What is the Metal Casting Market Overview – definition, scope, and significance?

The Metal Casting Market comprises the production of metal components by pouring molten metal into molds and allowing it to solidify. It spans a wide range of processes—including sand, investment, and gravity die casting—serving diverse applications such as automotive, aerospace, marine, and industrial machinery. The market is significant because it provides cost‑effective, high‑volume manufacturing of complex geometries, enabling critical sectors to meet performance, weight, and durability requirements.

What are the key drivers, restraints, challenges, and opportunities shaping the Metal Casting Market?

Primary drivers include rising demand for lightweight aluminum and high‑strength steel alloys in automotive and aerospace, and growing infrastructure projects that require durable cast components. Restraints involve stringent environmental regulations on emissions and waste, as well as rising raw‑material costs. Challenges arise from the need for advanced simulation tools and skilled labor shortages. Opportunities are found in additive manufacturing hybridization, recycling of scrap alloys, and the expansion of high‑precision investment casting for electric‑vehicle powertrains.

What are the current and emerging growth trends in the Metal Casting Market?

Current trends feature a shift toward high‑strength aluminum alloys and ductile iron to meet lightweighting goals, and increasing adoption of automation and robotics in foundries to boost productivity. Emerging trends include the integration of Industry 4.0 data analytics for real‑time process optimization, and the use of 3‑D printed molds for rapid prototyping, which reduces lead times and enables customization for niche applications.

How has COVID‑19 impacted the Metal Casting Market and what is the recovery trajectory?

The pandemic caused temporary shutdowns of many foundries, disrupting supply chains and delaying automotive and aerospace projects. However, stimulus‑driven infrastructure spending and a rapid rebound in vehicle production have accelerated recovery. The market’s resilience is reflected in a strong growth outlook, with a projected CAGR of 6.19% through 2032, indicating a robust post‑pandemic expansion.

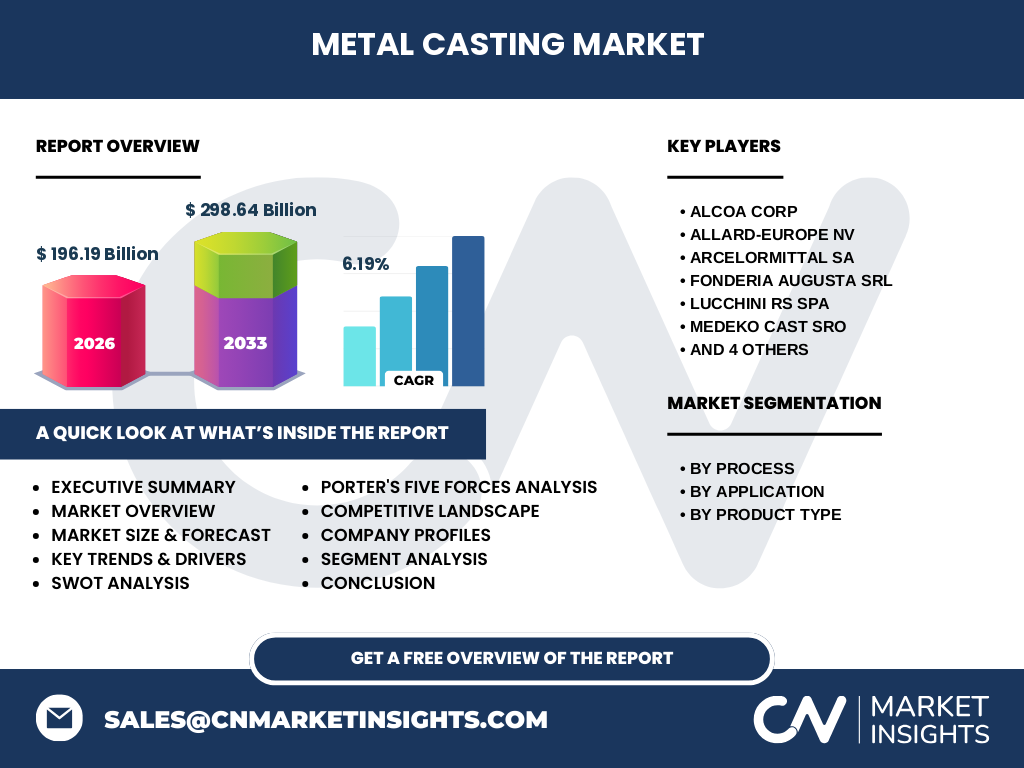

Who are the major competitors in the Metal Casting Market and what is the level of market consolidation?

The competitive landscape is populated by global players such as Alcoa Corp, ArcelorMittal SA, Posco Holdings Inc, and regional specialists like FONDERIA AUGUSTA Srl and MEDEKO CAST Sro. Consolidation is moderate, with strategic acquisitions aimed at expanding capabilities in specific alloy families or geographic regions, while many mid‑size foundries remain independent, focusing on niche process expertise.

What are the key findings highlighted in the Executive Summary of the Metal Casting Market?

The executive summary underscores a market size of $196.19 billion in 2026, projected to reach $298.64 billion by 2033, driven by a 6.19% CAGR. Growth is fueled by automotive lightweighting, aerospace safety standards, and expanding infrastructure. While environmental compliance and raw‑material costs pose challenges, technological adoption and regional demand, especially in emerging economies, provide substantial upside.

What are the forecast expectations for the Metal Casting Market for the 2025‑2032 period?

Forecasts indicate continued expansion, with the market advancing from its 2026 base of $196.19 billion to $298.64 billion by 2033. The 6.19% CAGR reflects sustained demand across automotive, aerospace, and industrial sectors, supported by investments in advanced casting technologies and recycling initiatives. The outlook remains positive despite regulatory pressures, as firms innovate to maintain cost competitiveness.

