Osteoporosis Treatment Market Overview - Definition, scope, and significance

The Osteoporosis Treatment Market encompasses pharmaceutical interventions and therapeutic approaches designed to prevent, manage, and treat osteoporosis, a progressive bone disease characterized by decreased bone mass and density, leading to increased fracture risk. This market includes various drug classes such as bisphosphonates, selective estrogen receptor modulators (SERMs), calcitonin, and parathyroid hormone-related anabolic agents, along with supportive treatments and delivery mechanisms through hospital pharmacies, retail pharmacies, and online pharmacies. The market's significance lies in its critical role in addressing the global burden of osteoporosis, particularly among aging populations, where fractures can severely impact quality of life, increase mortality rates, and create substantial healthcare costs. With the rising prevalence of osteoporosis, especially among postmenopausal women and elderly individuals, this market represents a vital component of preventive healthcare and chronic disease management strategies worldwide.

Osteoporosis Treatment Market Drivers, Restraints, Challenges, and Opportunities - Key growth factors and obstacles

The primary drivers of the Osteoporosis Treatment Market include the rapidly aging global population, increasing awareness about bone health, and rising healthcare expenditure. Growing prevalence of osteoporosis, particularly in developed nations with higher life expectancies, creates sustained demand for effective treatments. Additionally, advancements in diagnostic technologies and screening programs have improved early detection rates, driving earlier intervention and treatment initiation. However, the market faces several restraints, including high treatment costs, potential side effects of long-term medication use, and limited patient adherence to prescribed regimens. Challenges include the need for more effective therapies with fewer side effects, addressing treatment gaps in developing regions, and managing the complex interplay between osteoporosis and other age-related conditions. Opportunities exist in developing novel drug formulations, expanding into emerging markets, and leveraging digital health technologies for improved patient monitoring and medication adherence. The market also benefits from increasing research into regenerative therapies and personalized medicine approaches tailored to individual patient risk profiles.

Osteoporosis Treatment Market Growth Trends - Current and emerging trends shaping the market

The Osteoporosis Treatment Market is experiencing several notable growth trends that are reshaping the industry landscape. One prominent trend is the shift toward combination therapies that target multiple pathways involved in bone metabolism, offering potentially superior efficacy compared to monotherapy approaches. Another significant trend is the development of long-acting injectable formulations that reduce dosing frequency and improve patient compliance. The market is also witnessing increased focus on anabolic therapies that stimulate bone formation rather than merely slowing bone resorption, representing a paradigm shift in treatment philosophy. Emerging trends include the integration of artificial intelligence and machine learning in treatment optimization, the rise of telemedicine for remote patient monitoring, and growing interest in nutraceuticals and complementary therapies alongside conventional pharmaceutical treatments. Additionally, there is a trend toward personalized medicine approaches that consider genetic factors, lifestyle variables, and individual risk factors to tailor treatment regimens. The market is also seeing increased investment in regenerative medicine approaches, including stem cell therapies and tissue engineering solutions for bone regeneration.

COVID-19 Impact on the Osteoporosis Treatment Market - Pandemic effects and recovery trajectory

The COVID-19 pandemic has had a multifaceted impact on the Osteoporosis Treatment Market, creating both challenges and opportunities. During the initial pandemic phases, healthcare systems worldwide experienced significant disruptions, with many routine osteoporosis screenings and consultations being postponed or canceled due to lockdown measures and prioritization of COVID-19 care. This led to delayed diagnoses and treatment initiation for many patients, potentially exacerbating the disease burden. However, the pandemic also accelerated the adoption of telemedicine and remote monitoring solutions, which have become increasingly important for managing chronic conditions like osteoporosis. The market witnessed supply chain disruptions affecting drug availability and distribution, while economic uncertainties impacted healthcare budgets and patient affordability in some regions. Looking at the recovery trajectory, the market is rebounding as healthcare systems adapt to the new normal, with renewed focus on preventive care and chronic disease management. The pandemic has also heightened awareness about bone health, particularly among elderly populations who are at higher risk for both COVID-19 complications and osteoporosis-related fractures. This increased awareness, combined with the normalization of digital health solutions, is expected to drive market recovery and create new opportunities for innovative treatment delivery models.

