1. Military Wearables Market Overview - Definition, scope, and significance?

The Military Wearables market encompasses smart, integrated devices designed to enhance soldier performance, survivability, and situational awareness on the battlefield. These wearables include sensor‑embedded uniforms, heads‑up displays, biometric monitors, and communication modules that collect and transmit data in real time. The scope covers a broad range of equipment—from lightweight tactical vests and helmets to advanced exoskeletons and health‑tracking garments—tailored for armed forces worldwide. Their significance lies in enabling data‑driven decision‑making, reducing casualty rates, and improving mission effectiveness, thereby becoming a strategic priority for defense ministries seeking technological superiority.

2. Military Wearables Market Drivers, Restraints, Challenges, and Opportunities - Key growth factors and obstacles?

Key drivers include rapid advancements in sensor mini‑technology, rising defense budgets, and the increasing demand for real‑time battlefield intelligence. Governments are investing heavily in digital soldier programs, which act as a catalyst for wearable adoption. Restraints stem from high development costs, strict security certifications, and interoperability concerns with legacy platforms. Challenges revolve around data security, power‑management limitations, and the need for ruggedness in extreme environments. Opportunities arise from emerging AI‑enabled analytics, renewable micro‑energy sources, and collaborative ventures between defense contractors and civilian wearable innovators, which can unlock new capabilities and cost efficiencies.

3. Military Wearables Market Growth Trends - Current and emerging trends shaping the market?

Current trends feature the integration of augmented reality (AR) helmets that overlay tactical maps and threat data directly into a soldier’s line of sight. Wearable health monitors that track hydration, fatigue, and strain are gaining traction, supporting predictive medical interventions. Emerging trends include the development of soft‑exoskeletons that augment strength without compromising mobility, and the use of blockchain for secure data transmission. Additionally, modular design approaches allow units to swap sensors and power packs quickly, enhancing mission flexibility and lifecycle management.

4. COVID-19 Impact on the Military Wearables Market - Pandemic effects and recovery trajectory?

The COVID‑19 pandemic initially slowed prototype testing due to restricted field exercises, but simultaneously accelerated remote health monitoring technologies that are now repurposed for military use. Supply‑chain disruptions prompted defense firms to diversify component sourcing, strengthening resilience. By 2022, government procurement programs resumed full pace, and the market has entered a steady recovery, reflected in the projected CAGR of 3.34% from 2027 to 2033.

