with other advanced packaging technologies, such as through-silicon vias (TSVs) and embedded die packaging, to further improve device functionality and performance.

COVID-19 Impact on the Redistribution Layer Material Market - Pandemic effects and recovery trajectory

The COVID-19 pandemic had a significant impact on the Redistribution Layer Material Market, causing disruptions in the global supply chain and manufacturing operations. The initial lockdowns and restrictions led to temporary closures of semiconductor fabrication facilities and packaging plants, resulting in production delays and inventory shortages. However, the pandemic also accelerated the demand for certain electronic devices, particularly those used in remote work, online education, and healthcare applications, which indirectly supported the RDL material market. As the industry recovers, there is a renewed focus on building more resilient supply chains and increasing domestic production capabilities in various regions. The market is expected to rebound strongly, driven by the continued growth of 5G technology deployment, the expansion of data centers, and the increasing adoption of artificial intelligence and IoT devices, which all require advanced packaging solutions supported by RDL materials.

Redistribution Layer Material Market Competitive Landscape - Major competitors and market consolidation

The Redistribution Layer Material Market features a competitive landscape with several key players vying for market share. Major competitors include ASE Technology Holding Co Ltd., Amkor Technology Inc., Dupont De Nemours Inc., Fujifilm Holdings Corp., Infineon Technologies AG, JCET Group Co Ltd., NXP Semiconductors NV, SK Hynix Inc., Samsung Electronics Co Ltd., and Shin-Etsu Chemical Co Ltd. These companies are engaged in intense competition, focusing on product innovation, strategic partnerships, and mergers and acquisitions to strengthen their market positions. The market has seen some consolidation through strategic alliances and acquisitions, particularly aimed at expanding product portfolios and enhancing technological capabilities. For instance, collaborations between material suppliers and semiconductor manufacturers are becoming more common to develop customized RDL solutions for specific applications. The competitive landscape is further characterized by ongoing research and development efforts to introduce materials with improved performance characteristics, such as lower dielectric constants and better thermal stability, to meet the evolving demands of advanced packaging technologies.

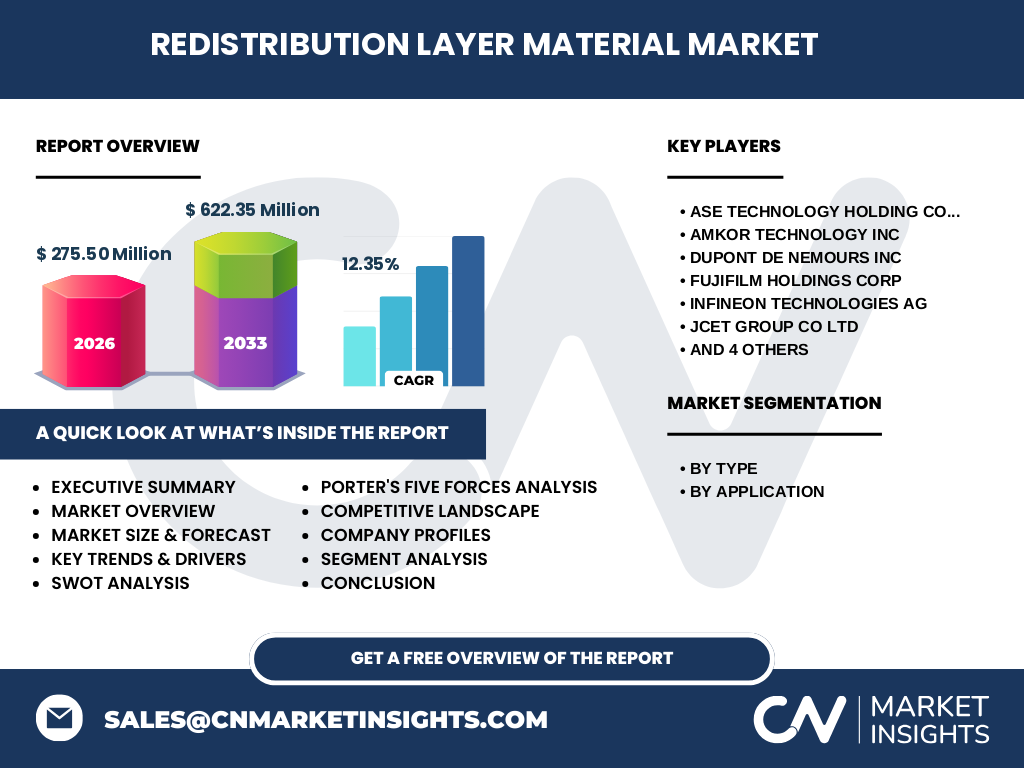

Executive Summary - High-level overview and key findings about Redistribution Layer Material Market

