1. Europe Aircraft Landing Gear Market Overview - Definition, scope, and significance?

The Europe Aircraft Landing Gear Market encompasses the design, manufacture, supply, maintenance, and overhaul of landing‑gear systems for both commercial and armed‑forces aircraft operating within the European region. Landing gear includes main and nose gear assemblies, tricycle, tandem, and tail‑wheel configurations, and is critical for safe take‑off, landing, and ground handling. The market’s scope covers new equipment for newly delivered airplanes and helicopters, as well as aftermarket services such as repairs, retrofits, and upgrades for legacy fleets. Its significance stems from Europe’s position as a hub for major air‑frame manufacturers, a dense network of airports, and a robust defense aviation sector, all of which generate sustained demand for reliable, high‑performance landing‑gear solutions.

2. Europe Aircraft Landing Gear Market Drivers, Restraints, Challenges, and Opportunities - Key growth factors and obstacles?

Key drivers include a rebound in commercial air travel, ongoing modernization of military fleets, and regulatory pressure for higher safety standards, which together stimulate new‑equipment orders and aftermarket activity. The rise of narrow‑body and wide‑body aircraft programs in Europe also fuels demand for both main and nose gear. Restraints arise from high capital intensity, long product development cycles, and stringent certification requirements that can delay market entry. Challenges involve supply‑chain disruptions, especially for specialised alloys and electronic components, and the need for skilled maintenance personnel. Opportunities are evident in the adoption of lightweight materials, predictive‑maintenance analytics, and the growing retrofit market for older helicopters seeking extended service life.

3. Europe Aircraft Landing Gear Market Growth Trends - Current and emerging trends shaping the market?

Current trends show a shift toward integrated landing‑gear systems that combine mechanical, hydraulic, and electronic functions to improve reliability and reduce weight. Manufacturers are increasingly investing in additive manufacturing for complex gear components, enabling design optimisation and faster prototyping. The aftermarket is seeing a surge in condition‑based maintenance contracts, leveraging sensor data to predict wear and schedule interventions. Additionally, the European defence sector is prioritising modular gear arrangements that can be quickly reconfigured for different mission profiles, creating niche demand for tandem and tail‑wheel setups.

