Bottled Water Market Overview - Definition, scope, and significance

The bottled water market encompasses the commercial production, distribution, and sale of packaged drinking water in various formats, including plastic bottles, glass containers, and other packaging materials. This market serves both individual consumers and institutional clients, providing convenient access to purified, mineral, or spring water. The significance of the bottled water industry extends beyond simple hydration, as it represents a critical component of the global beverage sector, addressing consumer demands for safe, portable, and accessible drinking water across diverse geographical and socioeconomic contexts.

Bottled Water Market Drivers, Restraints, Challenges, and Opportunities - Key growth factors and obstacles

The bottled water market is driven by increasing health consciousness, rising disposable incomes, and growing urbanization, which create demand for convenient hydration solutions. Changing consumer preferences toward healthier beverage options and concerns about tap water quality further propel market growth. However, the industry faces significant restraints, including environmental concerns about plastic waste, stringent regulations, and the high cost of sustainable packaging alternatives. Challenges include managing supply chain logistics, addressing water scarcity issues, and navigating complex regulatory environments. Opportunities exist in developing innovative packaging solutions, expanding into emerging markets, and creating premium and functional water products that cater to evolving consumer preferences.

Bottled Water Market Growth Trends - Current and emerging trends shaping the market

Current growth trends in the bottled water market include a significant shift toward premium and functional water products, with consumers increasingly seeking enhanced hydration options with added minerals, vitamins, or unique flavor profiles. The market is witnessing a growing emphasis on sustainable packaging, with manufacturers investing in recyclable and biodegradable materials to address environmental concerns. Digital transformation is also reshaping the industry, with e-commerce platforms and direct-to-consumer models gaining traction. Additionally, there is a rising trend of personalized water products, where brands are offering customized packaging and specialized formulations to target specific consumer segments, particularly health-conscious millennials and Gen Z consumers.

COVID-19 Impact on the Bottled Water Market - Pandemic effects and recovery trajectory

The COVID-19 pandemic had a complex impact on the bottled water market, initially causing disruptions in supply chains and manufacturing processes due to lockdowns and transportation restrictions. However, the market demonstrated resilience, with increased consumer focus on health and hygiene driving demand for packaged water products. Panic buying and stockpiling behaviors during early pandemic stages led to temporary supply shortages. As economies recover, the market is experiencing a rebound, with manufacturers adapting to new consumer preferences and implementing enhanced safety protocols. The pandemic has accelerated trends toward e-commerce and contactless delivery, potentially reshaping long-term distribution strategies in the bottled water industry.

Bottled Water Market Competitive Landscape - Major competitors and market consolidation

The bottled water market features a highly competitive landscape with both multinational corporations and regional players competing for market share. Major competitors include global giants like Nestlé, PepsiCo, and The Coca-Cola Company, which leverage extensive distribution networks and strong brand recognition. These companies are increasingly focusing on product diversification, sustainable packaging, and strategic acquisitions to maintain their competitive edge. Market consolidation is evident through mergers and acquisitions, with larger players acquiring smaller, innovative brands to expand their product portfolios and enter niche market segments. The competitive dynamics are characterized by intense price competition, brand differentiation strategies, and continuous innovation in product offerings and packaging solutions.