The Redistribution Layer Material Market is experiencing robust growth, driven by the increasing demand for advanced semiconductor packaging solutions in various high-tech applications. The market is characterized by a compound annual growth rate (CAGR) of 12.35%, with projections indicating significant expansion from 275.50 Million in 2026 to 622.35 Million by 2033. Key findings highlight the critical role of RDL materials in enabling miniaturization and performance enhancement in electronic devices, particularly in emerging technologies such as 5G, artificial intelligence, and Internet of Things (IoT). The market is segmented by type, including polyimide, polybenzoxazole, and benzocyclobutene, and by application, encompassing fan-out wafer level packaging and 2.5D/3D IC packaging. Leading companies in the market are focusing on innovation and strategic partnerships to maintain competitive advantages. Despite challenges such as high material costs and manufacturing complexities, the market presents significant opportunities for growth, particularly in the development of next-generation materials and expansion into new application areas like automotive electronics and medical devices.

Redistribution Layer Material Market Forecast - Projections for 2025-2032 period

The Redistribution Layer Material Market is poised for substantial growth over the 2025-2032 period, with projections indicating a robust expansion trajectory. Starting from a market size of 275.50 Million in 2026, the market is expected to reach 622.35 Million by 2033, reflecting a compound annual growth rate (CAGR) of 12.35%. This growth is driven by several factors, including the increasing adoption of advanced packaging technologies, the proliferation of 5G networks, and the rising demand for high-performance computing applications. The forecast period is likely to witness significant investments in research and development, leading to the introduction of innovative RDL materials with enhanced properties. Additionally, the market is expected to benefit from the growing trend of miniaturization in electronics and the increasing integration of artificial intelligence and IoT devices across various industries. Geographically, while Asia-Pacific is expected to maintain its dominance due to the presence of major semiconductor manufacturing hubs, other regions such as North America and Europe are also projected to experience substantial growth, driven by advancements in automotive electronics and the expansion of data centers.

Redistribution Layer Material Market Size and Share by Segmentation - Breakdown by {segmentData}

The Redistribution Layer Material Market is segmented by type and application, each contributing to the overall market dynamics. By type, the market is divided into polyimide, polybenzoxazole, and benzocyclobutene materials. Polyimide currently holds a significant share of the market due to its excellent thermal stability and chemical resistance, making it suitable for a wide range of applications. However, polybenzoxazole is gaining traction due to its lower dielectric constant and improved electrical properties, which are crucial for high-frequency applications. By application, the market is segmented into fan-out wafer level packaging (FOWLP) and 2.5D/3D IC packaging. FOWLP currently dominates the market share, driven by its widespread adoption in mobile devices and consumer electronics. The 2.5D/3D IC packaging segment is expected to witness the highest growth rate during the forecast period, fueled by the increasing demand for high-performance computing and advanced memory solutions. This segmentation analysis provides insights into the specific growth drivers and challenges within each segment, allowing stakeholders to make informed decisions regarding product development and market strategies.

Global Redistribution Layer Material Market Size and Share by Region - Geographic distribution

The global Redistribution Layer Material Market exhibits varying growth patterns across different geographic regions, influenced by factors such as technological advancements, manufacturing capabilities, and regional economic conditions. Asia-Pacific currently dominates the market, accounting for the largest share due to the presence of major semiconductor manufacturing hubs in countries like China, South Korea, Taiwan, and Japan. This region benefits from a strong ecosystem of semiconductor companies, advanced research facilities, and government initiatives supporting the electronics industry. North America is the second-largest market, driven by the presence of leading technology companies and significant investments in research and development. The region's focus on emerging technologies such as artificial intelligence and 5G is expected to fuel the demand for advanced RDL materials. Europe is also a significant market, particularly in automotive electronics and industrial applications, where there is a growing need for sophisticated packaging solutions. Other regions, including Latin America and the Middle East & Africa, are expected to witness moderate growth, primarily driven by the increasing adoption of consumer electronics and the development of local semiconductor industries. The regional analysis highlights the importance of understanding local market dynamics and tailoring strategies to capitalize on region-specific opportunities and challenges.

