1. North America PACS and RIS Market Overview - Definition, scope, and significance?

The North America Picture Archiving Communication System (PACS) and Radiology Information System (RIS) market encompasses technologies that capture, store, transmit, and manage medical imaging and associated data. PACS converts analog images to digital format, enabling rapid access across facilities, while RIS streamlines radiology workflow, scheduling, reporting, and billing. The market scope includes hardware, software, and services deployed in hospitals, diagnostic centers, and research or academic institutes, delivered via on‑premise, cloud‑based, or web‑based solutions. This ecosystem is crucial for improving diagnostic accuracy, reducing patient turnaround time, and supporting value‑based care initiatives throughout the United States and Canada.

2. North America PACS and RIS Market Drivers, Restraints, Challenges, and Opportunities - Key growth factors and obstacles?

Key drivers are the increasing demand for digital imaging, rising prevalence of chronic diseases, and strong government incentives for health‑IT adoption. Expanding tele‑radiology and the shift toward integrated health information exchanges further accelerate demand. Restraints include high upfront capital costs for on‑premise installations and stringent regulatory compliance requirements. Challenges arise from data security concerns and interoperability issues across legacy systems. Opportunities exist in cloud migration, AI‑enhanced image analysis, and service‑based models that lower entry barriers for smaller providers.

3. North America PACS and RIS Market Growth Trends - Current and emerging trends shaping the market?

Current trends feature a steady migration from traditional on‑premise architectures to hybrid cloud and fully web‑based deployments, providing scalability and cost efficiency. AI and deep‑learning algorithms are being embedded within PACS/RIS platforms for automated lesion detection and workflow prioritization. Additionally, consolidation among health systems drives standardized imaging protocols and centralized image repositories, while subscription‑based service models gain traction as providers seek predictable OPEX.

4. COVID-19 Impact on the North America PACS and RIS Market - Pandemic effects and recovery trajectory?

The COVID‑19 pandemic heightened the need for remote image access, prompting rapid adoption of web‑based and cloud‑enabled PACS solutions. Tele‑radiology volumes surged, reinforcing the market’s resilience. Although elective imaging volumes temporarily declined, the subsequent rebound was fueled by pent‑up demand and heightened awareness of digital health capabilities. The recovery trajectory is strong, with continued investment in remote access tools and a focus on building pandemic‑resilient imaging infrastructure.

