What is the Autotransfusion Devices Market overview – definition, scope, and significance?

The Autotransfusion Devices Market comprises technologies that collect, filter, and reinfuse a patient’s own blood lost during surgery or trauma. This scope includes complete systems, consumable accessories, and related software used across hospitals, specialty clinics, and ambulatory surgery centers. The market is significant because autotransfusion reduces reliance on allogeneic blood, lowers transfusion‑related complications, shortens hospital stay, and supports cost containment in increasingly cash‑constrained health‑care systems.

What are the main drivers, restraints, challenges, and opportunities shaping the Autotransfusion Devices Market?

Key drivers include rising surgical volumes, especially cardiac and orthopedic procedures, and heightened awareness of blood‑conservation benefits. Regulatory support for patient‑blood‑management programs also propels growth. Restraints stem from high upfront equipment costs and strict sterility requirements that can limit adoption in low‑resource settings. Challenges involve integration with electronic health records and the need for staff training. Opportunities arise from emerging disposable technologies, miniaturized devices for outpatient settings, and expanding applications in trauma and organ‑transplant surgeries.

What current and emerging trends are influencing the Autotransfusion Devices Market growth?

Current trends feature a shift toward single‑use, pre‑sterilized kits that streamline workflow and reduce infection risk. Manufacturers are investing in digital monitoring interfaces that provide real‑time hemoglobin concentrations and volume analytics. Emerging trends include the development of portable autotransfusion units for field hospitals and combat zones, as well as AI‑driven predictive algorithms that optimize when autotransfusion should be initiated during surgery.

How did COVID‑19 impact the Autotransfusion Devices Market and what is the recovery trajectory?

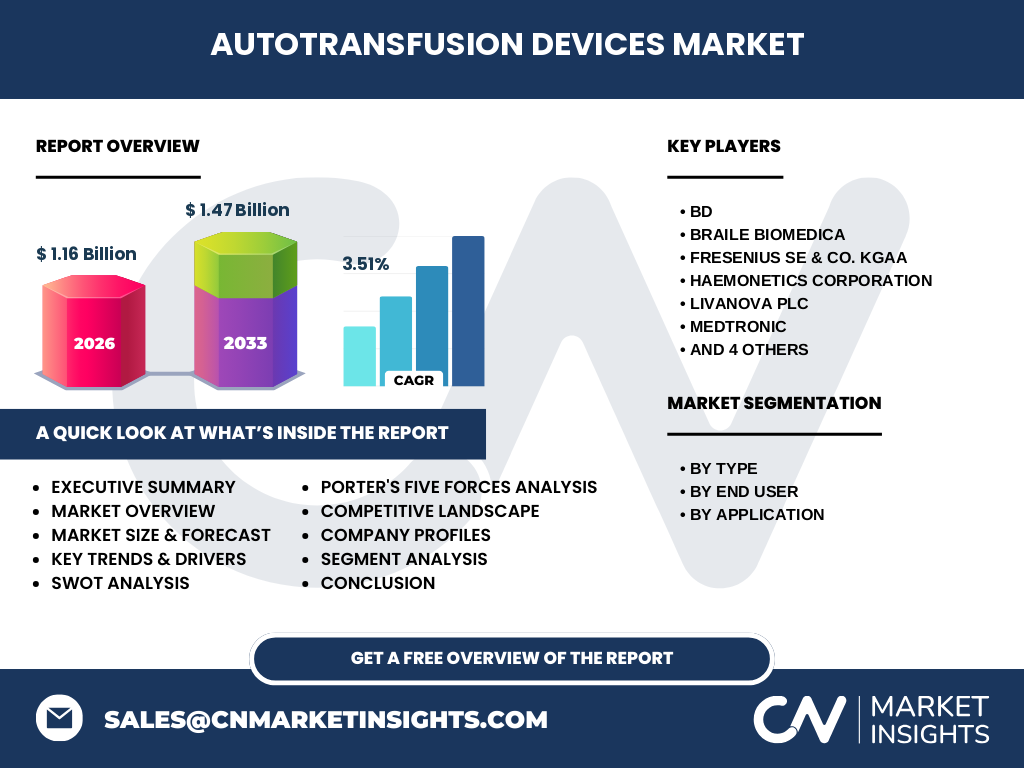

The pandemic caused a temporary slowdown in elective surgeries, reducing short‑term device utilization. However, heightened emphasis on blood safety and supply chain resilience accelerated interest in autotransfusion as a means to conserve donor blood. Post‑2020, elective procedures rebounded, and the market resumed growth, aligning with the projected CAGR of 3.51% through 2032. Recovery is supported by renewed surgical volumes and increased hospital investment in blood‑management technologies.

Who are the major competitors in the Autotransfusion Devices Market and what is the state of market consolidation?

Key competitors include BD, Braile Biomedica, Fresenius SE & Co. KGaA, Haemonetics Corporation, LivaNova PLC, Medtronic, Redax S.p.A., SARSTEDT AG & Co. KG, Teleflex Incorporated, and Zimmer Biomet. The market shows moderate consolidation, with large diversified medical device firms acquiring niche autotransfusion players to broaden product portfolios and achieve scale. Strategic alliances and joint ventures are also common, enhancing geographic reach and technology sharing.

What are the high‑level findings in the Executive Summary of the Autotransfusion Devices Market?

The market is valued at USD 1.16 billion in 2026 and is expected to reach USD 1.47 billion by 2033, growing at a 3.51% CAGR. Growth is driven by expanding surgical procedures, blood‑conservation mandates, and technological innovations in disposables and monitoring. Hospitals dominate usage, while specialty clinics and ambulatory surgery centers present emerging demand. Competitive dynamics are shaped by a blend of legacy OEMs and agile innovators, creating a balanced yet competitive landscape.