4. COVID-19 Impact on the Europe Aircraft Landing Gear Market - Pandemic effects and recovery trajectory?

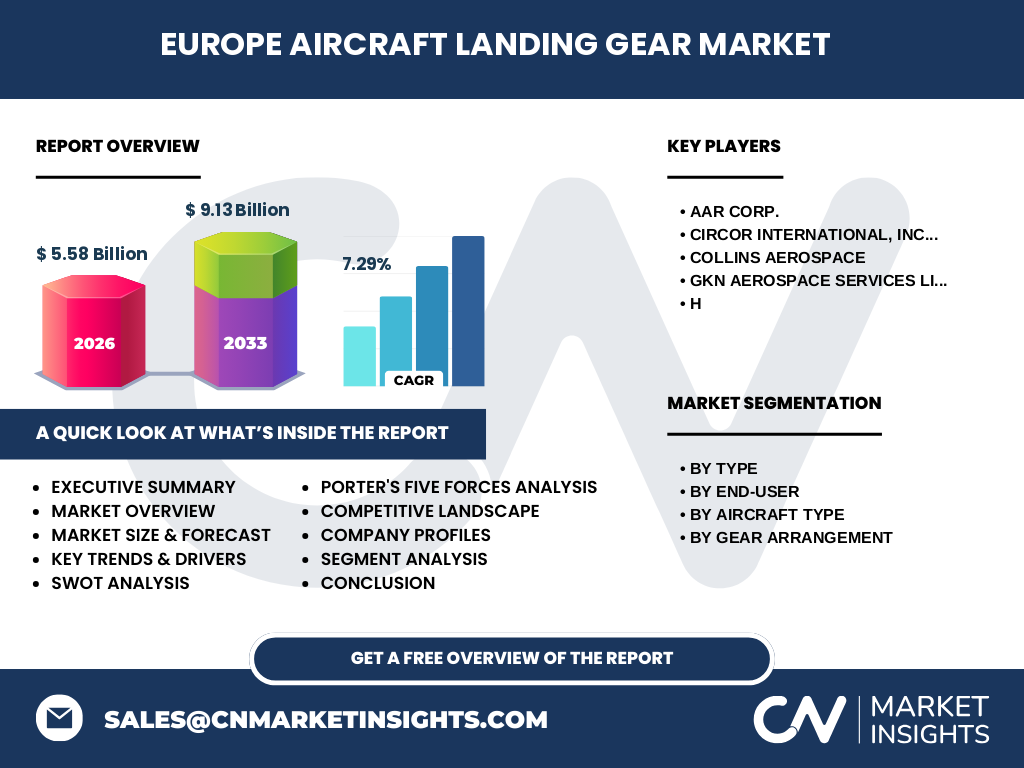

COVID‑19 caused a sharp decline in commercial flight activity, leading to postponed deliveries and reduced new‑gear orders in 2020‑2021. However, the aftermarket proved resilient as airlines and militaries accelerated maintenance programmes to keep existing fleets airworthy. Recovery accelerated in 2022‑2023 as travel demand rebounded, with a notable uptick in retrofitting projects for fuel‑efficiency and environmental compliance. The market is now on a clear recovery trajectory, supported by the forecasted CAGR of 7.29% from 2027 to 2033.

5. Europe Aircraft Landing Gear Market Competitive Landscape - Major competitors and market consolidation?

The competitive landscape is dominated by a mix of global OEMs and specialised suppliers. Key players include AAR Corp., Circor International, Inc., Collins Aerospace, and GKN Aerospace Services Limited. These firms compete on technology leadership, after‑sales support, and strategic partnerships with aircraft manufacturers. Recent years have seen modest consolidation, with larger firms acquiring niche technology providers to broaden their product portfolios and enhance their service networks across Europe.

6. Executive Summary - High-level overview and key findings about Europe Aircraft Landing Gear Market?

The Europe Aircraft Landing Gear Market is projected to grow from a 2026 value of €5.58 billion to €9.13 billion by 2033, reflecting a robust 7.29% CAGR. Growth is driven by renewed commercial demand, defence modernization, and a strong aftermarket supported by predictive‑maintenance trends. Key opportunities lie in lightweight material adoption, additive manufacturing, and digital service models. While high entry barriers and supply‑chain complexities present challenges, the market’s attractive outlook encourages continued investment and innovation.

7. Europe Aircraft Landing Gear Market Forecast - Projections for 2025-2032 period?

Based on the provided forecast, the market is expected to expand steadily, reaching €9.13 billion by 2033. This translates into consistent annual growth, with the market size in 2025 positioned just below the 2026 baseline of €5.58 billion, followed by a compound expansion that maintains the 7.29% CAGR through 2032. The trajectory suggests increasing demand across all segments—type, end‑user, aircraft type, and gear arrangement—especially for main gear solutions in commercial airplanes and modular gear for armed‑forces platforms.

8. Europe Aircraft Landing Gear Market Size and Share by Segmentation - Breakdown by segment?

Segmentation is defined by four dimensions. By type, the market splits into main gear and nose gear, with main gear typically representing the larger share due to its structural complexity. By end‑user, commercial aviation commands the bulk of revenue, while armed forces contribute a growing niche, especially for specialized tandem and tail‑wheel arrangements. By aircraft type, airplanes dominate the market, with helicopters providing a distinct, smaller but technically demanding segment. Finally, gear arrangement is led by tricycle configurations used on most modern airliners, followed by tandem and tail‑wheel setups which are prevalent in military and certain regional aircraft.

9. Global Europe Aircraft Landing Gear Market Size and Share by Region - Geographic distribution?

Within the global context, the Europe region accounts for a substantial portion of total landing‑gear revenue, reflecting the concentration of aircraft manufacturers, defense programs, and high‑traffic airport infrastructure. While precise global share percentages are not disclosed, the European market’s €5.58 billion baseline underscores its role as a core hub for both original equipment manufacturing and aftermarket services.

10. Regional Analysis of the Europe Aircraft Landing Gear Market - Detailed regional market performance?

Regionally, Western Europe—including the United Kingdom, France, Germany, and the Netherlands—drives the majority of market activity, thanks to major OEMs and a dense commercial airline network. Central and Eastern European countries are witnessing incremental growth driven by defence procurement and emerging low‑cost carrier operations. The Nordic region contributes niche demand for rugged landing‑gear suited to harsh climates, particularly for helicopter fleets.

11. Leading Company Profiles in the Europe Aircraft Landing Gear Market - Industry players and strategies?

AAR Corp. focuses on aftermarket support, offering extensive repair, overhaul, and spare‑parts services across Europe. Circor International, Inc. leverages its fluid‑control expertise to supply hydraulic components integral to gear actuation. Collins Aerospace invests heavily in integrated digital landing‑gear solutions, combining sensors and analytics. GKN Aerospace Services Limited emphasizes lightweight composite gear structures and strategic partnerships with European aircraft manufacturers to secure OEM contracts.