Osteoporosis Treatment Market Competitive Landscape - Major competitors and market consolidation

The Osteoporosis Treatment Market features a moderately consolidated competitive landscape dominated by several key pharmaceutical companies with established portfolios and strong research capabilities. Major competitors include Amgen Inc., Novartis AG, Eli Lilly and Company, Pfizer Inc., and Daiichi Sankyo Company, Limited, among others. These companies compete based on factors such as drug efficacy, safety profiles, pricing, and innovative delivery mechanisms. The market has witnessed strategic collaborations and partnerships aimed at developing next-generation therapies and expanding geographic presence. Competition is intensifying with the entry of biosimilar products and the development of novel treatment modalities that offer improved efficacy or reduced side effects compared to traditional therapies. Companies are investing heavily in research and development to maintain competitive advantages, with particular focus on anabolic agents and combination therapies. The competitive landscape is also characterized by patent expirations of key blockbuster drugs, creating opportunities for generic manufacturers while challenging innovator companies to develop new intellectual property. Geographic expansion strategies, particularly into emerging markets with growing elderly populations, represent another competitive dimension as companies seek to capitalize on untapped market potential.

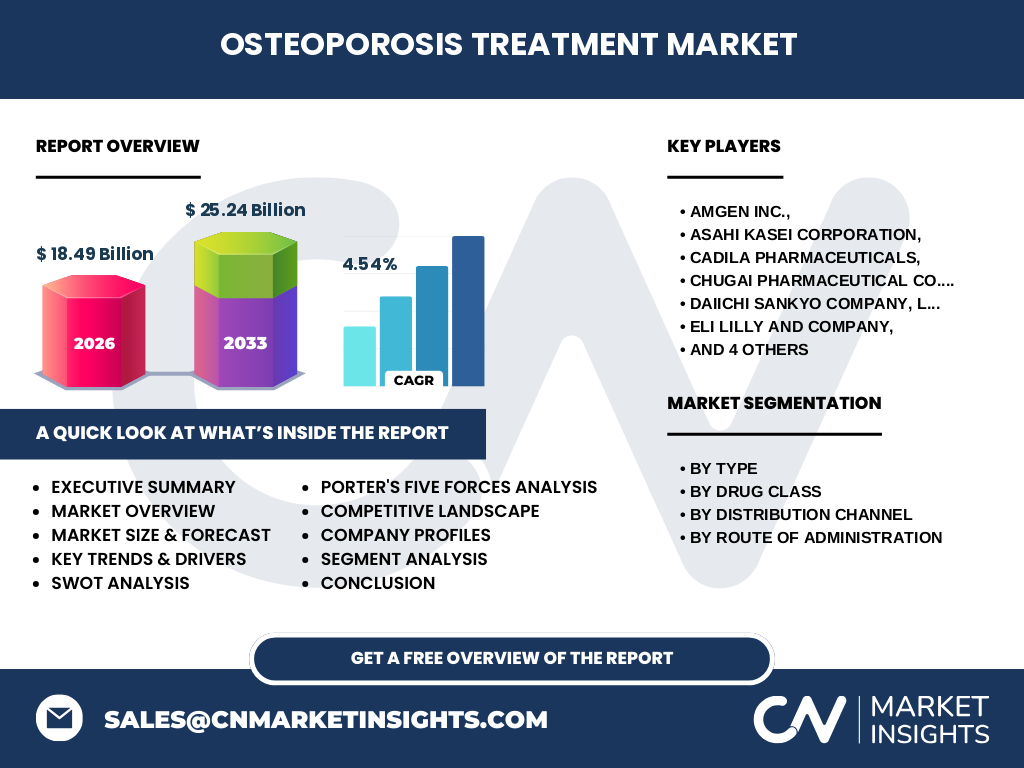

Executive Summary - High-level overview and key findings about Osteoporosis Treatment Market

The Osteoporosis Treatment Market represents a critical segment of the pharmaceutical industry, addressing the growing global burden of bone density disorders among aging populations. With a market size of $18.49 billion projected for 2026 and expected to reach $25.24 billion by 2033, growing at a CAGR of 4.54%, the market demonstrates steady growth driven by demographic shifts and increasing disease awareness. Key findings indicate that bisphosphonates remain the dominant drug class, while emerging anabolic therapies are gaining traction for their ability to stimulate bone formation. The market is characterized by diverse distribution channels, with hospital pharmacies maintaining significant share while online pharmacies experience rapid growth. Geographic analysis reveals strong market presence in North America and Europe, with Asia-Pacific emerging as a high-growth region due to improving healthcare infrastructure and rising disposable incomes. The competitive landscape features established pharmaceutical giants alongside innovative biotechnology firms, with strategic collaborations and R&D investments shaping market dynamics. Overall, the market presents substantial opportunities for growth through technological innovation, geographic expansion, and the development of personalized treatment approaches that address the complex needs of osteoporosis patients.

