1. Asia Pacific Medical Equipment Maintenance Market Overview - Definition, scope, and significance?

The Asia Pacific Medical Equipment Maintenance market encompasses all services that ensure the optimal performance, safety, and longevity of medical devices used in hospitals, clinics, and diagnostic centers across the region. It covers preventive, corrective, and operational maintenance for a broad range of equipment, including electromedical devices, endoscopic systems, surgical instruments, and other medical apparatus. The scope extends to services delivered by original equipment manufacturers (OEMs), independent service organizations (ISOs), and in‑house maintenance teams. This market is significant because reliable equipment directly impacts patient outcomes, regulatory compliance, and operational efficiency in healthcare facilities, driving substantial investment in maintenance solutions throughout the fast‑growing Asia Pacific health sector.

2. Asia Pacific Medical Equipment Maintenance Market Drivers, Restraints, Challenges, and Opportunities - Key growth factors and obstacles?

Key drivers include increasing healthcare spending, rapid expansion of hospitals and diagnostic centers, and rising adoption of advanced medical technologies that demand specialized upkeep. Government initiatives aimed at improving healthcare infrastructure and stringent regulatory requirements for equipment safety further stimulate demand. Restraints arise from high servicing costs, limited skilled technician availability in certain sub‑regions, and price sensitivity among smaller providers. Challenges involve managing the complexity of heterogeneous device portfolios and integrating predictive maintenance technologies. Opportunities exist in digitalization—using IoT and AI for condition‑based monitoring—, growth of outsourcing to ISOs, and expanding service offerings for emerging device categories such as robotic surgery platforms.

3. Asia Pacific Medical Equipment Maintenance Market Growth Trends - Current and emerging trends shaping the market?

Current trends show a shift from reactive to preventive maintenance, with contracts covering scheduled inspections, calibration, and software updates. An emerging trend is the adoption of remote diagnostics and predictive analytics, leveraging connectivity within equipment to forecast failures. Another notable development is the increasing preference for bundled service models that combine preventive and corrective maintenance under a single SLA, creating predictable cost structures for healthcare providers. Finally, strategic partnerships between OEMs and ISOs are accelerating knowledge transfer and helping bridge the talent gap.

4. COVID-19 Impact on the Asia Pacific Medical Equipment Maintenance Market - Pandemic effects and recovery trajectory?

The COVID‑19 pandemic initially disrupted routine maintenance schedules due to lockdowns and the redeployment of technical staff to emergency response activities. However, the crisis also highlighted the critical need for reliable equipment, prompting hospitals to accelerate maintenance contracts and adopt remote service capabilities. Post‑pandemic, the market has entered a robust recovery phase, with renewed focus on resilience and uptime, driving a higher propensity to invest in comprehensive maintenance programs. This recovery contributes to the projected CAGR of 9.70% through 2033.

5. Asia Pacific Medical Equipment Maintenance Market Competitive Landscape - Major competitors and market consolidation?

The competitive landscape features a blend of global OEMs and specialized service providers. Leading players such as Abbott, B. Braun Melsungen AG, Johnson & Johnson, Medtronic, and Stryker leverage their extensive device portfolios to offer integrated maintenance solutions. Independent service organizations like Althea and Aramark Services, Inc. focus on cost‑effective, multi‑vendor support, while some hospitals maintain in‑house teams for critical assets. Recent consolidation activity includes acquisitions of niche service firms by larger OEMs, aiming to broaden service footprints and enhance technical expertise across the region.

