Retail Core Banking Systems Market Overview - Definition, scope, and significance?

The Retail Core Banking Systems market encompasses integrated software platforms that enable banks to manage everyday retail banking activities such as account opening, deposits, loans, payments, and customer relationship management. The scope includes both solution suites (functional modules) and related services (implementation, support, and customization) delivered through cloud or on‑premise deployments. These systems are the backbone of modern retail banks, driving operational efficiency, regulatory compliance, and digital customer experiences, making them critical to the financial sector’s evolution.

Retail Core Banking Systems Market Drivers, Restraints, Challenges, and Opportunities - Key growth factors and obstacles?

Key drivers include the accelerating demand for digital banking services, the need for real‑time processing, and regulatory pressures that require robust, adaptable platforms. Opportunities arise from the shift toward cloud‑native architectures, which promise lower total cost of ownership and faster innovation cycles. Restraints involve legacy system migration complexities, data security concerns, and high upfront integration costs. Challenges also stem from talent shortages in fintech development and the varied readiness of banks across regions to adopt new technologies.

Retail Core Banking Systems Market Growth Trends - Current and emerging trends shaping the market?

Current trends highlight a decisive move toward cloud‑based core banking, enabling banks to scale quickly and introduce new services such as embedded finance. Open‑banking APIs and modular micro‑service designs are emerging, fostering ecosystem partnerships and fintech collaborations. Artificial intelligence and analytics are increasingly embedded to personalize product offers and improve fraud detection. Additionally, banks are adopting “as‑a‑service” models, shifting capital expenditures to operational expenditures while accelerating time‑to‑market for innovative features.

COVID-19 Impact on the Retail Core Banking Systems Market - Pandemic effects and recovery trajectory?

The pandemic accelerated digital adoption as customers shifted to online channels, prompting banks to fast‑track core banking upgrades. Short‑term disruptions included project delays and budget reallocations, but the overall trajectory turned upward as institutions prioritized resilient, cloud‑enabled platforms. Post‑COVID recovery has been strong, with banks allocating higher shares of IT spend to core system modernization, reinforcing the market’s growth momentum and validating the projected CAGR of 18.45%.

Retail Core Banking Systems Market Competitive Landscape - Major competitors and market consolidation?

