Telecom Cloud Market Overview - Definition, scope, and significance

The Telecom Cloud Market represents a transformative shift in how telecommunications infrastructure and services are delivered, leveraging cloud computing technologies to provide scalable, flexible, and cost-effective solutions for network operators and service providers. This market encompasses the deployment of cloud-based architectures for core network functions, including network function virtualization (NFV), software-defined networking (SDN), and cloud-native applications that enable telecom operators to modernize their infrastructure. The scope extends across various deployment models including public, private, and hybrid cloud environments, serving both small and medium enterprises (SMEs) and large enterprises. The significance of this market lies in its ability to reduce capital expenditures, accelerate service deployment, enhance operational efficiency, and enable new revenue streams through innovative services such as 5G network slicing, edge computing, and IoT connectivity solutions.

Telecom Cloud Market Drivers, Restraints, Challenges, and Opportunities - Key growth factors and obstacles

The primary drivers fueling the Telecom Cloud Market include the accelerating adoption of 5G networks, which demand highly flexible and scalable infrastructure, and the increasing need for network operators to reduce operational costs while improving service delivery speed. The growing demand for edge computing capabilities, rising enterprise cloud adoption, and the need for enhanced network security and reliability also contribute significantly to market growth. However, the market faces several restraints including high initial implementation costs, concerns about data privacy and security in cloud environments, and the complexity of migrating legacy systems to cloud-based architectures. Major challenges include ensuring seamless integration between traditional telecom infrastructure and cloud platforms, managing multi-vendor environments, and addressing regulatory compliance across different regions. Despite these obstacles, substantial opportunities exist in emerging markets, the expansion of IoT and smart city initiatives, and the development of AI-driven network management solutions that can optimize cloud-based telecom operations.

Telecom Cloud Market Growth Trends - Current and emerging trends shaping the market

Several key growth trends are currently shaping the Telecom Cloud Market, with the most prominent being the accelerated migration toward cloud-native architectures that enable telecom operators to deploy services more rapidly and efficiently. The integration of artificial intelligence and machine learning for network automation and predictive maintenance is becoming increasingly prevalent, allowing operators to optimize resource allocation and improve service quality. Another significant trend is the rise of multi-cloud and hybrid cloud strategies, where telecom companies leverage multiple cloud providers to enhance flexibility and avoid vendor lock-in. The emergence of 5G Standalone (SA) networks is driving demand for cloud-native core networks, while the expansion of edge computing is enabling ultra-low latency applications and services. Additionally, the growing focus on sustainability and energy efficiency is pushing telecom operators to adopt cloud solutions that can optimize power consumption and reduce carbon footprints across their infrastructure.

COVID-19 Impact on the Telecom Cloud Market - Pandemic effects and recovery trajectory

The COVID-19 pandemic had a profound impact on the Telecom Cloud Market, initially causing disruptions in supply chains and delaying infrastructure deployments due to lockdowns and restrictions. However, the crisis also accelerated digital transformation initiatives across the telecom sector, as the sudden surge in remote work, online education, and digital services highlighted the critical need for scalable and resilient cloud infrastructure. Telecom operators rapidly expanded their cloud capabilities to handle unprecedented traffic volumes and ensure service continuity. The pandemic also accelerated the adoption of cloud-based collaboration tools, video conferencing platforms, and cloud-managed network services. As the market recovers, we are witnessing a sustained increase in cloud adoption driven by lessons learned during the pandemic, with operators now prioritizing cloud-native architectures that can provide the flexibility and scalability needed to handle future demand surges and support emerging technologies such as 5G and IoT.

Telecom Cloud Market Competitive Landscape - Major competitors and market consolidation

The Telecom Cloud Market features a highly competitive landscape characterized by the presence of major technology giants, traditional telecom equipment manufacturers, and specialized cloud service providers. The market is witnessing significant consolidation as companies seek to expand their cloud capabilities through strategic partnerships, acquisitions, and joint ventures. Traditional telecom vendors are increasingly partnering with cloud hyperscalers to deliver integrated solutions, while cloud providers are expanding their telecom-specific offerings to capture a larger share of the market. The competitive dynamics are further intensified by the entry of new players offering innovative cloud-native solutions and the growing importance of ecosystem partnerships that combine hardware, software, and services. Companies are differentiating themselves through their ability to provide end-to-end solutions, strong service level agreements, and expertise in specific deployment models such as private or hybrid cloud environments.

