Engineering Software Market Overview - Definition, scope, and significance

Engineering software encompasses a broad range of digital tools and applications designed to assist engineers, designers, and technical professionals in various stages of product development, design, simulation, testing, and manufacturing processes. This market includes specialized software solutions such as Computer-Aided Design (CAD), Computer-Aided Manufacturing (CAM), Computer-Aided Engineering (CAE), Electronic Design Automation (EDA), and Architecture, Engineering, and Construction (AEC) software. The significance of this market lies in its critical role in driving innovation across industries including automotive, aerospace, construction, electronics, and manufacturing, enabling organizations to streamline workflows, reduce development costs, improve product quality, and accelerate time-to-market for new products and solutions.

Engineering Software Market Drivers, Restraints, Challenges, and Opportunities - Key growth factors and obstacles

The engineering software market is propelled by several key drivers including the increasing adoption of digital transformation initiatives across industries, the growing demand for automation and smart manufacturing solutions, and the rising need for complex product design and simulation capabilities. The integration of advanced technologies such as artificial intelligence, machine learning, and cloud computing into engineering software platforms is creating new opportunities for enhanced functionality and accessibility. However, the market faces restraints such as high implementation costs, the complexity of software integration with existing systems, and the shortage of skilled professionals capable of utilizing advanced engineering tools effectively. Challenges include data security concerns, the need for continuous software updates and maintenance, and the increasing competition from open-source alternatives. Despite these challenges, opportunities abound in emerging markets, the growing demand for sustainable design solutions, and the expanding applications of engineering software in new industries such as renewable energy and biotechnology.

Engineering Software Market Growth Trends - Current and emerging trends shaping the market

The engineering software market is experiencing significant growth trends driven by technological advancements and changing industry requirements. One prominent trend is the shift toward cloud-based engineering solutions, which offer enhanced collaboration capabilities, scalability, and cost-effectiveness compared to traditional on-premise software. Another major trend is the integration of artificial intelligence and machine learning algorithms into engineering software, enabling predictive analytics, automated design optimization, and intelligent decision-making support. The market is also witnessing increased adoption of virtual and augmented reality technologies for immersive design visualization and simulation. Additionally, there is a growing emphasis on sustainable design and manufacturing processes, leading to the development of specialized software tools that help engineers optimize energy efficiency and reduce environmental impact. The convergence of engineering software with Internet of Things (IoT) platforms is creating new opportunities for real-time monitoring, predictive maintenance, and digital twin implementations across various industries.

COVID-19 Impact on the Engineering Software Market - Pandemic effects and recovery trajectory

The COVID-19 pandemic had a profound impact on the engineering software market, initially causing disruptions in supply chains, project delays, and reduced capital expenditures across many industries. However, the pandemic also accelerated digital transformation initiatives as organizations sought to enable remote work capabilities and maintain operational continuity. This led to increased demand for cloud-based engineering software solutions, collaborative design platforms, and simulation tools that could be accessed remotely. The crisis highlighted the importance of digital engineering capabilities in maintaining business resilience and prompted many companies to accelerate their investments in advanced software technologies. As industries recover from the pandemic, the engineering software market is experiencing a strong rebound, with increased focus on automation, digital twin technologies, and integrated design-manufacturing solutions. The lessons learned during the pandemic have permanently shifted many organizations' approach to engineering software adoption and implementation strategies.

Engineering Software Market Competitive Landscape - Major competitors and market consolidation

The engineering software market features a competitive landscape characterized by both established industry leaders and innovative emerging players. Major competitors such as Autodesk, Dassault Systèmes, Siemens, and PTC dominate the market with comprehensive product portfolios and strong global presence. These companies are engaged in continuous innovation, strategic acquisitions, and partnerships to expand their market share and technological capabilities. The market is witnessing consolidation through mergers and acquisitions as larger companies seek to acquire specialized technologies and expand into new application areas. Smaller, niche players are also making significant contributions by focusing on specific industry verticals or offering specialized solutions for particular engineering challenges. The competitive dynamics are further intensified by the entry of technology giants and the increasing availability of open-source alternatives, forcing established players to continuously innovate and enhance their value propositions to maintain their competitive edge.

