Europe Third Party Logistics Market Overview - Definition, scope, and significance

The Europe Third Party Logistics (3PL) Market encompasses the outsourcing of logistics and supply chain management activities to specialized service providers. This market includes a comprehensive range of services such as transportation, warehousing, distribution, freight forwarding, and value-added services like packaging, labeling, and inventory management. The scope of the Europe 3PL market extends across various industries including automotive, healthcare, retail, consumer goods, and manufacturing sectors, serving both small & medium enterprises and large enterprises. The significance of this market lies in its ability to help businesses optimize their supply chain operations, reduce costs, improve efficiency, and focus on core competencies while leveraging the expertise and infrastructure of specialized logistics providers. As Europe continues to be a major hub for international trade and commerce, the 3PL market plays a crucial role in facilitating seamless movement of goods across the continent and beyond, supporting economic growth and international business operations.

Europe Third Party Logistics Market Drivers, Restraints, Challenges, and Opportunities

The Europe Third Party Logistics Market is driven by several key factors including the rapid growth of e-commerce, increasing globalization of supply chains, and the need for cost optimization by businesses. The expansion of cross-border trade within Europe and with other regions creates substantial demand for sophisticated logistics solutions. Additionally, the growing complexity of supply chain management and the need for advanced technology integration are pushing companies to outsource logistics functions to specialized providers. However, the market faces restraints such as high initial investment costs for infrastructure and technology, stringent regulatory requirements across different European countries, and the challenge of finding skilled workforce. The industry also faces challenges related to sustainability concerns, carbon footprint reduction, and the need for real-time visibility and transparency in supply chain operations. Despite these challenges, significant opportunities exist in the form of technological advancements including AI, IoT, and blockchain integration, the growing demand for last-mile delivery solutions, and the increasing focus on sustainable logistics practices. The market also presents opportunities in emerging sectors such as healthcare logistics and cold chain transportation.

Europe Third Party Logistics Market Growth Trends

The Europe Third Party Logistics Market is experiencing several notable growth trends that are reshaping the industry landscape. One of the most prominent trends is the increasing adoption of digital technologies and automation in logistics operations. This includes the implementation of warehouse management systems, transportation management systems, and the use of robotics and automated guided vehicles in warehousing facilities. Another significant trend is the growing emphasis on sustainability and green logistics, with companies investing in electric vehicles, sustainable packaging, and energy-efficient warehouses. The market is also witnessing a shift towards more integrated and end-to-end supply chain solutions, where 3PL providers offer comprehensive services beyond traditional transportation and warehousing. The rise of omnichannel retail and the need for faster delivery times are driving innovations in last-mile delivery solutions and urban logistics. Additionally, there is an increasing focus on data analytics and real-time tracking capabilities to provide better visibility and control over supply chain operations. The market is also seeing growth in specialized logistics services for specific industries, such as temperature-controlled transportation for pharmaceuticals and perishable goods.

COVID-19 Impact on the Europe Third Party Logistics Market

The COVID-19 pandemic had a profound impact on the Europe Third Party Logistics Market, initially causing significant disruptions in supply chains due to lockdowns, border closures, and workforce shortages. The pandemic exposed vulnerabilities in global supply chains and led to increased demand for resilient and flexible logistics solutions. During the peak of the crisis, there was a surge in demand for essential goods, medical supplies, and e-commerce deliveries, putting immense pressure on logistics providers to adapt quickly. Many 3PL companies had to implement new safety protocols, increase digital capabilities, and enhance their last-mile delivery services to meet changing consumer demands. The pandemic accelerated the adoption of digital technologies in logistics operations, including contactless delivery, real-time tracking, and automated warehousing solutions. While some sectors experienced temporary slowdowns, others saw unprecedented growth, particularly in healthcare logistics and e-commerce fulfillment. As the market recovers, there is a renewed focus on building more resilient supply chains, diversifying sourcing strategies, and investing in technology to better prepare for future disruptions.