Osteoporosis Treatment Market Forecast - Projections for 2025-2032 period

The Osteoporosis Treatment Market is projected to experience steady growth throughout the 2025-2032 period, building on the established trajectory of 4.54% CAGR. The market is expected to expand from its 2026 baseline of $18.49 billion to reach approximately $25.24 billion by 2033, representing significant absolute growth of $6.75 billion over the forecast period. This growth will be driven by multiple factors, including continued demographic aging in developed markets, increasing healthcare access in emerging economies, and ongoing innovation in treatment modalities. The forecast period will likely see the introduction of several novel therapies, particularly in the anabolic drug class, which could accelerate market expansion beyond current projections. Geographic expansion will play a crucial role, with Asia-Pacific and Latin American markets expected to outperform mature markets in terms of growth rates. The distribution channel landscape is anticipated to evolve, with online pharmacies gaining substantial market share as digital health adoption increases. Additionally, the forecast period will likely witness increased focus on combination therapies and personalized medicine approaches, potentially creating new market segments and revenue streams. Economic factors, including healthcare spending trends and insurance coverage policies, will significantly influence market dynamics across different regions during this period.

Osteoporosis Treatment Market Size and Share by Segmentation - Breakdown by {segmentData}

The Osteoporosis Treatment Market exhibits distinct segmentation patterns across various dimensions. By type, the market is divided between primary osteoporosis, which accounts for the majority share due to its higher prevalence, and secondary osteoporosis, which represents a smaller but growing segment linked to various medical conditions and medications. Within drug class segmentation, bisphosphonates maintain the largest market share due to their established efficacy, cost-effectiveness, and widespread adoption, while selective estrogen receptor modulators (SERMs) represent the second-largest segment, particularly among postmenopausal women. The calcitonin segment, though smaller, serves specific patient populations, while PTH-related anabolic agents, despite their higher cost, are experiencing the fastest growth rate due to their unique mechanism of action in stimulating bone formation. Distribution channel analysis reveals that hospital pharmacies command the largest share, driven by institutional prescriptions and complex treatment regimens, followed by retail pharmacies which benefit from convenience and accessibility. Online pharmacies represent the fastest-growing distribution channel, particularly accelerated by the COVID-19 pandemic's impact on digital health adoption. By route of administration, oral medications dominate the market due to patient preference and ease of use, while injectable formulations, though representing a smaller share, are gaining traction for their convenience in long-acting formulations and specific clinical indications.

Global Osteoporosis Treatment Market Size and Share by Region - Geographic distribution

The global Osteoporosis Treatment Market demonstrates significant regional variations in market size, growth rates, and treatment preferences. North America currently represents the largest regional market, driven by high healthcare expenditure, advanced medical infrastructure, and a substantial aging population. Europe follows as the second-largest market, characterized by strong government healthcare initiatives and high disease awareness. The Asia-Pacific region, while currently smaller in absolute terms, exhibits the highest growth rate, propelled by rapidly aging populations in countries like Japan, China, and South Korea, along with improving healthcare access and rising disposable incomes. Latin America presents a growing market with increasing urbanization and healthcare modernization, though economic volatility in some countries creates market uncertainties. The Middle East and Africa region, while representing the smallest market share, shows promising growth potential driven by improving healthcare infrastructure and increasing awareness about osteoporosis. Regional differences in treatment preferences are notable, with developed markets showing higher adoption of newer, premium therapies, while emerging markets often rely more heavily on cost-effective generic options. Regulatory environments also vary significantly across regions, influencing market access and product availability, with some regions implementing favorable policies for innovative treatments while others maintain more conservative approaches to drug approvals and reimbursements.

