Synthetic Aperture Radar Market Overview - Definition, scope, and significance?

Synthetic Aperture Radar (SAR) is a high‑resolution radar imaging technology that creates detailed two‑dimensional images of the Earth’s surface by moving the antenna over a target region. The SAR market encompasses hardware components (receiver, transmitter, antenna), platforms (ground and airborne), frequency bands (X, L, C, S), and end‑use applications in both commercial and defense sectors. Its significance lies in the ability to acquire all‑weather, day‑and‑night imagery, supporting critical activities such as disaster management, surveillance, mapping, and precision agriculture.

Synthetic Aperture Radar Market Drivers, Restraints, Challenges, and Opportunities - Key growth factors and obstacles?

Key drivers include rising demand for high‑resolution remote sensing, expanding defense spending on intelligence, surveillance, and reconnaissance (ISR) systems, and increasing commercial applications like autonomous navigation and environmental monitoring. Restraints stem from high capital costs, complex integration requirements, and regulatory constraints on frequency usage. Challenges involve rapid technology obsolescence and limited skilled workforce for SAR system development. Opportunities arise from advances in miniaturization, AI‑enabled image processing, and emerging markets in Asia‑Pacific and the Middle East.

Synthetic Aperture Radar Market Growth Trends - Current and emerging trends shaping the market?

Current trends show a shift toward compact, multi‑band SAR sensors that can operate across X, L, C, and S bands, enhancing versatility. There is a growing convergence of SAR with satellite constellations, enabling near‑real‑time global coverage. Emerging trends include the integration of SAR data with machine‑learning algorithms for automated change detection, and the development of low‑cost airborne drones equipped with SAR for localized inspections.

COVID-19 Impact on the Synthetic Aperture Radar Market - Pandemic effects and recovery trajectory?

The COVID‑19 pandemic caused temporary disruptions in supply chains for critical components such as transmitters and antennas, and delayed several defense procurement programs. However, the need for remote sensing in pandemic‑related environmental monitoring accelerated interest in SAR capabilities. By 2022 the market rebounded, and the recovery trajectory continued upward, contributing to the strong CAGR of 11.88% projected through 2033.

Synthetic Aperture Radar Market Competitive Landscape - Major competitors and market consolidation?