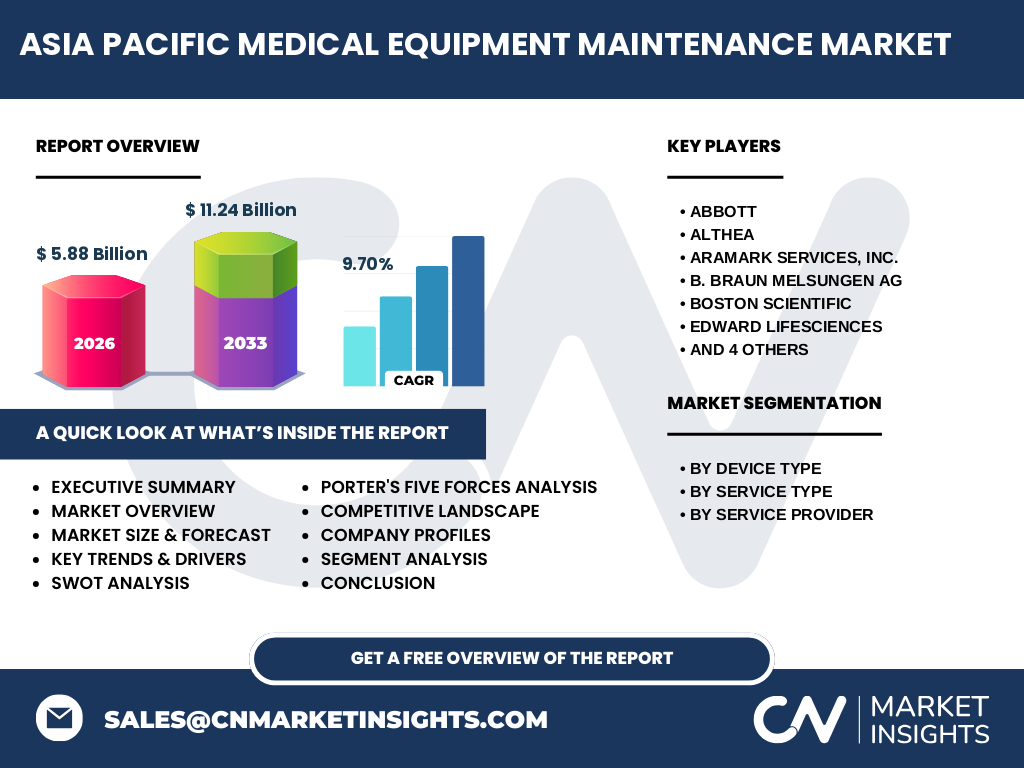

6. Executive Summary - High-level overview and key findings about Asia Pacific Medical Equipment Maintenance Market?

The Asia Pacific Medical Equipment Maintenance market, valued at USD 5.88 billion in 2026, is projected to reach USD 11.24 billion by 2033, expanding at a 9.70% CAGR. Growth is driven by rising healthcare expenditures, expanding hospital networks, and increasing complexity of medical devices. Preventive maintenance dominates service types, while OEMs and ISOs compete for market share through digital service platforms and bundled contracts. The market exhibits strong resilience post‑COVID‑19, with digital transformation and talent development emerging as critical success factors. Key opportunities lie in predictive maintenance, outsourcing, and regional expansion into emerging economies.

7. Asia Pacific Medical Equipment Maintenance Market Forecast - Projections for 2025-2032 period?

Based on the provided CAGR of 9.70%, the market is expected to sustain robust growth throughout the 2025‑2032 horizon. Starting from the 2026 base of USD 5.88 billion, the market will surpass the USD 10 billion mark by the early 2030s, reaching the forecasted USD 11.24 billion by 2033. This trajectory reflects continued capital investment in health infrastructure, expanding device inventories, and the scaling of advanced service models across the Asia Pacific region.

8. Asia Pacific Medical Equipment Maintenance Market Size and Share by Segmentation - Breakdown by segment data?

By Device Type, the market serves electromedical equipment, endoscopic devices, surgical instruments, and other medical equipment, with electromedical devices typically commanding the largest share due to their prevalence in imaging and monitoring. By Service Type, preventive maintenance leads, followed by corrective and operational maintenance, reflecting the industry’s focus on scheduled upkeep to avoid downtime. By Service Provider, OEMs hold a strong position owing to proprietary knowledge, while independent service organizations capture growth through cost‑effective multi‑vendor solutions, and in‑house maintenance remains important for high‑priority assets.

9. Global Asia Pacific Medical Equipment Maintenance Market Size and Share by Region - Geographic distribution?

The Asia Pacific region accounts for the entirety of the market under review, with the overall size reflected in the USD 5.88 billion figure for 2026. Within the region, sub‑markets such as Greater China, Japan, India, and Southeast Asia exhibit varying degrees of maturity, but collectively they drive the forecasted growth to USD 11.24 billion by 2033.

10. Regional Analysis of the Asia Pacific Medical Equipment Maintenance Market - Detailed regional market performance?

China leads the regional market due to its massive hospital network and government incentives for equipment upgrades. Japan shows high adoption of advanced surgical instruments, prompting strong demand for specialized service contracts. India’s rapid healthcare expansion and growing private hospital sector generate increasing maintenance needs, particularly for cost‑effective independent service providers. Southeast Asian economies like Australia, Singapore, and Malaysia benefit from higher per‑capita health spending, fostering sophisticated maintenance ecosystems and openness to digital service solutions.

11. Leading Company Profiles in the Asia Pacific Medical Equipment Maintenance Market - Industry players and strategies?

Abbott leverages its extensive device portfolio to provide bundled maintenance packages, emphasizing remote monitoring. Althea, an independent service organization, focuses on multi‑vendor support and competitive pricing. Aramark Services, Inc. differentiates through integrated facilities management that includes equipment upkeep. B. Braun Melsungen AG offers OEM‑driven service contracts with strong field engineer networks. Boston Scientific and Johnson & Johnson prioritize technology‑enabled predictive maintenance for their high‑margin devices. Medtronic and Stryker expand service offerings via strategic acquisitions of niche service firms, while Terumo Corporation emphasizes after‑sales support for its cardiovascular devices.