Europe Third Party Logistics Market Competitive Landscape

The Europe Third Party Logistics Market features a highly competitive landscape with a mix of global giants and regional players vying for market share. The market is characterized by the presence of major international logistics companies such as Deutsche Post AG, DHL Supply Chain Solutions, Kuehne + Nagel International AG, DB Schenker, and XPO Logistics, Inc., which have established extensive networks across Europe. These large players compete on the basis of their comprehensive service offerings, technological capabilities, and global reach. The market also includes strong regional players who leverage their local expertise and networks to serve specific geographic areas or industry segments. Competition in the market is intense, with companies focusing on service quality, technological innovation, and pricing strategies to differentiate themselves. There is also a trend towards strategic partnerships, mergers, and acquisitions as companies seek to expand their capabilities and market presence. The competitive landscape is further shaped by the entry of new players, particularly in the technology-driven segments of the market, and the growing influence of e-commerce companies developing their own logistics capabilities.

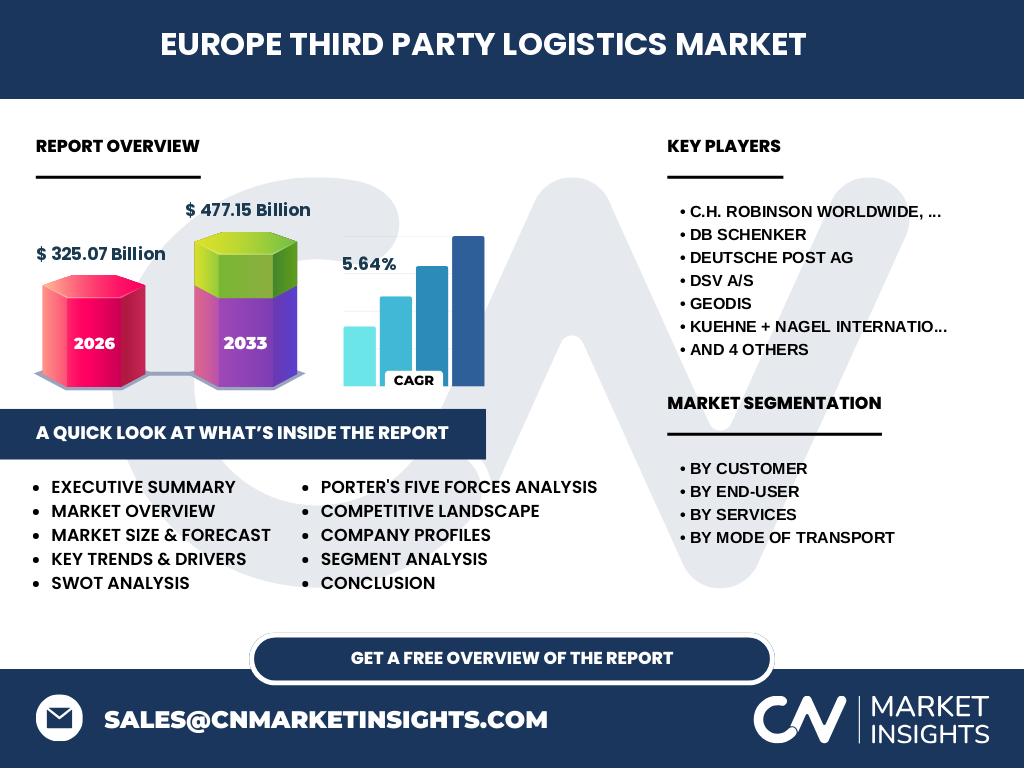

Executive Summary

The Europe Third Party Logistics Market is poised for significant growth, with the market size projected to reach 325.07 Billion in 2026 and expand to 477.15 Billion by 2033, representing a CAGR of 5.64% during the forecast period. This growth is driven by the increasing complexity of supply chains, the rise of e-commerce, and the growing need for cost-effective logistics solutions across various industries. The market is segmented by customer type (Small & Medium Enterprises and Large Enterprises), end-user industries (Automotive, Healthcare, Retail, Consumer Goods), services (International Transportation, Warehousing, Domestic Transportation, Inventory Management), and mode of transport (Roadways, Railways, Waterways, Airways). Key players in the market include C.H. Robinson Worldwide, Inc., DB Schenker, Deutsche Post AG, DSV A/S, Geodis, Kuehne + Nagel International AG, Nippon Express Co., Ltd., Sinotrans Co., Ltd., UPS Supply Chain Solutions, and XPO Logistics, Inc. The market is characterized by intense competition, technological innovation, and a growing focus on sustainability. As businesses continue to seek ways to optimize their supply chain operations and improve efficiency, the demand for third-party logistics services in Europe is expected to remain strong, presenting significant opportunities for market participants.