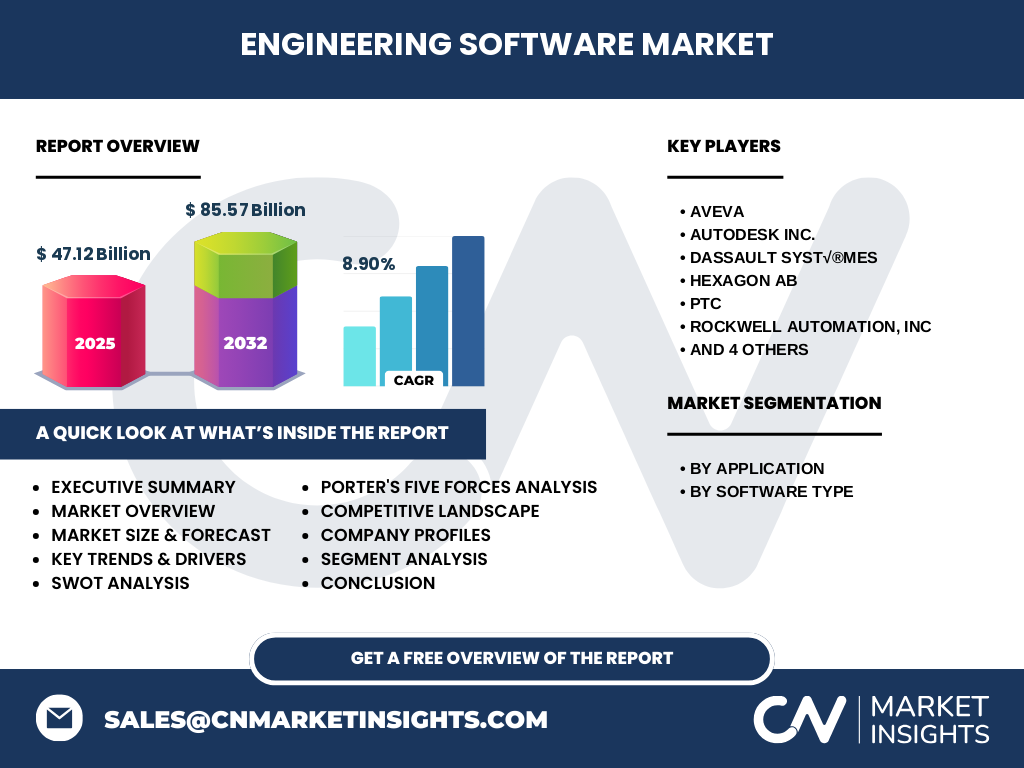

Executive Summary - High-level overview and key findings about Engineering Software Market

The engineering software market represents a dynamic and rapidly evolving sector that plays a crucial role in modern industrial innovation and digital transformation. With a market size of 47.12 Billion in 2025 and projected to reach 85.57 Billion by 2032, growing at a CAGR of 8.90%, the market demonstrates robust growth potential driven by technological advancements and increasing demand across multiple industries. Key findings indicate that cloud-based solutions, AI integration, and sustainable design capabilities are among the most significant growth drivers. The market is characterized by intense competition, continuous technological innovation, and expanding applications across traditional and emerging industries. Companies are increasingly focusing on integrated solutions that offer end-to-end engineering capabilities, while also addressing the growing demand for specialized tools in areas such as digital twin technology, simulation, and collaborative design platforms.

Engineering Software Market Forecast - Projections for 2025-2032 period

The engineering software market is projected to experience substantial growth over the 2025-2032 period, with the market size expected to increase from 47.12 Billion to 85.57 Billion, representing a compound annual growth rate of 8.90%. This growth trajectory is supported by several factors including the accelerating pace of digital transformation across industries, the increasing complexity of engineering projects, and the growing adoption of advanced technologies such as artificial intelligence and cloud computing. The forecast period will likely see continued expansion in emerging markets, increased demand for integrated engineering solutions, and the development of new software capabilities to address evolving industry challenges. Key growth areas include simulation and analysis tools, collaborative design platforms, and specialized software for emerging industries such as renewable energy and electric vehicles. The market is also expected to witness increased investment in research and development, leading to the introduction of innovative solutions that further drive market expansion.

