What is the Asia Pacific 5G Chipset Market Overview – Definition, scope, and significance?

The Asia Pacific 5G chipset market comprises integrated circuits that enable 5G radio access, core network functions, and device connectivity across the region. It includes chipsets used in smartphones, consumer electronics, automotive telematics, industrial automation, and network‑infrastructure equipment. The market’s scope extends from design and fabrication to testing, deployment, and after‑sales support for sub‑6 GHz, mid‑band (26‑39 GHz), and mmWave (>39 GHz) frequencies. Its significance lies in powering the digital transformation of economies, supporting the rollout of high‑speed mobile broadband, enabling massive‑IoT deployments, and fostering new services such as autonomous driving, remote healthcare, and smart‑city applications across Asia Pacific’s rapidly expanding consumer base.

What are the key drivers, restraints, challenges, and opportunities shaping the Asia Pacific 5G Chipset Market?

Key drivers include aggressive 5G network rollouts by governments, soaring demand for high‑performance smartphones, and the rise of data‑intensive use cases in automotive, industrial automation, and public safety. The region’s strong manufacturing ecosystem and the presence of leading fab facilities lower production costs, further stimulating growth. Restraints stem from high R&D expenditures required to develop multi‑band, low‑latency chips and from supply‑chain vulnerabilities that can affect component availability. Challenges involve intense competition among global and local semiconductor firms, regulatory fragmentation across countries, and the need for backward compatibility with 4G networks. Opportunities arise from emerging verticals such as edge‑AI for smart factories, 5G‑enabled healthcare tele‑services, and the development of energy‑efficient chip architectures that meet sustainability targets.

What growth trends are currently influencing the Asia Pacific 5G chipset market?

Current trends include the convergence of 5G and AI on a single chipset, enabling on‑device intelligence for real‑time analytics. Another trend is the shift toward heterogeneous integration, where multiple semiconductor technologies (e.g., RF, baseband, and power management) are combined in a single package to reduce size and power consumption. There is also a noticeable rise in the adoption of open‑rural and private‑network solutions, prompting chipset vendors to develop customized firmware for enterprise and industrial customers. Finally, the proliferation of mid‑band (26‑39 GHz) deployments is accelerating the demand for chipsets that balance coverage and capacity, driving product diversification.

How did COVID‑19 impact the Asia Pacific 5G chipset market and what is the recovery trajectory?

