1. What is the Construction Equipment Market Overview – definition, scope, and significance?

The Construction Equipment Market encompasses the design, manufacture, distribution, and servicing of machines and tools used in building, civil engineering, and mining projects. Scope includes heavy construction vehicles, earthmoving equipment, and material handling equipment deployed across residential, commercial, and industrial applications. Its significance lies in enabling infrastructure development, urbanization, and economic growth; equipment availability directly influences project timelines, cost efficiency, and safety standards worldwide.

2. What are the Construction Equipment Market Drivers, Restraints, Challenges, and Opportunities?

Key drivers are robust global infrastructure spending, rapid urbanization in emerging economies, and the adoption of automation and telematics that boost productivity. Restraints include high capital intensity, volatile raw‑material prices, and stringent emissions regulations that increase compliance costs. Challenges stem from supply‑chain disruptions, skilled‑labor shortages, and the need for rapid technology integration. Opportunities arise from the shift toward electric and hybrid equipment, growth of modular construction, and expanding aftermarket services such as predictive maintenance and equipment‑as‑a‑service models.

3. What Construction Equipment Market Growth Trends are currently shaping the industry?

Current trends feature a strong move toward digitalization, with IoT sensors and fleet‑management platforms delivering real‑time performance data. manufacturers are expanding product lines to include autonomous earthmoving machines and remote‑operated cranes. Sustainability drives the development of low‑emission engines and electric power‑train prototypes. Additionally, the rise of prefabricated building methods is increasing demand for material‑handling equipment that can operate in confined, high‑velocity sites.

4. How has COVID‑19 impacted the Construction Equipment Market and what is the recovery trajectory?

The pandemic caused an initial dip in equipment orders due to project delays, restricted labor mobility, and financing pauses. However, stimulus packages targeting infrastructure revitalization accelerated a rebound in 2021–2022. Recovery is evident in renewed procurement activity, especially for residential and commercial projects aiming to meet post‑pandemic housing demand. The market is now on a clear upward path, supported by accelerated digital adoption that mitigated many pandemic‑related operational constraints.

5. What does the Construction Equipment Market Competitive Landscape look like?

The market is characterized by a few dominant global OEMs and a high degree of consolidation through strategic acquisitions and joint ventures. Major competitors—AB Volvo, CNH Industrial, Caterpillar, Deere & Company, Hitachi Construction Machinery, JCB, Komatsu, Liebherr, Terex, and Zoomlion—control a large share of the heavy‑vehicle and earthmoving segments. Competition focuses on technology leadership, after‑sales service networks, and geographic reach. Recent consolidation includes partnerships to co‑develop electric platforms and regional alliances to strengthen distribution in high‑growth markets.