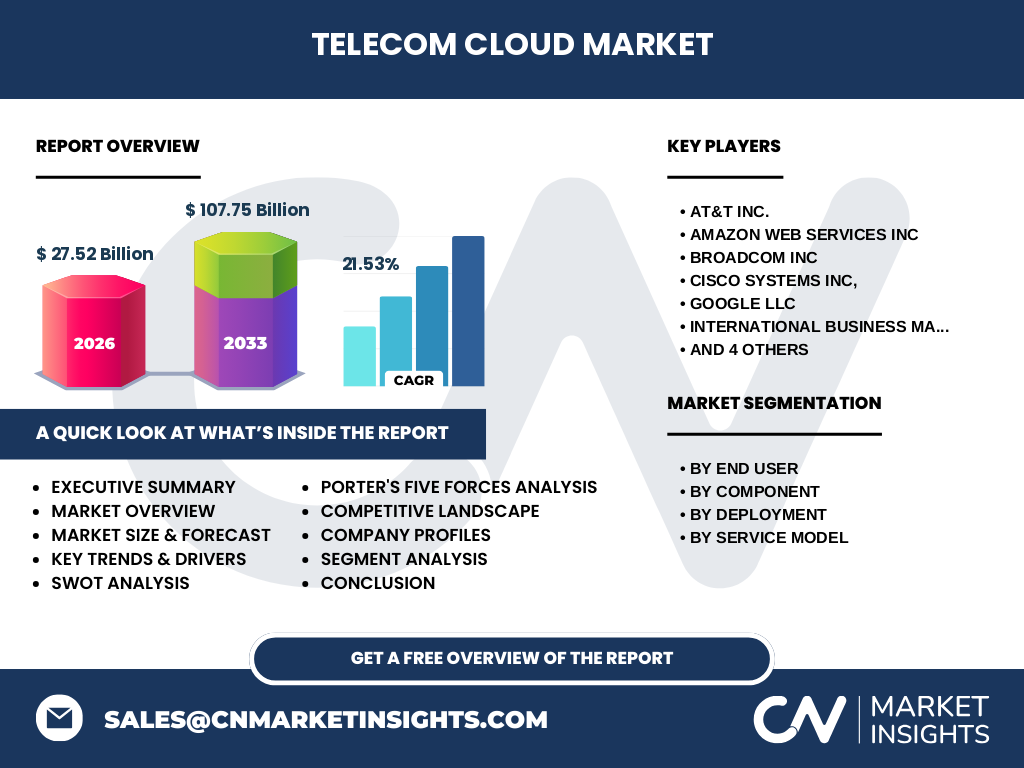

Executive Summary - High-level overview and key findings about Telecom Cloud Market

The Telecom Cloud Market is experiencing robust growth driven by the convergence of cloud computing and telecommunications, with a projected CAGR of 21.53% from 2026 to 2033. The market is transitioning from traditional hardware-based infrastructure to software-defined, cloud-native architectures that offer unprecedented flexibility and scalability. Key findings indicate that the market is being propelled by 5G deployment, increasing enterprise cloud adoption, and the need for operational efficiency. The services segment is expected to dominate the market, while hybrid cloud deployment models are gaining traction due to their balance of security and flexibility. Large enterprises currently represent the largest end-user segment, though SMEs are rapidly adopting cloud solutions as costs decrease and usability improves. The competitive landscape is characterized by strategic partnerships between telecom operators and cloud providers, with a focus on developing industry-specific solutions that address unique telecom requirements.