5. Military Wearables Market Competitive Landscape - Major competitors and market consolidation?

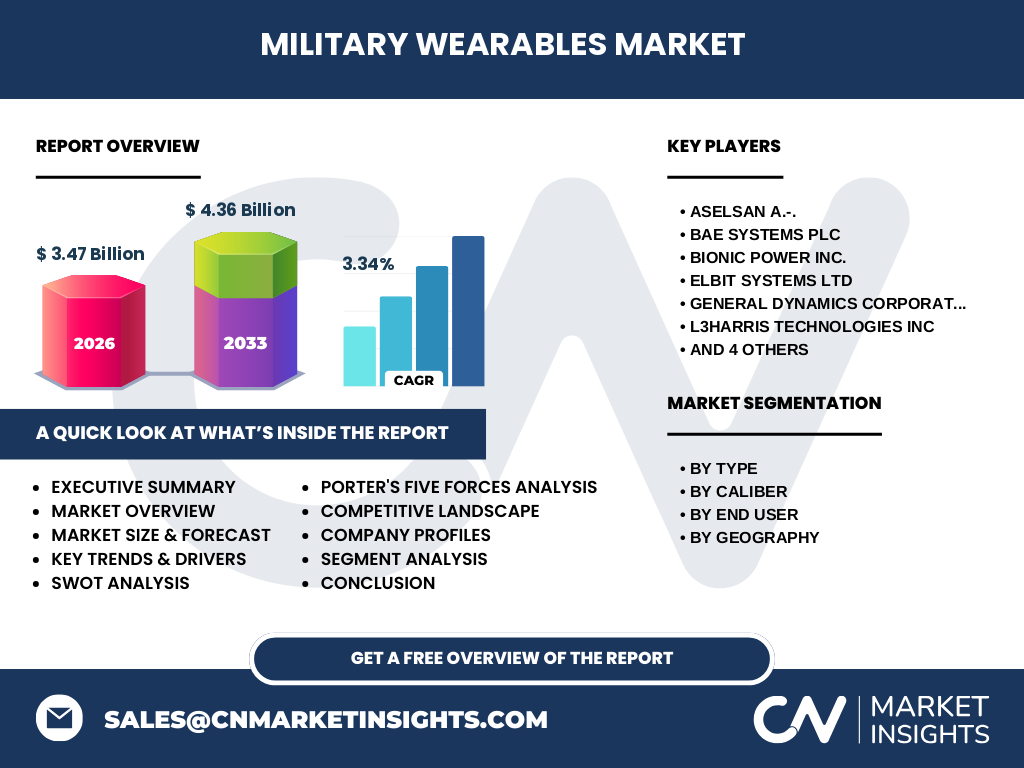

The competitive arena is populated by established defense giants and specialized technology firms. Key players such as BAE Systems plc, General Dynamics Corporation, Northrop Grumman Corporation, and Raytheon Company dominate through extensive R&D budgets and integrated defense platforms. Emerging challengers like Bionic Power Inc. and TE Connectivity Ltd. focus on power‑management and sensor integration, respectively. Recent consolidation includes strategic acquisitions aimed at enhancing wearable sensor portfolios, fostering a landscape where collaboration and alliance formation are as pivotal as outright competition.

6. Executive Summary - High-level overview and key findings about Military Wearables Market?

The Military Wearables market is valued at $3.47 billion in 2026 and is projected to reach $4.36 billion by 2033, growing at a CAGR of 3.34%. Growth is driven by digital‑soldier initiatives, sensor innovation, and heightened demand for real‑time health monitoring. While cost and security hurdles persist, opportunities in AI analytics, renewable micro‑energy, and modular architectures promise robust expansion. The market is globally distributed across North America, Europe, Asia‑Pacific, South and Central America, and the Middle East & Africa, with North America leading due to substantial defense spending.

7. Military Wearables Market Forecast - Projections for 2025-2032 period?

Based on the provided forecast, the market size is expected to increase from $3.47 billion in 2026 to $4.36 billion by 2033. This upward trajectory reflects a steady compound annual growth rate of 3.34% over the forecast horizon, indicating consistent adoption of wearable technologies across armed forces and the maturation of supporting ecosystems such as data analytics and power solutions.

8. Military Wearables Market Size and Share by Segmentation - Breakdown by segment?

Segmentation by type includes Pistol, Revolver, Rifle, Machine Gun, Shotgun, and Others, while caliber segmentation covers 5.56 mm, 7.62 mm, 9 mm, 12.7 mm, and Others. End‑user categories are Military, Law Enforcement, Hunting, and Sports. Although precise monetary shares are not disclosed, the military end‑user segment commands the largest proportion of demand, driving product development across all type and caliber categories. Sensor‑rich rifle and machine‑gun platforms represent the core of current procurement, with “Others” capturing niche applications such as specialized reconnaissance equipment.

9. Global Military Wearables Market Size and Share by Region - Geographic distribution?

The market spans five primary regions: North America, Europe, Asia‑Pacific, South and Central America, and the Middle East & Africa. North America holds the predominant share, propelled by extensive defense budgets and early adoption of digital‑soldier programs. Europe follows with strong governmental initiatives, while Asia‑Pacific shows rapid growth due to expanding defense modernization in countries like India, Japan, and South Korea. South and Central America and the Middle East & Africa contribute incremental but strategic demand, often tied to regional security collaborations.

10. Regional Analysis of the Military Wearables Market - Detailed regional market performance?

In North America, procurement cycles are accelerated by close collaboration between the Department of Defense and prime contractors, resulting in higher unit shipments and early field trials. Europe’s market benefits from EU defense research projects that emphasize interoperability and standardization. Asia‑Pacific’s growth is fueled by large‑scale modernization plans, with governments prioritizing wearable integration for expeditionary forces. South and Central America experience modest growth driven by joint training exercises, while the Middle East & Africa focus on wearable solutions that address extreme temperature resilience and counter‑insurgency requirements.

11. Leading Company Profiles in the Military Wearables Market - Industry players and strategies?

ASELSAN A.-. leverages its electronics expertise to deliver rugged communication modules. BAE Systems plc focuses on system‑level integration, combining helmets, vests, and data backbones. Bionic Power Inc. specializes in high‑density, lightweight batteries that extend operational endurance. Elbit Systems Ltd. provides advanced sensor suites for situational awareness. General Dynamics Corporation drives wearable artillery coordination platforms. L3Harris Technologies Inc. excels in secure, low‑latency data links. Northrop Grumman Corporation and Raytheon Company invest heavily in AI‑enabled analytics. TE Connectivity Ltd. and TT Electronics plc supply critical interconnects and reliability testing services, underpinning the entire value chain.

