What is the Anti-obesity Drugs Market Overview – definition, scope, and significance?

The Anti-obesity Drugs Market comprises pharmaceuticals designed to treat excess body weight and associated metabolic disorders. It covers both prescription and over‑the‑counter (OTC) products, spanning multiple drug classes such as GLP‑1 agonists, lipase inhibitors, and MC4R agonists. Applications range from appetite suppression to inhibition of fat absorption, metabolic enhancement, and combination therapies. Distribution channels include hospital pharmacies, retail pharmacies, and online platforms, while routes of administration are oral and parenteral. The market is significant because obesity is a global health crisis linked to diabetes, cardiovascular disease, and reduced quality of life, driving demand for effective pharmacological interventions.

What are the key drivers, restraints, challenges, and opportunities shaping the Anti-obesity Drugs Market?

Key drivers include rising prevalence of obesity, increasing healthcare spending on chronic disease management, and breakthrough efficacy of GLP‑1 agonists. Regulatory support for novel mechanisms of action and expanding insurance coverage further stimulate growth. Restraints involve high drug acquisition costs, stringent safety requirements, and potential side‑effects that may limit adoption. Challenges arise from market fragmentation, competition from lifestyle‑based interventions, and the need for long‑term efficacy data. Opportunities exist in developing oral GLP‑1 formulations, expanding into emerging markets, and leveraging digital health platforms for adherence monitoring.

What are the current and emerging growth trends in the Anti-obesity Drugs Market?

Current trends highlight a shift toward injectable GLP‑1 agonists with proven weight‑loss outcomes, leading to rapid market expansion. Emerging trends include the pipeline of oral GLP‑1 candidates, integration of combination therapies that target multiple metabolic pathways, and personalized medicine approaches using genetic markers. Additionally, the rise of tele‑pharmacy and direct‑to‑consumer online sales channels is reshaping distribution dynamics, while real‑world evidence studies are supporting broader label expansions.

How has COVID‑19 impacted the Anti-obesity Drugs Market and what is the recovery trajectory?

The COVID‑19 pandemic underscored the vulnerability of obese patients to severe outcomes, prompting heightened clinical focus on weight management. Short‑term disruptions in clinical trials and supply chains delayed some product launches, but telehealth adoption accelerated patient access to prescriptions. Post‑pandemic, demand has rebounded strongly, with health systems prioritizing obesity treatment as part of chronic disease prevention strategies, positioning the market for robust growth.

What does the Competitive Landscape of the Anti-obesity Drugs Market look like?

The market is moderately consolidated, led by multinational innovators such as Novo Nordisk, Eli Lilly, and Roche, alongside strong generic players like Teva and Sun Pharmaceutical. Recent M&A activity reflects strategic consolidation, with larger firms acquiring niche pipelines or distribution networks. Companies differentiate through novel drug classes, extended dosing intervals, and diversified delivery channels, creating a competitive environment focused on efficacy, safety, and patient convenience.