Telecom Cloud Market Forecast - Projections for 2025-2032 period

The Telecom Cloud Market is projected to experience substantial growth over the 2025-2032 period, expanding from a market size of 27.52 Billion in 2026 to 107.75 Billion by 2033, representing a CAGR of 21.53%. This impressive growth trajectory is driven by several factors including the widespread deployment of 5G networks, increasing enterprise digital transformation initiatives, and the growing adoption of cloud-native architectures in the telecom sector. The forecast period will likely see accelerated investment in cloud infrastructure as telecom operators seek to modernize their networks and reduce operational costs. Regional markets, particularly in Asia-Pacific and North America, are expected to lead growth due to strong 5G momentum and high cloud adoption rates. The services segment, including professional and managed services, is anticipated to witness the highest growth rate as operators seek expertise in cloud migration and optimization. Additionally, the increasing complexity of telecom networks will drive demand for cloud-based network management and orchestration solutions throughout the forecast period.

Telecom Cloud Market Size and Share by Segmentation - Breakdown by {segmentData}

The Telecom Cloud Market segmentation reveals distinct patterns in market adoption and growth across different categories. By end user, large enterprises currently dominate the market due to their substantial IT budgets and complex infrastructure requirements, though SMEs are rapidly catching up as cloud solutions become more accessible and cost-effective. In terms of components, the solution segment, which includes cloud platforms, software, and infrastructure, holds a significant market share, while the services segment is experiencing the fastest growth as organizations require expertise for implementation and management. By deployment model, hybrid cloud solutions are gaining the most traction as they offer the ideal balance between the security of private clouds and the scalability of public clouds. The service model segmentation shows that Infrastructure-as-a-Service (IaaS) currently leads in market share due to its foundational nature, but Software-as-a-Service (SaaS) is growing rapidly as telecom-specific applications become more sophisticated and cloud-native.

Global Telecom Cloud Market Size and Share by Region - Geographic distribution

The global Telecom Cloud Market exhibits significant regional variations in adoption rates, market maturity, and growth potential. North America currently leads the market due to early technology adoption, strong 5G deployment, and the presence of major cloud providers and telecom operators. The region benefits from advanced digital infrastructure and high enterprise cloud adoption rates. Europe represents the second-largest market, driven by strong regulatory frameworks supporting cloud adoption and significant investments in 5G infrastructure. The Asia-Pacific region is expected to witness the highest growth rate during the forecast period, fueled by rapid 5G deployment in countries like China, South Korea, and Japan, along with increasing digital transformation initiatives across emerging economies. Latin America and Middle East & Africa regions are experiencing steady growth, though at a slower pace due to infrastructure challenges and varying levels of digital maturity. Regional differences in regulatory environments, economic conditions, and technology adoption rates significantly influence market dynamics across geographies.

Regional Analysis of the Telecom Cloud Market - Detailed regional market performance

A detailed regional analysis reveals distinct market characteristics and growth patterns across different geographies. In North America, the market is characterized by mature cloud adoption, with telecom operators rapidly transitioning to cloud-native architectures to support 5G and edge computing initiatives. The region benefits from strong technology infrastructure and significant R&D investments. Europe's market is shaped by strict data protection regulations and a focus on sustainable cloud solutions, with operators emphasizing energy-efficient cloud deployments. The Asia-Pacific region presents a dynamic landscape where rapid urbanization and digital transformation are driving massive cloud adoption, particularly in telecommunications hubs like Singapore, Hong Kong, and major Indian cities. China's market is unique due to its domestic cloud ecosystem and aggressive 5G rollout strategy. In Latin America, market growth is influenced by economic factors and varying levels of infrastructure development, with Brazil and Mexico leading adoption. The Middle East & Africa region shows promising growth potential, particularly in Gulf Cooperation Council countries investing heavily in smart city initiatives and digital infrastructure.

Leading Company Profiles in the Telecom Cloud Market - Industry players and strategies

The Telecom Cloud Market features a diverse array of leading companies, each employing distinct strategies to capture market share and drive innovation. AT&T Inc. has positioned itself as a comprehensive telecom cloud provider, leveraging its extensive network infrastructure to offer integrated cloud solutions. Amazon Web Services Inc. dominates through its broad cloud portfolio and specialized telecom services, including 5G and edge computing solutions. Broadcom Inc. focuses on providing semiconductor and infrastructure software solutions that enable cloud-based telecom operations. Cisco Systems Inc. emphasizes its expertise in networking and security, offering cloud-managed services and virtualized network functions. Google LLC leverages its artificial intelligence capabilities and global infrastructure to deliver advanced cloud solutions for telecom operators. International Business Machines Corp specializes in hybrid cloud and AI-driven network management solutions. Microsoft Corp integrates its cloud platform with telecom-specific services and strong enterprise relationships. Telefonaktiebolaget LM Ericsson and Verizon Communications Inc. represent traditional telecom operators transitioning to cloud-native architectures, while Telstra Corp Ltd focuses on providing cloud solutions tailored to regional market needs.

