1. What is the EV Connector Market and why is it significant?

The EV Connector Market comprises hardware that enables electrical power transfer between electric vehicles (EVs) and charging infrastructure, as well as internal vehicle systems. It spans sealed and unsealed connectors, various voltage classes, and multiple connection types. Its significance lies in supporting the rapid adoption of battery‑electric, plug‑in hybrid, fuel‑cell, and hybrid vehicles, which are central to global decarbonisation and mobility strategies.

2. What are the main drivers, restraints, challenges, and opportunities shaping the EV Connector Market?

Key drivers include rising EV sales, government incentives, and the need for faster, reliable charging solutions. Restraints involve high component costs and stringent safety standards. Challenges stem from heterogeneous connector standards and supply‑chain bottlenecks. Opportunities arise from standardisation efforts, advances in high‑voltage sealed connectors, and integration of connectors with smart diagnostics and over‑the‑air updates.

3. Which growth trends are currently influencing the EV Connector Market?

Current trends feature a shift toward high‑power (medium‑ and high‑voltage) sealed connectors, growing demand for wire‑to‑board designs in compact vehicle architectures, and the incorporation of connectors into vehicle‑to‑grid (V2G) ecosystems. Emerging trends include modular connector platforms that support multiple propulsion types and the use of advanced materials to enhance durability and reduce weight.

4. How did COVID‑19 affect the EV Connector Market and what is the recovery outlook?

The pandemic temporarily slowed production lines and disrupted supply chains, delaying new connector roll‑outs. However, stimulus packages and renewed emphasis on sustainable transport accelerated post‑pandemic recovery. Demand rebounded strongly in 2022, and the market is now on a clear upward trajectory, benefiting from pent‑up demand and accelerated EV adoption plans.

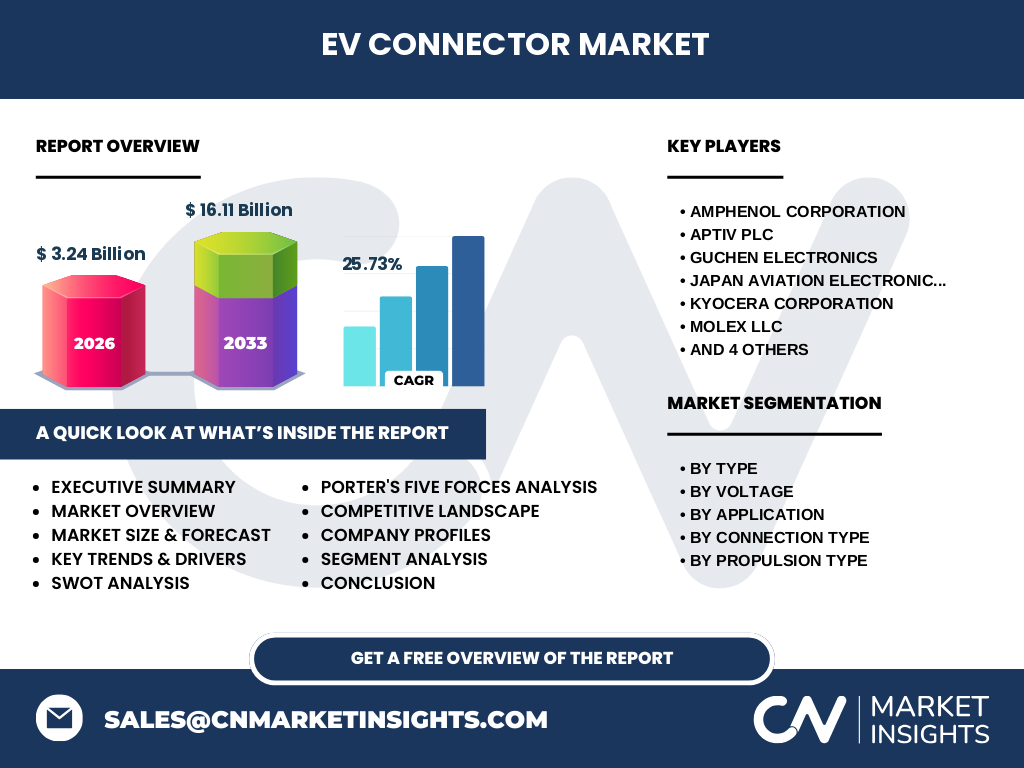

5. Who are the major competitors and what is the state of consolidation in the EV Connector Market?

Leading players include Amphenol Corporation, Aptiv Plc, Guchen Electronics, Japan Aviation Electronics Industry, Ltd., KYOCERA Corporation, Molex LLC, Rosenberger Hochfrequenztechnik GmbH & Co KG, Sumitomo Electric Industries Ltd, TE Connectivity Ltd, and Yazaki Corp. The industry shows moderate consolidation, with strategic acquisitions focused on expanding high‑voltage product portfolios and enhancing geographical reach.

6. What are the key findings highlighted in the Executive Summary?

The market is valued at $3.24 billion in 2026 and is projected to reach $16.11 billion by 2033, reflecting a robust CAGR of 25.73 %. Growth is driven by expanding EV fleets, stricter safety regulations, and the emergence of high‑power charging standards. North America and Asia‑Pacific dominate adoption, while innovation in sealed and high‑voltage connectors offers the greatest upside.

