What is the Ultrasound Transducer Market Overview – definition, scope, and significance?

The Ultrasound Transducer Market comprises manufacturers and suppliers of devices that convert electrical energy into acoustic waves and vice‑versa, enabling diagnostic imaging across a wide range of clinical settings. The market scope spans a diverse product portfolio—including linear, convex, phased‑array, endocavitary, CW Doppler, and TEE probes—serving hospitals, clinics, diagnostic centers, and ambulatory surgical facilities. Its significance lies in the critical role of transducers in non‑invasive imaging, early disease detection, and guided interventions, which collectively drive demand for advanced medical imaging solutions worldwide.

What are the primary drivers, restraints, challenges, and opportunities shaping the Ultrasound Transducer Market?

Key drivers include rising prevalence of chronic diseases, expanding point‑of‑care imaging, and increasing adoption of portable ultrasound systems. Technological advances such as miniaturization, AI‑enhanced image processing, and higher‑frequency probes further stimulate growth. Restraints stem from high initial equipment costs and stringent regulatory requirements that can delay product launches. Challenges involve supply‑chain constraints for piezoelectric materials and competitive pressure from alternative imaging modalities like MRI and CT. Opportunities arise from emerging applications in musculoskeletal and obstetrics imaging, as well as growth in emerging economies where healthcare infrastructure is being modernized.

What are the current growth trends in the Ultrasound Transducer Market?

The market is witnessing a shift toward handheld, wireless transducers that integrate with smartphones and cloud platforms, enabling real‑time tele‑ultrasound. There is a growing preference for high‑resolution linear and phased‑array probes for vascular and cardiovascular diagnostics. Additionally, the convergence of ultrasound with contrast agents and elastography is expanding clinical utility. Companies are investing in modular designs that allow users to swap probe heads, reducing total cost of ownership and fostering a service‑oriented business model.

How did COVID‑19 impact the Ultrasound Transducer Market and what is the recovery trajectory?

During the pandemic, elective imaging procedures were postponed, leading to a short‑term dip in demand for new transducers. Conversely, the need for bedside imaging in intensive care units accelerated adoption of portable and point‑of‑care ultrasound devices, partially offsetting the decline. Post‑COVID, the market has entered a steady recovery phase, with hospitals and clinics replenishing equipment inventories and expanding their point‑of‑care capabilities, supporting a rebound in sales and a positive outlook.

Who are the major competitors in the Ultrasound Transducer Market and how is consolidation progressing?

