What is the Asia Pacific Digital Language Learning Market Overview – Definition, scope, and significance?

The Asia Pacific Digital Language Learning Market comprises software, platforms, and services that enable learners to acquire new languages through digital channels such as mobile apps, web portals, and cloud‑based solutions. The market’s scope spans academic institutions, corporate training programs, and individual consumers across the region. Its significance lies in addressing the growing demand for multilingual proficiency driven by cross‑border trade, tourism, and the digital economy, while also supporting inclusive education and lifelong learning initiatives.

What are the main drivers, restraints, challenges, and opportunities in the Asia Pacific Digital Language Learning Market?

Key drivers include rapid internet penetration, rising disposable income, and the need for English and other foreign language skills in the global workforce. Government support for digital education and the proliferation of smartphones further stimulate growth. Restraints stem from uneven broadband quality in remote areas and concerns over data privacy. Challenges involve intense competition and the need for localized content. Opportunities arise from AI‑powered adaptive learning, hybrid classroom‑digital models, and expansion into underserved rural markets.

What growth trends are currently shaping the Asia Pacific Digital Language Learning Market?

Current trends feature the integration of artificial intelligence for personalized lesson paths, gamification to boost engagement, and micro‑learning modules that fit busy schedules. Cloud deployment is accelerating, enabling rapid scaling and cross‑device synchronization. Additionally, corporate B2B subscriptions are expanding as enterprises prioritize upskilling, while B2C platforms are diversifying language portfolios beyond English to include Mandarin, German, and Spanish.

How has COVID‑19 impacted the Asia Pacific Digital Language Learning Market and what is the recovery trajectory?

The pandemic forced school closures and remote work, dramatically increasing demand for online language solutions. User adoption surged, prompting many providers to upgrade infrastructure and introduce free trial periods. As economies reopen, the market retains elevated usage levels, with hybrid learning models becoming the norm. Recovery is steady, supported by continued institutional investment in digital curricula and sustained consumer interest in language acquisition for travel and career advancement.

Who are the major competitors and what is the level of market consolidation in the Asia Pacific Digital Language Learning Market?

The competitive landscape features established global players such as Rosetta Stone, Pearson PLC, and Babbel, alongside fast‑growing regional platforms like Busuu, Lingoda, and Preply. While the market remains fragmented, recent strategic partnerships and acquisitions indicate a gradual consolidation trend, as larger firms seek to broaden language libraries and strengthen AI capabilities. This consolidation aims to create integrated ecosystems that serve both B2B and B2C segments.

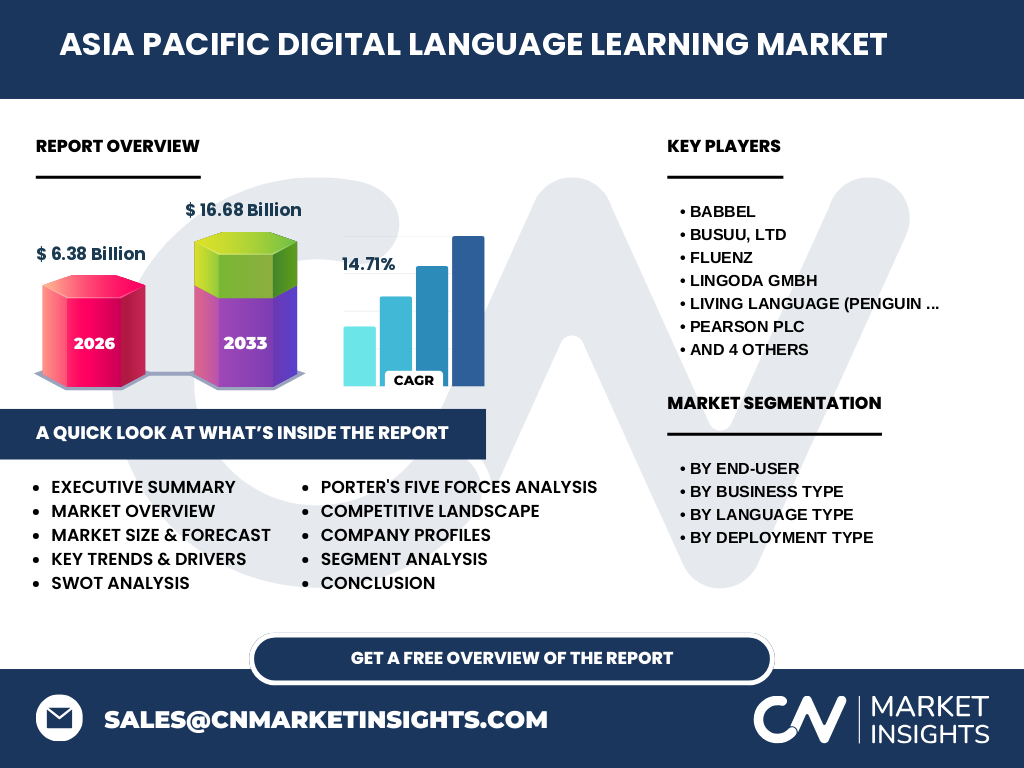

What are the key findings presented in the Executive Summary of the Asia Pacific Digital Language Learning Market?

The market is valued at US 6.38 billion in 2026 and is projected to reach US 16.68 billion by 2033, reflecting a robust 14.71% CAGR. Growth is propelled by digital transformation in education, corporate language upskilling, and rising multilingual demand. Cloud deployment leads the technology mix, while English remains the dominant language, complemented by growing interest in Mandarin, German, and Spanish. Competitive dynamics favor firms that combine AI personalization with localized content.