12. Porter's Five Forces Analysis of the Europe Aircraft Landing Gear Market - Competitive forces assessment?

Threat of new entrants: Low, due to high capital requirements, certification barriers, and entrenched supplier relationships.

Bargaining power of suppliers: Moderate, as specialised alloy and electronic component suppliers hold some leverage, but large OEMs mitigate risk through long‑term contracts.

Bargaining power of buyers: High for commercial airlines that can negotiate volume discounts, while defence customers have less price flexibility due to specific performance criteria.

Threat of substitutes: Minimal, as landing gear performs a unique safety function with no viable alternatives.

Industry rivalry: Strong, with a few dominant players competing on technology, service quality, and geographic coverage.

13. SWOT Analysis of the Europe Aircraft Landing Gear Market - Strengths, weaknesses, opportunities, threats?

Strengths: Established OEM base, advanced engineering talent, and strong after‑sales infrastructure.

Weaknesses: High production costs, reliance on complex supply chains, and lengthy certification timelines.

Opportunities: Adoption of additive manufacturing, digital twins for predictive maintenance, and expansion into emerging defence contracts.

Threats: Economic downturns affecting airline profitability, geopolitical tensions influencing defence spending, and potential supply disruptions for critical raw materials.

14. Europe Aircraft Landing Gear Market Value Chain Analysis - Industry structure and value flow?

The value chain begins with raw‑material sourcing (high‑strength alloys, composites), followed by component design and engineering, then manufacturing (casting, machining, additive processes). Integration of hydraulics and electronics forms the assembly stage, after which the gear is tested and certified. Distribution occurs through OEM contracts or direct sales to airlines and defence agencies. The aftermarket—maintenance, repair, overhaul (MRO), and spare‑parts logistics—adds significant recurring value, often exceeding the original equipment margin.

15. Key Investment Insights in the Europe Aircraft Landing Gear Market - Strategic investment recommendations?

Investors should target companies with strong MRO capabilities, as aftermarket services generate stable cash flows. Technologies enabling weight reduction—such as carbon‑fibre composites and 3D‑printed metal parts—offer differentiation and align with sustainability goals. Partnerships with European defence ministries provide a hedge against commercial cyclicality. Finally, digital platforms for condition‑based monitoring represent a high‑growth, high‑margin avenue for future expansion.

16. Europe Aircraft Landing Gear Market Conclusion - Summary and key takeaways?

The market is on a clear upward trajectory, moving from a €5.58 billion base in 2026 to €9.13 billion by 2033, driven by a 7.29% CAGR. Robust demand from commercial airlines, ongoing defence modernization, and a vibrant aftermarket underpin this growth. Innovation in lightweight materials, additive manufacturing, and digital maintenance will shape competitive advantage. While supply‑chain and regulatory challenges persist, the overall outlook remains strongly positive for stakeholders.

17. Research Methodology - How this research was conducted?

The study combined primary interviews with industry executives, OEM engineers, and MRO service managers, alongside secondary data from company reports, regulatory filings, and reputable aerospace databases. Market sizing employed a bottom‑up approach, aggregating unit shipment forecasts with average selling prices, while growth rates were validated through triangulation with historical performance and expert opinion.

18. Research Scope - Coverage and limitations?

The scope covers the European region, addressing all landing‑gear types (main, nose), end‑users (commercial, armed forces), aircraft categories (airplanes, helicopters), and gear arrangements (tricycle, tandem, tail‑wheel). The analysis excludes unrelated aerospace components and focuses solely on the financial figures and segments provided. Forecasts extend to 2033, reflecting current market dynamics without speculative macro‑economic scenarios.

19. Key Companies and Recent Developments in the Europe Aircraft Landing Gear Market - Introduction to top companies and their recent announcements, product launches, partnerships, and strategic developments?

AAR Corp. recently expanded its European MRO network with a new facility in Poland, enhancing rapid‑turnaround services for main‑gear components.

Circor International, Inc. launched an advanced hydraulic actuator series designed for next‑generation narrow‑body aircraft, emphasizing energy efficiency.

Collins Aerospace announced a partnership with a leading European airline to pilot a sensor‑based predictive‑maintenance platform across its fleet’s landing‑gear systems.

GKN Aerospace Services Limited unveiled a carbon‑fibre reinforced nose‑gear prototype that reduces weight by 12% while meeting stringent safety standards, positioning the firm for upcoming OEM contracts.