Regional Analysis of the Redistribution Layer Material Market - Detailed regional market performance

The Redistribution Layer Material Market exhibits distinct characteristics and growth patterns across different regions, shaped by local industrial strengths, technological capabilities, and economic factors. In Asia-Pacific, particularly in countries like China, South Korea, Taiwan, and Japan, the market is experiencing robust growth due to the concentration of semiconductor manufacturing facilities and a strong electronics industry. This region benefits from a well-established supply chain, skilled workforce, and government support for technological advancements. North America, led by the United States, is characterized by a focus on innovation and the development of advanced packaging technologies. The region's strong presence in sectors such as artificial intelligence, data centers, and automotive electronics drives the demand for sophisticated RDL materials. Europe, while smaller in market size compared to Asia-Pacific and North America, is witnessing steady growth, particularly in automotive electronics and industrial applications. The region's emphasis on electric vehicles and Industry 4.0 initiatives is creating new opportunities for RDL material suppliers. Other regions, including Latin America and the Middle East & Africa, are gradually emerging as potential markets, driven by increasing investments in electronics manufacturing and the growing adoption of consumer technologies. The regional analysis underscores the importance of understanding local market dynamics, regulatory environments, and industry trends to develop effective strategies for market penetration and growth.

Leading Company Profiles in the Redistribution Layer Material Market - Industry players and strategies

The Redistribution Layer Material Market is characterized by the presence of several key players, each employing distinct strategies to maintain and enhance their market positions. ASE Technology Holding Co Ltd. is a prominent player, leveraging its comprehensive semiconductor assembly and testing services to offer integrated RDL solutions. The company focuses on expanding its product portfolio through continuous research and development efforts. Amkor Technology Inc. is another major competitor, known for its advanced packaging technologies and global manufacturing footprint. The company's strategy revolves around providing customized RDL solutions for specific applications, particularly in the mobile and consumer electronics sectors. Dupont De Nemours Inc. brings its expertise in material science to the market, offering high-performance RDL materials with enhanced thermal and electrical properties. Fujifilm Holdings Corp. leverages its polymer technology capabilities to develop innovative RDL materials, particularly in the area of photosensitive dielectrics. Infineon Technologies AG, while primarily known for its semiconductor solutions, has been expanding its presence in the RDL material market through strategic partnerships and acquisitions. JCET Group Co Ltd. focuses on providing cost-effective RDL solutions, particularly for mass-market applications. NXP Semiconductors NV emphasizes the development of RDL materials for automotive and IoT applications. SK Hynix Inc. and Samsung Electronics Co Ltd. leverage their strong positions in the memory and logic chip markets to drive demand for advanced RDL materials. Shin-Etsu Chemical Co Ltd. specializes in the development of high-performance polymers for RDL applications, focusing on improving material properties such as dielectric constant and thermal stability. These companies' strategies include investments in research and development, strategic partnerships, and expansion of manufacturing capabilities to meet the growing demand for advanced RDL materials across various applications.

Porter's Five Forces Analysis of the Redistribution Layer Material Market - Competitive forces assessment

Porter's Five Forces analysis provides a framework for understanding the competitive dynamics of the Redistribution Layer Material Market. The threat of new entrants is relatively low due to the high capital requirements for research and development, as well as the need for specialized manufacturing capabilities. Established players benefit from economies of scale and strong relationships with semiconductor manufacturers, creating barriers to entry for potential new competitors. The bargaining power of suppliers is moderate, as the market relies on a limited number of raw material suppliers, but the presence of multiple material options provides some flexibility. The bargaining power of buyers, primarily semiconductor manufacturers, is significant due to their large order volumes and ability to switch between suppliers. However, the increasing complexity of RDL materials and the need for customized solutions are reducing buyer power in some segments. The threat of substitute products is low, as RDL materials are highly specialized and integral to advanced packaging technologies. Competitive rivalry within the market is intense, with major players competing on factors such as material performance, cost, and technical support. The market is also characterized by ongoing technological advancements, which drive continuous innovation and product development. Overall, the analysis suggests that while the market presents challenges, it also offers opportunities for established players to leverage their expertise and market position to drive growth and profitability.