What forecasts are provided for the Asia Pacific Digital Language Learning Market for 2025‑2032?

Based on the stated CAGR of 14.71%, the market is expected to continue expanding at a double‑digit pace through 2032. The upward trajectory will be supported by expanding cloud infrastructure, increased corporate B2B contracts, and broader penetration of digital learning in secondary and higher education. Emerging economies within the region will contribute disproportionately to volume growth as connectivity improves.

How is the Asia Pacific Digital Language Learning Market sized and shared by segmentation?

Segmentation reveals four primary dimensions. By end‑user, the market splits between Academic institutions and Non‑Academic users such as corporate learners and private individuals. By business type, Business‑to‑Business (B2B) solutions target enterprises and schools, while Business‑to‑Consumer (B2C) platforms serve individual learners. Language type segmentation includes English, German, Spanish, and Mandarin. Deployment is divided into On‑Premise solutions for large organizations and Cloud offerings for scalable, subscription‑based access.

What is the global Asia Pacific Digital Language Learning Market size and share by region?

The Asia Pacific region accounts for the majority of the global digital language learning market, with a 2026 valuation of US 6.38 billion. While precise regional breakdowns are not disclosed, the forecast to US 16.68 billion by 2033 underscores the region’s dominant share relative to other continents, driven by population size, economic growth, and digital adoption rates.

What does the regional analysis reveal about performance across the Asia Pacific Digital Language Learning Market?

East Asian economies exhibit strong demand for English and Mandarin learning, supported by government digital education initiatives. Southeast Asian nations show rapid B2C growth due to youthful populations and mobile‑first internet usage. South Asian markets are emerging, with increasing corporate B2B contracts as multinational firms expand operations. Overall, each sub‑region contributes uniquely: infrastructure intensity in East Asia, consumer enthusiasm in Southeast Asia, and cost‑sensitive enterprise adoption in South Asia.

Which leading companies operate in the Asia Pacific Digital Language Learning Market and what are their strategies?

Key players include Babbel, Busuu, Fluenz, Lingoda, Living Language (Penguin Random House), Pearson PLC, Preply, Rosetta Stone, Verbling, and Yabla. Strategies focus on AI‑driven personalization, expansion of language catalogs, strategic partnerships with educational institutions, and hybrid pricing models that combine subscription and pay‑per‑lesson options. Several firms are investing in cloud migration and localized content creation to capture regional language preferences.

How does Porter’s Five Forces framework apply to the Asia Pacific Digital Language Learning Market?

Bargaining power of buyers is high, as learners can switch between numerous apps. Supplier power is moderate; content creators and technology providers influence pricing but face competition. Threat of new entrants is moderate‑high, given low entry barriers for app development, though brand trust and AI capabilities pose hurdles. Threat of substitutes includes traditional classroom instruction and free online resources. Industry rivalry is intense, with frequent product innovation and price competition driving differentiation.

What are the SWOT insights for the Asia Pacific Digital Language Learning Market?

Strengths: Rapid digital adoption, diverse language portfolio, and scalable cloud solutions.

Weaknesses: Dependence on internet quality and limited offline accessibility in remote areas.

Opportunities: AI personalization, corporate upskilling contracts, and expansion into underserved rural markets.

Threats: Data privacy regulations, intense price competition, and potential market saturation in premium segments.

What does the value chain of the Asia Pacific Digital Language Learning Market look like?

The value chain begins with content creation (linguistic experts, curriculum designers), followed by technology development (software engineering, AI algorithms). Next is platform integration (cloud hosting, mobile app deployment). Distribution occurs through digital marketplaces and direct B2B sales. End‑users receive learning experiences supported by customer service and continuous content updates, completing the cycle.

What key investment insights can be drawn for the Asia Pacific Digital Language Learning Market?

Investors should target companies that combine strong AI capabilities with localized language libraries, as these are positioned to capture both B2B and B2C growth. Partnerships with telecom providers can unlock rural penetration, while acquisitions of niche language specialists can enhance content depth. Emphasis on cloud scalability and data analytics will drive higher lifetime value per subscriber, making such firms attractive for long‑term capital infusion.

What conclusions can be drawn about the Asia Pacific Digital Language Learning Market?

The market demonstrates solid momentum, underpinned by a 14.71% CAGR and a forecasted rise to US 16.68 billion by 2033. Digital infrastructure, AI‑enhanced personalization, and corporate language demand are the primary engines of growth. While competition is fierce, firms that invest in localized content, cloud delivery, and strategic B2B alliances are likely to secure sustainable market share.

How was the research methodology designed for this market study?

The study employed a mixed‑method approach: secondary data collection from industry reports, company filings, and reputable databases; primary insights gathered via expert interviews with educators, corporate training managers, and technology providers; and quantitative modeling using the provided market size, forecast, and CAGR figures. Trend analysis and competitive benchmarking were applied to validate projections.

What is the scope of this research and its coverage limitations?

The research covers the Asia Pacific Digital Language Learning Market from 2026 to 2033, focusing on end‑user, business type, language, and deployment segments. Geographic scope includes all Asia Pacific economies. Limitations arise from the reliance on publicly available data and the exclusion of proprietary financial details beyond the supplied market size and growth rates.

Which key companies and recent developments define the Asia Pacific Digital Language Learning Market?

Prominent players such as Rosetta Stone, Pearson PLC, and Babbel have launched AI‑driven adaptive learning modules in 2023‑2024. Busuu announced a partnership with several Southeast Asian universities to embed its platform into curricula. Lingoda expanded its live‑class offering in India, while Preply introduced a subscription tier tailored for corporate clients. These developments highlight a shift toward blended learning, AI personalization, and deeper regional collaborations.