Porter's Five Forces Analysis of the Telecom Cloud Market - Competitive forces assessment

Porter's Five Forces analysis reveals the competitive dynamics shaping the Telecom Cloud Market. The threat of new entrants is moderate, as entering the market requires substantial capital investment, technical expertise, and established relationships with telecom operators. However, the growing demand for cloud solutions continues to attract new players, particularly in niche segments. The bargaining power of buyers is increasing as telecom operators gain more options and become more knowledgeable about cloud technologies, leading to price sensitivity and demand for customized solutions. Suppliers, particularly cloud infrastructure providers and technology vendors, hold significant power due to the specialized nature of their offerings and the critical role they play in enabling cloud-based telecom services. The threat of substitute products or services is relatively low, as cloud solutions offer unique advantages in terms of scalability and flexibility that traditional infrastructure cannot match. Competitive rivalry is intense, with numerous players competing on price, innovation, service quality, and comprehensive solution offerings, driving continuous improvement and market evolution.

SWOT Analysis of the Telecom Cloud Market - Strengths, weaknesses, opportunities, threats

A SWOT analysis of the Telecom Cloud Market reveals key strategic insights. Strengths include the inherent scalability and flexibility of cloud solutions, the ability to rapidly deploy new services, and the potential for significant cost reduction through operational efficiency. The market also benefits from strong technological foundations and the growing expertise of both providers and users in cloud technologies. Weaknesses encompass concerns about data security and privacy, the complexity of migrating legacy systems, and potential vendor lock-in issues. Additionally, the high initial investment costs and the need for specialized skills represent significant challenges. Opportunities abound in emerging markets, the continued expansion of 5G networks, the growth of IoT and edge computing applications, and the potential for developing industry-specific cloud solutions. Threats include increasing cybersecurity risks, evolving regulatory requirements across different regions, potential economic downturns affecting IT spending, and the rapid pace of technological change that could render current solutions obsolete.

Telecom Cloud Market Value Chain Analysis - Industry structure and value flow

The Telecom Cloud Market value chain encompasses multiple layers of activity that create and deliver value to end customers. At the foundation are hardware and infrastructure providers who supply the physical components including servers, storage systems, and networking equipment. Above this layer are platform providers who offer the software frameworks and development tools necessary for building cloud-based telecom applications. Cloud service providers operate the next level, delivering various service models including IaaS, PaaS, and SaaS to telecom operators and enterprises. System integrators and managed service providers play a crucial role in implementing and maintaining cloud solutions, bridging the gap between technology providers and end users. Value is created through the optimization of network functions, reduction in operational costs, acceleration of service deployment, and the enablement of new revenue-generating services. The value chain is characterized by increasing collaboration between traditionally separate industry segments, with telecom operators, cloud providers, and technology vendors forming strategic partnerships to deliver comprehensive solutions.

Key Investment Insights in the Telecom Cloud Market - Strategic investment recommendations

Strategic investment insights for the Telecom Cloud Market highlight several promising areas for capital allocation and business development. Investors should consider focusing on companies that are developing cloud-native network functions and 5G core infrastructure, as these technologies represent the future of telecom operations. The edge computing segment presents significant investment opportunities due to its critical role in enabling low-latency applications and supporting 5G use cases. Investments in AI and machine learning capabilities for network automation and optimization are likely to yield strong returns as operators seek to improve efficiency and service quality. The services segment, including professional services for cloud migration and managed services for ongoing operations, represents a growing market with recurring revenue potential. Additionally, companies focusing on hybrid cloud solutions that address the unique security and compliance requirements of telecom operators are well-positioned for growth. Strategic investments in emerging markets with high 5G deployment rates could provide substantial returns as these regions accelerate their digital transformation initiatives.