The engineering software market is segmented by application and software type, providing a comprehensive view of the market structure and growth opportunities. By application, the market includes Plant Design, Design Automation, Drafting & 3D Modelling, and Product Design & Testing segments. Each of these application areas serves specific industry needs and contributes differently to the overall market growth. By software type, the market is categorized into CAD (Computer-Aided Design), CAM (Computer-Aided Manufacturing), CAE (Computer-Aided Engineering), AEC (Architecture, Engineering, and Construction), and EDA (Electronic Design Automation). These software types represent different aspects of the engineering workflow, from initial design concepts to manufacturing execution and testing. The segmentation analysis reveals that while traditional CAD and CAE software continue to dominate the market, there is significant growth potential in specialized segments such as digital twin technology, simulation software, and cloud-based collaborative platforms.

Global Engineering Software Market Size and Share by Region - Geographic distribution

The global engineering software market exhibits distinct regional characteristics and growth patterns across different geographic areas. North America currently holds a significant market share, driven by the presence of major technology companies, advanced manufacturing infrastructure, and early adoption of digital technologies. Europe represents another substantial market, characterized by strong automotive and aerospace industries, along with increasing focus on sustainable engineering solutions. The Asia-Pacific region is emerging as the fastest-growing market, fueled by rapid industrialization, expanding manufacturing capabilities, and increasing investments in infrastructure development. Countries such as China, India, and Japan are leading the growth in this region, supported by government initiatives promoting digital manufacturing and smart factory implementations. The Middle East and Africa region, while currently smaller in market size, shows promising growth potential due to increasing infrastructure investments and the adoption of advanced engineering technologies in construction and industrial projects. Latin America presents moderate growth opportunities, with Brazil and Mexico being key markets for engineering software adoption.

Regional Analysis of the Engineering Software Market - Detailed regional market performance

A detailed regional analysis of the engineering software market reveals distinct market dynamics and growth patterns across different geographic areas. In North America, the market is characterized by mature adoption rates, strong technological infrastructure, and significant investments in research and development. The region benefits from a robust ecosystem of software developers, engineering firms, and end-user industries that drive continuous innovation and adoption of advanced engineering solutions. Europe presents a market with strong emphasis on sustainable engineering practices, strict regulatory requirements, and a well-established manufacturing base. The region is witnessing increased adoption of digital twin technology and simulation software, particularly in the automotive and aerospace sectors. The Asia-Pacific region demonstrates the highest growth potential, driven by rapid industrialization, expanding manufacturing capabilities, and increasing government support for digital transformation initiatives. Countries like China and India are experiencing particularly strong growth due to their large manufacturing sectors and growing engineering talent pools. The Middle East and Africa region shows promising growth in infrastructure development projects and industrial diversification efforts, creating new opportunities for engineering software adoption. Latin America, while facing some economic challenges, presents opportunities in sectors such as oil and gas, mining, and construction, where engineering software solutions are increasingly being adopted to improve operational efficiency and project management.

Leading Company Profiles in the Engineering Software Market - Industry players and strategies

The engineering software market is dominated by several leading companies that have established strong market positions through continuous innovation, comprehensive product portfolios, and strategic business approaches. AVEVA stands out as a key player, particularly strong in industrial software solutions and digital transformation platforms for the process and energy industries. Autodesk Inc. maintains its leadership position through its widely adopted CAD and design software solutions, serving multiple industries from architecture to manufacturing. Dassault Systèmes has built a strong reputation for its 3D design, digital mock-up, and product lifecycle management solutions, particularly through its CATIA and SOLIDWORKS platforms. Hexagon AB has established itself as a leader in digital reality solutions, combining sensor, software, and autonomous technologies. PTC continues to innovate in areas such as Internet of Things, augmented reality, and product lifecycle management. Rockwell Automation, Inc. focuses on industrial automation and digital transformation solutions, while SAP SE brings its enterprise software expertise to engineering and manufacturing processes. Siemens maintains a strong presence through its comprehensive portfolio of digital enterprise solutions, and Synopsys, Inc. leads in electronic design automation and semiconductor design software. Vectorworks, Inc. specializes in design and Building Information Modeling (BIM) solutions for the architecture and entertainment industries. These companies are pursuing various strategies including cloud transformation, AI integration, strategic acquisitions, and industry-specific solutions to maintain and expand their market positions.