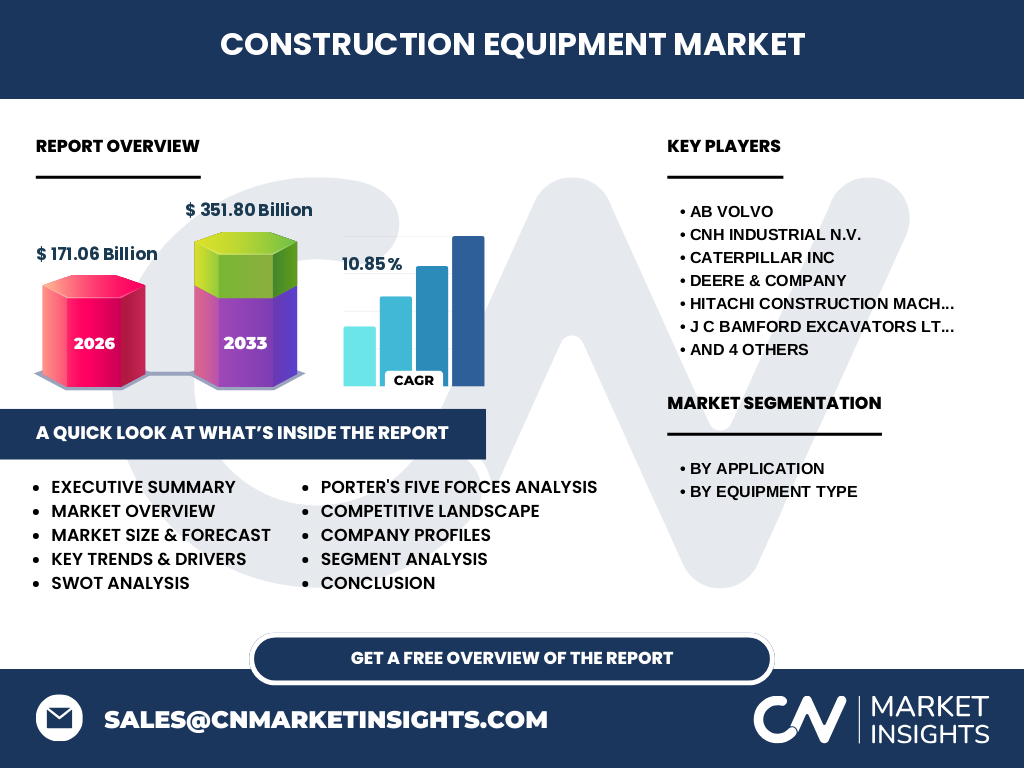

6. What are the key findings in the Executive Summary of the Construction Equipment Market?

The market is valued at $171.06 billion in 2026 and is projected to reach $351.80 billion by 2033, reflecting a robust CAGR of 10.85 % over the forecast horizon. Growth is propelled by strong infrastructure pipelines, digital transformation, and a shift toward greener equipment. The residential segment leads application demand, while heavy construction vehicles command the largest revenue share. North America and Asia‑Pacific remain the primary geographic contributors, with Asia‑Pacific exhibiting the fastest growth due to urban expansion. Competitive dynamics are defined by technology investment and expanding aftermarket services.

7. What is the Construction Equipment Market Forecast for 2025‑2032?

Based on the provided CAGR of 10.85 %, the market is expected to maintain double‑digit expansion through 2032. Steady increases in government‑funded infrastructure projects, coupled with private‑sector construction activity, will sustain demand across all equipment types. Electric and hybrid models are anticipated to capture an increasingly larger portion of new orders, especially in regions with strict emission standards. The forecast period also foresees heightened aftermarket revenue as operators extend equipment life cycles through retrofits and digital services.

8. How is the Construction Equipment Market sized and shared by segmentation?

By application, the market splits into residential, commercial, and industrial segments. Residential construction drives the highest demand for compact excavators and material‑handling equipment due to rapid housing development. Commercial projects, such as office towers and retail complexes, raise demand for higher‑capacity earthmoving and lifting solutions. Industrial applications—mining, energy, and large‑scale infrastructure—require the most robust heavy construction vehicles. By equipment type, heavy construction vehicles (e.g., bulldozers, loaders) dominate the revenue base, followed by earthmoving equipment (excavators, backhoes) and material‑handling equipment (cranes, forklifts).

9. What is the Global Construction Equipment Market size and share by region?

The global market totals $171.06 billion in 2026. Geographic distribution shows North America and Asia‑Pacific as the two primary contributors. Asia‑Pacific, driven by China, India, and Southeast Asian economies, holds the largest share due to extensive urbanization and infrastructure investment. North America retains a strong position owing to mature construction activities and early adoption of advanced equipment technologies. Europe and the Middle East exhibit moderate shares, with growth linked to renovation projects and renewable‑energy infrastructure.

10. What are the key insights from the Regional Analysis of the Construction Equipment Market?

In Asia‑Pacific, rapid city expansion and government‑backed highway and rail programs fuel demand for high‑productivity earthmoving machines. China’s “Belt and Road” initiatives and India’s housing schemes are particularly influential. North America benefits from steady commercial‑real‑estate development and a push for sustainable construction, encouraging investment in low‑emission equipment. Europe’s market is shaped by stringent EU environmental directives, prompting OEMs to accelerate electric‑equipment roll‑outs. The Middle East sees a resurgence in megaprojects for tourism and logistics, increasing demand for heavy lifting and material‑handling solutions.