Europe Third Party Logistics Market Forecast

The Europe Third Party Logistics Market is projected to experience steady growth from 2027 to 2033, with the market size expected to increase from 325.07 Billion to 477.15 Billion during this period. This represents a compound annual growth rate (CAGR) of 5.64%, indicating a robust and sustainable expansion of the market. The forecast period is characterized by several key factors that will influence market growth, including the continued expansion of e-commerce, increasing cross-border trade within Europe, and the growing adoption of advanced technologies in logistics operations. The market is expected to benefit from the ongoing digital transformation of supply chains, with increased implementation of IoT, AI, and blockchain technologies. Additionally, the focus on sustainability and green logistics is likely to drive investments in eco-friendly transportation and warehousing solutions. The healthcare and retail sectors are anticipated to be significant growth drivers, particularly with the increasing demand for temperature-controlled logistics and last-mile delivery solutions. As businesses continue to recognize the benefits of outsourcing logistics functions, the market is well-positioned for sustained growth throughout the forecast period.

Europe Third Party Logistics Market Size and Share by Segmentation

The Europe Third Party Logistics Market can be analyzed through various segmentation perspectives to understand its composition and growth dynamics. By customer type, the market serves both Small & Medium Enterprises (SMEs) and Large Enterprises, with large enterprises typically accounting for a significant portion of the market share due to their higher logistics needs and outsourcing budgets. In terms of end-user industries, the Automotive sector represents a substantial segment, driven by the complex supply chain requirements of automotive manufacturing and distribution. The Healthcare sector is another significant segment, characterized by the need for specialized logistics services such as temperature-controlled transportation and strict regulatory compliance. The Retail and Consumer Goods sectors also contribute notably to the market, particularly with the growth of e-commerce and changing consumer expectations for fast delivery. By services, International Transportation and Warehousing are typically the largest segments, reflecting the importance of cross-border trade and the need for storage and distribution facilities. Domestic Transportation and Inventory Management services also play crucial roles in the overall market structure. The mode of transport segmentation shows that Roadways currently dominate due to their flexibility and extensive network coverage, while Railways, Waterways, and Airways each serve specific logistics needs based on distance, cost, and type of goods transported.

Global Europe Third Party Logistics Market Size and Share by Region

The Europe Third Party Logistics Market demonstrates significant regional variations in terms of market size and share across different European countries and sub-regions. Western Europe, comprising countries such as Germany, France, the United Kingdom, and the Netherlands, typically represents the largest share of the market due to its advanced industrial base, high volume of international trade, and well-developed logistics infrastructure. Germany, in particular, stands out as a major logistics hub, given its central location and strong manufacturing sector. Southern Europe, including Italy, Spain, and Portugal, shows growing market potential, driven by increasing trade activities and the development of logistics capabilities. Eastern Europe is emerging as an attractive region for 3PL services, with countries like Poland, Czech Republic, and Hungary experiencing rapid growth in manufacturing and logistics outsourcing. The Nordic countries contribute to the market with their focus on sustainable logistics solutions and advanced technological adoption. The Benelux region (Belgium, Netherlands, Luxembourg) plays a crucial role due to its strategic location for international trade and the presence of major ports. Each region's market share is influenced by factors such as economic development, industrialization levels, trade volumes, and the presence of key industries that require logistics services.