SWOT Analysis of the Redistribution Layer Material Market - Strengths, weaknesses, opportunities, threats

A SWOT analysis of the Redistribution Layer Material Market reveals key insights into its internal strengths and weaknesses, as well as external opportunities and threats. Strengths of the market include the increasing demand for advanced semiconductor packaging solutions, driven by the proliferation of 5G technology, artificial intelligence, and IoT devices. The market also benefits from ongoing technological advancements in material science, leading to the development of RDL materials with improved properties such as lower dielectric constants and enhanced thermal stability. Additionally, the presence of established players with strong research and development capabilities contributes to the market's strength. However, the market faces certain weaknesses, including the high cost of advanced RDL materials and the complexity of manufacturing processes, which can limit adoption in cost-sensitive applications. Opportunities in the market are significant, particularly in emerging applications such as automotive electronics, medical devices, and flexible electronics, where there is a growing need for sophisticated packaging solutions. The market also presents opportunities for expansion into new geographic regions and the development of next-generation materials with superior performance characteristics. Threats to the market include potential supply chain disruptions, intense competition among existing players, and the rapid pace of technological change, which may render current materials obsolete. Additionally, economic uncertainties and geopolitical tensions could impact the market's growth trajectory. Overall, the SWOT analysis highlights the market's potential for growth while also identifying key challenges that need to be addressed to capitalize on emerging opportunities.

Redistribution Layer Material Market Value Chain Analysis - Industry structure and value flow

The value chain analysis of the Redistribution Layer Material Market provides insights into the various stages of production and distribution, highlighting the key activities that add value to the final product. The value chain begins with raw material suppliers, who provide the basic chemicals and polymers used in RDL material production. These materials are then processed by material manufacturers, who develop and produce the specialized RDL materials with specific properties tailored to different applications. The next stage involves semiconductor packaging companies, which integrate the RDL materials into advanced packaging solutions such as fan-out wafer level packaging and 2.5D/3D IC packaging. These packaging solutions are then incorporated into electronic devices by original equipment manufacturers (OEMs). Throughout the value chain, research and development plays a crucial role in driving innovation and improving material properties. Distribution and sales activities ensure that RDL materials reach end-users efficiently, while after-sales support and technical assistance add further value by helping customers optimize the use of these materials in their applications. The value chain also includes support activities such as logistics, quality control, and regulatory compliance, which are essential for maintaining product quality and meeting industry standards. Understanding the value chain structure helps identify opportunities for value creation and potential areas for improvement in terms of cost reduction, efficiency enhancement, and innovation.

Key Investment Insights in the Redistribution Layer Material Market - Strategic investment recommendations

Strategic investment insights for the Redistribution Layer Material Market highlight several key areas that offer significant potential for growth and returns. Investors should consider focusing on companies that are at the forefront of developing next-generation RDL materials with enhanced properties, such as ultra-low dielectric constants and improved thermal stability. These advanced materials are crucial for emerging applications in 5G, artificial intelligence, and high-performance computing, which are expected to drive substantial demand in the coming years. Another attractive investment opportunity lies in companies that are expanding their manufacturing capabilities to meet the growing global demand for RDL materials, particularly in regions with strong semiconductor manufacturing ecosystems like Asia-Pacific. Additionally, investments in research and development initiatives aimed at creating RDL materials for new applications, such as flexible electronics and advanced automotive systems, could yield significant returns as these markets continue to evolve. Strategic partnerships and collaborations between material suppliers and semiconductor manufacturers represent another area of interest, as they can lead to the development of customized solutions and strengthen market positions. Investors should also consider the potential of companies that are working on sustainable and environmentally friendly RDL materials, as this aligns with the growing emphasis on green technologies in the electronics industry. Finally, keeping an eye on companies that are actively pursuing mergers and acquisitions to expand their product portfolios and geographic presence could provide opportunities for value creation through synergies and market consolidation.

Redistribution Layer Material Market Conclusion - Summary and key takeaways

The Redistribution Layer Material Market is poised for significant growth, driven by the increasing demand for advanced semiconductor packaging solutions across various high-tech applications. With a projected compound annual growth rate (CAGR) of 12.35%, the market is expected to expand from 275.50 Million in 2026 to 622.35 Million by 2033. Key takeaways from the market analysis include the critical role of RDL materials in enabling miniaturization and performance enhancement in electronic devices, particularly in emerging technologies such as 5G, artificial intelligence, and Internet of Things (IoT). The market is characterized by intense competition among major players, who are focusing on innovation, strategic partnerships, and expansion of manufacturing capabilities to maintain their competitive edge. While the market faces challenges such as high material costs and manufacturing complexities, it also presents significant opportunities for growth, particularly in the development of next-generation materials and expansion into new application areas like automotive electronics and medical devices. The regional analysis highlights the dominance of Asia-Pacific in the market, driven by the presence of major semiconductor manufacturing hubs, while North America and Europe are also expected to witness substantial growth. Overall, the Redistribution Layer Material Market offers promising prospects for stakeholders who can navigate the complex technological landscape and capitalize on emerging trends in advanced packaging technologies.

