1. What is the definition, scope, and significance of the Asia Pacific Cryogenic Pump Market?

The Asia Pacific Cryogenic Pump Market comprises manufacturers and suppliers of pumps designed to transfer gases at extremely low temperatures, typically below -150 °C. These pumps are essential for handling cryogenic gases such as nitrogen, oxygen, liquefied natural gas (LNG), and argon in industries that require ultra‑pure and temperature‑controlled processes. The market scope includes centrifugal and positive displacement pump types, serving verticals such as electronics, healthcare and pharmaceutical, energy and power, metallurgy, and chemical manufacturing across key Asia Pacific economies. Its significance lies in enabling high‑efficiency gas liquefaction, storage, and distribution, which are critical for emerging clean‑energy projects, semiconductor fabrication, and advanced medical therapies. The rapid industrialisation of China, India, Japan, South Korea, and Southeast Asian nations fuels demand for reliable cryogenic fluid handling, positioning the region as a strategic hub for global cryogenic pump technology.

2. What are the main drivers, restraints, challenges, and opportunities influencing the Asia Pacific Cryogenic Pump Market?

Key growth drivers include rising LNG infrastructure, expanding semiconductor fabs, and increased investment in renewable‑energy storage that require cryogenic gas handling. Government incentives for clean‑energy projects and growing healthcare expenditures further boost demand. Restraints stem from high capital costs of cryogenic systems and stringent safety regulations that can delay project implementation. Challenges involve limited skilled maintenance personnel and the complexity of integrating pumps with existing plant automation. Opportunities arise from the development of energy‑efficient pump designs, digital monitoring solutions, and the emergence of localized manufacturing hubs that can lower logistics costs and improve supply‑chain resilience.

3. Which current and emerging trends are shaping the growth of the Asia Pacific Cryogenic Pump Market?

Current trends feature a shift toward modular pump systems that allow rapid installation and scalability. Manufacturers are increasingly embedding IoT sensors for real‑time performance analytics, predictive maintenance, and remote diagnostics. Emerging trends include the adoption of hydrogen‑compatible cryogenic pumps as the region explores green‑hydrogen production, and the integration of advanced materials such as composites to reduce weight and improve thermal insulation. Collaboration between pump vendors and gas‑processing firms to co‑develop customised solutions is also gaining traction.

4. How did COVID‑19 affect the Asia Pacific Cryogenic Pump Market, and what is the recovery trajectory?

The pandemic caused temporary project postponements, especially in non‑essential sectors like certain chemical plants, leading to a short‑term dip in orders. Supply‑chain disruptions impacted the availability of critical components, extending lead times. However, the market demonstrated resilience as demand from essential sectors—healthcare, energy, and food processing—remained robust. Post‑2022, a steady recovery has been observed, supported by renewed capital spending on LNG terminals and semiconductor expansions. The recovery trajectory is positive, with the market expected to continue its upward momentum as economies normalize and new projects launch.