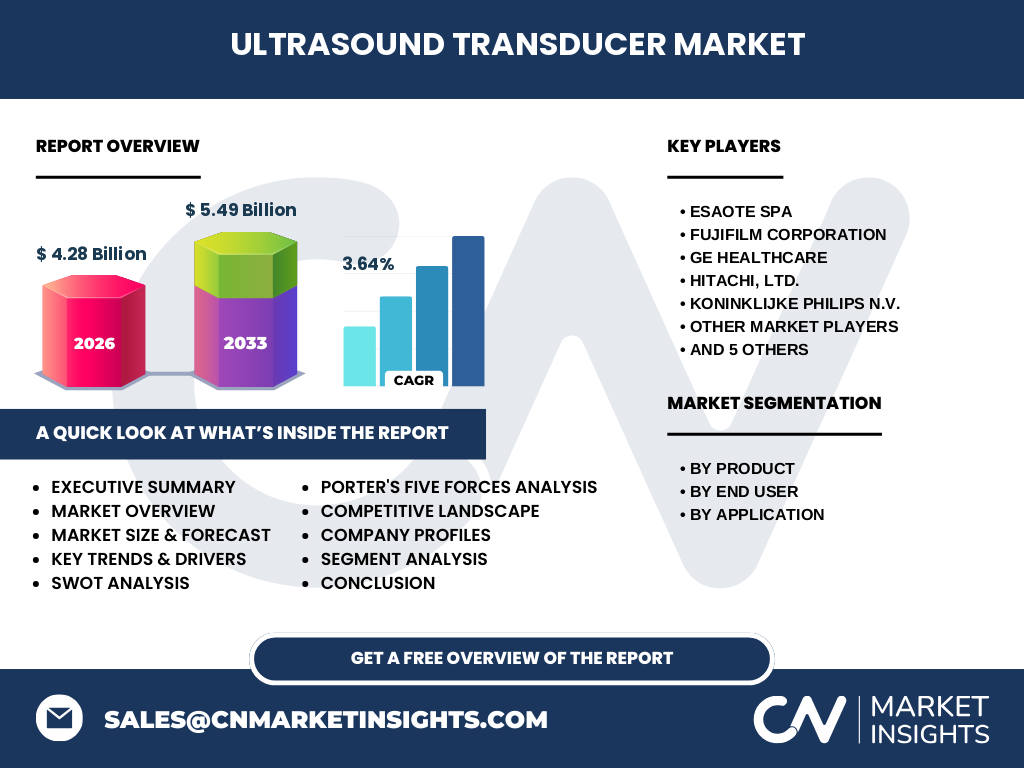

Leading players include ESAOTE SPA, Fujifilm Corporation, GE Healthcare, Hitachi Ltd., Koninklijke Philips N.V., SIUI, Samsung, Shenzhen Mindray Bio‑Medical Electronics Co., Ltd., Shenzhen Ruqi Technology Co., Ltd., and Siemens Healthineers. The competitive landscape is characterized by strategic collaborations, joint R&D initiatives, and selective mergers aimed at broadening product portfolios and geographic reach. While the market remains fragmented, consolidation is intensifying as larger OEMs acquire niche technology firms to enhance capabilities in AI‑driven imaging and miniaturized probe design.

What are the high‑level findings highlighted in the Executive Summary?

The Ultrasound Transducer Market is projected to reach USD 5.49 billion by 2033, growing at a CAGR of 3.64% from 2027 onward. Growth is underpinned by expanding clinical applications, the rise of portable ultrasound solutions, and sustained investment in advanced probe technologies. North America and Europe retain mature adoption rates, while Asia‑Pacific exhibits the highest growth potential due to expanding healthcare infrastructure. Leading companies are differentiating through innovation, strategic partnerships, and value‑added services, positioning the market for steady expansion over the next decade.

What are the forecasted market size and growth expectations for 2025‑2032?

Based on the provided data, the market is valued at USD 4.28 billion in 2026. With a compound annual growth rate of 3.64%, the market is expected to expand to approximately USD 5.49 billion by 2033. This trajectory implies a consistent upward trend throughout the 2025‑2032 period, driven by continued product innovation and broader adoption across clinical environments.

How is the market sized and shared across product, end‑user, and application segments?

The market segmentation includes:

By Product: Linear, convex, phased‑array, endocavitary, CW Doppler, and TEE probes.

By End User: Hospitals, clinics, diagnostic centers, and ambulatory surgical centers.

By Application: Cardiovascular, general imaging, musculoskeletal, obstetrics and gynaecology, and vascular.

Each segment contributes to the overall market, with hospitals representing the largest end‑user due to their extensive imaging needs, while linear and convex probes dominate the product mix because of their versatility in general and specialized imaging.

What is the global market size and share by region?

The global market is anchored by strong demand in North America and Europe, reflecting mature healthcare systems and high adoption of advanced imaging technologies. Asia‑Pacific is emerging as a rapid growth hub, supported by increasing hospital construction, rising disposable incomes, and government initiatives to enhance diagnostic capabilities. While specific regional dollar values are not disclosed, the relative prominence of these regions aligns with overall industry patterns.

What does the regional analysis reveal about market performance?

In North America, demand is driven by technology‑focused hospitals and a robust reimbursement environment. Europe benefits from a well‑established private‑public mix and strong regulatory frameworks that encourage innovation. Asia‑Pacific shows the strongest growth momentum, with China, India, and Japan leading investments in modern imaging equipment. Latin America and the Middle East exhibit moderate growth, influenced by healthcare reforms and expanding private sector participation.