Regional Analysis of the Osteoporosis Treatment Market - Detailed regional market performance

Regional analysis of the Osteoporosis Treatment Market reveals distinct market characteristics and growth dynamics across different geographic areas. In North America, particularly the United States, the market benefits from high disease awareness, strong reimbursement frameworks, and early adoption of innovative therapies. The region's market is characterized by high per capita treatment rates and significant investment in research and development. Europe demonstrates strong market performance driven by comprehensive healthcare systems, aging populations in Western European countries, and proactive osteoporosis screening programs. However, economic disparities between Western and Eastern Europe create varying market dynamics, with Eastern European markets showing lower treatment rates but higher growth potential. The Asia-Pacific region presents a complex landscape where developed markets like Japan and Australia show high treatment sophistication, while emerging economies in Southeast Asia are experiencing rapid market expansion due to improving healthcare infrastructure and increasing disease awareness. China represents a particularly significant growth opportunity due to its massive elderly population and improving healthcare access. Latin American markets, led by Brazil and Mexico, show steady growth driven by urbanization and healthcare modernization, though economic volatility in some countries creates market uncertainties. The Middle East and Africa region, while currently representing a smaller market share, demonstrates promising growth in Gulf Cooperation Council countries, with South Africa emerging as a regional leader in treatment adoption.

Leading Company Profiles in the Osteoporosis Treatment Market - Industry players and strategies

The Osteoporosis Treatment Market features several prominent companies with distinct strategic approaches and market positions. Amgen Inc. has established itself as a leader through its innovative anabolic therapies, particularly with teriparatide-based treatments that stimulate bone formation. The company's strategy focuses on premium positioning and leveraging its strong R&D capabilities to maintain competitive advantages. Novartis AG maintains a significant market presence through its diverse portfolio of osteoporosis treatments, including both established bisphosphonates and newer therapies, supported by a global distribution network and strategic partnerships. Eli Lilly and Company has gained market share through its focus on anabolic agents and combination therapies, emphasizing clinical differentiation and patient outcomes. Pfizer Inc. leverages its extensive pharmaceutical expertise and global reach, with a strategy centered on portfolio optimization and strategic acquisitions to strengthen its market position. Daiichi Sankyo Company, Limited brings strong presence in Asian markets, particularly Japan, where it has developed treatments tailored to regional patient needs and regulatory requirements. Other notable players include Asahi Kasei Corporation, which focuses on innovative drug delivery systems, and Teva Pharmaceuticals Inc., which has established itself in the generic and biosimilar segments. These companies employ various strategies including R&D investment, geographic expansion, strategic partnerships, and portfolio diversification to maintain and grow their market positions in this competitive landscape.

Porter's Five Forces Analysis of the Osteoporosis Treatment Market - Competitive forces assessment

Porter's Five Forces analysis reveals important insights into the competitive dynamics of the Osteoporosis Treatment Market. The threat of new entrants remains moderate due to high barriers to entry, including substantial R&D costs, stringent regulatory requirements, and the need for extensive clinical trial data to demonstrate safety and efficacy. However, the potential for innovative biotechnology firms to enter the market with novel treatment approaches creates ongoing competitive pressure. The bargaining power of buyers, primarily healthcare providers and patients, is increasing due to greater treatment options and growing price sensitivity, particularly in markets with healthcare cost containment measures. Supplier bargaining power is relatively low for most components, though specialized raw materials for certain advanced therapies may command higher prices. The threat of substitutes is moderate, with alternative treatments and preventive measures (such as lifestyle modifications and nutritional supplements) competing with pharmaceutical interventions, though their efficacy limitations limit substitution potential. Competitive rivalry among existing players is intense, characterized by ongoing patent expirations, the entry of biosimilars, and continuous innovation efforts. Companies compete on multiple dimensions including efficacy, safety, pricing, and delivery convenience. The overall industry attractiveness remains favorable due to consistent demand growth, though profit margins may face pressure from generic competition and cost containment measures in various healthcare systems.