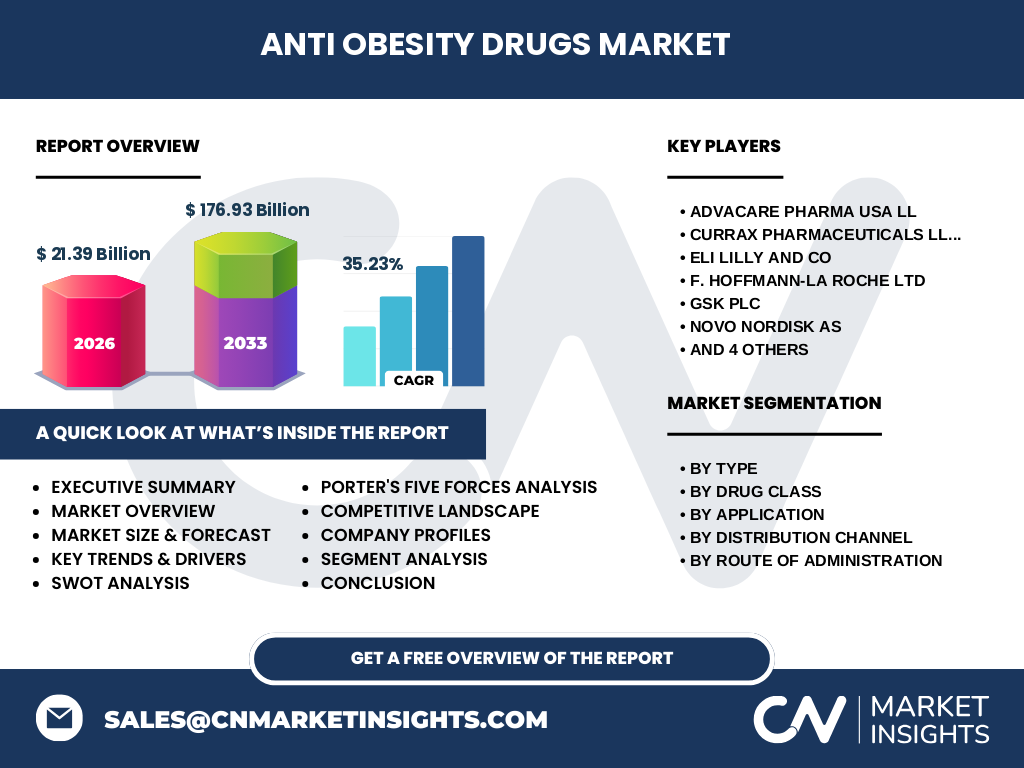

Can you provide an Executive Summary of the Anti-obesity Drugs Market?

The Anti‑obesity Drugs Market is valued at USD 21.39 billion in 2026 and is projected to reach USD 176.93 billion by 2033, reflecting a compound annual growth rate (CAGR) of 35.23 %. Growth is driven by rising obesity prevalence, breakthrough GLP‑1 therapies, and expanding access via digital channels. While high pricing and regulatory scrutiny pose challenges, opportunities abound in oral formulations, emerging markets, and combination regimens. Leading players are consolidating through acquisitions and pipeline investments, positioning the market for sustained expansion.

What are the forecast expectations for the Anti-obesity Drugs Market from 2025 to 2032?

Based on the provided CAGR of 35.23 %, the market is expected to continue accelerating through 2032, with annual revenues increasing substantially each year. The upward trajectory is underpinned by new product approvals, broader insurance reimbursement, and heightened consumer awareness. Forecasts indicate that by 2032 the market will exceed the 2033 projection of USD 176.93 billion, reinforcing its status as a high‑growth therapeutic segment.

How is the Anti-obesity Drugs Market sized and shared by segmentation?

Segmentation by type shows Prescription drugs leading the market, driven by clinically proven efficacy, while OTC products capture price‑sensitive segments. Within drug class, GLP‑1 agonists hold the largest share owing to superior weight‑loss outcomes, followed by Lipase Inhibitors and MC4R agonists. Application‑wise, Appetite Suppression dominates, with Inhibition of Fat Absorption, Metabolic Enhancement, and Combination therapies contributing progressively. Distribution channels are split among Hospital Pharmacies, Retail Pharmacies, and the rapidly growing Online Channel. Oral administration accounts for a growing proportion of sales, while Parenteral routes remain vital for biologics.

What is the Global Anti-obesity Drugs Market size and share by region?

The market exhibits a worldwide footprint, with North America and Europe accounting for a substantial portion due to mature healthcare systems and high obesity rates. The Asia‑Pacific region is emerging as a significant growth engine, driven by expanding middle‑class populations and increasing awareness of obesity‑related risks. Latin America and the Middle East show moderate participation, reflecting growing payer acceptance and regulatory progress.

What are the key findings of the Regional Analysis of the Anti-obesity Drugs Market?

North America leads in absolute revenue, propelled by early adoption of GLGL‑1 therapies and robust reimbursement frameworks. Europe follows closely, with multiple national health services integrating anti‑obesity drugs into standard care pathways. In Asia‑Pacific, China and India present the highest upside due to large patient pools and evolving regulatory landscapes. Latin America’s growth is anchored by Brazil and Mexico, where private insurance drives demand. The Middle East and Africa remain nascent but are expected to benefit from rising urbanization and lifestyle changes.

Which companies are leading in the Anti-obesity Drugs Market and what are their strategies?