Regional Analysis of the Europe Third Party Logistics Market

The Europe Third Party Logistics Market exhibits distinct characteristics and growth patterns across different regions, reflecting the diverse economic landscape and industrial strengths of the continent. Western Europe, led by Germany, France, and the UK, dominates the market with its advanced logistics infrastructure, high concentration of multinational corporations, and significant international trade volumes. This region benefits from well-established transportation networks, including major ports, airports, and intermodal facilities, making it a preferred location for logistics operations. Southern Europe, particularly Italy and Spain, shows strong growth potential driven by increasing manufacturing activities and the development of logistics hubs to serve the Mediterranean trade routes. Eastern Europe is emerging as a key growth region, with countries like Poland, Czech Republic, and Hungary attracting investments in logistics infrastructure and serving as manufacturing bases for European companies. The Nordic countries contribute to the market with their focus on sustainability and technological innovation in logistics, while the Baltic states are gaining importance as logistics gateways between Europe and Russia. The Benelux region continues to play a crucial role due to its strategic location, with major ports like Rotterdam and Antwerp serving as vital logistics nodes. Each region's market dynamics are influenced by factors such as local economic conditions, regulatory environments, and the presence of key industries that drive logistics demand.

Leading Company Profiles in the Europe Third Party Logistics Market

The Europe Third Party Logistics Market is characterized by the presence of several major players who have established strong market positions through their comprehensive service offerings and extensive networks. C.H. Robinson Worldwide, Inc. is known for its technology-driven approach to logistics, offering a wide range of services including freight transportation, warehousing, and supply chain consulting. DB Schenker, a division of Deutsche Bahn, is one of Europe's largest logistics providers, with a strong presence in both domestic and international markets, offering end-to-end supply chain solutions. Deutsche Post AG, through its DHL Supply Chain division, is a global leader in logistics, providing services across various industries with a focus on innovation and sustainability. DSV A/S has grown significantly through strategic acquisitions and offers a comprehensive portfolio of transport and logistics services across Europe. Geodis, part of the SNCF Group, specializes in supply chain optimization and has a strong presence in contract logistics and freight forwarding. Kuehne + Nagel International AG is renowned for its sea freight and air freight services, as well as its advanced IT solutions for logistics management. Nippon Express Co., Ltd. brings strong Asian connections to the European market, offering integrated logistics solutions. Sinotrans Co., Ltd. is a major player in China-Europe trade lanes, providing comprehensive logistics services. UPS Supply Chain Solutions leverages the global UPS network to offer customized logistics solutions, while XPO Logistics, Inc. is known for its technology-driven approach and asset-light business model in Europe.

Porter's Five Forces Analysis of the Europe Third Party Logistics Market

Porter's Five Forces analysis provides valuable insights into the competitive dynamics of the Europe Third Party Logistics Market. The threat of new entrants is moderate, as the market requires significant capital investment in infrastructure, technology, and establishing a reliable network, which can be barriers to entry. However, technological advancements and the rise of digital freight marketplaces are lowering some entry barriers. The bargaining power of buyers is relatively high due to the availability of multiple service providers and the commoditization of certain logistics services. Large customers can often negotiate favorable terms and demand value-added services. The bargaining power of suppliers is moderate, with key suppliers including transportation providers, warehouse operators, and technology vendors. The threat of substitute products or services is low, as logistics is an essential function that is difficult to substitute. However, the trend of companies developing in-house logistics capabilities poses a potential long-term threat. Competitive rivalry in the market is intense, with numerous global and regional players competing on price, service quality, and technological capabilities. The market is characterized by price pressure, service differentiation efforts, and strategic partnerships to gain competitive advantage. Overall, the 5 Forces analysis suggests a moderately attractive market with opportunities for established players to leverage their scale and capabilities while facing pressure on margins and the need for continuous innovation.

