What is the Biofertilizers Market Overview – definition, scope, and significance?

The biofertilizers market comprises products that contain living microorganisms which enhance the availability of nutrients to plants. These microorganisms—such as Rhizobium, Azotobacter, and phosphate‑solubilizing bacteria—facilitate biological nitrogen fixation, phosphorus solubilization, and potassium mobilization. The scope of the market spans agricultural applications across major crop categories, including cereals and grains, oil seeds and pulses, and fruits and vegetables. Biofertilizers are significant because they reduce dependence on synthetic chemicals, lower environmental impact, and support sustainable intensification of agriculture, aligning with global goals for soil health and climate‑friendly farming.

What are the main drivers, restraints, challenges, and opportunities in the Biofertilizers Market?

Key drivers include rising awareness of ecological farming, government incentives for organic inputs, and the need to improve soil fertility amid growing food demand. Restraints involve limited awareness among smallholder farmers, variable efficacy due to climate conditions, and higher upfront costs compared with conventional fertilizers. Challenges encompass stringent regulatory approvals for microbial products and the need for robust distribution networks to maintain microbial viability. Opportunities arise from expanding seed‑treatment technologies, integration with digital agriculture platforms, and the development of multifunctional strains that address multiple nutrient deficiencies simultaneously.

What are the current and emerging growth trends shaping the Biofertilizers Market?

Current trends feature the rapid adoption of biofertilizers in seed‑treatment processes, driven by enhanced germination rates and early‑stage vigor. Emerging trends include the formulation of consortia containing nitrogen‑fixing, phosphorus‑solubilizing, and potassium‑mobilizing microorganisms to deliver a holistic nutrient package. Precision agriculture tools are being used to match specific microbial strains with soil microbiome profiles, optimizing performance. Additionally, partnerships between biotech firms and agribusinesses are accelerating product pipelines and market penetration.

How has COVID‑19 impacted the Biofertilizers Market and what is the recovery trajectory?

The COVID‑19 pandemic temporarily disrupted supply chains for raw materials and limited field trials, causing a short‑term slowdown in new product launches. However, the crisis also highlighted the vulnerability of conventional fertilizer supply chains, prompting growers to explore resilient alternatives such as biofertilizers. Post‑pandemic, demand has rebounded strongly, supported by increased government focus on sustainable agriculture and a surge in organic produce consumption. The recovery trajectory is upward, with market confidence restoring to pre‑COVID levels and positioning the sector for accelerated growth.