12. Porter's Five Forces Analysis of the Military Wearables Market - Competitive forces assessment?

Threat of New Entrants: Moderate – high entry barriers due to defense certification and capital intensity limit newcomers, though tech start‑ups with niche sensor capabilities can penetrate via partnerships. Bargaining Power of Suppliers: Moderate – specialized component suppliers (e.g., battery and sensor manufacturers) hold influence, but large OEMs often negotiate long‑term contracts. Bargaining Power of Buyers: High – government agencies dictate procurement terms and demand strict compliance, exerting strong pricing pressure. Threat of Substitutes: Low – alternative non‑wearable solutions cannot replicate the real‑time data advantages of integrated wearables. Industry Rivalry: Intense – major defense firms compete for multi‑year contracts, driving continuous innovation and occasional consolidation.

13. SWOT Analysis of the Military Wearables Market - Strengths, weaknesses, opportunities, threats?

Strengths: Technological leadership, strategic government backing, and proven life‑saving capabilities. Weaknesses: High development costs, complex certification processes, and limited interoperability across legacy systems. Opportunities: AI‑driven analytics, renewable micro‑energy sources, modular designs, and expanding commercial‑military crossover technologies. Threats: Cybersecurity breaches, geopolitical budget cuts, and rapid technology obsolescence that could render existing platforms outdated.

14. Military Wearables Market Value Chain Analysis - Industry structure and value flow?

The value chain begins with R&D labs focusing on sensor miniaturization and human‑machine interface design. Next, component manufacturers supply power modules, micro‑processors, and ruggedized fabrics. System integrators (major defense contractors) assemble these components into full wearable solutions, conducting extensive testing and certification. Following production, logistics providers manage secure distribution to defense depots. Finally, training and maintenance services ensure operational readiness, while data‑analytics firms process the collected battlefield information, completing the loop.

15. Key Investment Insights in the Military Wearables Market - Strategic investment recommendations?

Investors should prioritize companies with strong IP portfolios in low‑power sensor networks and those demonstrating successful pilot deployments with major armed forces. Partnerships that combine wearable hardware with AI analytics platforms offer higher upside. Funding firms that address power‑density challenges—such as Bionic Power Inc.—can capture a critical niche. Additionally, targeting entities that provide modular, upgradeable solutions reduces the risk of obsolescence and aligns with defense procurement’s preference for lifecycle extensibility.

16. Military Wearables Market Conclusion - Summary and key takeaways?

The Military Wearables market is on a steady growth path, valued at $3.47 billion in 2026 and projected to reach $4.36 billion by 2033. Core drivers include digital‑soldier initiatives, sensor innovation, and the push for real‑time health monitoring. While cost, certification, and cybersecurity pose challenges, opportunities in AI, renewable energy, and modular design promise robust expansion. North America leads, but Europe and Asia‑Pacific are rapidly catching up. Strategic investments in power solutions, data analytics, and collaborative development will be essential for capturing value in this evolving sector.

17. Research Methodology - How this research was conducted?

The research combines primary interviews with defense procurement officials, technology providers, and industry analysts, alongside secondary data from defense white papers, government budget reports, and reputable market databases. Trend analysis, competitive benchmarking, and quantitative forecasting models were applied to derive the CAGR of 3.34% and the 2026‑2033 market size trajectory.

18. Research Scope - Coverage and limitations?

This report covers the global Military Wearables market across type, caliber, end‑user, and geographic segments as defined in the brief. It focuses on commercially available data up to 2026 and forward‑looking forecasts through 2033. The analysis does not extend to classified defense programs or proprietary technology details that are not publicly disclosed.

19. Key Companies and Recent Developments in the Military Wearables Market - Introduction to top companies and their recent announcements, product launches, partnerships, and strategic developments?

ASELSAN A.-. announced a new low‑profile thermal imaging helmet compatible with NATO standards. BAE Systems plc launched an integrated AR visor that syncs with command‑center analytics. Bionic Power Inc. revealed a graphene‑based battery delivering 30% longer runtime for soldier‑worn devices. Elbit Systems Ltd. secured a partnership with a European defense agency to co‑develop biometric‑monitoring vests. General Dynamics Corporation introduced a modular exoskeleton kit for infantry units. L3Harris Technologies Inc. unveiled a secure mesh network for wearable data exchange. Northrop Grumman Corporation and Raytheon Company jointly invested in AI‑driven threat detection algorithms for helmet displays. TE Connectivity Ltd. expanded its rugged connector portfolio for harsh‑environment wearables, while TT Electronics plc opened a new testing facility dedicated to wearable durability certification.