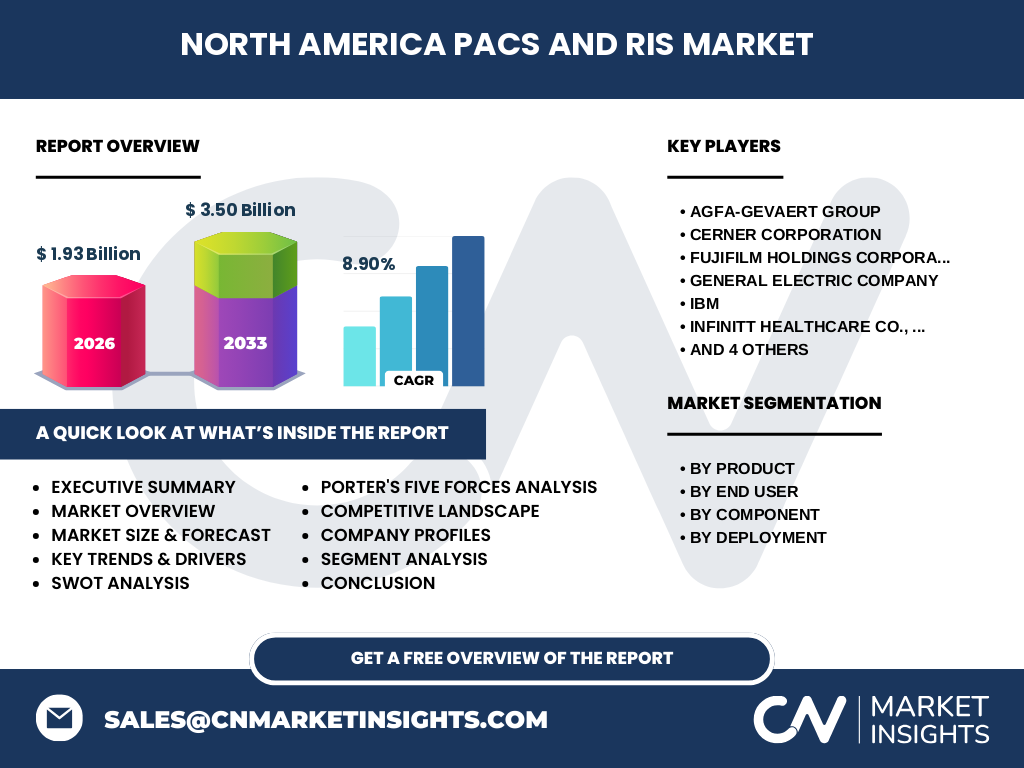

5. North America PACS and RIS Market Competitive Landscape - Major competitors and market consolidation?

The competitive arena is led by Agfa‑Gevaert Group, Cerner Corporation, FUJIFILM Holdings Corporation, General Electric Company, IBM, INFINITT Healthcare Co., Ltd., Koninklijke Philips N.V., McKesson Corporation, Novarad, and Siemens AG. These firms compete on technology integration, AI capabilities, and service offerings. Recent consolidation includes strategic acquisitions to broaden cloud portfolios and enhance AI analytics, strengthening the market position of larger vendors while encouraging niche players to specialize in specific components or verticals.

6. Executive Summary - High-level overview and key findings about North America PACS and RIS Market?

The North America PACS and RIS market is valued at USD 1.93 billion in 2026 and is projected to reach USD 3.50 billion by 2033, reflecting a robust CAGR of 8.90 %. Growth is driven by digital transformation, AI integration, and expanding tele‑radiology services. Cloud‑based and web‑enabled solutions dominate the deployment landscape, while hospitals remain the largest end‑user segment. Competitive dynamics are shaped by ten leading vendors, with ongoing M&A activity and innovation pipelines focused on AI and subscription models. The market is poised for sustained expansion through 2032.

7. North America PACS and RIS Market Forecast - Projections for 2025-2032 period?

Based on the provided CAGR of 8.90 %, the market is expected to continue its upward trajectory from the 2026 baseline of USD 1.93 billion, reaching approximately USD 3.50 billion by 2033. This forecast underlines a steady demand for both hardware upgrades and software‑as‑a‑service solutions, with a notable shift toward cloud and web‑based deployments as organizations prioritize scalability and remote accessibility.

8. North America PACS and RIS Market Size and Share by Segmentation - Breakdown by segment?

Segmentation is structured across product, end‑user, component, and deployment dimensions. The product segment is solely PACS and RIS. End‑users are divided among hospitals, diagnostic centers, and research & academic institutes, with hospitals accounting for the largest share due to high imaging volumes. Component-wise, hardware, software, and services each contribute to overall spend, while deployment splits into web‑based, on‑premise, and cloud‑based solutions, the latter two gaining momentum as providers hybridize their IT environments.

9. Global North America PACS and RIS Market Size and Share by Region - Geographic distribution?

Within the global context, North America represents the primary contributor to PACS and RIS revenue, anchored by the United States' extensive hospital network and Canada’s advancing digital health agenda. While exact regional percentages are not disclosed, the market’s valuation of USD 1.93 billion in 2026 underscores its dominant position relative to other continents.

10. Regional Analysis of the North America PACS and RIS Market - Detailed regional market performance?

In the United States, high‑volume academic medical centers and large integrated delivery networks drive demand for advanced imaging workflows and AI‑enabled analytics. Canada’s market growth is propelled by national health‑system initiatives that prioritize electronic health record integration and cross‑provincial image sharing. Both countries exhibit strong adoption of cloud and hybrid deployment models, supported by robust broadband infrastructure and regulatory frameworks encouraging data interoperability.

11. Leading Company Profiles in the North America PACS and RIS Market - Industry players and strategies?

Agfa‑Gevaert Group focuses on integrated imaging solutions combining PACS, RIS, and AI analytics. Cerner leverages its EHR platform to embed radiology workflows. FUJIFILM offers cloud‑first PACS with advanced visualization tools. GE Healthcare emphasizes hardware robustness and scalable cloud services. IBM integrates cognitive computing for diagnostic assistance. INFINITT specializes in interoperability modules. Philips combines diagnostic imaging hardware with unified software suites. McKesson provides distribution and managed services, while Novarad targets midsize practices with cost‑effective platforms. Siemens AG delivers high‑performance imaging hardware tightly coupled with enterprise‑grade RIS.