SWOT Analysis of the Osteoporosis Treatment Market - Strengths, weaknesses, opportunities, threats

A comprehensive SWOT analysis of the Osteoporosis Treatment Market reveals several key factors shaping its current and future trajectory. Strengths of the market include strong and growing demand driven by aging populations worldwide, established treatment protocols with proven efficacy, and continuous innovation in drug development leading to improved therapeutic options. The market also benefits from increasing disease awareness and screening programs that drive earlier diagnosis and treatment initiation. However, weaknesses exist in the form of high treatment costs limiting access in some regions, potential side effects associated with long-term medication use creating patient hesitancy, and the complex nature of osteoporosis requiring multifaceted treatment approaches. Opportunities abound in emerging markets with growing healthcare infrastructure, the development of novel therapies with improved efficacy and safety profiles, and the integration of digital health technologies for better patient monitoring and adherence. Additionally, the potential for personalized medicine approaches based on genetic and biomarker profiling represents a significant opportunity for market expansion. Threats to the market include increasing price pressure from healthcare cost containment measures, potential regulatory challenges for new drug approvals, competition from alternative therapies and preventive approaches, and the economic impact of global events that could affect healthcare spending priorities. The market also faces threats from potential safety concerns with existing treatments that could lead to decreased utilization or stricter prescribing guidelines.

Osteoporosis Treatment Market Value Chain Analysis - Industry structure and value flow

The Osteoporosis Treatment Market value chain encompasses multiple interconnected stages, each contributing to the delivery of effective treatments to patients. The chain begins with research and development, where pharmaceutical companies and biotechnology firms invest heavily in discovering and developing new drug candidates, supported by academic institutions and research organizations. This is followed by preclinical testing and clinical trials, representing significant cost centers that determine whether potential treatments advance to market approval. Regulatory approval represents a critical gatekeeping stage, with agencies like the FDA and EMA evaluating safety and efficacy data before granting market access. Manufacturing involves both large-scale production of active pharmaceutical ingredients and formulation development, with quality control processes ensuring product consistency and compliance. Distribution channels, including hospital pharmacies, retail pharmacies, and increasingly online pharmacies, serve as the bridge between manufacturers and end-users, with each channel offering distinct advantages in terms of reach and patient convenience. Healthcare providers, including physicians, specialists, and pharmacists, play a crucial role in prescribing decisions and patient education. Insurance companies and government payers influence market dynamics through coverage policies and reimbursement decisions that affect patient access and treatment affordability. Finally, patients and caregivers represent the end-users whose needs and preferences ultimately drive market demand, with patient support programs and adherence initiatives playing important roles in treatment success. This value chain is characterized by complex interdependencies, with innovations or disruptions at any stage potentially impacting the entire system.

Key Investment Insights in the Osteoporosis Treatment Market - Strategic investment recommendations

Strategic investment insights for the Osteoporosis Treatment Market highlight several promising areas for capital allocation and business development. Investment in research and development of novel anabolic therapies represents a particularly attractive opportunity, as these treatments that stimulate bone formation rather than merely inhibiting resorption are gaining traction and commanding premium pricing. Companies should consider increasing R&D investment in combination therapies that target multiple pathways involved in bone metabolism, potentially offering superior efficacy compared to monotherapy approaches. Geographic expansion into emerging markets, particularly in Asia-Pacific and Latin America, presents significant growth opportunities as these regions experience demographic aging and healthcare infrastructure improvements. Investment in digital health technologies, including telemedicine platforms, remote monitoring solutions, and adherence support applications, can create competitive advantages by improving patient outcomes and treatment compliance. Strategic partnerships and collaborations between pharmaceutical companies, biotechnology firms, and digital health startups can accelerate innovation and market access. Additionally, investment in personalized medicine approaches, including biomarker research and genetic testing capabilities, can enable more targeted treatment selection and improved patient outcomes. Companies should also consider investments in manufacturing capabilities for complex biologics and long-acting formulations that offer competitive differentiation. Finally, strategic acquisitions of promising drug candidates or technology platforms in early development stages can provide access to innovative approaches while mitigating development risks.

Osteoporosis Treatment Market Conclusion - Summary and key takeaways

The Osteoporosis Treatment Market represents a dynamic and essential segment of the pharmaceutical industry, characterized by steady growth, ongoing innovation, and significant unmet medical needs. With a projected market size of $25.24 billion by 2033 and a CAGR of 4.54%, the market demonstrates robust fundamentals driven by demographic trends, increasing disease awareness, and continuous therapeutic advancements. Key takeaways include the market's resilience despite challenges such as treatment costs and potential side effects, the growing importance of emerging markets in driving future growth, and the transformative potential of novel treatment approaches particularly in the anabolic drug class. The competitive landscape remains active with established players investing heavily in R&D while facing challenges from generic competition and the need for continuous innovation. Distribution channels are evolving with online pharmacies gaining prominence, and treatment paradigms are shifting toward more personalized approaches based on individual patient characteristics. The market's future will likely be shaped by the successful integration of digital health technologies, the development of next-generation therapies with improved efficacy and safety profiles, and the expansion of treatment access in underserved regions. Overall, the Osteoporosis Treatment Market presents substantial opportunities for companies that can effectively navigate its complexities while addressing the growing global burden of osteoporosis through innovative and accessible treatment solutions.