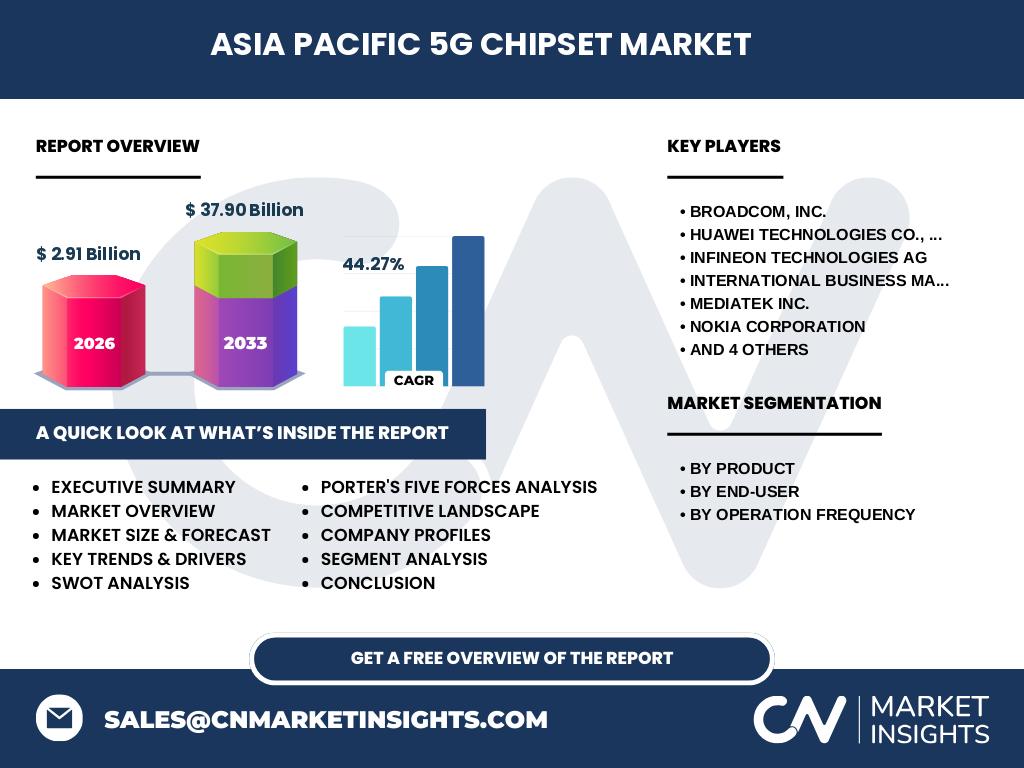

During the pandemic, supply‑chain disruptions and temporary factory shutdowns slowed chipset production, while postponement of some network rollout projects reduced short‑term demand. However, remote work, e‑learning, and increased video streaming amplified consumer demand for high‑speed connectivity, offsetting supply constraints. Post‑2020, the market entered a rapid recovery as governments prioritized digital infrastructure, and manufacturers ramped up capacity with new fab lines. The recovery trajectory is strong, with the market projected to grow from a 2026 size of $2.91 billion to $37.90 billion by 2033, reflecting robust demand across all segments.

Who are the major competitors and what is the consolidation landscape in the Asia Pacific 5G chipset market?

Key competitors include Broadcom, Inc.; Huawei Technologies Co., Ltd.; Infineon Technologies AG; International Business Machines Corporation; MediaTek Inc.; Nokia Corporation; Qualcomm Incorporated; Samsung Electronics Co., Ltd.; Telefonaktiebolaget LM Ericsson; and Xilinx, Inc. The market has seen strategic alliances, joint ventures, and acquisitions aimed at strengthening technology portfolios and expanding regional presence. Consolidation is driven by the need to acquire advanced RF and AI capabilities, secure access to fab capacity, and enhance end‑to‑end 5G solutions for telecom operators and enterprise customers.

What are the high‑level insights and key findings from the Asia Pacific 5G chipset market?

The market is poised for explosive growth, evidenced by a 44.27 % CAGR and a projected value of $37.90 billion by 2033. Sub‑6 GHz and mid‑band frequencies dominate current deployments, while mmWave chipsets are gaining traction for high‑capacity urban zones. Device and network‑infrastructure segments together account for the largest revenue share, driven by smartphone demand and carrier‑grade base stations. Automotive, healthcare, and industrial automation are emerging as high‑growth end‑users. Competitive dynamics favor firms that combine advanced process technology with strong IP portfolios and regional manufacturing capabilities.

What is the forecast for the Asia Pacific 5G chipset market through 2032?

Based on the provided CAGR of 44.27 %, the market is expected to expand from $2.91 billion in 2026 to approximately $37.90 billion by 2033. Extending this trajectory, the market will likely continue to rise through 2032, driven by sustained 5G coverage expansion, increasing adoption of 5G‑enabled devices, and the diversification of vertical applications. The forecast indicates a multi‑year growth pattern, with peak acceleration expected as mid‑band and mmWave networks mature and as new chipset generations incorporate AI and edge‑computing capabilities.

How is the Asia Pacific 5G chipset market sized and shared by product, end‑user, and operation frequency segments?

By product, the market is divided into devices, customer premises equipment, and network‑infrastructure equipment, each addressing distinct demand drivers such as consumer adoption, enterprise connectivity, and carrier deployment. By end‑user, the market covers automotive & transportation, energy & utilities, healthcare, retail, building automation, industrial automation, consumer electronics, and public safety & surveillance, reflecting the breadth of 5G use cases. By operation frequency, chipsets are classified into sub‑6 GHz, 26‑39 GHz, and >39 GHz categories, aligning with coverage, capacity, and latency requirements across varied deployment scenarios.

What is the global Asia Pacific 5G chipset market size and share by region?

The Asia Pacific region accounts for the majority of the global 5G chipset market, underpinned by leading economies such as China, Japan, South Korea, India, and Australia. While exact regional share percentages are not disclosed, the region’s market size of $2.91 billion in 2026 and the projected $37.90 billion in 2033 illustrate its dominant position in the worldwide landscape.

What are the detailed regional performance trends within the Asia Pacific 5G chipset market?

China leads with extensive network rollouts and a strong domestic semiconductor supply chain, driving high demand for both device and infrastructure chipsets. Japan and South Korea focus on advanced manufacturing and premium device markets, emphasizing high‑frequency mmWave solutions. India’s large consumer base fuels rapid growth in sub‑6 GHz device chipsets, while Southeast Asian nations such as Singapore and Australia invest in private‑network deployments for industrial and public‑safety applications. These regional dynamics create a mosaic of demand patterns that collectively support the market’s high growth rate.

Which companies are leading the Asia Pacific 5G chipset market and what are their strategic approaches?