Leading firms include Novo Nordisk, Eli Lilly, Roche, GSK, and Sun Pharmaceutical. Novo Nordisk leverages its GLP‑1 platform, expanding dosing options and pursuing oral delivery. Eli Lilly focuses on next‑generation MC4R agonists and strategic partnerships for global distribution. Roche emphasizes combination therapies and biosimilar pathways. GSK invests in lipase inhibitors and digital adherence tools. Sun Pharmaceutical and Teva strengthen their presence through generic launches and market expansion in emerging economies. Each player prioritizes pipeline innovation, geographic diversification, and strategic alliances.

How does Porter’s Five Forces analysis apply to the Anti-obesity Drugs Market?

Threat of new entrants is moderate; high R&D costs and regulatory hurdles limit newcomers, yet biotech startups with novel mechanisms pose occasional risk. Bargaining power of suppliers is low to moderate, as raw material markets are competitive, though specialty biologic components can be concentrated. Bargaining power of buyers is increasing, with payers demanding cost‑effectiveness and outcome‑based contracts. Threat of substitutes includes lifestyle interventions and surgical options, but pharmacotherapy remains unique for patients needing medically managed weight loss. Competitive rivalry is intense, driven by multiple large players launching differentiated agents and pursuing market share through pricing and access strategies.

What are the SWOT elements of the Anti-obesity Drugs Market?

Strengths: Strong clinical efficacy of GLP‑1 agonists, high unmet medical need, and robust pipeline diversity. Weaknesses: High product pricing and potential adverse‑event profiles. Opportunities: Oral GLP‑1 formulations, expansion into emerging markets, and combination regimens. Threats: Stringent regulatory scrutiny, payer cost‑containment measures, and competition from non‑pharmacologic therapies.

What does the Value Chain of the Anti-obesity Drugs Market look like?

The value chain begins with discovery research (academia and biotech), followed by pre‑clinical development and clinical trials conducted by pharmaceutical firms. Regulatory approval processes add a critical validation layer. Manufacturing involves both small‑molecule synthesis and biologics production, with contract manufacturing organizations (CMOs) playing a supportive role. Distribution channels—hospital pharmacies, retail chains, and online platforms—deliver the final product to patients, while post‑market surveillance and real‑world evidence generation close the loop, informing future R&D.

What key investment insights can be derived for the Anti-obesity Drugs Market?

Investors should focus on companies with strong GLP‑1 pipelines, as these drivers underpin the highest growth potential. Strategic acquisitions of niche biotech firms developing oral or combination agents can deliver accelerated market entry. Allocation toward firms expanding digital engagement and adherence technologies offers ancillary upside. Finally, exposure to emerging‑market players can capture the next wave of demand as obesity rates rise globally.

What is the overall conclusion of the Anti-obesity Drugs Market analysis?

The Anti‑obesity Drugs Market is poised for extraordinary expansion, moving from a niche therapeutic area to a mainstream pillar of chronic disease management. Robust clinical data, expanding payer acceptance, and innovative delivery formats are converging to drive a CAGR of 35.23 % and a market size surpassing USD 176 billion by 2033. Companies that invest in pipeline diversification, geographic reach, and patient‑centric solutions will likely dominate the evolving landscape.

What research methodology was employed for this report?

The study combined primary interviews with industry experts, physicians, and payer representatives, alongside secondary analysis of regulatory filings, peer‑reviewed journals, and company financial statements. Market sizing employed top‑down and bottom‑up approaches, triangulating prescription volume data with pricing information. Forecast modeling applied historical growth patterns and the stated CAGR of 35.23 % to project revenues through 2033.

What is the scope of the research and its limitations?

The research covers global anti‑obesity pharmaceuticals across prescription and OTC categories, segmented by drug class, application, distribution channel, and administration route. It includes major geographic regions and the top ten identified companies. Limitations stem from reliance on publicly disclosed data; confidential pipeline details and unpublished trial results are not incorporated.

Which key companies and recent developments are shaping the Anti-obesity Drugs Market?

Key players include AdvaCare Pharma USA, Currax Pharmaceuticals, Eli Lilly, Roche, GSK, Novo Nordisk, Rhythm Pharmaceuticals, Sun Pharmaceutical, Teva, and VIVUS. Recent developments feature Novo Nordisk’s launch of an oral GLP‑1 formulation, Eli Lilly’s partnership with a digital health firm to improve adherence, Roche’s acquisition of a combination‑therapy startup, and Sun Pharmaceutical’s entry into the OTC appetite‑suppression segment. These activities highlight a focus on expanding product portfolios, entering new channels, and leveraging technology to enhance patient outcomes.