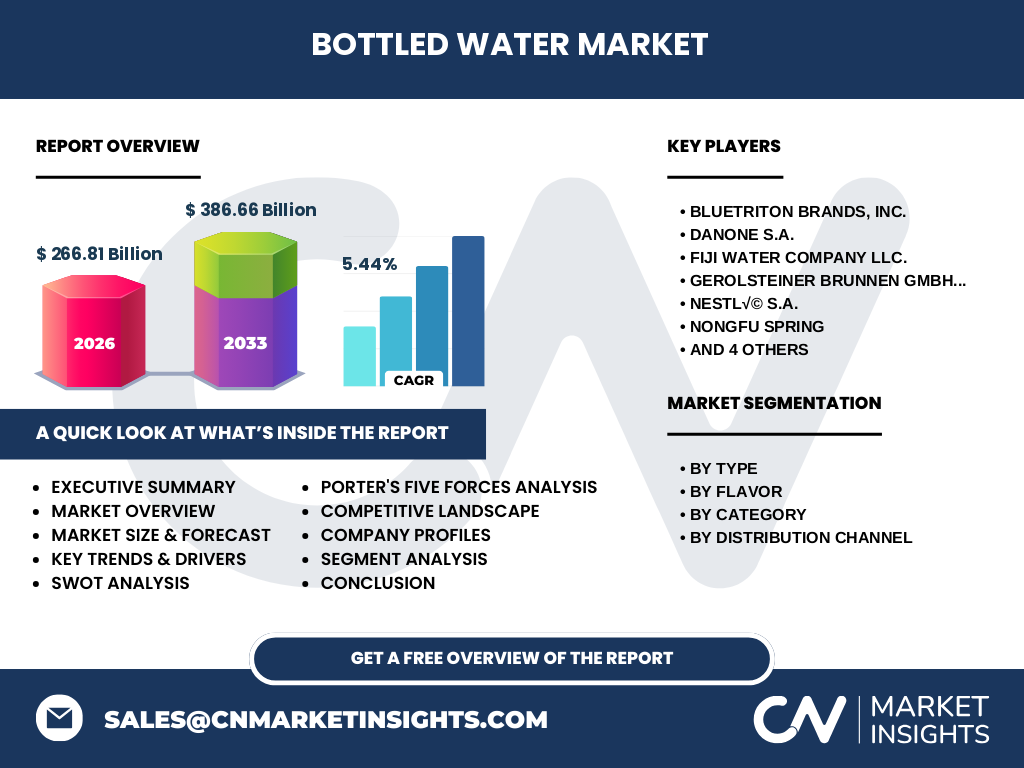

Executive Summary - High-level overview and key findings about Bottled Water Market

The bottled water market represents a dynamic and rapidly evolving industry, projected to grow from $266.81 billion in 2026 to $386.66 billion by 2033, with a compound annual growth rate of 5.44%. This growth is driven by increasing health consciousness, rising disposable incomes, and changing consumer preferences toward convenient hydration solutions. The market is characterized by diverse product segments, including sparkling and still water, flavored and plain options, functional and conventional categories, and multiple distribution channels. Key trends include a shift toward sustainable packaging, premium product development, and digital transformation in distribution. The industry faces challenges related to environmental concerns and regulatory pressures but continues to innovate and adapt to changing market dynamics.

Bottled Water Market Forecast - Projections for 2025-2032 period

The bottled water market is poised for substantial growth between 2025 and 2032, with projections indicating a robust expansion from its current valuation. The market is expected to witness a compound annual growth rate of 5.44%, reaching an estimated value of $386.66 billion by 2033. This growth trajectory is underpinned by increasing global population, rising health awareness, and expanding middle-class demographics in emerging economies. The forecast period will likely see continued innovation in product offerings, with a particular emphasis on functional and premium water segments. Additionally, technological advancements in packaging and distribution are expected to play a crucial role in shaping the market's future landscape.

Bottled Water Market Size and Share by Segmentation - Breakdown by {segmentData}

The bottled water market is segmented across multiple dimensions, each contributing to the overall market dynamics. By type, the market is divided into sparkling and still water, with still water currently dominating the segment due to its widespread consumer preference. Flavor segmentation reveals a growing trend toward flavored water, particularly among younger consumers seeking variety in their hydration options. The category segmentation distinguishes between functional and conventional water, with functional water gaining traction due to increasing health consciousness. Distribution channels are segmented into supermarkets and hypermarkets, convenience stores, and online retail, with traditional retail channels currently holding the largest share but online retail showing the fastest growth.

Global Bottled Water Market Size and Share by Region - Geographic distribution

The global bottled water market exhibits significant regional variations in terms of size and growth potential. North America and Europe represent mature markets with high per capita consumption rates, driven by strong health awareness and disposable incomes. The Asia-Pacific region is emerging as a key growth driver, fueled by rapid urbanization, increasing middle-class population, and improving living standards in countries like China and India. Latin America and the Middle East & Africa regions are also showing promising growth, albeit from a lower base, due to improving economic conditions and rising health consciousness. Regional market dynamics are influenced by factors such as local water quality, cultural preferences, and regulatory environments.

Regional Analysis of the Bottled Water Market - Detailed regional market performance

Regional analysis of the bottled water market reveals distinct patterns of growth and consumer behavior across different geographies. In North America, the market is characterized by high consumption rates and a strong preference for premium and functional water products. Europe shows a similar trend, with an added emphasis on sustainability and eco-friendly packaging solutions. The Asia-Pacific region, particularly countries like China and India, is experiencing rapid market expansion due to improving economic conditions and increasing health awareness. Latin American markets are growing steadily, driven by rising middle-class populations and changing consumer preferences. The Middle East & Africa region presents unique challenges and opportunities, with water scarcity issues influencing market dynamics and creating demand for premium bottled water products.

Leading Company Profiles in the Bottled Water Market - Industry players and strategies

The bottled water market is dominated by several key players, each employing distinct strategies to maintain and expand their market presence. Bluetriton Brands, Inc. has established itself as a leader in sustainable packaging solutions, focusing on eco-friendly materials and innovative product designs. Danone S.A. leverages its global presence and diverse product portfolio to cater to various consumer segments across different regions. Fiji Water Company LLC. has successfully positioned itself as a premium brand, emphasizing the unique source and quality of its water. Nestlé S.A., with its extensive brand portfolio, continues to dominate through strategic acquisitions and product innovations. PepsiCo, Inc. and The Coca-Cola Company, leveraging their vast distribution networks and brand recognition, are expanding their water product lines to compete more aggressively in this growing market.