How is the Metal Casting Market size and share distributed across its segmentation?

By process, sand casting retains the largest share due to its flexibility and low tooling cost, while investment casting captures high‑value aerospace and medical segments, and gravity die casting serves high‑volume automotive parts. Application‑wise, automotive leads, followed by aerospace, industrial machinery, and oil & gas. In product type, aluminum alloys dominate lightweighting trends, carbon steel alloys support heavy‑duty components, and both grey and ductile iron hold steady in casting‑intensive sectors.

What is the global Metal Casting Market size and share by region?

The market is globally distributed, with North America and Europe contributing significant shares through mature automotive and aerospace industries. Asia‑Pacific shows the fastest growth, driven by expanding automotive production, infrastructure development, and increased manufacturing capacity. The Middle East & Africa and Latin America present modest but growing participation, primarily in oil & gas and construction projects.

What does the Regional Analysis reveal about the performance of the Metal Casting Market?

North America benefits from strong demand for high‑performance alloys in aerospace and defense, while Europe focuses on sustainability and recycling initiatives. Asia‑Pacific’s rapid industrialization fuels demand across all casting processes, especially for aluminum and steel alloys in automotive and consumer goods. Emerging markets in Latin America and the Middle East see rising investment in oil & gas infrastructure, driving localized casting activity.

Which leading companies are profiled in the Metal Casting Market and what are their key strategies?

Key profiles include Alcoa Corp’s focus on aluminum alloy innovation, ArcelorMittal’s vertical integration of steel casting, Posco’s expansion of high‑purity steel lines, and Lucchini RS’s specialization in precision steel components. Regional players such as FONDERIA AUGUSTA Srl and MEDEKO CAST Sro emphasize niche process expertise, while companies like RYOBI Aluminium Casting (UK) Ltd leverage advanced die‑casting for consumer products. Strategies revolve around technology upgrades, capacity expansion, and strategic partnerships.

How does Porter’s Five Forces assess the competitive environment of the Metal Casting Market?

Threat of new entrants is moderate due to high capital requirements and regulatory barriers. Supplier power is relatively high because of limited sources for specialty alloys. Buyer power varies; large automotive OEMs exert strong negotiating leverage, while smaller manufacturers have less influence. The threat of substitutes is low, as alternative manufacturing methods cannot match casting’s cost efficiency for complex geometries. Competitive rivalry is intense, driven by price competition and continuous process improvement.

What are the Strengths, Weaknesses, Opportunities, and Threats identified in the SWOT Analysis of the Metal Casting Market?

Strengths: proven cost‑effective production, ability to cast complex shapes, and a broad alloy portfolio. Weaknesses: environmental compliance costs and dependence on volatile raw‑material prices. Opportunities: adoption of digital twins, recycling of scrap alloys, and growth in electric‑vehicle components. Threats: stricter emissions regulations, competition from additive manufacturing for low‑volume high‑precision parts, and geopolitical supply‑chain disruptions.

What does the Value Chain analysis reveal about the Metal Casting Market?

The value chain starts with raw‑material procurement (iron ore, bauxite, alloy additives), followed by melt preparation, mold making (sand, wax, metal), casting, cooling, and finishing processes such as heat treatment and machining. Post‑processing services—including surface coating and inspection—add value, while distribution channels range from direct OEM supply to third‑party distributors. Automation and data analytics are increasingly integrated at each stage to improve efficiency and traceability.

What key investment insights can be drawn for stakeholders in the Metal Casting Market?

Investors should prioritize companies with advanced automation, strong recycling capabilities, and diversified alloy portfolios. Growth capital is attractive in Asia‑Pacific foundries expanding capacity for lightweight aluminum alloys. Strategic acquisitions of niche process specialists can accelerate market entry. Monitoring regulatory trends is essential, as firms that proactively adopt low‑emission technologies are likely to enjoy competitive advantage and stable margins.

What are the concluding remarks and key takeaways from the Metal Casting Market report?

The metal casting sector is poised for robust growth, moving from $196.19 billion in 2026 to $298.64 billion by 2033. Lightweighting, digitalization, and recycling are the primary engines of expansion, while environmental compliance remains a critical focus. Companies that invest in technology, expand in high‑growth regions, and diversify alloy offerings will be best positioned to capture market share.

How was the research methodology designed for this Metal Casting Market study?

The methodology combined primary interviews with industry experts, secondary data from company reports, trade publications, and government sources. Quantitative forecasting employed time‑series analysis anchored on the 2026 market size and the projected CAGR of 6.19%. Segmentation and regional analyses were validated through cross‑referencing multiple data sets to ensure reliability.

What is the scope of the research and any limitations?

The study covers global metal casting activities across all major processes, applications, and alloy types, focusing on the period 2025‑2032. It includes competitive, financial, and technological dimensions. Limitations are limited to publicly available data; proprietary cost structures and confidential R&D details of individual firms are not disclosed.

Which key companies and recent developments are highlighted in the Metal Casting Market?

Recent developments include Alcoa Corp’s launch of a high‑purity aluminum alloy line for electric‑vehicle battery housings, ArcelorMittal’s partnership with automotive OEMs to supply advanced high‑strength steel castings, Posco’s investment in a green hydrogen‑based steel melting facility, and Lucchini RS’s acquisition of a precision die‑casting plant in Central Europe. Additionally, RYOBI Aluminium Casting (UK) Ltd introduced an automated die‑casting system targeting consumer power‑tools, while Tycon Alloy Industries expanded its product range to include specialty aerospace alloys.