Porter's Five Forces Analysis of the Engineering Software Market - Competitive forces assessment

Porter's Five Forces analysis provides valuable insights into the competitive dynamics of the engineering software market. The threat of new entrants remains moderate to high, as the market requires significant investment in research and development, established distribution channels, and strong customer relationships. However, the increasing availability of cloud-based platforms and open-source alternatives has lowered some barriers to entry, particularly for specialized niche solutions. The bargaining power of buyers is increasing due to the growing availability of alternatives and the commoditization of certain software functionalities. Large enterprises have particularly strong negotiating power, while small and medium-sized businesses may have less influence. The bargaining power of suppliers, primarily software component providers and technology partners, remains moderate as engineering software companies can often develop key components in-house or through strategic partnerships. The threat of substitute products is significant, with traditional manual engineering methods, alternative software solutions, and emerging technologies all presenting potential substitutes. Competitive rivalry is intense, with major players competing on technology innovation, pricing, customer service, and comprehensive solution offerings. The market is characterized by continuous product development, strategic partnerships, and occasional consolidation through mergers and acquisitions.

SWOT Analysis of the Engineering Software Market - Strengths, weaknesses, opportunities, threats

A comprehensive SWOT analysis of the engineering software market reveals several key factors influencing its development and growth potential. The market's strengths include strong technological capabilities, widespread industry adoption, and the ability to drive significant improvements in engineering efficiency and innovation. The continuous advancement in technologies such as artificial intelligence, cloud computing, and simulation capabilities provides a solid foundation for market growth. However, the market faces certain weaknesses, including high implementation costs, the complexity of software integration, and the need for specialized training and expertise. These factors can create barriers to adoption, particularly for small and medium-sized enterprises. Opportunities abound in emerging markets, the growing demand for sustainable engineering solutions, and the increasing adoption of digital twin technology across industries. The market also benefits from the expanding applications of engineering software in new sectors such as renewable energy, electric vehicles, and biotechnology. Threats to the market include intense competition, the rapid pace of technological change requiring continuous innovation, and potential economic downturns that could impact capital investment in software solutions. Additionally, concerns about data security and privacy, as well as the increasing availability of open-source alternatives, pose challenges to market growth.

Engineering Software Market Value Chain Analysis - Industry structure and value flow

The engineering software market value chain encompasses multiple stages and participants, creating a complex ecosystem of value creation and delivery. At the foundation of the value chain are software developers and technology providers who create the core engineering software solutions, including CAD, CAM, CAE, and specialized simulation tools. These developers work closely with component suppliers who provide essential technologies such as graphics processing units, cloud infrastructure, and artificial intelligence frameworks. System integrators and consulting firms play a crucial role in implementing and customizing engineering software solutions for specific industry needs. Value-added resellers and distributors help expand market reach and provide local support services. End-user industries, including manufacturing, automotive, aerospace, construction, and electronics, represent the primary consumers of engineering software solutions. Supporting services such as training, maintenance, and technical support form an essential part of the value chain, ensuring successful software implementation and ongoing optimization. The value chain is further enhanced by partnerships and collaborations between different stakeholders, creating integrated solutions that address complex engineering challenges across the product lifecycle.

Key Investment Insights in the Engineering Software Market - Strategic investment recommendations

Investment insights in the engineering software market highlight several strategic opportunities for stakeholders looking to capitalize on market growth. The increasing adoption of cloud-based engineering solutions presents significant investment potential, as companies continue to migrate from traditional on-premise software to more flexible and scalable cloud platforms. Investments in artificial intelligence and machine learning capabilities within engineering software are particularly promising, as these technologies enable advanced simulation, predictive analytics, and automated design optimization. The growing demand for digital twin technology and simulation software represents another attractive investment opportunity, particularly in industries such as manufacturing, automotive, and aerospace. Emerging markets, especially in the Asia-Pacific region, offer substantial growth potential due to rapid industrialization and increasing adoption of advanced engineering technologies. Strategic investments in research and development, particularly in areas such as sustainable design, collaborative platforms, and industry-specific solutions, are likely to yield strong returns. Additionally, investments in companies that offer comprehensive, integrated engineering solutions that address multiple aspects of the product lifecycle are well-positioned for success in the evolving market landscape.