Porter's Five Forces Analysis of the Bottled Water Market - Competitive forces assessment

Porter's Five Forces analysis reveals a complex competitive landscape in the bottled water market. The threat of new entrants is moderate, as established brands have strong market positions and significant economies of scale, but niche markets and innovative products continue to attract new players. Bargaining power of suppliers is relatively low due to the commoditized nature of water and the availability of multiple sourcing options. Buyers, particularly large retailers, have moderate to high bargaining power due to their ability to influence pricing and shelf space allocation. The threat of substitutes is significant, with tap water, other beverages, and emerging alternatives like flavored water posing competition. Competitive rivalry is intense, with major players constantly innovating and engaging in price competition to maintain market share.

SWOT Analysis of the Bottled Water Market - Strengths, weaknesses, opportunities, threats

The bottled water market's strengths include its essential nature as a product, strong brand recognition of major players, and established distribution networks. The industry benefits from growing health consciousness and increasing global demand for safe drinking water. However, weaknesses such as environmental concerns over plastic waste, high transportation costs, and vulnerability to regulatory changes pose challenges. Opportunities exist in developing sustainable packaging solutions, expanding into emerging markets, and creating innovative functional water products. Threats include potential regulatory restrictions on single-use plastics, competition from alternative beverages, and the growing popularity of home water filtration systems, which could reduce demand for bottled water in some markets.

Bottled Water Market Value Chain Analysis - Industry structure and value flow

The value chain in the bottled water market encompasses several key stages, each contributing to the final product's value and cost. The process begins with water sourcing, where companies secure rights to natural springs, municipal water supplies, or develop proprietary filtration technologies. This is followed by water treatment and purification, where raw water is processed to meet quality standards. Packaging represents a significant value addition, with companies investing in innovative and sustainable packaging solutions. Distribution involves complex logistics to ensure product availability across various retail channels. Marketing and branding play crucial roles in differentiating products and building consumer loyalty. Finally, retail and direct-to-consumer sales complete the value chain, with each stage offering opportunities for value addition and cost optimization.

Key Investment Insights in the Bottled Water Market - Strategic investment recommendations

Investment opportunities in the bottled water market are diverse and promising, driven by the sector's projected growth and evolving consumer preferences. Strategic investments in sustainable packaging technologies and materials present significant potential, as environmental concerns continue to shape consumer choices and regulatory landscapes. The functional water segment offers attractive investment prospects, with growing demand for products offering additional health benefits beyond basic hydration. Emerging markets in Asia-Pacific and Africa represent untapped potential for expansion, particularly in regions with improving economic conditions and increasing health awareness. Additionally, investments in digital transformation, including e-commerce platforms and smart packaging technologies, could provide competitive advantages in an increasingly connected consumer landscape.

Bottled Water Market Conclusion - Summary and key takeaways

The bottled water market presents a compelling growth story, characterized by robust expansion, evolving consumer preferences, and dynamic competitive landscapes. With a projected growth from $266.81 billion in 2026 to $386.66 billion by 2033, the industry demonstrates strong resilience and adaptability. Key trends such as sustainable packaging, premium product development, and digital transformation are reshaping the market, while challenges like environmental concerns and regulatory pressures continue to influence strategic decisions. The market's future success will depend on companies' ability to innovate, address sustainability concerns, and effectively navigate diverse regional markets and consumer preferences.

Research Methodology - How this research was conducted

This comprehensive market research was conducted using a rigorous methodology combining primary and secondary data sources. Primary research involved interviews with industry experts, manufacturers, and distributors to gather firsthand insights into market dynamics and trends. Secondary research encompassed analysis of company reports, industry publications, and government statistics to validate and supplement primary findings. The research employed both top-down and bottom-up approaches to estimate market size and growth projections. Data triangulation techniques were used to ensure accuracy and reliability of the findings. The study also incorporated SWOT and Porter's Five Forces analyses to provide a holistic view of the market landscape.

Research Scope - Coverage and limitations

This research report covers the global bottled water market, providing comprehensive analysis across various segments including type, flavor, category, and distribution channels. The scope encompasses major geographic regions, with detailed insights into market dynamics, competitive landscapes, and future projections. The study focuses on the period from 2025 to 2033, with particular emphasis on the forecast period. While the research aims to provide a thorough analysis of the market, it is important to note that certain limitations exist, such as the availability of specific regional data and the rapidly changing nature of consumer preferences and regulatory environments. The report strives to offer the most current and accurate information possible within these constraints.

Key Companies and Recent Developments in the Bottled Water Market - Introduction to top companies and their recent announcements, product launches, partnerships, and strategic developments

The bottled water market's key players have been actively pursuing strategic initiatives to strengthen their market positions. Bluetriton Brands, Inc. has recently announced significant investments in sustainable packaging technologies, aiming to reduce plastic usage in its products. Danone S.A. has expanded its portfolio through strategic acquisitions, focusing on premium and functional water segments. Fiji Water Company LLC. has launched a new line of flavored water products, targeting younger consumers. Nestlé S.A. has announced partnerships with environmental organizations to improve water stewardship in its sourcing regions. PepsiCo, Inc. has introduced smart packaging technologies to enhance consumer engagement and traceability. The Coca-Cola Company has expanded its vitamin water range, emphasizing health benefits. These developments reflect the industry's focus on innovation, sustainability, and meeting evolving consumer demands.