Research Methodology - How this research was conducted

The research methodology employed for this Redistribution Layer Material Market analysis combines both primary and secondary research approaches to ensure comprehensive and accurate insights. Primary research involved conducting interviews with industry experts, including material scientists, semiconductor packaging engineers, and executives from leading companies in the RDL material market. These interviews provided valuable firsthand information on market trends, technological advancements, and competitive dynamics. Secondary research encompassed a thorough review of industry reports, company annual reports, technical journals, and relevant publications from reputable sources such as industry associations and government databases. Market size and forecast data were derived through a combination of top-down and bottom-up approaches, triangulating information from multiple sources to ensure accuracy. The analysis also incorporated Porter's Five Forces framework and SWOT analysis to provide a comprehensive understanding of the market's competitive landscape and strategic positioning. Data validation was performed through cross-referencing with multiple sources and expert consultations to ensure the reliability of the findings. The research methodology was designed to provide a holistic view of the Redistribution Layer Material Market, covering aspects such as market dynamics, competitive landscape, regional analysis, and future growth prospects.

Research Scope - Coverage and limitations

The research scope for this Redistribution Layer Material Market analysis encompasses a comprehensive examination of the market's current state and future prospects. The study covers key aspects such as market size, growth trends, competitive landscape, and regional analysis, providing insights into the market's dynamics from 2025 to 2032. The research focuses on major types of RDL materials, including polyimide, polybenzoxazole, and benzocyclobutene, as well as key applications such as fan-out wafer level packaging and 2.5D/3D IC packaging. The analysis includes a detailed examination of the market's value chain, investment insights, and strategic recommendations for stakeholders. However, it is important to note certain limitations of the research. The study is primarily based on publicly available information and expert opinions, which may not capture all nuances of the market. Additionally, the rapidly evolving nature of the semiconductor industry and potential technological disruptions could impact future market dynamics in ways that are difficult to predict. The research also does not account for potential geopolitical factors or sudden economic shifts that could affect the market's growth trajectory. Despite these limitations, the research provides a robust foundation for understanding the Redistribution Layer Material Market and its future prospects, offering valuable insights for industry participants, investors, and other stakeholders.

Key Companies and Recent Developments in the Redistribution Layer Material Market - Introduction to top companies and their recent announcements, product launches, partnerships, and strategic developments

The Redistribution Layer Material Market is characterized by the presence of several key players who are continuously innovating and expanding their market presence through various strategic initiatives. ASE Technology Holding Co Ltd. has recently announced the expansion of its advanced packaging capabilities, focusing on the development of next-generation RDL materials for high-performance computing applications. Amkor Technology Inc. has launched a new line of ultra-thin RDL materials designed specifically for mobile and wearable devices, addressing the growing demand for miniaturization in consumer electronics. Dupont De Nemours Inc. has introduced a novel polybenzoxazole-based RDL material with enhanced thermal stability and lower dielectric constant, targeting the 5G and AI markets. Fujifilm Holdings Corp. has formed a strategic partnership with a leading semiconductor manufacturer to develop photosensitive RDL materials for advanced packaging applications. Infineon Technologies AG has announced the acquisition of a specialized RDL material supplier to strengthen its position in the automotive electronics market. JCET Group Co Ltd. has expanded its production capacity for cost-effective RDL materials, aiming to capture a larger share of the mass-market segment. NXP Semiconductors NV has unveiled a new RDL material solution for IoT and edge computing applications, emphasizing improved reliability and performance. SK Hynix Inc. and Samsung Electronics Co Ltd. have both announced investments in R&D for next-generation RDL materials to support their advanced memory and logic chip development efforts. Shin-Etsu Chemical Co Ltd. has launched a new series of high-performance polymers for RDL applications, focusing on improving material properties such as dielectric constant and thermal stability. These recent developments highlight the dynamic nature of the market and the ongoing efforts by key players to innovate and meet the evolving demands of advanced semiconductor packaging technologies.