Engineering Software Market Conclusion - Summary and key takeaways

The engineering software market presents a compelling growth story, characterized by robust expansion, technological innovation, and increasing adoption across diverse industries. With a market size of 47.12 Billion in 2025 and projected to reach 85.57 Billion by 2032, growing at a CAGR of 8.90%, the market demonstrates strong growth potential driven by digital transformation initiatives and technological advancements. Key takeaways include the increasing importance of cloud-based solutions, the integration of artificial intelligence and machine learning capabilities, and the growing demand for sustainable engineering practices. The market is characterized by intense competition among major players, continuous innovation, and expanding applications across traditional and emerging industries. Regional analysis reveals varying growth patterns, with Asia-Pacific emerging as the fastest-growing market while North America and Europe maintain their positions as mature markets with strong technological infrastructure. The future of the engineering software market will be shaped by advancements in digital twin technology, simulation capabilities, and the continued convergence of engineering software with other emerging technologies such as IoT and augmented reality.

Research Methodology - How this research was conducted

The research methodology for this engineering software market analysis employed a comprehensive and systematic approach to ensure accuracy and reliability of findings. The study utilized both primary and secondary research methods to gather and validate market data. Primary research involved interviews with industry experts, software developers, end-users, and other stakeholders to gain insights into market trends, challenges, and opportunities. Secondary research included analysis of company annual reports, industry publications, market databases, and relevant academic sources to gather historical data and market intelligence. The research methodology incorporated data triangulation techniques to validate findings across multiple sources and ensure consistency. Market size calculations were based on both top-down and bottom-up approaches, considering various factors such as software type, application areas, and regional markets. The forecast period analysis utilized statistical modeling techniques and considered various market drivers, restraints, and macroeconomic factors to project future market growth. Regular updates and validation of data were conducted throughout the research process to maintain accuracy and relevance of the findings.

Research Scope - Coverage and limitations

The research scope for this engineering software market analysis encompasses a comprehensive examination of the global market, covering key segments, regional markets, competitive landscape, and future growth projections. The study focuses on major software categories including CAD, CAM, CAE, AEC, and EDA, as well as key application areas such as plant design, design automation, drafting & 3D modelling, and product design & testing. The research covers the period from 2025 to 2032, with detailed analysis of market trends, growth drivers, and challenges. Regional coverage includes North America, Europe, Asia-Pacific, Middle East & Africa, and Latin America, providing a global perspective on market dynamics. However, it's important to note certain limitations in the research scope, including the availability of detailed market data for certain emerging markets and the rapid pace of technological change that may impact future market developments. The study primarily focuses on commercial engineering software solutions and may not fully capture the impact of open-source alternatives or specialized niche solutions in certain segments.

Key Companies and Recent Developments in the Engineering Software Market - Introduction to top companies and their recent announcements, product launches, partnerships, and strategic developments

The engineering software market features several key companies that are driving innovation and shaping industry trends through their strategic initiatives and technological advancements. AVEVA has recently announced expanded partnerships focused on industrial AI and digital transformation solutions, particularly in the energy and process industries. Autodesk Inc. continues to enhance its cloud-based offerings with new features in its BIM and design software platforms, while also expanding its sustainability-focused solutions. Dassault Systèmes has made significant strides in virtual twin technology and announced new industry-specific solutions for sectors such as life sciences and renewable energy. Hexagon AB has strengthened its position in digital reality solutions through strategic acquisitions and partnerships, particularly in areas such as metrology and autonomous technologies. PTC has advanced its IoT and augmented reality capabilities, launching new solutions that integrate with its core CAD and PLM offerings. Rockwell Automation, Inc. has expanded its industrial automation portfolio through strategic acquisitions and partnerships focused on digital transformation. SAP SE continues to enhance its engineering and manufacturing solutions, particularly in areas such as supply chain management and digital manufacturing. Siemens has announced new digital enterprise solutions and expanded its Xcelerator platform with additional industry-specific applications. Synopsys, Inc. has launched new electronic design automation tools with enhanced AI capabilities for semiconductor design. Vectorworks, Inc. has introduced new BIM and design solutions with improved collaboration features and sustainability analysis capabilities. These companies are continuously evolving their product portfolios and strategic partnerships to address emerging market needs and technological trends.