Research Methodology - How this research was conducted

The research methodology employed for this Osteoporosis Treatment Market analysis combines multiple approaches to ensure comprehensive and reliable insights. The process began with extensive secondary research, utilizing reputable industry databases, scientific publications, company reports, and regulatory documents to establish a foundational understanding of market dynamics, historical trends, and competitive landscape. Primary research complemented this through interviews with key opinion leaders, including physicians specializing in osteoporosis treatment, pharmaceutical industry executives, and market analysts, providing expert perspectives on current market conditions and future trajectories. Data triangulation techniques were applied to validate findings across multiple sources, enhancing the reliability of market size estimates and growth projections. The research incorporated both bottom-up and top-down approaches to market sizing, analyzing individual segment contributions and aggregating them to derive total market values. Regional analysis involved examining country-specific factors including healthcare policies, demographic trends, and economic indicators to provide nuanced geographic insights. The methodology also included competitive analysis frameworks to assess market positioning and strategic initiatives of key players. Throughout the research process, emphasis was placed on identifying credible data sources and applying rigorous analytical frameworks to ensure the accuracy and relevance of findings presented in this report.

Research Scope - Coverage and limitations

The research scope for this Osteoporosis Treatment Market analysis encompasses a comprehensive examination of the global market, covering key segments including drug classes (bisphosphonates, selective estrogen receptor modulators, calcitonin, PTH-related anabolic agents), distribution channels (hospital pharmacies, retail pharmacies, online pharmacies), routes of administration (oral, injectable), and geographic regions. The analysis includes market sizing for the base year of 2023, with projections through 2033, focusing on revenue generation across different segments and regions. The scope incorporates examination of market drivers, restraints, challenges, and opportunities, along with competitive landscape analysis of major industry players. However, certain limitations exist within this research scope. The analysis primarily focuses on pharmaceutical interventions and does not extensively cover non-pharmaceutical approaches such as lifestyle modifications, nutritional supplementation, or physical therapy, though these may be mentioned in context. Market data for certain emerging regions may have limitations due to availability of reliable statistics and reporting inconsistencies. The research also acknowledges potential impacts from unforeseen global events, regulatory changes, or technological breakthroughs that could significantly alter market trajectories beyond the forecast period. Additionally, while the analysis provides comprehensive insights into market dynamics, it does not include detailed individual country-level regulations or reimbursement policies that may significantly impact market access in specific regions.

Key Companies and Recent Developments in the Osteoporosis Treatment Market - Introduction to top companies and their recent announcements, product launches, partnerships, and strategic developments

The Osteoporosis Treatment Market features several key companies driving innovation and market growth through strategic initiatives and product developments. Amgen Inc. has recently announced advancements in its anabolic therapy portfolio, with new clinical trial data demonstrating improved efficacy in specific patient subpopulations, while also expanding its manufacturing capabilities to meet growing global demand. Novartis AG has launched a next-generation bisphosphonate with improved dosing convenience and has entered into strategic partnerships with digital health companies to develop integrated patient monitoring solutions. Eli Lilly and Company has made headlines with the FDA approval of its novel anabolic agent, representing a significant advancement in bone formation stimulation technology, and has announced plans for expanded clinical trials in combination therapy approaches. Pfizer Inc. has focused on portfolio optimization through the acquisition of a biotechnology firm specializing in bone metabolism research, gaining access to promising drug candidates in early development stages. Daiichi Sankyo Company, Limited has strengthened its presence in the Asian market through the launch of region-specific formulations and has announced collaborations with local research institutions to develop treatments tailored to Asian patient populations. Teva Pharmaceuticals Inc. has expanded its generic portfolio with the introduction of cost-effective biosimilar versions of established osteoporosis treatments, targeting price-sensitive markets. Additionally, several companies have announced strategic partnerships between pharmaceutical manufacturers and digital health companies to develop comprehensive care platforms that combine medication with remote monitoring and patient support services, representing a significant trend toward integrated treatment approaches in the osteoporosis market.