12. Porter's Five Forces Analysis of the Asia Pacific Medical Equipment Maintenance Market - Competitive forces assessment?

Threat of New Entrants: Moderate. High capital requirements for technical expertise and regulatory compliance deter many newcomers, though niche ISOs can enter with focused capabilities. Bargaining Power of Buyers: High. Hospitals and health systems negotiate contract terms and price, especially in price‑sensitive markets. Bargaining Power of Suppliers: Low to moderate. OEMs control proprietary knowledge, but independent providers can source generic parts, balancing supplier power. Threat of Substitutes: Low. Alternative options are limited to equipment replacement, which is costlier than maintenance. Rivalry Among Existing Competitors: Intense. OEMs, ISOs, and in‑house teams compete on service quality, response times, and digital capabilities, driving ongoing innovation and consolidation.

13. SWOT Analysis of the Asia Pacific Medical Equipment Maintenance Market - Strengths, weaknesses, opportunities, threats?

Strengths: Growing healthcare investment, regulatory focus on equipment safety, and expanding device portfolios. Weaknesses: Skilled technician shortage and high servicing costs in certain markets. Opportunities: Adoption of IoT‑enabled predictive maintenance, outsourcing trends, and expansion into emerging economies. Threats: Price pressure from cost‑conscious buyers, rapid technology turnover requiring continual upskilling, and potential supply chain disruptions for spare parts.

14. Asia Pacific Medical Equipment Maintenance Market Value Chain Analysis - Industry structure and value flow?

The value chain begins with OEMs designing and manufacturing devices, followed by distribution to healthcare facilities. Service initiation occurs through contracts—either OEM‑direct, ISO‑based, or in‑house. Maintenance execution involves field engineers conducting preventive checks, corrective repairs, and operational support, often supported by remote diagnostics platforms. After‑service activities include parts replenishment, performance reporting, and contract renewal negotiations, completing the cycle and creating feedback loops for product improvement.

15. Key Investment Insights in the Asia Pacific Medical Equipment Maintenance Market - Strategic investment recommendations?

Investors should target companies that blend OEM expertise with digital service platforms, as these are well‑positioned to capture growth from predictive maintenance. Acquisitions of niche independent service firms can accelerate geographic reach and broaden multi‑vendor capabilities. Funding for skill development programs and remote‑service technologies will enhance service quality and reduce cost pressures. Additionally, focusing on high‑growth sub‑regions such as India and Southeast Asia offers attractive long‑term returns.

16. Asia Pacific Medical Equipment Maintenance Market Conclusion - Summary and key takeaways?

The Asia Pacific Medical Equipment Maintenance market is on a clear upward trajectory, moving from a USD 5.88 billion base in 2026 to an anticipated USD 11.24 billion by 2033, driven by a 9.70% CAGR. Core drivers include expanding healthcare infrastructure, rising device complexity, and a shift toward preventive and predictive service models. Competitive dynamics favor players that integrate digital solutions, forge strategic partnerships, and address talent gaps. The market presents compelling investment opportunities, especially in digitalization, outsourcing, and regional expansion.

17. Research Methodology - How this research was conducted?

The study employed a mixed‑method approach, combining primary interviews with industry experts, OEM representatives, and independent service providers, alongside secondary data collection from company reports, regulatory publications, and reputable market databases. Quantitative analysis utilized the provided market size (USD 5.88 billion) and forecast (USD 11.24 billion) figures to calculate the 9.70% CAGR. Qualitative insights were derived from trend observation and competitive mapping.

18. Research Scope - Coverage and limitations?

The scope encompasses all medical equipment maintenance activities across the Asia Pacific region, segmented by device type, service type, and service provider. It covers both preventive and corrective services and includes analysis of major OEMs, independent service firms, and in‑house teams. The research does not extend to equipment manufacturing volumes or pricing details beyond the provided market values.

19. Key Companies and Recent Developments in the Asia Pacific Medical Equipment Maintenance Market - Introduction to top companies and their recent announcements, product launches, partnerships, and strategic developments?

Recent developments include Abbott’s launch of a cloud‑based remote monitoring platform for its cardiovascular devices, enhancing predictive maintenance capabilities. Althea announced a partnership with several regional hospitals to provide bundled multi‑vendor service contracts at discounted rates. B. Braun Melsungen AG expanded its field service network in Southeast Asia, adding 150 new technicians. Johnson & Johnson introduced an AI‑driven service scheduler that optimizes technician routing across Japan and Australia. Medtronic completed the acquisition of a local ISO in India, strengthening its after‑sales footprint. Stryker rolled out a new line‑service program for robotic surgical systems, combining on‑site training with continuous equipment health monitoring. These initiatives illustrate the market’s focus on digitalization, geographic expansion, and integrated service solutions.