1. Embedded Display Market Overview - Definition, scope, and significance?

The Embedded Display Market encompasses thin‑film display technologies that are integrated directly into electronic devices to provide visual output. These displays are “embedded” within the housing of products such as industrial controllers, wearables, fitness machines, and smart home appliances, eliminating the need for separate screens and enabling compact, robust designs. The scope covers all major display technologies—LCD, LED, and OLED—and spans a wide range of applications from industrial automation to consumer wearables. Their significance lies in supporting the growing demand for smarter, connected devices, enhancing user interfaces, and driving the evolution of the Internet of Things (IoT) by providing reliable visual feedback in harsh environments.

2. Embedded Display Market Drivers, Restraints, Challenges, and Opportunities - Key growth factors and obstacles?

Key drivers include the rapid adoption of IoT, increasing automation in manufacturing, and the rising popularity of wearable health monitors that demand low‑power, high‑contrast displays. The transition to edge computing also fuels demand for compact, efficient visual interfaces. Restraints stem from high component cost, especially for OLED and advanced LED modules, and supply‑chain sensitivities for glass substrates and rare‑earth elements. Challenges involve meeting stringent reliability standards for industrial and medical applications, as well as overcoming design integration complexities. Opportunities arise from emerging flexible display formats, advances in low‑temperature poly‑silicon (LTPS) backplanes, and the expansion of AI‑driven UI/UX that require higher resolution and faster response times.

3. Embedded Display Market Growth Trends - Current and emerging trends shaping the market?

Current trends highlight a shift toward higher resolution OLED panels for wearable devices, driven by consumer demand for vivid colors and curved form factors. Meanwhile, LED‑backlit LCDs remain dominant in industrial automation due to their ruggedness and lower cost. Emerging trends include the development of transparent and flexible displays for smart glass and automotive dashboards, and the integration of micro‑LED technology for ultra‑bright, low‑power applications. Additionally, the convergence of display modules with embedded processing (smart displays) is gaining traction, enabling edge AI capabilities directly on the screen.

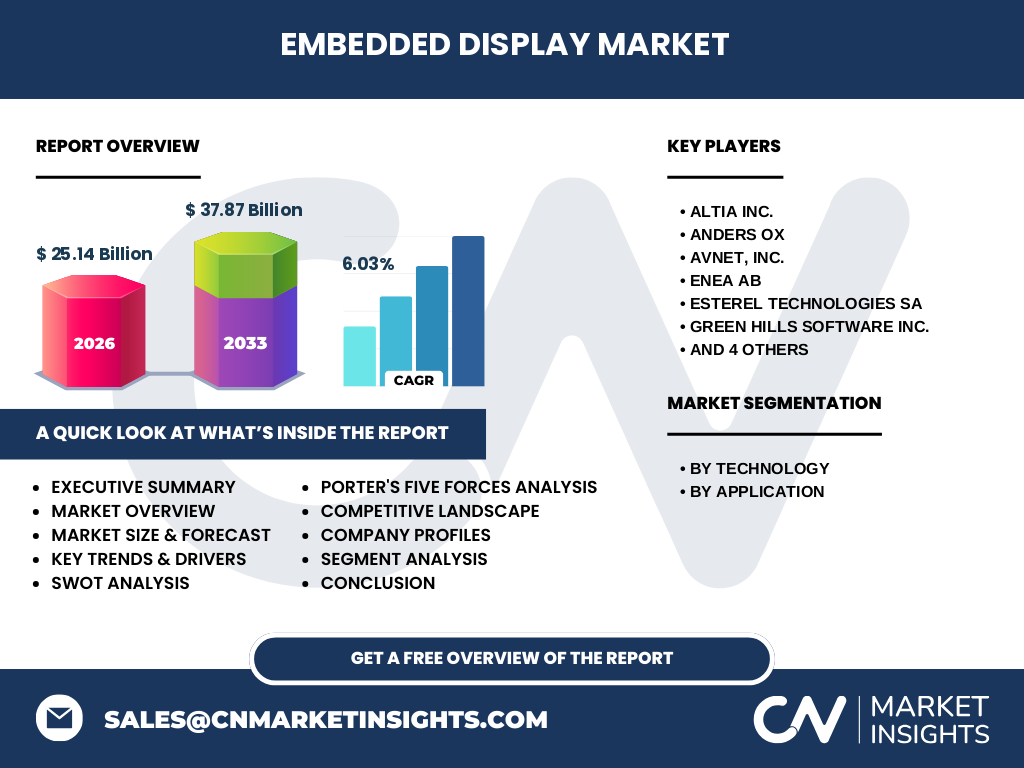

4. COVID-19 Impact on the Embedded Display Market - Pandemic effects and recovery trajectory?

The pandemic initially disrupted supply chains for glass substrates and semiconductor components, causing short‑term inventory shortages. However, the surge in remote work and telehealth accelerated demand for home‑based medical devices and fitness equipment, partially offsetting the slowdown. By late 2021, the market entered a recovery phase, benefitting from resumed factory operations and a rebound in consumer spending on smart appliances. The overall trajectory remains positive, with growth resuming at a pace that aligns with the projected CAGR of 6.03%.

