1. Europe Digital banking platform Market Overview – Definition, scope, and significance?

The Europe Digital Banking Platform market comprises software solutions and services that enable banks—both corporate and retail—to deliver end‑to‑end digital experiences to customers and enterprise clients. These platforms integrate core banking, payments, lending, compliance, analytics, and omnichannel interaction layers, and can be deployed either on cloud infrastructure or on‑premise data centres. The scope of the market extends to the full lifecycle of digital banking services, from onboarding and identity verification to real‑time transaction processing and advanced data‑driven insights. Its significance lies in transforming traditional banking models into agile, customer‑centric ecosystems, thereby driving operational efficiency, reducing cost‑to‑serve, and meeting the heightened expectations of a digitally savvy European populace.

2. Europe Digital banking platform Market Drivers, Restraints, Challenges, and Opportunities – Key growth factors and obstacles?

Key drivers include the rapid adoption of mobile wallets, open‑banking regulations that mandate API‑based data sharing, and the strategic push by incumbents to retain market share against fintech disruptors. The demand for cloud‑native solutions, accelerated by the need for scalability and faster time‑to‑market, further propels growth. Restraints involve stringent data‑privacy laws such as GDPR, which increase compliance costs and slow integration efforts. Challenges encompass legacy system migration complexities and a shortage of skilled talent in emerging technologies like AI and blockchain. Opportunities arise from the expansion of embedded finance, the rise of digital‑only banks, and the potential to monetize data through advanced analytics, positioning the market for sustained expansion.

3. Europe Digital banking platform Market Growth Trends – Current and emerging trends shaping the market?

Current trends feature a shift toward cloud deployments, with banks leveraging public‑cloud partnerships to enhance resilience and innovation speed. Open APIs are becoming standard, fostering ecosystem collaboration with fintechs and third‑party service providers. AI‑driven personalization, predictive credit scoring, and conversational banking via chatbots are emerging capabilities that differentiate platforms. Additionally, the rise of “banking‑as‑a‑service” models enables non‑bank entities to embed financial functionalities, widening the addressable market. Sustainable finance is also influencing platform roadmaps, as regulators require greener lending processes embedded within digital solutions.

4. COVID‑19 Impact on the Europe Digital banking platform Market – Pandemic effects and recovery trajectory?

The COVID‑19 pandemic acted as a catalyst for digital adoption across Europe. Lockdown measures forced customers to rely on remote banking channels, prompting institutions to accelerate platform rollouts, especially cloud‑based solutions that support rapid scaling. While the initial shock caused short‑term project delays, the subsequent recovery has been robust, with banks prioritising digital transformation budgets. The market’s post‑pandemic trajectory shows a steady upward curve, underpinned by heightened consumer confidence in digital channels and ongoing regulatory encouragement for digital resilience.

5. Europe Digital banking platform Market Competitive Landscape – Major competitors and market consolidation?

The competitive arena is populated by a mix of global technology giants and specialised European vendors. Leading players include Oracle Corporation, SAP SE, Temenos Headquarters SA, and Tata Consultancy Services Limited (TCS), each offering comprehensive suites that span core banking to advanced analytics. Niche innovators such as Appway AG, CREALOGIX Holding AG, and EdgeVerve Systems Limited differentiate through workflow automation and AI‑enabled decision engines. Recent years have witnessed strategic mergers, joint ventures, and acquisition activity aimed at consolidating capabilities—e.g., larger system integrators acquiring fintech‑focused platform builders—to deliver end‑to‑end value propositions.