Telecom Cloud Market Conclusion - Summary and key takeaways

The Telecom Cloud Market stands at a pivotal juncture, characterized by robust growth, technological innovation, and transformative potential for the telecommunications industry. With a projected market size expansion from 27.52 Billion to 107.75 Billion and a CAGR of 21.53%, the market demonstrates compelling investment potential and strategic importance. Key takeaways include the accelerating shift toward cloud-native architectures driven by 5G deployment, the growing importance of edge computing and network virtualization, and the increasing collaboration between traditional telecom operators and cloud service providers. The market's segmentation reveals diverse opportunities across different deployment models, service types, and end-user categories, with hybrid cloud solutions and managed services showing particularly strong growth trajectories. Regional analysis indicates that while North America and Europe currently lead in market maturity, the Asia-Pacific region represents the highest growth potential. Success in this market will require companies to navigate complex technological transitions, address security and compliance challenges, and develop solutions that meet the evolving needs of telecom operators in an increasingly digital world.

Research Methodology - How this research was conducted

The research methodology employed for this Telecom Cloud Market analysis combines comprehensive secondary research with selective primary research to ensure accuracy and reliability of findings. Secondary research involved extensive review of industry reports, company annual reports, financial statements, press releases, and regulatory filings to gather market data and competitive intelligence. Industry publications, technology journals, and market databases provided additional context and trend analysis. For primary research, selective interviews were conducted with industry experts, technology providers, and telecom operators to validate findings and gain insights into market dynamics, challenges, and opportunities. The research process included data triangulation to cross-verify information from multiple sources, ensuring consistency and reliability. Market size calculations were derived using both top-down and bottom-up approaches, considering factors such as regional adoption rates, deployment models, and service types. The forecast period analysis incorporated consideration of macroeconomic factors, technology roadmaps, and regulatory environments across different regions to provide a comprehensive market outlook.

Research Scope - Coverage and limitations

The research scope for this Telecom Cloud Market report encompasses a comprehensive analysis of the market from 2026 to 2033, covering key segments including end users (SMEs and large enterprises), components (solution and services), deployment models (public, private, and hybrid cloud), and service models (SaaS, IaaS, and PaaS). The geographic coverage includes major regions such as North America, Europe, Asia-Pacific, Latin America, and Middle East & Africa, with detailed analysis of market dynamics within each region. The scope also includes competitive landscape analysis of key players, technology trends, and strategic developments in the market. However, certain limitations exist, including the exclusion of specific country-level data for all regions due to data availability constraints, and the focus primarily on commercial market segments while excluding certain niche or experimental applications. The research also does not cover detailed pricing analysis across all service models and regions due to the highly variable and negotiated nature of cloud service pricing in the telecom sector.

Key Companies and Recent Developments in the Telecom Cloud Market - Introduction to top companies and their recent announcements, product launches, partnerships, and strategic developments

The Telecom Cloud Market features several key companies driving innovation and market growth through strategic initiatives and technological advancements. AT&T Inc. has recently announced expanded partnerships with major cloud providers to enhance its edge computing capabilities and support 5G network slicing. Amazon Web Services Inc. continues to strengthen its telecom cloud offerings with new services specifically designed for 5G core network functions and network function virtualization. Broadcom Inc. has launched advanced semiconductor solutions optimized for cloud-based telecom infrastructure, focusing on improved performance and energy efficiency. Cisco Systems Inc. recently unveiled enhanced cloud-managed networking solutions and expanded its partnership ecosystem to deliver integrated cloud and security offerings. Google LLC has introduced specialized AI-driven network management tools for telecom operators and expanded its cloud region presence to support edge computing applications. International Business Machines Corp announced new hybrid cloud solutions tailored for telecom operators, emphasizing AI-powered network automation. Microsoft Corp continues to expand its Azure for Operators portfolio with new 5G and edge computing capabilities. Telefonaktiebolaget LM Ericsson has launched next-generation cloud-native core network solutions and formed strategic partnerships with cloud hyperscalers. Telstra Corp Ltd recently announced investments in cloud infrastructure to support 5G expansion and digital services growth. Verizon Communications Inc. has introduced new cloud-based managed services for enterprise customers and expanded its network-as-a-service offerings.