SWOT Analysis of the Europe Third Party Logistics Market

A SWOT analysis of the Europe Third Party Logistics Market reveals key strengths, weaknesses, opportunities, and threats that shape the industry landscape. Strengths of the market include a well-developed infrastructure across Europe, advanced technological capabilities, and the presence of established global players with extensive networks. The market also benefits from the strategic geographic location of Europe for international trade and the high level of economic integration within the European Union. However, weaknesses exist in the form of high operational costs, particularly in Western European countries, and the complexity of navigating diverse regulatory environments across different European nations. The market faces opportunities in the growing e-commerce sector, the increasing demand for sustainable logistics solutions, and the potential for digital transformation through technologies like AI and IoT. Additionally, the expansion of cross-border e-commerce and the development of new trade corridors present significant growth opportunities. Threats to the market include economic uncertainties, geopolitical tensions that may disrupt trade flows, and the potential for supply chain disruptions due to various factors such as pandemics or natural disasters. The market also faces challenges from increasing competition, both from traditional logistics providers and new technology-driven entrants, as well as the need to continuously invest in technology and sustainability initiatives to remain competitive.

Europe Third Party Logistics Market Value Chain Analysis

The value chain analysis of the Europe Third Party Logistics Market provides insights into the various stages and activities that create and deliver value in the industry. The primary activities in the value chain include inbound logistics, where 3PL providers manage the receipt and storage of goods from suppliers; operations, which involve the processing and handling of products in warehouses or distribution centers; outbound logistics, covering the distribution of finished goods to customers; marketing and sales, where providers promote their services and acquire customers; and service, which includes after-sales support and value-added services. Support activities in the value chain include procurement of transportation assets and technology, technology development for logistics management systems, human resource management to ensure skilled workforce, and infrastructure development for warehousing and transportation networks. The value chain is characterized by significant interdependence between activities, with technology playing an increasingly crucial role in integrating and optimizing various stages. For instance, advanced warehouse management systems can enhance inventory accuracy, while transportation management systems can optimize route planning and reduce costs. The value chain also includes partnerships and collaborations with carriers, technology providers, and industry-specific experts to deliver comprehensive logistics solutions. As the market evolves, there is a growing emphasis on adding value through services such as supply chain consulting, reverse logistics, and customized reporting and analytics.

Key Investment Insights in the Europe Third Party Logistics Market

The Europe Third Party Logistics Market presents several compelling investment opportunities driven by the sector's growth potential and evolving dynamics. Key investment insights suggest focusing on technology-driven logistics solutions, as the market is experiencing rapid digital transformation. Investments in warehouse automation, AI-powered supply chain analytics, and IoT-enabled tracking systems are likely to yield significant returns as companies seek to improve efficiency and reduce costs. The growing e-commerce sector represents another attractive investment area, particularly in last-mile delivery solutions and urban logistics facilities. Sustainability is emerging as a critical investment theme, with opportunities in electric vehicle fleets, green warehousing, and circular economy logistics solutions. Investors should also consider the potential of specialized logistics services for high-growth sectors such as healthcare and pharmaceuticals, which require temperature-controlled transportation and strict compliance with regulatory standards. The market's consolidation trend presents opportunities for strategic acquisitions and mergers, allowing companies to expand their geographic presence and service offerings. Additionally, investments in data analytics and predictive modeling capabilities can provide a competitive edge in optimizing supply chain operations. The development of intermodal transportation solutions and the integration of rail and sea freight with last-mile delivery services offer potential for improving efficiency and reducing environmental impact. As the market continues to evolve, investments that align with the trends of digitalization, sustainability, and supply chain resilience are likely to generate the most value.

Europe Third Party Logistics Market Conclusion

The Europe Third Party Logistics Market is positioned for sustained growth, with the market size expected to increase from 325.07 Billion in 2026 to 477.15 Billion by 2033, representing a CAGR of 5.64%. This growth is underpinned by the increasing complexity of supply chains, the rise of e-commerce, and the growing need for cost-effective and efficient logistics solutions across various industries. The market's segmentation by customer type, end-user industries, services, and mode of transport reflects its diverse and dynamic nature, catering to the specific needs of different sectors and business sizes. The competitive landscape is characterized by the presence of major global players and regional specialists, all vying to offer innovative and comprehensive logistics solutions. As the market continues to evolve, key trends such as digitalization, sustainability, and the integration of advanced technologies will shape its future trajectory. The COVID-19 pandemic has further highlighted the importance of resilient and flexible supply chains, potentially accelerating investments in logistics capabilities. Overall, the Europe Third Party Logistics Market presents significant opportunities for growth and innovation, driven by changing consumer expectations, technological advancements, and the ongoing globalization of trade. Companies that can effectively navigate these trends and offer value-added, technology-driven solutions are likely to emerge as leaders in this dynamic and essential industry.