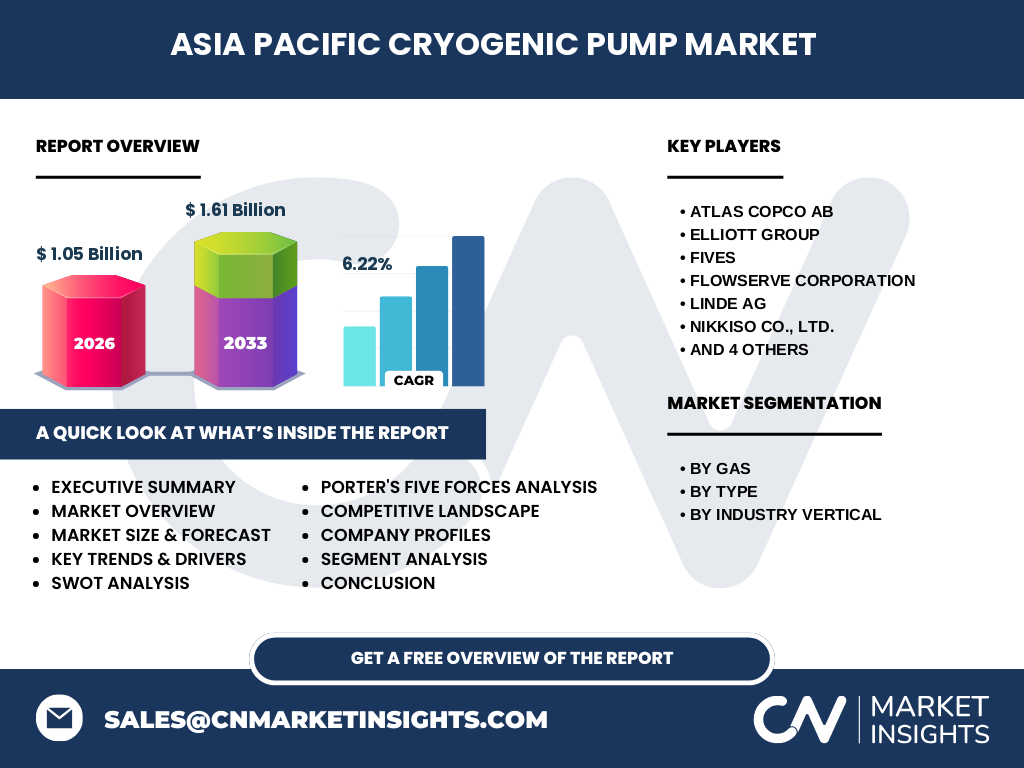

5. Who are the major competitors in the Asia Pacific Cryogenic Pump Market, and what is the level of market consolidation?

The competitive landscape is characterised by a mix of global leaders and strong regional players. Key competitors include Atlas Copco AB, Elliott Group, Fives, Flowserve Corporation, Linde AG, NIKKISO CO., LTD., PHPK Technologies, Ruhrpumpen Group, SEHWA TECH, INC., and Sumitomo Heavy Industries, Ltd. These firms compete on technology innovation, product reliability, and service networks. While the market remains fragmented, recent strategic alliances and joint ventures indicate a moderate level of consolidation, as companies seek to broaden their geographic reach and enhance product portfolios.

6. What are the high‑level findings from the executive summary of the Asia Pacific Cryogenic Pump Market?

The executive summary highlights a market valued at USD 1.05 billion in 2026, with a projected increase to USD 1.61 billion by 2033, reflecting a CAGR of 6.22 % over the forecast period. Growth is driven by expanding LNG infrastructure, semiconductor demand, and healthcare applications. The market benefits from technological advances in pump efficiency and digitalisation, while facing challenges related to cost and regulatory compliance. Competitive intensity is moderate, with several established players reinforcing their positions through innovation and strategic partnerships. The outlook remains strong, underpinned by sustained industrialisation and the region’s commitment to low‑carbon energy solutions.

7. What are the forecast expectations for the Asia Pacific Cryogenic Pump Market from 2025 to 2032?

Based on the provided CAGR of 6.22 %, the market is expected to grow steadily throughout the 2025‑2032 window. By 2027, the market will approach the midpoint of the forecast range, moving toward the USD 1.61 billion target for 2033. This growth will be propelled by ongoing investments in LNG import terminals, the rollout of hydrogen‑fuel projects, and continued expansion of high‑tech manufacturing facilities that rely on cryogenic gases. Seasonal variations in construction activity and policy changes may cause short‑term fluctuations, but the overall trajectory remains upward.

8. How is the Asia Pacific Cryogenic Pump Market sized and shared across its major segments?

The market segmentation can be examined across three dimensions:

By Gas: Nitrogen, oxygen, LNG, and argon each command distinct application niches. Nitrogen dominates in electronics and metal processing, oxygen is critical for healthcare and steelmaking, LNG pumps serve the energy sector, and argon is essential for semiconductor wafer handling.

By Type: Centrifugal pumps are favoured for high‑flow, low‑pressure applications, while positive displacement pumps are chosen for precise metering and high‑pressure requirements.

By Industry Vertical: Electronics, healthcare and pharmaceutical, energy and power, metallurgy, and chemical sectors all utilise cryogenic pumps, with electronics and energy representing the largest consumption due to the volume of gases handled.

While exact monetary shares are not disclosed, the segmentation framework underscores the market’s diversified demand base and informs product‑development focus.

9. What is the geographic distribution of the Asia Pacific Cryogenic Pump Market?

The market spans the broader Asia Pacific region, encompassing major economies such as China, India, Japan, South Korea, and emerging markets in Southeast Asia. These countries collectively host the majority of LNG terminals, semiconductor fabs, and large‑scale chemical complexes that drive pump demand. The distribution reflects a concentration of demand in coastal and industrial corridors where cryogenic gas infrastructure is most developed.

10. How does each sub‑region within Asia Pacific perform in the Cryogenic Pump Market?

East Asia (China, Japan, South Korea): Leads in volume due to extensive semiconductor manufacturing, advanced healthcare facilities, and large LNG import capacity.

South Asia (India, Bangladesh, etc.): Shows rapid growth potential as new petrochemical parks and LNG projects come online, supported by government incentives.

Southeast Asia (Vietnam, Malaysia, Singapore, Indonesia): Benefits from regional gas‑trading hubs and increasing investment in renewable‑energy storage, creating modest but steady demand.

Each sub‑region contributes uniquely, with East Asia providing the bulk of current sales while South and Southeast Asia present high‑growth opportunities.

11. Which companies lead the Asia Pacific Cryogenic Pump Market and what are their key strategies?

Leading firms include Atlas Copco AB, known for its robust centrifugal pump line and extensive service network; Linde AG, leveraging its gas‑production expertise to offer integrated pump‑gas solutions; and Sumitomo Heavy Industries, focusing on high‑precision positive displacement pumps for semiconductor applications. Common strategies involve R&D investment in low‑energy‑consumption designs, expansion of local service centres, and partnerships with OEMs in the energy and electronics sectors to embed pumps within larger system offerings.