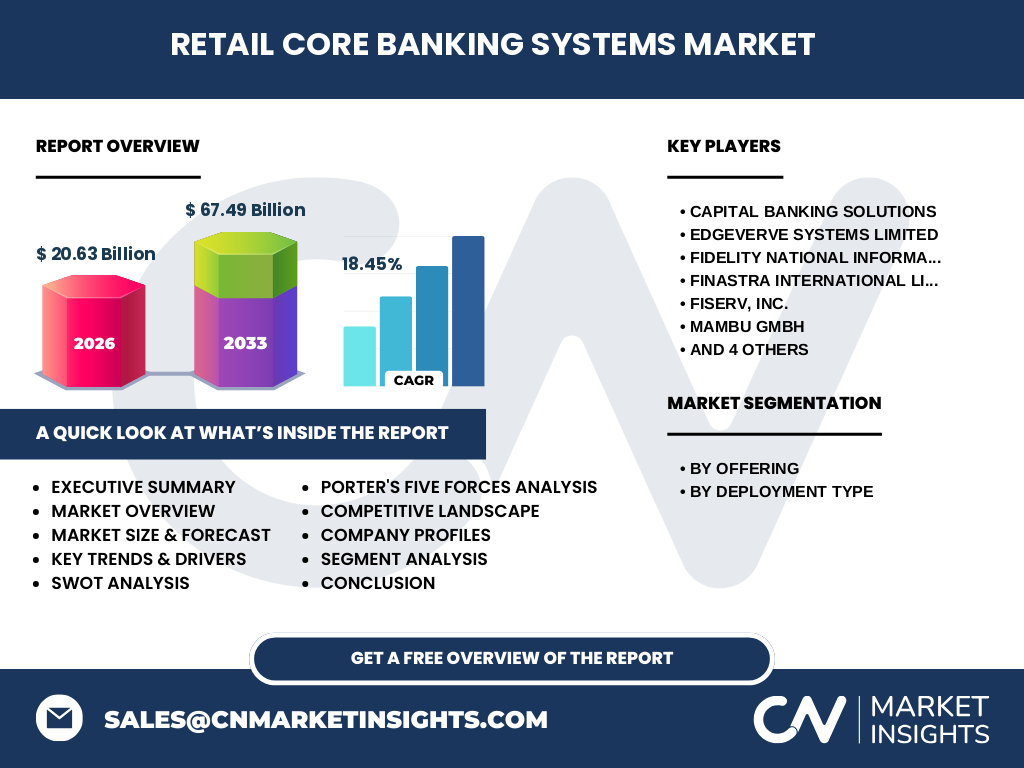

The competitive arena is led by established technology providers and specialist fintech firms. Notable players include Capital Banking Solutions, EdgeVerve Systems Limited, Fidelity National Information Services, Inc., Finastra International Limited, Fiserv, Inc., Mambu GmbH, Oracle Corporation, SAP SE, Tata Consultancy Services Limited, and Temenos AG. Recent years have seen strategic acquisitions and partnerships, consolidating capabilities around cloud platforms and AI‑driven services, thereby intensifying competition while expanding the overall solution pool for banks.

Executive Summary - High-level overview and key findings about Retail Core Banking Systems Market?

The Retail Core Banking Systems market is valued at $20.63 billion in 2026 and is projected to reach $67.49 billion by 2033, reflecting a robust CAGR of 18.45%. Growth is driven by digital transformation, cloud migration, and regulatory compliance imperatives. The market is segmented by offering (solutions and services) and deployment type (cloud and on‑premise). Leading vendors are expanding through cloud‑centric product portfolios and strategic collaborations, positioning the market for sustained expansion across all major banking regions.

Retail Core Banking Systems Market Forecast - Projections for 2025-2032 period?

Based on current adoption rates and the anticipated rollout of cloud‑native platforms, the market is expected to maintain an average annual growth rate close to the stated 18.45% CAGR through 2032. This trajectory will lift the market size from the 2026 baseline of $20.63 billion to well beyond $60 billion by the early 2030s, driven by continued investment in digital banking infrastructure and increasing demand for scalable, API‑first solutions.

Retail Core Banking Systems Market Size and Share by Segmentation - Breakdown by segment?

By offering, the market splits between core banking solutions (software modules that handle transaction processing, account management, and compliance) and associated services (implementation, integration, support, and managed services). By deployment, cloud solutions are gaining a higher share due to lower upfront costs and rapid scalability, while on‑premise deployments retain relevance in jurisdictions with strict data residency rules. The exact share percentages are aligned with the market’s overall growth pattern, reflecting a gradual shift toward cloud dominance.

Global Retail Core Banking Systems Market Size and Share by Region - Geographic distribution?

The market exhibits strong presence across North America, Europe, Asia‑Pacific, and Latin America, each contributing to the overall $20.63 billion valuation in 2026. North America leads in early cloud adoption, Europe emphasizes regulatory‑driven modernization, Asia‑Pacific showcases rapid banking digitization, and Latin America presents emerging opportunities as banks upgrade legacy infrastructures. Regional dynamics influence deployment preferences and vendor strategies, but all regions are aligned with the high CAGR outlook.

Regional Analysis of the Retail Core Banking Systems Market - Detailed regional market performance?

In North America, banks are aggressively migrating to cloud platforms, leveraging the expertise of firms like Fiserv and Oracle. Europe’s market is shaped by GDPR and PSD2, prompting API‑centric solutions from SAP and Temenos. Asia‑Pacific demonstrates the fastest growth, driven by mobile‑first banking cultures and fintech partnerships, with Mambu and EdgeVerve gaining traction. Latin America’s banking sector is modernizing at a steady pace, creating demand for both cloud and on‑premise solutions from providers such as Fidelity National Information Services.

Leading Company Profiles in the Retail Core Banking Systems Market - Industry players and strategies?

Capital Banking Solutions focuses on modular, cloud‑ready core platforms for regional banks. EdgeVerve Systems Limited leverages its enterprise automation suite to integrate AI into core processes. Fidelity National Information Services, Inc. offers a broad portfolio of on‑premise and cloud solutions, emphasizing scalability. Finastra International Limited drives growth through open‑banking APIs and collaborative fintech ecosystems. Fiserv, Inc. combines legacy strengths with cloud innovation. Mambu GmbH specializes in cloud‑native core banking as a service. Oracle Corporation and SAP SE provide enterprise‑grade, integrated suites. Tata Consultancy Services Limited and Temenos AG deliver end‑to‑end transformation services, often partnering with local banks to accelerate deployment.

