What is the Autonomous Mobile Robots Market Overview – definition, scope, and significance?

The Autonomous Mobile Robots (AMR) market encompasses robotic systems that navigate and operate without fixed guiding infrastructure, using sensors, AI, and advanced software to perform tasks such as material handling, picking, and inventory management. The scope includes hardware platforms (mobility chassis, power systems, manipulators) and the accompanying software, services, and integration solutions that enable deployment across manufacturing, distribution, and warehousing environments. Its significance lies in the ability to boost operational efficiency, reduce labor costs, and enhance safety, positioning AMRs as a cornerstone of Industry 4.0 and the broader automation agenda.

What are the key drivers, restraints, challenges, and opportunities in the Autonomous Mobile Robots Market?

Key drivers include rising labor shortages, the demand for higher warehouse throughput, and the acceleration of digital transformation initiatives. Technological advances in perception, SLAM (simultaneous localization and mapping), and AI analytics further propel adoption. Restraints stem from high upfront capital outlays, integration complexity with legacy systems, and regulatory concerns regarding safety standards. Challenges involve ensuring cybersecurity of connected robots and managing change within workforces resistant to automation. Opportunities arise from expanding use cases beyond traditional logistics—such as collaborative manufacturing, cold‑chain handling, and last‑mile intra‑facility delivery—where AMRs can create new value streams.

What growth trends are currently shaping the Autonomous Mobile Robots Market?

Current trends feature a shift from point‑to‑point conveyor automation toward flexible, fleet‑based AMR solutions that can be reprogrammed on demand. Cloud‑based fleet management platforms are gaining traction, offering real‑time analytics and remote diagnostics. The convergence of 5G connectivity with edge computing enables lower latency decision‑making, supporting more complex navigation in dynamic environments. Additionally, there is a pronounced move toward modular hardware that allows customers to retrofit existing robots with new sensors or payload modules, extending product lifecycles.

How has COVID‑19 impacted the Autonomous Mobile Robots Market and what is the recovery trajectory?

The pandemic highlighted the vulnerability of labor‑intensive supply chains, prompting many firms to accelerate automation projects to maintain operations during workforce disruptions. Short‑term impacts included supply‑chain delays for components, but demand for AMRs surged as companies sought resilience. Recovery is now characterized by a steady increase in capital allocation for automation, with firms prioritizing scalable solutions that can be deployed quickly. The market’s rebound is reinforced by ongoing e‑commerce growth, which sustains the need for higher fulfillment speeds.

Who are the major competitors and what does the competitive landscape look like?