11. Which companies lead the Construction Equipment Market and what are their strategic approaches?

Leading firms include AB Volvo, CNH Industrial, Caterpillar, Deere & Company, Hitachi Construction Machinery, JCB, Komatsu, Liebherr, Terex, and Zoomlion. Strategies focus on expanding product portfolios with electric and autonomous models, strengthening global dealer networks, and investing in digital services such as remote diagnostics. Many are pursuing strategic acquisitions to gain technology capabilities—e.g., Caterpillar’s acquisition of autonomous‑driving startups—and forming joint ventures to access emerging markets, as seen with Zoomlion’s partnerships in Africa.

12. How does Porter’s Five Forces analysis assess the Construction Equipment Market?

• Threat of new entrants: Low, due to high capital requirements, technological barriers, and established dealer networks.

• Bargaining power of suppliers: Moderate, as key components (engine, hydraulics) are sourced from specialized suppliers, but OEMs often negotiate long‑term contracts.

• Bargaining power of buyers: Moderate to high; large contractors can negotiate pricing and demand integrated service packages.

• Threat of substitutes: Low, because functional alternatives to heavy equipment are limited, though modular construction methods can reduce equipment intensity.

• Competitive rivalry: High, driven by a few dominant OEMs competing on technology, reliability, and service breadth.

13. What are the SWOT findings for the Construction Equipment Market?

Strengths: Essential role in global infrastructure, strong OEM brand equity, and expanding digital service ecosystems.

Weaknesses: High upfront costs, dependence on cyclical construction spending, and legacy product lines with older emissions profiles.

Opportunities: Electrification, autonomous operation, aftermarket digital services, and growth in emerging economies.

Threats: Economic downturns affecting construction spend, tightening environmental regulations, and supply‑chain volatility for critical components.

14. What does the Construction Equipment Market Value Chain look like?

The value chain begins with raw‑material suppliers (steel, hydraulics, electronics), proceeds to OEM design and engineering, followed by manufacturing and assembly. Distribution occurs through global dealer networks, after‑sales service centers, and third‑party rental firms. End‑users—contractors, mining firms, and municipalities—receive equipment, often accompanied by financing solutions and telematics services that enable performance monitoring and predictive maintenance, creating additional revenue streams for OEMs.

15. What key investment insights can be drawn for the Construction Equipment Market?

Investors should prioritize companies with proven electric‑power‑train roadmaps and strong aftermarket service platforms, as these segments promise higher margins and recurring revenue. Geographic diversification into fast‑growing Asia‑Pacific markets reduces exposure to mature‑region cyclicality. Partnerships with technology firms—especially those focused on AI‑driven fleet management—offer strategic upside. Finally, monitoring policy trends on emissions will help identify early‑stage opportunities in regulated markets.

16. How does the Construction Equipment Market conclude its analysis?

The market is on a decisive growth trajectory, underpinned by infrastructure demand, digital innovation, and sustainability imperatives. With a projected valuation of $351.80 billion by 2033 and a 10.85 % CAGR, the sector presents attractive opportunities for OEMs, service providers, and investors alike. Success will hinge on the ability to deliver technologically advanced, low‑emission equipment while expanding value‑added services that lock in long‑term customer relationships.

17. What research methodology was employed for this report?

The study combined primary interviews with industry executives, OEM representatives, and key distributors, alongside secondary data from company filings, trade publications, and government infrastructure statistics. Quantitative analysis used compound‑annual growth calculations based on the provided market size (2026: $171.06 billion) and forecast (2027‑2033: $351.80 billion). Qualitative insights were derived through thematic coding of expert responses and trend monitoring.

18. What is the scope of this research and its limitations?

The scope covers global construction equipment across residential, commercial, and industrial applications, segmented by equipment type. It includes market sizing, competitive landscape, and forward‑looking forecasts to 2033. Limitations stem from reliance on publicly available financial figures and the exclusion of proprietary regional sales data that may refine market‑share estimates.

19. Which key companies are highlighted and what recent developments have they announced?

Top firms—AB Volvo, CNH Industrial, Caterpillar, Deere & Company, Hitachi Construction Machinery, JCB, Komatsu, Liebherr, Terex, and Zoomlion—have all reported recent initiatives. Examples include Caterpillar’s launch of an autonomous loader series, Komatsu’s partnership with a battery‑technology provider to accelerate electric excavators, and Zoomlion’s entry into the African market through a joint venture focused on rental services. JCB unveiled a hybrid backhoe model, while Liebherr expanded its digital fleet‑management platform to integrate with third‑party construction software.