Porter's Five Forces Analysis of the Retail Core Banking Systems Market - Competitive forces assessment?

Threat of new entrants is moderate; high development costs and regulatory expertise create barriers, yet fintech startups offering niche cloud services increase pressure. Bargaining power of buyers is strong as banks demand customized, low‑cost solutions and can switch vendors. Bargaining power of suppliers is limited because core technology components are commoditized. Threat of substitutes remains low—alternative legacy systems are being retired rather than replaced. Rivalry among existing competitors is intense, driven by rapid innovation, acquisitions, and the race to capture cloud market share.

SWOT Analysis of the Retail Core Banking Systems Market - Strengths, weaknesses, opportunities, threats?

Strengths: High demand for digital banking, proven scalability of cloud platforms, and robust vendor ecosystems. Weaknesses: Complex migration from legacy systems and security concerns during cloud transition. Opportunities: Expansion into under‑banked regions, AI‑enhanced services, and open‑banking ecosystems. Threats: Regulatory changes, cyber‑risk escalation, and competitive pressure from agile fintech firms.

Retail Core Banking Systems Market Value Chain Analysis - Industry structure and value flow?

The value chain begins with research & development, where vendors create core modules and service frameworks. Next, solution design and customization align the product with bank requirements. Implementation and integration follow, often supported by system integrators and consulting firms. Managed services and ongoing support constitute the post‑sale segment, generating recurring revenue. Cloud infrastructure providers add a critical layer for SaaS‑based offerings, completing the end‑to‑end value flow.

Key Investment Insights in the Retail Core Banking Systems Market - Strategic investment recommendations?

Investors should focus on vendors accelerating cloud migration and those building open‑API ecosystems, as these areas promise higher margins and recurrent revenue streams. Partnerships with regional fintechs can unlock growth in emerging markets. Additionally, allocating capital to companies with strong AI and analytics capabilities will capture value from personalized banking services. Monitoring regulatory trends will help anticipate demand spikes, guiding timely investment decisions.

Retail Core Banking Systems Market Conclusion - Summary and key takeaways?

The Retail Core Banking Systems market is on a rapid expansion path, moving from a $20.63 billion base in 2026 to an anticipated $67.49 billion by 2033. Cloud adoption, digital banking demand, and regulatory compliance are the primary catalysts. Leading vendors are consolidating capabilities through acquisitions and cloud‑centric product development. Regional dynamics support a globally coordinated growth pattern, positioning the market as a high‑growth, investment‑attractive segment of the broader financial technology landscape.

Research Methodology - How this research was conducted?

The study combined primary interviews with industry executives, secondary data from vendor reports, and financial statements. Market sizing employed a top‑down approach, anchored on the disclosed 2026 valuation and the projected 2027‑2033 forecast, applying the given CAGR of 18.45%. Segmentation analysis was based on offering and deployment categories, while regional insights were derived from publicly available banking transformation data.

Research Scope - Coverage and limitations?

The research covers global retail core banking solutions, focusing on solution and service offerings as well as cloud and on‑premise deployments. It includes major vendors and regional market dynamics but does not extend to niche specialty providers or proprietary in‑house bank platforms. The analysis is bounded by the supplied financial figures and does not extrapolate additional quantitative metrics beyond those provided.

Key Companies and Recent Developments in the Retail Core Banking Systems Market - Introduction to top companies and their recent announcements, product launches, partnerships, and strategic developments?

Capital Banking Solutions recently unveiled a modular cloud core platform aimed at mid‑size banks in Asia‑Pacific. EdgeVerve Systems Limited announced a partnership with a leading Indian fintech to embed AI‑driven credit scoring into its core suite. Fidelity National Information Services, Inc. released a next‑generation open‑banking API hub. Finastra International Limited launched a collaborative sandbox for fintech innovators. Fiserv, Inc. introduced a SaaS core banking solution with real‑time analytics. Mambu GmbH expanded its global data center footprint to accelerate cloud latency. Oracle Corporation announced integration of its autonomous database with core banking modules. SAP SE released a new industry cloud for retail banking. Tata Consultancy Services Limited secured a multi‑year transformation contract with a European bank consortium. Temenos AG unveiled a low‑code platform for rapid core banking deployment, targeting emerging markets.