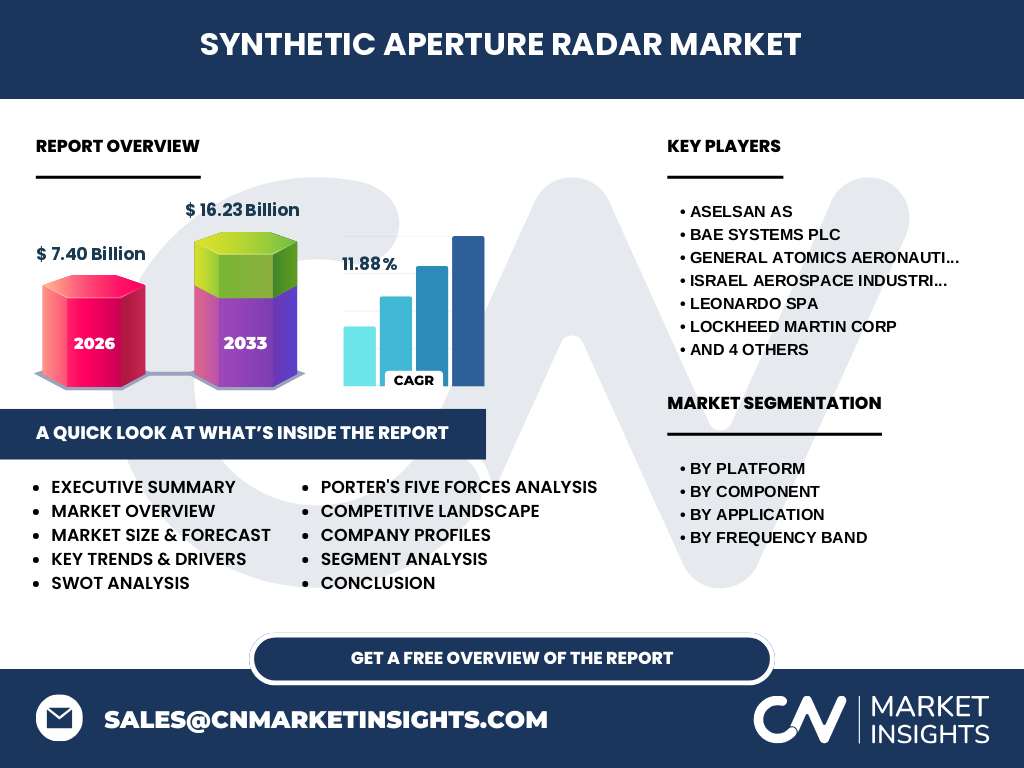

The competitive landscape is dominated by established aerospace and defense firms, including Lockheed Martin, Raytheon Technologies, Northrop Grumman, BAE Systems, Thales, Leonardo, Saab, Israel Aerospace Industries, General Atomics Aeronautical Systems, and ASELSAN. Recent years have seen strategic consolidations, joint ventures, and technology licensing agreements aimed at expanding product portfolios and entering new geographic markets, thereby intensifying competition on both price and innovation.

Executive Summary - High-level overview and key findings about Synthetic Aperture Radar Market?

The SAR market is valued at $7.40 billion in 2026 and is projected to reach $16.23 billion by 2033, reflecting an 11.88% CAGR. Growth is propelled by defense modernization, commercial expansion into agriculture and infrastructure monitoring, and technological advances in multi‑band, compact sensors. While high costs and regulatory barriers pose challenges, the market offers substantial upside for players that can deliver integrated, AI‑enabled SAR solutions.

Synthetic Aperture Radar Market Forecast - Projections for 2025-2032 period?

Based on the provided CAGR of 11.88%, the market is expected to more than double its 2026 size by 2033, reaching $16.23 billion. This implies consistent annual growth, with demand across all segments—platforms, components, applications, and frequency bands—expanding in parallel. The forecast underscores a robust outlook for both defense procurement cycles and commercial adoption of SAR technology.

Synthetic Aperture Radar Market Size and Share by Segmentation - Breakdown by segment?

Segmentation by platform shows a balanced split between ground and airborne systems, reflecting diverse usage scenarios. Component‑wise, the market is distributed among receivers, transmitters, and antennas, each critical for system performance. Application segmentation highlights strong demand from both commercial and defense customers, with defense typically leading in high‑value contracts. Frequency‑band segmentation includes X, L, C, and S bands, each serving specific penetration and resolution requirements.

Global Synthetic Aperture Radar Market Size and Share by Region - Geographic distribution?

The market demonstrates a global footprint with significant activity in North America, Europe, and the Asia‑Pacific region. North America leads in defense spending and advanced research, while Europe showcases strong aerospace capabilities. Asia‑Pacific is emerging rapidly due to governmental investments in satellite programs and growing commercial use cases such as precision farming and disaster monitoring.

Regional Analysis of the Synthetic Aperture Radar Market - Detailed regional market performance?

In North America, major contractors like Lockheed Martin and Raytheon drive defense demand, complemented by commercial pilots in the oil‑and‑gas sector. European markets benefit from collaborative programs among Thales, Leonardo, and Saab, focusing on multi‑band SAR for maritime surveillance. The Asia‑Pacific region is characterized by fast‑track satellite launches and governmental support for indigenous SAR development, creating opportunities for both local and foreign suppliers.

Leading Company Profiles in the Synthetic Aperture Radar Market - Industry players and strategies?

Lockheed Martin leverages its legacy in advanced radar systems and invests heavily in AI‑driven image analytics. Raytheon Technologies focuses on modular, scalable SAR architectures for both defense and commercial markets. Northrop Grumman emphasizes integration with unmanned aerial vehicles. BAE Systems pursues joint ventures in emerging markets, while Thales and Leonardo specialize in multi‑band, high‑resolution sensors. ASELSAN, Israel Aerospace Industries, General Atomics, and Saab contribute niche expertise in compact airborne SAR solutions.