7. What are the forecast expectations for the EV Connector Market from 2025 to 2032?

Based on the projected CAGR of 25.73 %, the market will experience sustained double‑digit growth throughout the 2025‑2032 horizon. Revenues are expected to climb steadily each year, propelled by rising demand for medium‑ and high‑voltage connectors, increased vehicle electrification across all propulsion types, and expanding charging network deployments worldwide.

8. How is the EV Connector Market sized and shared across its segments?

Segmentation covers Type (Sealed vs. Unsealed), Voltage (Low, Medium, High), Application (ADAS, Body Controls, Infotainment, Engine Management, Battery Management, Lighting), Connection Type (Wire‑to‑Wire, Wire‑to‑Board, Board‑to‑Board), and Propulsion Type (BEV, PHEV, FCEV, HEV). While exact monetary shares are undisclosed, sealed connectors and medium‑ to high‑voltage categories are gaining the largest traction due to safety and performance requirements.

9. What is the geographic distribution of the global EV Connector Market?

The market is globally dispersed, with strong concentration in regions investing heavily in EV infrastructure. North America, Europe, and the Asia‑Pacific exhibit the highest demand, reflecting rigorous emission standards and sizable vehicle production bases. Emerging economies in Latin America and the Middle East are beginning to contribute to overall market volume.

10. How does each region perform within the EV Connector Market?

North America leads in premium connector adoption, driven by advanced charging networks and OEM partnerships. Europe emphasizes regulatory compliance and standardisation, fostering growth in sealed high‑voltage solutions. Asia‑Pacific commands the largest manufacturing capacity, benefiting from domestic EV sales and government‑backed electrification programs. Regional nuances influence product focus, with Europe prioritising safety certifications and Asia‑Pacific emphasizing cost‑effective mass production.

11. Which companies are leading the EV Connector Market and what are their strategies?

Amphenol, TE Connectivity, and Molex focus on expanding high‑power sealed connector lines. Aptiv and Yazaki leverage software integration to embed diagnostics within connectors. Sumitomo Electric and KYOCERA pursue material innovation for corrosion resistance. Rosenberger and Guchen target niche board‑to‑board solutions for autonomous vehicle systems. These strategies reflect a blend of product diversification and technological differentiation.

12. How does Porter’s Five Forces model apply to the EV Connector Market?

Threat of New Entrants – moderate, due to high entry barriers like certification and capital intensity. Bargaining Power of Suppliers – relatively low, as many raw‑material sources exist. Bargaining Power of Buyers – high, with OEMs demanding cost‑effective, reliable connectors. Threat of Substitutes – low, because connectors are essential for power transfer. Industry Rivalry – intense, driven by rapid innovation and pricing pressure.

13. What are the SWOT elements for the EV Connector Market?

Strengths: Critical role in EV ecosystem, strong OEM demand. Weaknesses: High R&D costs, complex compliance landscape. Opportunities: Standardisation, V2G integration, growth in high‑voltage segments. Threats: Supply‑chain disruptions, evolving connector standards that could fragment the market.

14. How is the value chain structured for EV connectors?

The value chain begins with raw‑material suppliers (copper, alloys, polymers), proceeds to component design and engineering, then to fabrication (molding, stamping), followed by testing and certification. Distribution channels include Tier‑1 automotive suppliers, direct OEM contracts, and aftermarket distributors. After‑sales services encompass warranty support, firmware updates, and end‑of‑life recycling.

15. What investment insights are most relevant for stakeholders?

Investors should focus on companies expanding high‑voltage sealed connector portfolios and those securing long‑term OEM agreements. Partnerships with charging‑network operators and participation in standard‑setting bodies enhance market positioning. Capital allocation toward material‑science R&D and smart‑connector technologies can yield superior returns given the projected CAGR.

16. What conclusions can be drawn about the EV Connector Market?

The EV Connector Market is on a steep growth path, underpinned by escalating EV adoption and advancing charging standards. Sealed, high‑voltage solutions dominate future demand, while regional dynamics shape product emphasis. Competitive intensity will drive continued innovation, making the sector attractive for strategic investment and partnership opportunities.

17. What methodology was employed to conduct this research?

The study combined primary interviews with industry experts, secondary analysis of company reports, regulatory filings, and reputable market databases. Data triangulation ensured consistency, while trend extrapolation leveraged the provided CAGR of 25.73 % to model forecasts through 2033.

18. What is the scope of this research and its limitations?

The scope covers global EV connector segments by type, voltage, application, connection type, and propulsion type, along with regional performance and competitive analysis. Limitations include reliance on publicly available information and the absence of granular market‑share percentages, which are proprietary.

19. Which key companies have made recent developments in the EV Connector Market?

Amphenol announced a new high‑power sealed connector line for fast‑charging stations. TE Connectivity launched a wire‑to‑board solution with integrated temperature monitoring. Aptiv unveiled a partnership with a leading EV OEM to co‑develop smart connectors for autonomous driving. Yamaha (Yazaki) introduced a modular board‑to‑board platform aimed at battery‑management systems. These initiatives reflect ongoing product innovation and strategic collaborations.