Which companies lead the market and what are their strategic approaches?

Key leaders such as GE Healthcare, Philips, and Siemens Healthineers leverage extensive R&D pipelines, broad product portfolios, and global distribution networks. ESAOTE SPA focuses on high‑performance, compact probes targeting point‑of‑care settings. Fujifilm emphasizes integration of imaging with digital health platforms. Companies like Mindray and Samsung pursue aggressive pricing and rapid product cycles to capture emerging market share in cost‑sensitive regions.

How does Porter’s Five Forces model apply to the Ultrasound Transducer Market?

Threat of new entrants: Moderate, due to high capital requirements and regulatory barriers.

Bargaining power of suppliers: Moderate, as key components like piezoelectric crystals are sourced from a limited number of specialized suppliers.

Bargaining power of buyers: High, especially for large hospital groups that can negotiate volume discounts.

Threat of substitutes: Low to moderate, given the unique advantages of ultrasound over ionizing radiation modalities.

Rivalry among existing competitors: High, driven by rapid product innovation and price competition.

What are the SWOT insights for the overall Ultrasound Transducer Market?

Strengths: Non‑invasive nature, real‑time imaging, and expanding clinical applications.

Weaknesses: Dependence on specialist training and high initial equipment cost.

Opportunities: Integration with AI, growth in portable devices, and untapped emerging markets.

Threats: Regulatory delays, potential supply chain disruptions, and competition from alternative imaging technologies.

What does the value chain for ultrasound transducers look like?

The value chain begins with raw material sourcing (piezoelectric ceramics, polymers), followed by component manufacturing (transducer elements, cable assemblies). Next, core R&D activities design probe architecture and signal processing algorithms. Companies then move to assembly, testing, and quality certification before distributing finished probes through global sales networks, aftermarket service, and training programs. Post‑sale services, including calibration and software upgrades, form the final value‑adding stage.

What key investment insights should stakeholders consider?

Investors should focus on companies that demonstrate strong pipelines in portable and AI‑enabled transducers, as these segments are projected to command the fastest growth. Partnerships with healthcare providers for bundled imaging solutions can enhance revenue stability. Monitoring regulatory approvals and supply‑chain resilience for critical materials will also be essential for risk mitigation.

What are the concluding takeaways from the Ultrasound Transducer Market analysis?

The market is on a steady growth path, driven by technological innovation and expanding clinical use cases. While challenges such as cost and regulatory hurdles persist, the combination of portable technology, AI integration, and emerging market demand creates a robust outlook. Companies that can balance innovation with cost‑effectiveness are likely to capture the greatest share of the projected USD 5.49 billion market by 2033.

How was the research conducted for this report?

Research methodology involved primary interviews with industry experts, secondary data extraction from reputable databases, and triangulation of financial reports, press releases, and regulatory filings. Market sizing utilized top‑down and bottom‑up approaches, calibrated against the provided baseline figures (USD 4.28 billion in 2026) and the projected CAGR of 3.64%.

What is the scope of this research?

The study covers global ultrasound transducer manufacturers, segmented by product type, end‑user, and application. Geographic coverage includes North America, Europe, Asia‑Pacific, Latin America, and the Middle East. The analysis spans the period from 2025 to 2033, focusing on market size, growth drivers, competitive dynamics, and strategic recommendations.

Which key companies have recent developments worth noting?

GE Healthcare announced a new line of AI‑enhanced linear probes aimed at cardiovascular diagnostics. Philips launched a compact handheld device with cloud‑based image sharing. Siemens Healthineers introduced a modular probe system that allows clinicians to interchange heads for multiple applications. Mindray released a budget‑friendly convex probe targeting emerging markets, while ESAOTE SPA secured a partnership with a major hospital network to pilot remote ultrasound imaging solutions. These activities underscore the sector’s emphasis on innovation, accessibility, and collaborative growth.