Research Methodology

The research methodology for this Europe Third Party Logistics Market report involved a comprehensive and systematic approach to gather, analyze, and interpret data. The process began with extensive secondary research, utilizing reputable industry reports, market databases, company annual reports, and government publications to establish a foundation of market knowledge. This was complemented by primary research, including interviews with industry experts, logistics providers, and key stakeholders to gain insights into market trends, challenges, and opportunities. Data triangulation methods were employed to cross-verify information from multiple sources, ensuring accuracy and reliability. The market size and growth projections were derived using both top-down and bottom-up approaches, considering factors such as historical growth rates, industry trends, and economic indicators. Segmentation analysis was conducted to understand the market composition across different customer types, end-user industries, services, and modes of transport. Competitive analysis involved evaluating company profiles, market shares, and strategic developments of key players. The research also incorporated an analysis of macroeconomic factors, regulatory environments, and technological advancements influencing the market. Throughout the process, particular attention was paid to recent developments, such as the impact of COVID-19 on logistics operations and the growing emphasis on sustainability in the industry.

Research Scope

The research scope for this Europe Third Party Logistics Market report encompasses a comprehensive analysis of the market across various dimensions. The study covers the period from 2026 to 2033, with 2026 as the base year and projections extending to 2033. The geographic scope is focused on Europe, including all European Union countries as well as non-EU European nations. The market is analyzed across four key segmentation criteria: customer type (Small & Medium Enterprises and Large Enterprises), end-user industries (Automotive, Healthcare, Retail, Consumer Goods), services (International Transportation, Warehousing, Domestic Transportation, Inventory Management), and mode of transport (Roadways, Railways, Waterways, Airways). The research includes an analysis of market size, growth trends, competitive landscape, and key market dynamics such as drivers, restraints, opportunities, and challenges. The scope also covers the impact of COVID-19 on the market, regional variations in market performance, and the strategies of leading companies. Additionally, the study includes specialized analyses such as Porter's Five Forces, SWOT analysis, and value chain analysis to provide a holistic view of the market. The research aims to provide actionable insights for stakeholders, including logistics providers, investors, and businesses seeking to understand or enter the European 3PL market.

Key Companies and Recent Developments in the Europe Third Party Logistics Market

The Europe Third Party Logistics Market is dominated by several key companies that have established strong market positions through their comprehensive service offerings and extensive networks. C.H. Robinson Worldwide, Inc. has been focusing on digital freight solutions and expanding its European presence through strategic partnerships. DB Schenker, a division of Deutsche Bahn, continues to strengthen its position as one of Europe's largest logistics providers, with recent investments in sustainable transportation solutions and digital platforms. Deutsche Post AG, through its DHL Supply Chain division, has been at the forefront of innovation in logistics, with developments in automation, robotics, and green logistics initiatives. DSV A/S has made significant strides through strategic acquisitions, most notably the acquisition of Agility's global warehousing business, expanding its footprint in key European markets. Geodis has been focusing on enhancing its supply chain optimization capabilities and expanding its contract logistics services across Europe. Kuehne + Nagel International AG continues to leverage its strong air and sea freight capabilities while investing in digital solutions for supply chain visibility. Nippon Express Co., Ltd. has been strengthening its European operations, particularly in serving the automotive and high-tech industries. Sinotrans Co., Ltd. has been expanding its presence in Europe, capitalizing on growing trade between China and European countries. UPS Supply Chain Solutions has been enhancing its e-commerce fulfillment capabilities and last-mile delivery services. XPO Logistics, Inc. has been focusing on technology-driven solutions and asset-light business models in its European operations. These companies have been actively involved in recent developments such as the adoption of electric vehicle fleets, implementation of AI and IoT technologies in logistics operations, and the development of sustainable warehousing solutions to meet evolving customer demands and regulatory requirements.