12. Porter's Five Forces Analysis of the North America PACS and RIS Market - Competitive forces assessment?

Threat of new entrants is moderate; high capital requirements and regulatory barriers limit newcomers, yet cloud platforms lower entry thresholds. Bargaining power of buyers is strong, as hospitals and health systems can negotiate favorable terms given multiple vendor options. Bargaining power of suppliers is moderate, with component manufacturers (e.g., storage and networking) exerting some influence. Threat of substitutes remains low, because alternative imaging management solutions are limited. Industry rivalry is intense, driven by ten major players investing heavily in AI, cloud, and service models to differentiate their offerings.

13. SWOT Analysis of the North America PACS and RIS Market - Strengths, weaknesses, opportunities, threats?

Strengths: Established demand for digital imaging, high clinical value, and robust funding for health‑IT. Weaknesses: Capital intensity of on‑premise deployments and fragmented legacy systems. Opportunities: Expansion of AI‑driven diagnostics, cloud migration, and subscription‑based services. Threats: Cybersecurity risks, evolving regulatory standards, and potential economic slowdowns affecting capital expenditures.

14. North America PACS and RIS Market Value Chain Analysis - Industry structure and value flow?

The value chain begins with component suppliers (hardware manufacturers, semiconductor vendors, storage providers) followed by system integrators who assemble PACS/RIS platforms. Next are software developers delivering imaging viewers, AI modules, and workflow engines. Service providers add implementation, training, and maintenance. Finally, end‑users—hospitals, diagnostic centers, and academic institutes—consume the solutions, providing feedback that drives iterative product enhancements.

15. Key Investment Insights in the North America PACS and RIS Market - Strategic investment recommendations?

Investors should focus on companies with strong cloud and AI roadmaps, as these areas represent the fastest‑growing revenue streams. Firms that offer flexible subscription models and demonstrate interoperability across EHR ecosystems are positioned for scalable growth. M&A activity presents opportunities to acquire niche technology assets, particularly in AI‑based image analysis and secure data exchange platforms.

16. North America PACS and RIS Market Conclusion - Summary and key takeaways?

The North America PACS and RIS market is on a clear growth trajectory, moving from a USD 1.93 billion base in 2026 to an anticipated USD 3.50 billion by 2033, driven by an 8.90 % CAGR. Digital transformation, AI integration, and cloud adoption are the dominant forces shaping the market. While capital costs and security concerns persist, the opportunity landscape remains vibrant, especially for vendors that can deliver interoperable, subscription‑based, AI‑enabled solutions.

17. Research Methodology - How this research was conducted?

The study combined primary interviews with industry experts, vendor executives, and key end‑users, alongside secondary data from company reports, regulatory filings, and reputable market databases. Trend analysis employed CAGR calculations based on the provided market size (USD 1.93 billion in 2026) and forecast (USD 3.50 billion for 2033). Qualitative assessments such as SWOT, Porter’s Five Forces, and value‑chain mapping were derived from expert insights and documented industry practices.

18. Research Scope - Coverage and limitations?

The scope encompasses the full spectrum of PACS and RIS solutions in North America, covering hardware, software, and services across hospitals, diagnostic centers, and research/academic institutes. It evaluates deployment models (web‑based, on‑premise, cloud) and includes the top ten global vendors active in the region. Limitations are restricted to the use of publicly available data and disclosed market figures; granular market‑share percentages are not provided.

19. Key Companies and Recent Developments in the North America PACS and RIS Market - Introduction to top companies and their recent announcements, product launches, partnerships, and strategic developments?

Agfa‑Gevaert Group announced a partnership with a leading AI firm to embed automated lesion detection into its PACS suite. Cerner released an integrated RIS module within its flagship EHR, enhancing cross‑departmental data flow. FUJIFILM launched a cloud‑first PACS platform with built‑in cybersecurity controls. GE Healthcare introduced a hybrid deployment option combining on‑premise storage with cloud analytics. IBM unveiled a cognitive imaging assistant that leverages Watson for preliminary read suggestions. INFINITT Healthcare expanded its interoperability hub to support HL7 FHIR standards. Philips announced a subscription‑based imaging workflow service targeting midsize hospitals. McKesson rolled out a managed‑service package covering hardware refresh and software updates. Novarad introduced a cost‑effective, web‑based RIS solution for outpatient clinics. Siemens AG released the latest version of its syngo.via platform, integrating AI‑driven quantification tools for cardiovascular imaging.