What is the UK Ceramic Adhesives Market Overview – definition, scope, and significance?

The UK Ceramic Adhesives Market comprises products formulated to bond ceramic substrates in construction, renovation, and specialty applications. It spans a range of adhesive chemistries—cement‑based, acrylic, epoxy, and cyanoacrylate—used across flooring, roofing, and wall‑covering projects. The market is significant because ceramics offer durability, fire resistance, and aesthetic appeal, while modern adhesives enable faster installation, reduced labor, and improved performance, driving demand in both residential and commercial sectors.

What are the key drivers, restraints, challenges, and opportunities shaping the UK Ceramic Adhesives Market?

Key drivers include rising construction activity, stricter building‑code requirements for fire‑rated materials, and growing consumer preference for sustainable, low‑maintenance finishes. Restraints stem from volatile raw‑material costs and heightened competition from alternative bonding systems. Challenges involve compliance with evolving environmental regulations and the need for skilled applicators. Opportunities arise from the development of high‑performance, low‑VOC adhesives, digital tooling for precise application, and expansion into retrofit and heritage‑building projects.

What growth trends are currently influencing the UK Ceramic Adhesives Market?

Current trends feature a shift toward bio‑based and water‑borne adhesive formulations that meet green‑building standards. Manufacturers are also integrating nanotechnology to enhance bond strength and thermal stability. The market is seeing increased adoption of prefabricated ceramic panels that require rapid‑cure adhesives, and a rising preference for epoxy systems in high‑traffic commercial flooring due to their chemical resistance.

How has COVID‑19 impacted the UK Ceramic Adhesives Market, and what is the recovery trajectory?

The pandemic caused temporary disruptions in supply chains and a slowdown in non‑essential construction, leading to a short‑term dip in adhesive consumption. However, stimulus measures for residential building and the acceleration of renovation projects have spurred a swift rebound. The market is now on a recovery path that aligns with broader construction growth, positioning it for continued expansion.

Who are the major competitors in the UK Ceramic Adhesives Market and what is the level of market consolidation?

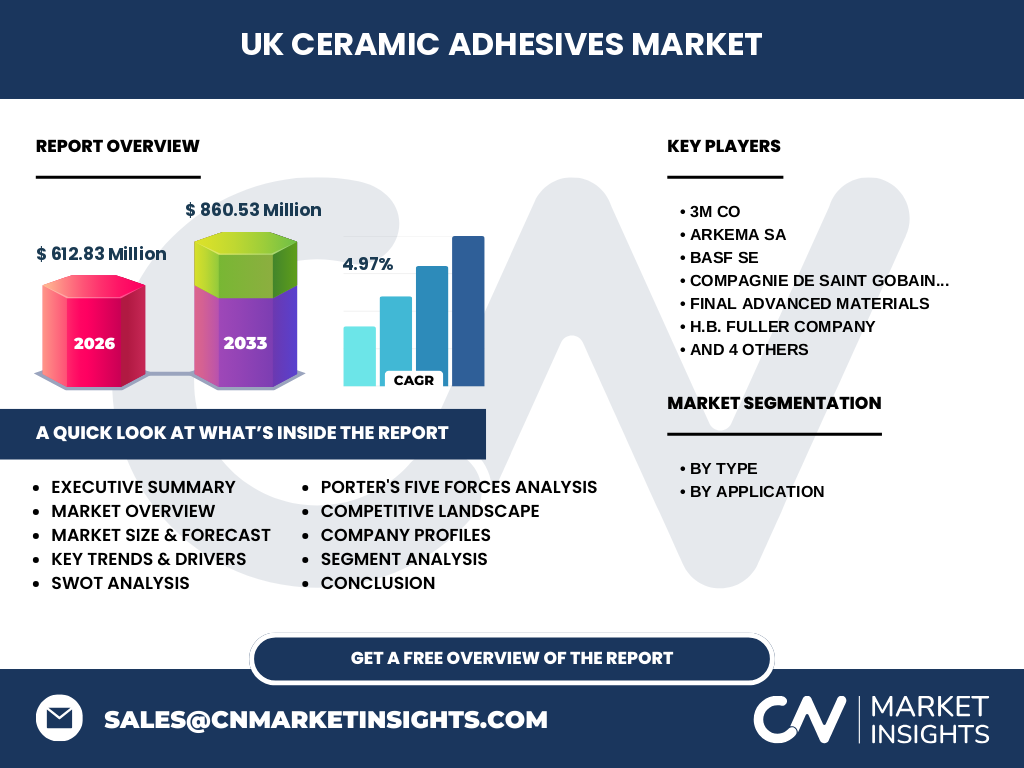

The competitive landscape is dominated by multinational chemical and building‑materials firms, including 3M Co, Arkema SA, BASF SE, Compagnie de Saint‑Gobain SA, Final Advanced Materials, H.B. Fuller Company, Henkel AG & Co KGaA, Kerakoll SpA, Mapei SpA, and Sika AG. While the market remains fragmented with many specialized players, recent strategic alliances and product‑line extensions indicate gradual consolidation aimed at broadening portfolio breadth and geographic reach.

What are the key findings presented in the executive summary of the UK Ceramic Adhesives Market?