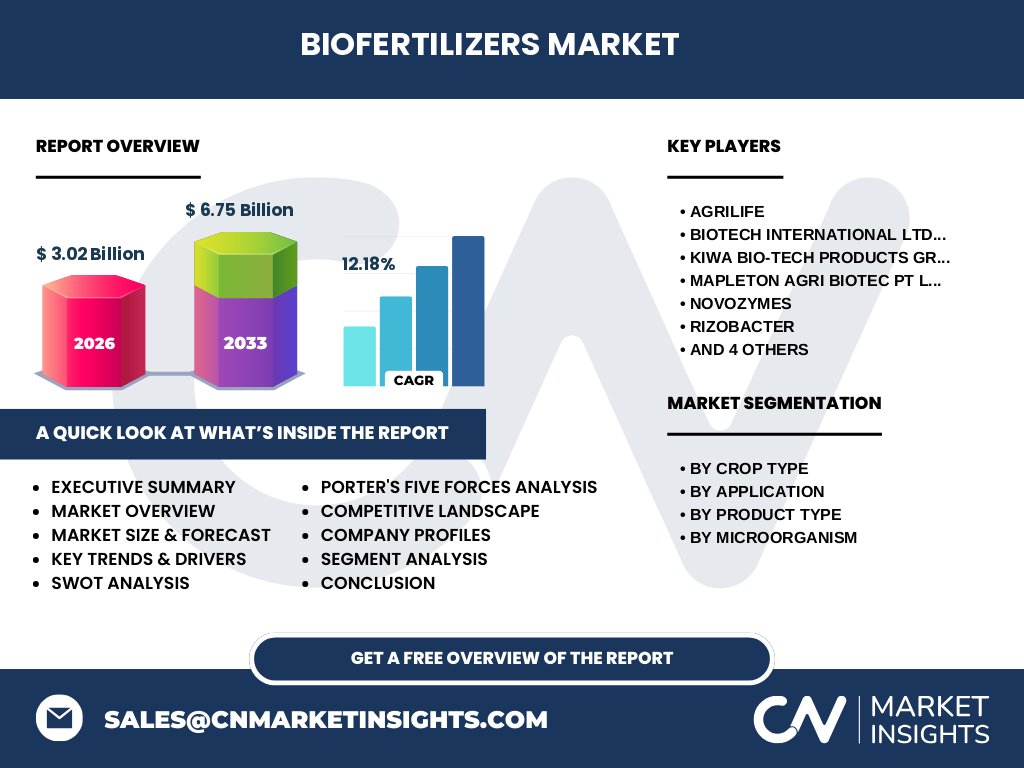

Who are the major competitors and what is the level of consolidation in the Biofertilizers Market?

The competitive landscape includes global leaders such as AgriLife, Biotech International Ltd., Kiwa Bio‑Tech Products Group Corporation, Mapleton Agri Biotec Pt Ltd., Novozymes, RIZOBACTER, Symborg, T. Stanes and Company Limited, UPL, and Vegalab SA. The market remains moderately fragmented, with several specialized firms focusing on niche microbial strains or regional distribution. Recent years have seen strategic alliances and joint ventures rather than large‑scale mergers, indicating a collaborative rather than highly consolidated environment.

What are the high‑level findings in the Executive Summary of the Biofertilizers Market?

The Biofertilizers Market is projected to expand from a 2026 size of USD 3.02 billion to USD 6.75 billion by 2033, representing a robust CAGR of 12.18 %. Growth is propelled by sustainability imperatives, governmental policies, and increasing adoption of seed‑treatment applications. Segmentation shows balanced demand across crop types, with cereals and grains leading, followed by oil seeds and pulses, and fruits and vegetables. Product diversification into nitrogen‑fixing, phosphorus‑solubilizing, and potassium‑mobilizing categories broadens the addressable market. Competitive dynamics are characterized by innovation‑driven players and collaborative partnerships aimed at expanding geographic reach.

What are the forecasts for the Biofertilizers Market for 2025‑2032?

Based on the provided CAGR of 12.18 %, the market is expected to maintain a steady upward trajectory throughout the forecast horizon. By 2032, the market size is anticipated to approach the upper range of the 2027‑2033 projection, reinforcing the sector’s attractiveness for long‑term investment. Growth will be underpinned by expanding applications in seed and soil treatment, intensified product development across microbial categories, and deeper penetration into emerging agricultural regions.

How is the Biofertilizers Market sized and shared by segmentation?

Segmentation by crop type includes cereals and grains, oil seeds and pulses, and fruits and vegetables, reflecting the broad applicability of microbial nutrients across staple and high‑value crops. By application, the market is divided between seed treatment and soil treatment, with seed treatment gaining momentum due to its immediate impact on germination. Product‑type segmentation covers nitrogen‑fixing, phosphorus‑solubilizing, and potassium‑mobilizing biofertilizers, each addressing a critical macro‑nutrient. Finally, microorganism segmentation highlights Rhizobium, Azotobacter, and phosphate‑solubilizing bacteria, the primary strains commercialized for their proven efficacy.

What is the geographic distribution of the Global Biofertilizers Market size and share?

The global market is dispersed across major agricultural regions, with North America, Europe, Asia‑Pacific, and Latin America constituting the primary zones of demand. While specific monetary shares are not disclosed, the trend indicates strong growth in Asia‑Pacific due to large arable land, government subsidies, and expanding organic farming initiatives. Europe and North America contribute significant volumes driven by strict environmental regulations and high adoption of sustainable inputs. Latin America shows emerging potential, particularly in Brazil and Argentina, where large‑scale soybean and corn production align with biofertilizer benefits.

What are the detailed regional analyses of the Biofertilizers Market?

In North America, the market is propelled by research institutions and a mature organic sector, fostering early adoption of seed‑treatment biofertilizers. Europe’s growth is anchored in the EU’s Farm to Fork strategy, encouraging reduced synthetic fertilizer use and supporting biofertilizer innovation. Asia‑Pacific leads in absolute demand, with China, India, and Southeast Asian nations investing heavily in sustainable agriculture programs. Latin America’s market is driven by large‑scale commodity growers seeking cost‑effective alternatives to volatile synthetic fertilizer prices.

Which companies lead the Biofertilizers Market and what strategies are they employing?