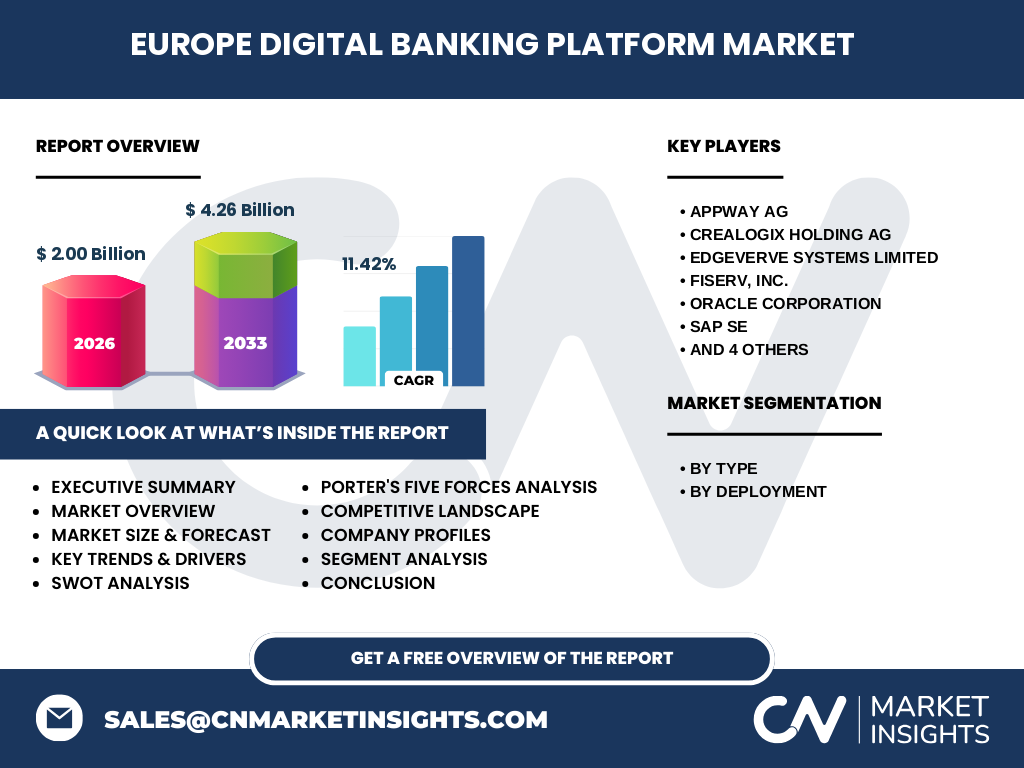

6. Executive Summary – High‑level overview and key findings about Europe Digital banking platform Market?

The Europe Digital Banking Platform market is valued at €2.00 billion in 2026 and is projected to reach €4.26 billion by 2033, reflecting a robust CAGR of 11.42 %. Growth is driven by regulatory momentum, cloud adoption, and increasing consumer demand for seamless digital experiences. Corporate and retail banking segments both benefit from platform convergence, while deployment models are split between cloud and on‑premise, with cloud gaining share. The competitive landscape is characterised by strong incumbents and emerging specialists, leading to a dynamic environment of collaboration and consolidation. Opportunities abound in open banking, embedded finance, and AI‑enhanced services, positioning the market for continued expansion.

7. Europe Digital banking platform Market Forecast – Projections for 2025‑2032 period?

Building on the 2026 base of €2.00 billion and the 11.42 % CAGR, the market is expected to sustain double‑digit growth through 2032. The forecast anticipates a gradual acceleration as cloud migration matures and open‑banking initiatives unlock new revenue streams. By 2032, the market is projected to exceed €4.0 billion, reinforcing Europe’s status as a leading hub for advanced digital banking solutions. The growth trajectory is underpinned by continued investment in AI, data analytics, and modular platform architectures that enable rapid feature rollout.

8. Europe Digital banking platform Market Size and Share by Segmentation – Breakdown by {segmentData}?

Segmentation by Type divides the market into Corporate Banking and Retail Banking solutions. Both segments are integral to the overall market, with corporate platforms often requiring complex cash‑management and trade‑finance capabilities, while retail platforms focus on high‑volume consumer transactions and personalized experiences. Deployment segmentation distinguishes Cloud and On‑Premise installations. Cloud deployments are gaining traction due to lower upfront CAPEX and scalability, whereas On‑Premise remains relevant for institutions with strict data‑sovereignty requirements. The exact share percentages are not disclosed, but the dual‑segmentation framework reflects the market’s diversity of use cases.

9. Global Europe Digital banking platform Market Size and Share by Region – Geographic distribution?

Within the broader global context, Europe accounts for a significant portion of digital banking platform spend, driven by mature banking ecosystems and regulatory frameworks that promote innovation. While specific regional share figures are not provided, the market’s €2.00 billion valuation in 2026 signals Europe’s leading role compared with other continents, where adoption rates are generally lower due to differing regulatory maturity and digital penetration levels.

10. Regional Analysis of the Europe Digital banking platform Market – Detailed regional market performance?

Regional performance varies across the European Economic Area. Western Europe, encompassing finance hubs such as London, Frankfurt, and Paris, demonstrates the highest adoption rates, spurred by extensive fintech ecosystems and early open‑banking legislation. Northern Europe, led by the Nordics, shows strong cloud migration due to progressive IT policies. Southern and Eastern European markets are emerging, with accelerated investments in digital platforms to modernise legacy infrastructures and meet EU‑wide compliance standards. Overall, the region exhibits a cohesive upward trend with localized nuances in deployment preferences.

11. Leading Company Profiles in the Europe Digital banking platform Market – Industry players and strategies?

Key players include:

• Appway AG – Focuses on digital onboarding and workflow automation, leveraging AI to streamline compliance.

• CREALOGIX Holding AG – Provides cloud‑native core banking suites with a strong emphasis on modularity.

• EdgeVerve Systems Limited – Offers AI‑driven analytics and decision platforms for enterprise banking.

• Fiserv, Inc. – Supplies end‑to‑end payment and digital banking solutions, emphasizing ecosystem integration.

• Oracle Corporation – Delivers robust cloud infrastructure coupled with comprehensive banking applications.

• SAP SE – Leverages its ERP heritage to embed financial processes within broader enterprise suites.

• Sopra Steria – Combines consulting expertise with custom platform development for regulated markets.

• Tata Consultancy Services Limited (TCS) – Utilises global delivery models to implement large‑scale digital transformations.