The executive summary highlights a market size of £612.83 million in 2026, with a projected growth to £860.53 million by 2033, representing a CAGR of 4.97 %. Growth is driven by strong construction pipelines, regulatory emphasis on fire‑safe materials, and innovation in eco‑friendly adhesive chemistries. Competitive dynamics are shaped by a few global leaders expanding through new product launches and strategic partnerships.

What are the forecast expectations for the UK Ceramic Adhesives Market from 2025 to 2032?

Forecasts anticipate a steady upward trajectory, maintaining the 4.97 % compound annual growth rate through 2032. The market is expected to benefit from continued urbanization, increased spending on energy‑efficient building envelopes, and the rollout of smart‑home ceramic installations that require specialized bonding solutions.

How is the UK Ceramic Adhesives Market sized and shared by type and application segmentation?

Segmentation by type comprises cement‑based, acrylic, epoxy, and cyanoacrylate adhesives, each catering to distinct performance requirements. By application, the market is divided among flooring, roofing, and wall coverings. While exact share percentages are undisclosed, cement‑based adhesives traditionally dominate the flooring segment, whereas epoxy and acrylic formulations are gaining traction in roofing and wall‑covering projects due to their superior moisture resistance.

What is the global distribution of the UK Ceramic Adhesives Market size and share by region?

Regionally, the United Kingdom accounts for the primary share of the market, reflecting its mature construction industry and strict building standards. Internationally, the market draws influence from European trends, particularly in neighboring countries where similar regulatory frameworks drive demand for high‑performance ceramic bonding solutions.

What does the regional analysis reveal about performance across the United Kingdom?

Within the UK, England leads in market volume owing to its dense urban development and large commercial‑building projects. Scotland, Wales, and Northern Ireland exhibit steady growth, supported by government‑funded housing initiatives and heritage‑restoration programmes that require specialist adhesive technologies.

Which companies lead the UK Ceramic Adhesives Market and what strategies are they employing?

Leading firms such as 3M, Arkema, BASF, Saint‑Gobain, and Sika leverage extensive R&D pipelines to launch low‑VOC, high‑strength adhesives. Partnerships with construction firms and certification bodies help these companies secure specification status in major projects. Acquisition of niche adhesive specialists further broadens their product portfolios and market reach.

How does Porter’s Five Forces framework assess the competitive environment of the UK Ceramic Adhesives Market?

Threat of new entrants is moderate due to high R&D costs and regulatory barriers. Bargaining power of suppliers is low to moderate, given multiple raw‑material sources. Buyers hold considerable power, demanding performance, price competitiveness, and sustainability. Substitute products, such as mechanical fixation methods, present a modest threat. Rivalry among existing firms is intense, driven by innovation cycles and brand loyalty.

What are the SWOT insights for the UK Ceramic Adhesives Market?

Strengths: Established demand, strong regulatory backing, and a portfolio of high‑performance chemistries.

Weaknesses: Sensitivity to raw‑material price fluctuations and reliance on skilled labor for application.

Opportunities: Development of bio‑based adhesives, digital installation tools, and expansion into retrofit sectors.

Threats: Stringent environmental legislation and the emergence of alternative bonding technologies.

How is value created and transferred in the UK Ceramic Adhesives value chain?

The value chain begins with raw‑material suppliers (resins, fillers, solvents), proceeds to formulation and manufacturing by adhesive producers, followed by distribution through specialty chemical distributors and building‑materials retailers. End‑users—contractors, architects, and DIY consumers—apply the adhesives, generating final value through improved construction speed, durability, and compliance with safety standards.

What investment insights are recommended for stakeholders considering the UK Ceramic Adhesives Market?

Investors should focus on companies with strong pipelines in low‑VOC and bio‑based adhesives, as sustainability drives future procurement criteria. Partnerships with construction tech firms that enable precise dosing and rapid curing present attractive growth avenues. Geographic diversification within the UK, especially targeting refurbishment projects, can mitigate cyclical exposure.

What conclusions can be drawn about the UK Ceramic Adhesives Market?

The market is on a robust growth path, underpinned by regulatory support, construction activity, and innovation in adhesive technology. While challenges such as raw‑material cost volatility exist, the sector’s ability to deliver high‑performance, environmentally compliant solutions positions it for sustained expansion through 2032.

Which research methodology was employed to develop this market report?

The study combined primary interviews with industry experts, secondary data analysis from reputable construction and chemical databases, and trend extrapolation using the provided market size and CAGR figures. Forecast modeling applied the 4.97 % CAGR to project future market values.

What is the scope of this research and its limitations?

The scope covers the UK ceramic adhesives market by type and application, examines competitive dynamics, and offers regional insights within the United Kingdom. Limitations include reliance on publicly available data and the exclusion of proprietary company financials beyond the supplied market size and growth rate.

Which key companies are active in the UK Ceramic Adhesives Market and what recent developments have they announced?

Prominent players include 3M Co, Arkema SA, BASF SE, Compagnie de Saint‑Gobain SA, Final Advanced Materials, H.B. Fuller Company, Henkel AG & Co KGaA, Kerakoll SpA, Mapei SpA, and Sika AG. Recent developments feature product launches of low‑VOC epoxy systems, strategic partnerships with green‑building certification bodies, and acquisitions aimed at expanding low‑temperature curing technology portfolios.