5. Embedded Display Market Competitive Landscape - Major competitors and market consolidation?

The competitive environment is characterized by a mix of specialist display manufacturers and large technology conglomerates. Key players include Altia Inc., Anders OX, Avnet, Inc., ENEA AB, Esterel Technologies SA, Green Hills Software Inc., Intel Corporation, Microsoft Corporation, Multitouch Ltd., and Planar Systems Inc. While traditional display makers focus on panel production, software‑focused firms such as Microsoft and Intel contribute through UI frameworks and embedded operating systems that complement hardware. Recent consolidation activity includes strategic partnerships between hardware suppliers and software providers to deliver turnkey embedded display solutions.

6. Executive Summary - High-level overview and key findings about Embedded Display Market?

The Embedded Display Market is valued at $25.14 billion in 2026 and is forecast to reach $37.87 billion by 2033, reflecting a steady compound annual growth rate of 6.03%. Growth is propelled by IoT expansion, rising automation, and the popularity of wearables. LCD remains the volume leader, while OLED gains share in premium wearables. Regional demand is strongest in North America and Asia‑Pacific, driven by industrial automation and consumer electronics. Competitive dynamics show increased collaboration between hardware and software firms, and emerging technologies such as micro‑LED and flexible displays present significant upside.

7. Embedded Display Market Forecast - Projections for 2025-2032 period?

Based on the provided CAGR of 6.03%, the market is expected to grow from its 2026 baseline of $25.14 billion to approximately $37.87 billion by 2033. This trajectory translates into consistent year‑over‑year growth, with each subsequent year adding roughly $1.6‑$2.0 billion in incremental revenue. The forecast underscores robust demand across all three technology segments, with OLED and micro‑LED showing the highest relative acceleration due to premium applications.

8. Embedded Display Market Size and Share by Segmentation - Breakdown by {segmentData}?

By technology, the market is divided among LCD, LED, and OLED displays. LCD dominates the volume share owing to its mature manufacturing base and cost advantage, especially in industrial automation and home appliances. LED displays hold a strong position in high‑brightness applications such as outdoor kiosks and scientific measurement devices. OLED, while smaller in absolute volume, commands a higher average selling price and is growing fastest in wearables and fitness equipment. By application, industrial automation accounts for the largest usage share, followed by fitness equipment, scientific test and measurement, wearables, and home appliances, reflecting the broad utility of embedded visual interfaces across sectors.

9. Global Embedded Display Market Size and Share by Region - Geographic distribution?

The market exhibits a global footprint with notable strength in North America, Europe, and Asia‑Pacific. North America leads in high‑value OLED and smart‑display integrations, driven by technology firms and consumer wearables. Asia‑Pacific, particularly China, Japan, and South Korea, contributes the largest volume share due to extensive manufacturing capacity and rapid adoption of industrial automation. Europe maintains a steady share, focusing on precision equipment and regulated medical devices.

10. Regional Analysis of the Embedded Display Market - Detailed regional market performance?

In North America, the market benefits from strong R&D investment, a high concentration of AI and edge‑computing firms, and early adoption of wearable health tech. Asia‑Pacific’s growth is powered by large‑scale production of LCD panels, aggressive deployment of smart factories, and burgeoning consumer demand for fitness and home‑automation devices. Europe’s market is characterized by stringent quality standards, fostering demand for reliable displays in scientific and medical instrumentation. Overall, each region’s performance aligns with its industrial maturity, consumer trends, and regulatory environment.

11. Leading Company Profiles in the Embedded Display Market - Industry players and strategies?

Altia Inc. focuses on UI development tools that accelerate embedded display integration. Anders OX supplies high‑performance display modules for automotive and industrial markets. Avnet, Inc. offers extensive distribution networks and design‑in services, bridging component manufacturers with OEMs. ENEA AB provides embedded graphics processors optimized for low‑power display rendering. Esterel Technologies SA delivers model‑based development environments for safety‑critical systems. Green Hills Software Inc. supplies real‑time operating systems that support secure display interfaces. Intel Corporation and Microsoft Corporation contribute platform‑level software stacks and edge‑AI capabilities. Multitouch Ltd. specializes in touch‑screen solutions that complement display hardware, while Planar Systems Inc. manufactures a broad portfolio of LCD and OLED panels for industrial use.