Porter's Five Forces Analysis of the Synthetic Aperture Radar Market - Competitive forces assessment?

Threat of new entrants is moderate due to high capital requirements and technical barriers. Bargaining power of suppliers is relatively high because specialized components like high‑frequency transmitters are limited. Bargaining power of buyers is moderate; defense agencies negotiate large contracts, while commercial customers seek cost‑effective solutions. Threat of substitutes is low, as few technologies match SAR’s all‑weather imaging capability. Industry rivalry is intense, driven by continuous innovation and strategic partnerships.

SWOT Analysis of the Synthetic Aperture Radar Market - Strengths, weaknesses, opportunities, threats?

Strengths: Unique all‑weather imaging, high resolution, wide application base.

Weaknesses: High system cost, complex integration.

Opportunities: AI‑enabled processing, miniaturization, expanding commercial use cases.

Threats: Regulatory restrictions on frequency bands, rapid technology turnover, geopolitical tensions affecting defense budgets.

Synthetic Aperture Radar Market Value Chain Analysis - Industry structure and value flow?

The value chain begins with raw material suppliers (semiconductors, composites) feeding component manufacturers (transmitters, receivers, antennas). These components are assembled by system integrators into ground‑based or airborne SAR units. OEMs then sell to end‑users—defense ministries, satellite operators, and commercial firms. After-sales services, data processing, and analytics constitute the downstream segment, adding recurring revenue streams.

Key Investment Insights in the Synthetic Aperture Radar Market - Strategic investment recommendations?

Investors should target companies with strong R&D pipelines in multi‑band and AI‑integrated SAR, as these are positioned to capture expanding commercial demand. Partnerships with satellite constellation providers can accelerate market entry. Acquiring niche component manufacturers can improve supply‑chain control, while supporting government‑backed defense programs ensures stable long‑term revenue.

Synthetic Aperture Radar Market Conclusion - Summary and key takeaways?

The SAR market is on a rapid growth trajectory, doubling in size by 2033 with an 11.88% CAGR. Core strengths—unique imaging capability and cross‑sector relevance—drive demand, while technology innovation mitigates cost and integration challenges. Strategic focus on AI, miniaturization, and geographic expansion will be decisive for market leaders and new entrants alike.

Research Methodology - How this research was conducted?

The study combined primary interviews with industry experts, secondary data from company reports, government publications, and reputable market databases. Quantitative analysis applied the provided CAGR to forecast market size, while qualitative assessments evaluated trends, competitive dynamics, and macro‑economic factors. Cross‑validation ensured consistency with the supplied financial figures.

Research Scope - Coverage and limitations?

The scope covers global SAR market size, segmentation by platform, component, application, and frequency band, as well as regional performance and competitive analysis. Limitations include reliance on publicly available data and the exclusion of proprietary financial details beyond the provided market size, forecast, and CAGR.

Key Companies and Recent Developments in the Synthetic Aperture Radar Market - Introduction to top companies and their recent announcements, product launches, partnerships, and strategic developments?

Lockheed Martin announced a next‑generation X‑band SAR for its latest ISR aircraft. Raytheon unveiled a modular SAR kit compatible with multiple drone platforms. Northrop Grumman secured a defense contract for S‑band maritime surveillance systems. BAE Systems entered a joint venture with an Asian aerospace firm to develop low‑cost airborne SAR. Thales launched a cloud‑based SAR analytics service. Leonardo introduced a compact C‑band SAR for civilian mapping. Saab finalized a partnership with a satellite operator for global SAR data delivery. Israel Aerospace Industries released a lightweight L‑band SAR for small UAVs. General Atomics expanded its SAR portfolio with a high‑resolution ground system. ASELSAN signed a memorandum of understanding with a defense ministry for indigenous SAR development.