North America Aircraft Heat Exchanger Market Overview - Definition, scope, and significance?

The North America Aircraft Heat Exchanger Market comprises devices that transfer thermal energy between fluid streams in aviation systems, ensuring optimal engine performance, cabin comfort, and structural integrity. The scope covers heat exchangers used in both commercial and military aircraft, spanning flat‑tube and plate‑fin technologies across engine, airframe, rotary‑wing, and fixed‑wing applications. Their significance lies in enhancing fuel efficiency, reducing emissions, and meeting stringent safety and reliability standards demanded by regulators and operators.

North America Aircraft Heat Exchanger Market Drivers, Restraints, Challenges, and Opportunities - Key growth factors and obstacles?

Key drivers include increasing demand for fuel‑efficient aircraft, stringent environmental regulations, and rising defense spending that fuels advanced heat‑management solutions. Opportunities arise from the adoption of lightweight materials and digital twins for predictive maintenance. Restraints involve high upfront R&D costs and lengthy certification processes, while challenges stem from supply‑chain constraints for specialty alloys and the need for skilled technicians to service complex systems.

North America Aircraft Heat Exchanger Market Growth Trends - Current and emerging trends shaping the market?

Current trends feature a shift toward plate‑fin exchangers for their compactness and superior heat‑transfer coefficients, especially in modern turbofan engines. Emerging trends include integration of additive manufacturing to produce optimized heat‑exchange geometries and the use of IoT sensors for real‑time thermal monitoring. Additionally, hybrid electric propulsion concepts are driving the development of exchangers that can manage both thermal and electrical loads.

COVID-19 Impact on the North America Aircraft Heat Exchanger Market - Pandemic effects and recovery trajectory?