Leading firms such as Novozymes and UPL leverage extensive R&D pipelines to develop high‑performance microbial strains and formulate blended products. AgriLife focuses on region‑specific solutions, tailoring formulations to local soil conditions. Biotech International Ltd. and Kiwa Bio‑Tech emphasize strategic partnerships with seed companies to embed biofertilizers in pre‑planting processes. Mapleton Agri Biotec and Symborg pursue market expansion through acquisitions of niche microbial startups, enhancing their product portfolios and geographic coverage.

How does Porter’s Five Forces analysis apply to the Biofertilizers Market?

Threat of new entrants is moderate; entry barriers include scientific expertise and regulatory compliance, yet the growing demand for sustainable inputs attracts startups. Bargaining power of suppliers is low to moderate, as raw microbial cultures are widely sourced, but specialized strains can command higher prices. Bargaining power of buyers is moderate; large agribusinesses can negotiate pricing, while smallholder farmers are price‑sensitive. Threat of substitutes is low; synthetic fertilizers remain alternatives but face regulatory and environmental pressures. Competitive rivalry is high, driven by innovation, product differentiation, and strategic collaborations among numerous active players.

What are the SWOT insights for the Biofertilizers Market?

Strengths: environmental benefits, alignment with sustainability policies, and proven yield improvements. Weaknesses: variable efficacy under diverse climatic conditions and higher upfront costs. Opportunities: integration with digital farming, development of multi‑nutrient consortia, and expansion into emerging markets. Threats: regulatory hurdles, potential competition from next‑generation synthetic fertilizers, and farmer skepticism due to inconsistent field results.

What does the Biofertilizers Market value chain look like?

The value chain begins with research and strain isolation in laboratories, followed by formulation development and pilot testing. Production involves large‑scale microbial fermentation and quality control to ensure viability. Distribution channels include agricultural input dealers, seed companies, and direct sales to large farms. End‑users—farmers and agronomists—apply the products via seed coating or soil amendment, after which feedback loops inform R&D for next‑generation strains, completing the cycle.

What key investment insights can be drawn for the Biofertilizers Market?

Investors should focus on companies with strong R&D pipelines, diversified product portfolios across nitrogen, phosphorus, and potassium biofertilizers, and solid distribution networks. Partnerships with seed manufacturers and agritech platforms enhance market reach. Geographic diversification, especially targeting the high‑growth Asia‑Pacific region, can mitigate regional risk. Monitoring regulatory developments and securing patents for proprietary microbial strains are critical for sustained competitive advantage.

What are the main conclusions of the Biofertilizers Market analysis?

The Biofertilizers Market is on a decisive growth path, underpinned by sustainability imperatives and supportive policy environments. With a projected CAGR of 12.18 % and an estimated market size of USD 6.75 billion by 2033, the sector offers significant commercial opportunities. Success will depend on technological innovation, effective farmer education, and strategic collaborations that bridge the gap between microbial science and practical field application.

How was the research for this Biofertilizers Market report conducted?

The research combined primary interviews with industry experts, secondary data review from reputable agricultural databases, and trend analysis of regulatory publications. Financial projections employed the disclosed CAGR of 12.18 % applied to the baseline 2026 market size of USD 3.02 billion, extending through the 2027‑2033 forecast horizon. Segmentation insights were derived from product catalogs and crop‑usage studies.

What is the scope of this Biofertilizers Market research?

The scope covers global market size, segmentation by crop type, application, product type, and microorganism, as well as regional performance across major agricultural zones. It includes competitive analysis of the top ten listed companies, Porter’s Five Forces, SWOT, value‑chain mapping, and investment recommendations. Limitations are confined to publicly available data; proprietary financial details of individual firms are not disclosed.

Which key companies are highlighted and what recent developments have they announced?

Key companies include AgriLife, Biotech International Ltd., Kiwa Bio‑Tech Products Group Corporation, Mapleton Agri Biotec Pt Ltd., Novozymes, RIZOBACTER, Symborg, T. Stanes and Company Limited, UPL, and Vegalab SA. Recent developments feature Novozymes’ launch of a next‑generation nitrogen‑fixing strain, UPL’s partnership with a major seed producer to embed biofertilizers in certified seed kits, and Symborg’s acquisition of a phosphorous‑solubilizing bacteria startup to broaden its product slate. AgriLife announced field trials in the Midwest demonstrating 8 % yield gains on corn using a Rhizobium‑based seed treatment.