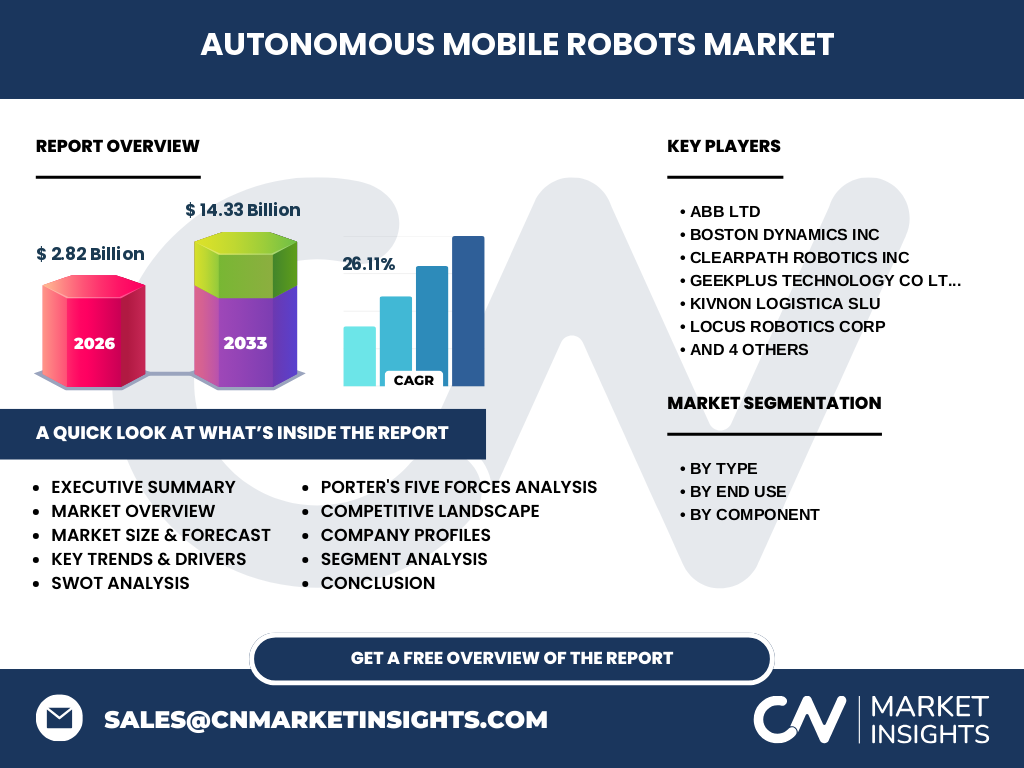

The market is fragmented with several technology‑driven players competing on innovation, ecosystem integration, and service excellence. Leading competitors include ABB Ltd, Boston Dynamics Inc, Clearpath Robotics Inc, Geekplus Technology Co Ltd, Kivnon Logistica SLU, Locus Robotics Corp, Milvus Robotics, Move Robotic Sdn Bhd, OMRON Corp, and Teradyne Inc. Consolidation activity is modest, focusing on strategic partnerships and acquisitions aimed at strengthening AI capabilities and expanding geographic reach rather than outright mergers.

What are the high‑level findings in the Executive Summary?

The Autonomous Mobile Robots market is projected to expand from a 2026 valuation of $2.82 billion to $14.33 billion by 2033, reflecting a robust CAGR of 26.11 %. Growth is driven by labor scarcity, e‑commerce acceleration, and the need for flexible, data‑rich automation. Segmental analysis shows picking robots and self‑driving forklifts leading adoption, while manufacturing and distribution/warehousing dominate end‑use demand. Geographic expansion is steady, with North America and Asia‑Pacific emerging as the largest adopters. The competitive field is innovation‑centric, emphasizing AI, cloud fleet management, and modular hardware.

What are the market forecasts for 2025‑2032?

Based on the provided CAGR of 26.11 %, the market is expected to maintain high‑double‑digit growth through 2032. By 2027 the market will surpass $4 billion, and by 2030 it is anticipated to approach $9 billion, continuing toward the $14.33 billion mark in 2033. This trajectory underscores sustained investment cycles, expanding use cases, and an increasingly price‑competitive ecosystem that lowers barriers for midsize enterprises.

How is the market sized and shared by segmentation?

Segmentation by type highlights three primary categories: Picking Robots, Self‑Driving Forklifts, and Autonomous Inventory Robots. By end use, the market splits between Manufacturing and Distribution & Warehousing. Component-wise, the split is between Hardware and Software & Services. While exact monetary shares are not disclosed, the emphasis on picking robots and self‑driving forklifts reflects their strong alignment with high‑volume pick‑and‑place operations in distribution centers, whereas autonomous inventory robots find niche adoption in inventory audit processes. Software & Services command a growing portion of spend as customers seek analytics, fleet orchestration, and predictive maintenance.

What is the global market size and share by region?

The global AMR market, valued at $2.82 billion in 2026, is distributed across major regions with North America and Asia‑Pacific leading adoption due to mature logistics networks and strong manufacturing bases. Europe follows with notable investments in Industry 4.0 initiatives, while emerging markets in Latin America and the Middle East show early‑stage growth. The combined regional demand underpins the forecasted $14.33 billion valuation by 2033.

What does the regional analysis reveal about market performance?

North America benefits from early technology adoption, robust funding ecosystems, and large e‑commerce volumes, driving rapid fleet deployments. Asia‑Pacific’s growth is propelled by China’s massive manufacturing sector, Japan’s robotics expertise, and Southeast Asia’s rising warehousing capacity. Europe’s performance is shaped by stringent safety regulations and strong collaborations between OEMs and research institutions, fostering advanced safety‑rated AMRs. Each region shows unique regulatory and labor dynamics that influence deployment speed and customization requirements.

Which companies lead the Autonomous Mobile Robots Market and what are their strategies?