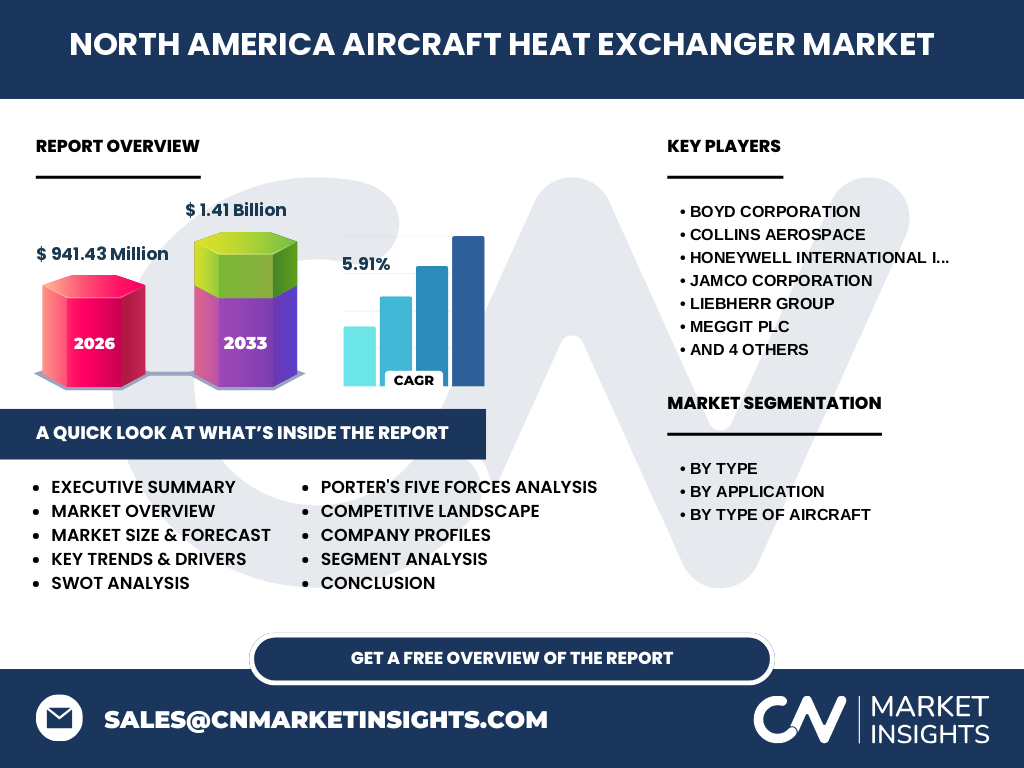

The pandemic caused a temporary dip in commercial aircraft production, slowing new‑order pipelines and deferring retrofit projects. However, defense programs remained relatively stable, cushioning the market. Recovery accelerated in 2022 as airlines resumed fleet modernization and operators prioritized fuel‑saving technologies, prompting a renewed focus on heat‑exchanger upgrades. The market is now on a clear upward trajectory, reflected in the projected CAGR of 5.91%.

North America Aircraft Heat Exchanger Market Competitive Landscape - Major competitors and market consolidation?

The competitive landscape is dominated by established aerospace suppliers such as BOYD Corporation, Collins Aerospace, Honeywell International Inc, Jamco Corporation, Liebherr Group, Meggit Plc, TAT Technologies Inc., Triumph Group, Wall Colmonoy, and Woodward Inc. Recent years have seen strategic alliances and joint ventures aimed at sharing technology platforms, but no major mergers have reshaped the market hierarchy. Companies compete on performance, weight reduction, and life‑cycle cost.

Executive Summary - High-level overview and key findings about North America Aircraft Heat Exchanger Market?

The North America Aircraft Heat Exchanger Market is valued at $941.43 million in 2026 and is projected to reach $1.41 billion by 2033, delivering a 5.91% CAGR. Growth is propelled by efficiency‑driven aircraft designs, regulatory pressure, and defense investment. Plate‑fin and flat‑tube technologies address distinct application needs, while key players focus on innovation and strategic partnerships to capture market share. The outlook remains robust, with expanding opportunities in electric‑propulsion support.

North America Aircraft Heat Exchanger Market Forecast - Projections for 2025-2032 period?

Based on the provided CAGR of 5.91%, the market is expected to maintain steady expansion from 2025 through 2032, moving from roughly $890 million in 2025 to well above $1.3 billion by the end of 2032. This forecast reflects continued investment in newer aircraft platforms, increased retrofit activity for existing fleets, and heightened demand for lightweight, high‑efficiency thermal management solutions across both commercial and military sectors.

North America Aircraft Heat Exchanger Market Size and Share by Segmentation - Breakdown by segment?

Segmentation by type highlights flat‑tube and plate‑fin exchangers, with plate‑fin gaining traction in newer engine designs due to higher heat‑transfer efficiency. Application‑wise, engine exchangers command the largest share, followed by airframe systems that manage cabin and avionics cooling. By aircraft type, fixed‑wing platforms dominate the market, though rotary‑wing applications are growing as helicopter manufacturers adopt advanced thermal‑management concepts for mission‑critical missions.

Global North America Aircraft Heat Exchanger Market Size and Share by Region - Geographic distribution?

North America represents the primary regional hub for aircraft heat‑exchanger production and consumption, leveraging a mature aerospace ecosystem, extensive certification infrastructure, and significant defense budgets. While the market is predominantly North American, ancillary demand comes from global OEMs that source components from the region, reinforcing its role as a strategic supplier to worldwide aircraft manufacturers.

Regional Analysis of the North America Aircraft Heat Exchanger Market - Detailed regional market performance?

Within North America, the United States accounts for the majority of market activity, driven by major commercial airlines, defense contractors, and aerospace OEMs. Canada contributes through its niche market in regional aircraft and maintenance, repair, and overhaul (MRO) services. The market benefits from strong R&D clusters in states such as Washington, Texas, and California, fostering rapid technology adoption and product innovation.

Leading Company Profiles in the North America Aircraft Heat Exchanger Market - Industry players and strategies?