12. Porter's Five Forces Analysis of the Embedded Display Market - Competitive forces assessment?

Threat of New Entrants: Moderate. High capital requirements for panel fabrication create barriers, but software‑centric entrants can gain footholds through development tools. Bargaining Power of Suppliers: High for specialized substrates and rare‑earth materials, influencing cost structures. Bargaining Power of Buyers: Growing, as OEMs consolidate purchasing and demand higher integration levels. Threat of Substitutes: Low to moderate; alternative interfaces like voice or haptic feedback exist but cannot fully replace visual output in many applications. Industry Rivalry: Intense, driven by technology differentiation (LCD vs OLED), price competition, and partnerships that bundle hardware with software ecosystems.

13. SWOT Analysis of the Embedded Display Market - Strengths, weaknesses, opportunities, threats?

Strengths: Mature LCD ecosystem, expanding OLED capabilities, strong demand from IoT and automation. Weaknesses: High cost of premium technologies, complex supply chains, and limited standardization across applications. Opportunities: Flexible and micro‑LED displays, AI‑enabled smart screens, and growth in wearables and medical diagnostics. Threats: Geopolitical trade tensions affecting component supply, rapid technology obsolescence, and potential macro‑economic slowdown impacting capital‑intensive industrial spend.

14. Embedded Display Market Value Chain Analysis - Industry structure and value flow?

The value chain begins with raw material suppliers (glass, substrates, rare‑earth phosphors) feeding panel manufacturers that produce LCD, LED, and OLED modules. These panels are then assembled into embedded display units by OEMs or system integrators, often incorporating touch sensors or custom driver ICs. Software firms provide UI frameworks and embedded operating systems, while distributors such as Avnet add logistics and design‑in services. End‑users—industrial equipment makers, fitness equipment manufacturers, and consumer electronics brands—integrate the displays into final products, completing the chain.

15. Key Investment Insights in the Embedded Display Market - Strategic investment recommendations?

Investors should prioritize companies that combine hardware expertise with software integration, as this synergy enhances value for OEMs seeking turnkey solutions. Funding flexible OLED and micro‑LED development offers high upside given their potential to unlock new form factors. Strategic stakes in supply‑chain entities (substrate producers) can mitigate raw‑material risk. Finally, targeting firms with strong IP in low‑power display drivers aligns with the growing emphasis on battery‑operated wearables and edge devices.

16. Embedded Display Market Conclusion - Summary and key takeaways?

The Embedded Display Market is on a clear growth trajectory, moving from a $25.14 billion base in 2026 to $37.87 billion by 2033, driven by IoT proliferation, automation, and wearable demand. LCD continues to dominate volume, while OLED and emerging micro‑LED technologies capture premium segments. Regional dynamics favor North America’s high‑value applications and Asia‑Pacific’s volume production. Competitive collaboration between hardware and software players is reshaping the landscape, creating ample investment opportunities in both component and solution layers.

17. Research Methodology - How this research was conducted?

The study employed a blend of primary interviews with industry executives, supplier surveys, and secondary data extraction from company filings, market databases, and reputable trade publications. Quantitative analysis used the provided market size ($25.14 billion in 2026) and forecast ($37.87 billion for 2033) to calculate a CAGR of 6.03%, which underpins growth projections. Qualitative assessments—including driver, restraint, and competitive analyses—were derived from expert insights and trend monitoring across technology and application domains.

18. Research Scope - Coverage and limitations?

The scope covers global embedded display technologies (LCD, LED, OLED) and key application segments (industrial automation, fitness equipment, scientific test and measurement, wearables, home appliances). Geographic coverage includes major regions—North America, Europe, and Asia‑Pacific. The research is limited to publicly available information and disclosed company data; proprietary financial details beyond the supplied market figures were not incorporated.

19. Key Companies and Recent Developments in the Embedded Display Market - Introduction to top companies and their recent announcements, product launches, partnerships, and strategic developments?

Altia Inc. announced a new UI development suite optimized for low‑power OLED wearables. Anders OX unveiled a rugged LED display module designed for harsh industrial environments. Avnet, Inc. expanded its design‑in services to include AI‑ready embedded graphics platforms. ENEA AB introduced a next‑generation graphics processor that reduces display latency for scientific instruments. Esterel Technologies SA released a model‑based safety validation tool for medical display systems. Green Hills Software Inc. launched an RTOS update featuring enhanced cryptographic support for secure display interfaces. Intel Corporation partnered with a leading wearable brand to integrate edge‑AI processing directly on OLED panels. Microsoft Corporation rolled out a suite of Azure‑based cloud services tailored for remote monitoring of embedded displays in smart factories. Multitouch Ltd. introduced a flexible touch‑sensor array compatible with curved OLED screens. Planar Systems Inc. announced a high‑brightness LCD panel line targeting outdoor fitness equipment.