Broadcom and Qualcomm dominate the mobile device chipset space with extensive IP portfolios and strong relationships with handset OEMs. Huawei and Samsung focus on both device and network‑infrastructure chipsets, leveraging in‑house fabs to control supply. MediaTek pursues cost‑effective solutions for mass‑market smartphones, while Infineon and Xilinx target specialized applications such as automotive and industrial automation through robust power‑management and FPGA technologies. Nokia, Ericsson, and IBM contribute primarily to network‑infrastructure and enterprise solutions, emphasizing software‑defined networking and cloud‑native architectures.

How does Porter’s Five Forces model apply to the Asia Pacific 5G chipset market?

Threat of new entrants is moderate due to high capital requirements and advanced technology barriers. Bargaining power of suppliers is relatively high, as few fab facilities can meet the sophisticated process nodes required for 5G chipsets. Bargaining power of buyers is strong, given the concentration of large telecom operators and OEMs that can negotiate pricing and demand customization. Threat of substitutes is low, as 5G chipsets are uniquely required for next‑generation connectivity. Industry rivalry is intense, driven by rapid innovation cycles, IP competition, and the race to secure multi‑band, low‑latency solutions.

What are the SWOT strengths, weaknesses, opportunities, and threats for the Asia Pacific 5G chipset market?

Strengths: Robust regional manufacturing base, high R&D investment, and growing demand across multiple verticals. Weaknesses: Dependence on advanced fab capacity and exposure to geopolitical trade restrictions. Opportunities: Expansion into AI‑enabled edge devices, private‑network solutions for enterprises, and integration of sustainable, low‑power chip architectures. Threats: Supply‑chain disruptions, escalating competition from emerging fab players, and regulatory uncertainties surrounding spectrum allocation.

What does the value chain of the Asia Pacific 5G chipset market look like?

The value chain begins with semiconductor design (IP licensing, architecture development), followed by wafer fabrication (foundry services), packaging and testing, and finally integration into end‑products (smartphones, base stations, automotive modules). Ancillary services such as firmware development, OTA updates, and after‑sales support complete the chain. Collaboration between design houses, fab partners, and OEMs is critical to reduce time‑to‑market and ensure compliance with regional standards.

What investment insights can be drawn for strategic stakeholders in the Asia Pacific 5G chipset market?

Investors should prioritize companies with diversified product portfolios spanning sub‑6 GHz to mmWave, strong IP assets, and secure access to advanced fabs. Partnerships that combine chipset expertise with AI or IoT platforms present high upside. Funding for fab expansion in emerging economies can mitigate supply‑chain risk. Additionally, financing ventures that develop low‑power, sustainable chip designs aligns with regulatory trends and corporate ESG goals.

What are the concluding takeaways from the Asia Pacific 5G chipset market analysis?

The market is on a steep growth trajectory, driven by government‑backed 5G deployments, expanding vertical applications, and relentless innovation in chipset integration. The combination of a sizable 2026 market base, a 44.27 % CAGR, and a forecasted $37.90 billion valuation by 2033 underscores the sector’s strategic importance. Companies that can navigate supply‑chain complexities, deliver multi‑band solutions, and align with emerging AI and edge‑computing needs will capture the greatest market share.

What research methodology was employed to compile this market report?

The study used a mixed‑method approach, integrating secondary data collection from industry publications, company filings, and reputable market databases with primary insights from expert interviews across semiconductor manufacturers, telecom operators, and end‑user industries. Quantitative data were validated through cross‑referencing, and qualitative assessments were applied to interpret trends, competitive dynamics, and strategic implications.

What is the scope of this research, including its coverage and any limitations?

The scope covers the Asia Pacific 5G chipset market from 2026 to 2033, focusing on product, end‑user, and frequency segments, as well as regional performance across major APAC economies. It includes competitive analysis of the top ten listed companies. While the report leverages the most recent available data, it does not extrapolate beyond the provided financial figures, and it does not incorporate proprietary financial disclosures not publicly released.

Which key companies are highlighted and what recent developments have they announced?

Highlighted firms include Broadcom, Huawei, Infineon, IBM, MediaTek, Nokia, Qualcomm, Samsung, Ericsson, and Xilinx. Recent developments feature Qualcomm’s launch of a multi‑band 5G modem supporting sub‑6 GHz and mmWave, MediaTek’s introduction of a cost‑optimized 5G chipset for mid‑range smartphones, Samsung’s partnership with regional carriers for network‑infrastructure chip supply, Huawei’s expansion of its fab capacity in southern China, and Xilinx’s release of an FPGA‑based 5G accelerator aimed at industrial automation. These announcements illustrate the market’s rapid product evolution and collaborative strategies.