BOYD Corporation focuses on high‑performance flat‑tube solutions for military platforms. Collins Aerospace leverages its systems integration expertise to offer modular plate‑fin units for commercial fleets. Honeywell International Inc invests in digital monitoring and advanced materials. Jamco Corporation and Liebherr Group emphasize precision manufacturing for engine applications. Other players such as Meggit Plc, TAT Technologies Inc., Triumph Group, Wall Colmonoy, and Woodward Inc. differentiate through niche specialty alloys and aftermarket support services.

Porter's Five Forces Analysis of the North America Aircraft Heat Exchanger Market - Competitive forces assessment?

Threat of new entrants is low due to high certification barriers and capital intensity. Bargaining power of suppliers is moderate; specialty alloy suppliers hold some leverage, yet large OEMs often secure long‑term contracts. Bargaining power of buyers is significant, as airlines and defense agencies demand cost‑effective, reliable solutions. Threat of substitutes remains limited because alternative cooling methods cannot match the proven efficiency of heat exchangers. Industry rivalry is intense, driven by technological differentiation and after‑sales service quality.

SWOT Analysis of the North America Aircraft Heat Exchanger Market - Strengths, weaknesses, opportunities, threats?

Strengths: Mature supply chain, high technical expertise, and strong defense backing. Weaknesses: High development costs and certification timelines. Opportunities: Adoption of lightweight composites, growth of electric‑propulsion aircraft, and expanding aftermarket services. Threats: Volatile raw‑material prices, potential trade restrictions, and rapid technology shifts that could render existing designs obsolete.

North America Aircraft Heat Exchanger Market Value Chain Analysis - Industry structure and value flow?

The value chain begins with raw‑material suppliers (copper, aluminum, titanium alloys), proceeds to component design and engineering firms, followed by precision manufacturing and testing facilities. Integration occurs at OEM assembly lines, after which the products enter the aftermarket for MRO activities. Key value‑adding steps include thermal‑performance simulation, lightweight design optimization, and digital monitoring integration.

Key Investment Insights in the North America Aircraft Heat Exchanger Market - Strategic investment recommendations?

Investors should target companies with strong IP in plate‑fin technology and those advancing additive‑manufacturing capabilities. Partnerships with defense agencies provide stable revenue streams, while collaborations with commercial airlines on retrofit programs offer growth upside. Funding R&D for IoT‑enabled thermal management can differentiate portfolio companies and unlock premium pricing.

North America Aircraft Heat Exchanger Market Conclusion - Summary and key takeaways?

The market’s $941.43 million 2026 valuation and projected $1.41 billion size by 2033 underscore a healthy growth trajectory. Drivers such as efficiency mandates and defense spending are outweighing constraints like certification costs. Plate‑fin exchangers are emerging as the preferred technology, and leading firms are intensifying innovation and partnership efforts. The outlook remains positive, with ample opportunities for strategic investors and technology developers.

Research Methodology - How this research was conducted?

This study employed a mixed‑method approach, combining primary interviews with industry executives, secondary data extraction from company reports, regulatory filings, and aerospace databases, and quantitative modeling to extrapolate market size and forecast. Trend analysis, competitive benchmarking, and scenario planning were applied to ensure robust, data‑driven insights.

Research Scope - Coverage and limitations?

The scope covers all heat‑exchanger types used in North American commercial and military aircraft, segmented by technology, application, and aircraft class. It excludes non‑aerospace heat‑exchange products and focuses on the period up to 2033. Geographic focus is limited to North America, though global supply‑chain dynamics are considered where relevant.

Key Companies and Recent Developments in the North America Aircraft Heat Exchanger Market - Introduction to top companies and their recent announcements, product launches, partnerships, and strategic developments?

Recent highlights include Collins Aerospace’s launch of a next‑generation plate‑fin module for the latest narrow‑body jets, Honeywell’s partnership with a leading MRO network to embed IoT sensors in existing exchangers, and Liebherr Group’s acquisition of a specialty alloy supplier to secure material supply. BOYD Corporation announced a defense‑focused flat‑tube redesign for high‑altitude UAVs, while Triumph Group expanded its aftermarket service footprint through a new regional hub in Canada.