• Temenos Headquarters SA – Known for its scalable core banking platform, Temenos continuously expands its digital front‑end capabilities.

• Worldline SA – Specialises in payment processing and embedded finance services, increasingly integrating with banking platforms.

These companies pursue strategies such as strategic alliances with fintechs, accelerated cloud migration roadmaps, and investment in AI to maintain competitive advantage.

12. Porter's Five Forces Analysis of the Europe Digital banking platform Market – Competitive forces assessment?

Threat of New Entrants: Moderate. High capital requirements and regulatory barriers limit newcomers, but fintech SaaS providers can enter niche segments.

Bargaining Power of Suppliers: Low to moderate. Cloud service providers hold influence, yet banks can select multiple vendors to mitigate risk.

Bargaining Power of Buyers: High. Banks demand tailored solutions, cost efficiency, and compliance, driving vendors to offer flexible licensing and services.

Threat of Substitutes: Low. Alternative channels such as direct fintech apps exist, but they often rely on the same underlying digital banking platforms.

Industry Rivalry: Intense. Established vendors compete on functionality, integration speed, and partnership ecosystems, prompting continuous innovation.

13. SWOT Analysis of the Europe Digital banking platform Market – Strengths, weaknesses, opportunities, threats?

Strengths: Mature regulatory environment fostering innovation; strong fintech talent pool; high digital penetration among consumers.

Weaknesses: Fragmented legacy infrastructures; compliance cost pressures; skill gaps in emerging technologies.

Opportunities: Expansion of open‑banking APIs; growth of embedded finance; AI‑driven risk and personalization tools.

Threats: Cybersecurity risks; evolving data‑privacy regulations; competitive pressure from agile fintech disruptors.

14. Europe Digital banking platform Market Value Chain Analysis – Industry structure and value flow?

The value chain begins with core technology providers (cloud infrastructure, middleware) and moves through platform developers who build modular banking suites. System integrators then customise and implement solutions for banks, adding consulting, integration, and change‑management services. Post‑implementation, managed services, support, and continuous improvement – often delivered via SaaS – complete the chain. Adjacent services, such as data analytics and cybersecurity, are increasingly embedded, creating a more interconnected ecosystem.

15. Key Investment Insights in the Europe Digital banking platform Market – Strategic investment recommendations?

Investors should focus on companies that demonstrate strong cloud capabilities, open‑API ecosystems, and proven AI integration. Partnerships between traditional vendors and niche fintechs signal a readiness to capture emerging revenue streams such as embedded finance. Acquisitions targeting workflow automation and compliance automation technologies can yield synergistic benefits. Additionally, backing firms with a diversified portfolio across corporate and retail segments reduces exposure to sector‑specific downturns.

16. Europe Digital banking platform Market Conclusion – Summary and key takeaways?

The Europe Digital Banking Platform market is on a clear growth trajectory, doubling its value from €2.00 billion in 2026 to an estimated €4.26 billion by 2033, driven by an 11.42 % CAGR. Cloud adoption, regulatory impetus, and consumer demand for seamless digital experiences are the primary catalysts. While data‑privacy and legacy migration pose challenges, the sector offers considerable opportunities in AI, open banking, and embedded finance. Competitive dynamics favor vendors that combine technological depth with strategic partnerships, making the market attractive for both strategic and financial investors.

17. Research Methodology – How this research was conducted?

The study employed a mixed‑method approach, combining primary interviews with senior executives from leading banks, fintechs, and technology vendors, with secondary data extraction from industry reports, regulatory publications, and financial statements. Market sizing leveraged the provided base year figure of €2.00 billion and applied the disclosed CAGR of 11.42 % to generate forward‑looking estimates. Segmentation analysis was grounded in the defined Type (Corporate vs. Retail) and Deployment (Cloud vs. On‑Premise) categories. Competitive assessment incorporated revenue rankings, product portfolios, and recent M&A activity.

18. Research Scope – Coverage and limitations?

The scope encompasses the full European geographic region, covering both corporate and retail banking digital platform services across cloud and on‑premise deployments. It includes analysis of major vendors, market sizing, trend evaluation, and strategic insights. Limitations arise from the reliance on publicly available financial data and the absence of granular market‑share percentages for individual segments, which are not disclosed in the source material.

19. Key Companies and Recent Developments in the Europe Digital banking platform Market – Introduction to top companies and their recent announcements, product launches, partnerships, and strategic developments?

Recent activity highlights a vibrant innovation landscape: Temenos announced a next‑generation digital front‑end suite that integrates AI‑driven chat interfaces. Oracle expanded its Cloud Infrastructure footprint in Europe, offering dedicated compliance zones for banking workloads. TCS entered a strategic partnership with a leading European fintech to co‑develop an open‑API hub, accelerating sandbox testing for new services. Appway launched an enhanced digital onboarding platform that leverages biometric verification, reducing KYC processing time. Worldline revealed a new payment‑as‑a‑service offering that embeds directly into retail banking portals, supporting the embedded finance trend. These developments underscore the market’s momentum toward integrated, cloud‑first, and AI‑enabled solutions.