12. What does Porter’s Five Forces analysis reveal about the competitive dynamics of the Asia Pacific Cryogenic Pump Market?

Threat of New Entrants: Moderate – high capital requirements and technical expertise create barriers, but niche players can enter through specialised technologies.

Bargaining Power of Suppliers: Low to moderate – a diversified supplier base for raw materials and components reduces dependence on any single source.

Bargaining Power of Buyers: Moderate – large industrial customers negotiate on price and service contracts, yet demand for high‑quality, reliable pumps limits their leverage.

Threat of Substitutes: Low – alternative fluid‑handling equipment cannot match cryogenic temperature performance, keeping substitution limited.

Industry Rivalry: High – numerous established manufacturers compete on technology, service, and price, driving continuous innovation.

13. What are the strengths, weaknesses, opportunities, and threats (SWOT) for the Asia Pacific Cryogenic Pump Market?

Strengths: Advanced manufacturing capabilities, growing industrial base, and strong demand from energy and high‑tech sectors.

Weaknesses: High upfront investment, complex regulatory environment, and scarcity of specialised maintenance talent.

Opportunities: Expansion into hydrogen‑compatible pumps, digital service platforms, and localized production to reduce costs.

Threats: Economic slowdown in key economies, potential trade restrictions, and rapid technology shifts that could render existing designs obsolete.

14. How is value created and transferred throughout the Asia Pacific Cryogenic Pump value chain?

The value chain begins with raw‑material sourcing (high‑grade alloys, composites), proceeds to engineering design and prototype testing, followed by manufacturing (casting, machining, assembly). After production, firms provide installation, commissioning, and after‑sales services such as spare‑part logistics and predictive maintenance. End‑users, principally large industrial complexes, integrate pumps into broader gas‑processing or storage systems, creating value through improved process efficiency and safety. Digital platforms increasingly link manufacturers and customers, enabling remote monitoring and service optimisation.

15. What investment insights can be drawn for stakeholders looking at the Asia Pacific Cryogenic Pump Market?

Investors should consider the market’s steady CAGR of 6.22 % and its exposure to high‑growth sectors like LNG and semiconductor manufacturing. Targeted investments in companies that are digitising their product offerings or expanding local service footprints are likely to yield superior returns. Joint ventures that combine pump technology with gas‑production expertise can accelerate market penetration. Finally, monitoring policy developments around hydrogen and clean‑energy incentives will help identify emerging niches for cryogenic pump applications.

16. What are the key takeaways from the Asia Pacific Cryogenic Pump Market analysis?

The market is on a clear growth path, underpinned by robust industrial demand and a supportive policy environment. Technological innovation—particularly in energy efficiency and digital connectivity—is a critical differentiator. While cost and regulatory hurdles persist, the region’s expanding LNG and high‑tech ecosystems create a fertile ground for continued expansion. Stakeholders should focus on partnerships, localized production, and service excellence to capture market share.

17. How was the research for this report conducted?

The study combined primary interviews with industry experts, technology providers, and end‑user engineers, alongside secondary data review from company reports, government publications, and reputable market databases. Trend analysis employed the provided market size (USD 1.05 billion for 2026) and forecast (USD 1.61 billion for 2033) to calculate the CAGR of 6.22 %. Qualitative insights were triangulated across multiple sources to ensure reliability.

18. What is the scope of this research and its limitations?

The research covers the cryogenic pump market within the Asia Pacific region, focusing on the defined segments (gas type, pump type, and industry vertical). It excludes detailed country‑level financials and does not provide proprietary market‑share percentages beyond the aggregate figures supplied. The analysis is confined to the period 2025‑2033 and does not extend to post‑2033 scenarios.

19. Which key companies are highlighted and what recent developments have they announced?

Highlighted firms include Atlas Copco AB (launch of a new high‑efficiency centrifugal pump series), Elliott Group (strategic partnership with a leading LNG terminal operator), Fives (introduction of IoT‑enabled monitoring for positive displacement pumps), Flowserve Corporation (acquisition of a regional service provider to strengthen after‑sales), Linde AG (integration of cryogenic pumps with its gas‑supply contracts), NIKKISO CO., LTD. (release of an argon‑specific pump for semiconductor fabs), PHPK Technologies (pilot project for hydrogen‑compatible pumps), Ruhrpumpen Group (expansion of a manufacturing facility in Vietnam), SEHWA TECH, INC. (collaboration with a Chinese petrochemical consortium), and Sumitomo Heavy Industries, Ltd. (roll‑out of a digital maintenance platform across its pump portfolio). These initiatives illustrate a market moving toward greater efficiency, digitalisation, and strategic collaboration.