ABB Ltd focuses on integrating AMRs with its broader automation portfolio, targeting large‑scale manufacturing plants. Boston Dynamics leverages its high‑mobility platforms to differentiate on agility and payload versatility. Clearpath Robotics emphasizes open‑source software ecosystems to attract developers. Geekplus Technology concentrates on AI‑driven picking solutions for e‑commerce fulfillment. Kivnon Logistica targets self‑driving forklift markets with strong after‑sales service networks. Locus Robotics builds a cloud‑based fleet management platform that reduces onboarding time. Milvus Robotics and Move Robotic prioritize cost‑effective hardware for emerging markets, while OMRON Corp and Teradyne Inc expand through strategic partnerships with system integrators.

How does Porter’s Five Forces analysis apply to the Autonomous Mobile Robots Market?

Threat of new entrants is moderate; high R&D costs and technical expertise create barriers, yet modular platforms lower entry thresholds. Bargaining power of suppliers is moderate to high because critical components such as Lidar and high‑density batteries are sourced from a limited pool of specialists. Bargaining power of buyers is increasing as more OEMs offer comparable solutions, prompting price competition and demand for value‑added services. Threat of substitutes remains low; traditional conveyors lack flexibility, and manual labor is increasingly scarce. Industry rivalry is intense, driven by rapid innovation cycles, patent portfolios, and the race to secure long‑term service contracts.

What are the key strengths, weaknesses, opportunities, and threats in the market (SWOT analysis)?

Strengths: Strong growth drivers, high scalability, and alignment with digital transformation. Weaknesses: Elevated initial investment and integration complexity. Opportunities: Expansion into new verticals (healthcare, retail), development of AI‑powered analytics, and growth of as‑a‑service models. Threats: Cybersecurity vulnerabilities, evolving safety regulations, and potential supply‑chain disruptions for key components.

What does the value chain of the Autonomous Mobile Robots market look like?

The value chain begins with raw material suppliers (metals, batteries, sensors), proceeds to component manufacturers (motors, Lidar, processors), then to system integrators who assemble hardware and embed proprietary software. Next, solution providers offer customization, integration, and training services. Finally, end users operate the robots, supported by aftermarket services such as maintenance, software updates, and data analytics. Cloud service providers increasingly sit alongside the software layer, delivering fleet management and AI analytics as a subscription.

What are the key investment insights for stakeholders?

Investors should focus on companies that combine strong hardware reliability with scalable, subscription‑based software platforms, as this model generates recurring revenue and lowers total cost of ownership for customers. Partnerships that bridge hardware with cloud analytics, as well as firms securing long‑term service contracts in high‑volume logistics hubs, present attractive upside. Monitoring supply‑chain resilience for critical components will be essential for risk mitigation.

What conclusions can be drawn from the Autonomous Mobile Robots market analysis?

The AMR market is on a steep growth trajectory, underpinned by labor market pressures and the digitalization of supply chains. With a projected valuation of $14.33 billion by 2033 and a 26.11 % CAGR, the sector offers compelling opportunities for technology innovators, system integrators, and investors alike. Success will hinge on delivering flexible, data‑rich solutions that integrate seamlessly with existing operations while addressing safety and cybersecurity concerns.

How was the research methodology designed?

The study employed a mixed‑method approach, combining primary interviews with industry experts, OEM executives, and end‑user managers, with secondary data from reputable market reports, company filings, and trade publications. Quantitative projections were derived using compound annual growth rate (CAGR) calculations based on the provided market size figures, while qualitative insights were validated through triangulation across multiple sources.

What is the scope of this research?

The research covers global autonomous mobile robots used in manufacturing, distribution, and warehousing, focusing on hardware, software, and service components. It excludes stationary industrial robots, autonomous vehicles for outdoor logistics, and consumer‑grade robotics. Geographic coverage includes all major regions, with particular emphasis on North America, Europe, and Asia‑Pacific.

Which key companies are highlighted and what recent developments have they announced?

Key players include ABB Ltd, Boston Dynamics Inc, Clearpath Robotics Inc, Geekplus Technology Co Ltd, Kivnon Logistica SLU, Locus Robotics Corp, Milvus Robotics, Move Robotic Sdn Bhd, OMRON Corp, and Teradyne Inc. Recent developments feature Boston Dynamics launching a next‑generation Spot platform with enhanced payload capacity, Locus Robotics expanding its cloud fleet manager to support multi‑site orchestration, Geekplus unveiling an AI‑enhanced picking robot optimized for high‑SKU environments, and ABB announcing a strategic partnership with a major e‑commerce retailer to deploy self‑driving forklifts across its fulfillment network. These initiatives illustrate the market’s focus on AI, cloud integration, and strategic collaborations.