What is the forecast for the Autotransfusion Devices Market from 2025 to 2032?

Based on a steady 3.51% compound annual growth rate, the market is projected to expand from roughly USD 1.10 billion in 2025 to USD 1.47 billion by 2033. This trajectory reflects consistent adoption across core segments, incremental penetration into ambulatory settings, and sustained replacement cycles for aging equipment. The forecast underscores a robust upside for manufacturers that can deliver cost‑effective, user‑friendly solutions.

How is the Autotransfusion Devices Market sized and shared by segmentation?

Segmentation is organized by type, end‑user, and application. The “Product and Accessories” category captures the bulk of revenue, encompassing devices, filters, and consumables. By end‑user, hospitals hold the largest share, followed by specialty clinics and ambulatory surgery centers, reflecting volume differentials. Application‑wise, cardiac surgeries lead demand, with orthopedic surgeries, organ transplantation, and trauma procedures contributing significant, growing portions as procedural techniques evolve.

What is the geographic distribution of the Global Autotransfusion Devices Market?

While specific regional dollar values are not disclosed, the market exhibits a worldwide presence across North America, Europe, Asia‑Pacific, Latin America, and the Middle East & Africa. Developed regions drive early adoption due to mature health‑care infrastructure, whereas emerging markets are gaining traction as hospitals modernize and adopt blood‑conservation protocols.

How does each major region perform in the Autotransfusion Devices Market?

North America remains the largest contributor, propelled by high surgical volumes and strong reimbursement frameworks. Europe follows, benefitting from stringent blood‑safety regulations. Asia‑Pacific shows the fastest growth rate, fueled by rapid hospital expansion and increasing awareness of autotransfusion benefits. Latin America and the Middle East & Africa present steady growth, supported by ongoing health‑care investments and rising demand for advanced surgical technologies.

What are the profiles and strategies of leading companies in the Autotransfusion Devices Market?

BD focuses on integrated blood‑management solutions and expanding its consumable portfolio. Haemonetics leverages its strong service network and invests in digital monitoring. LivaNova emphasizes innovation in low‑volume devices for cardiac applications. Medtronic integrates autotransfusion into its broader surgical ecosystem. Zimmer Biomet targets orthopedic surgeons with specialized accessories. Most players pursue R&D, strategic acquisitions, and geographic expansion to strengthen market position.

How does Porter’s Five Forces model apply to the Autotransfusion Devices Market?

Threat of new entrants is moderate due to high regulatory barriers and capital intensity. Bargaining power of suppliers is low to moderate; key components are relatively commoditized. Bargaining power of buyers is growing as hospitals demand cost‑effective, high‑quality solutions. Threat of substitutes is limited; allogeneic blood transfusion remains an alternative but is less favored. Industry rivalry is intense, with multiple established firms competing on technology, price, and service.

What are the SWOT analysis highlights for the Autotransfusion Devices Market?

Strengths: Proven clinical benefits, cost savings, and alignment with patient‑blood‑management initiatives. Weaknesses: High initial equipment cost and dependence on skilled operators. Opportunities: Expansion into ambulatory centers, development of portable units, and digital integration. Threats: Stringent regulatory changes and potential budget cuts in health‑care spending.

What does the value chain of the Autotransfusion Devices Market look like?

The value chain begins with raw material suppliers (metals, polymers, filtration media), proceeds to component manufacturing (pumps, filters), then to system assembly and integration of software. Afterward, distributors and medical‑device wholesalers deliver finished units to hospitals and clinics. Post‑sale services, including maintenance contracts, training, and consumable replenishment, complete the chain, creating recurring revenue streams.

What key investment insights can be drawn for the Autotransfusion Devices Market?

Investors should prioritize companies with strong R&D pipelines for disposable technologies and digital platforms. Partnerships that enable entry into emerging markets, especially Asia‑Pacific, offer upside. Firms that secure long‑term service agreements and consumable contracts demonstrate stable cash flow. Monitoring regulatory developments and reimbursement policies will be essential for evaluating risk.

What are the main conclusions from the Autotransfusion Devices Market analysis?

The market is poised for steady growth, anchored by clinical efficacy, cost advantages, and expanding surgical applications. While equipment costs and training needs pose challenges, innovation in disposables and portable systems mitigates these barriers. Geographic diversification and strategic collaborations will be critical for companies aiming to capture the projected USD 1.47 billion market size by 2033.

How was the research for this Autotransfusion Devices Market report conducted?

The study combined secondary data from industry reports, company filings, and regulatory databases with primary insights from expert interviews with surgeons, procurement officers, and device manufacturers. Market sizing employed a top‑down approach anchored to the provided 2026 market value and CAGR, while forecasts used trend‑adjusted extrapolation. Competitive analysis integrated publicly available financials and product roadmaps.

What is the scope of this Autotransfusion Devices Market research?

The scope covers global market size, segmentation by type, end‑user, and application, and regional performance across major continents. It includes competitive landscape, value‑chain mapping, and strategic analyses (Porter’s Five Forces, SWOT). The study excludes proprietary financial details beyond the disclosed market size and CAGR, and it does not assess device pricing at the SKU level.

Which key companies have announced recent developments in the Autotransfusion Devices Market?

BD launched a next‑generation autotransfusion system with integrated hemoglobin monitoring. Haemonetics announced a partnership with a leading Asian hospital network to supply disposable kits. LivaNova introduced a compact device tailored for minimally invasive cardiac surgery. Medtronic released a software upgrade enabling seamless data integration with operating‑room information systems. Zimmer Biomet unveiled new orthopedic‑specific accessories designed to improve blood‑collection efficiency.