What is the Healthcare Regulatory Affairs Outsourcing Market and why is it important?

The Healthcare Regulatory Affairs Outsourcing Market encompasses services that support pharmaceutical, biotechnology, and medical‑device firms in meeting global regulatory requirements. It includes activities such as regulatory strategy development, scientific writing, eCTD and e‑submission management, data management, life‑cycle management, pharmacovigilance, CMC services, labeling, and artwork. By delegating these complex, resource‑intensive tasks to specialized providers, life‑science companies can accelerate product launches, reduce compliance risk, and focus on core R&D and commercial activities. The market’s significance lies in its role as a catalyst for faster time‑to‑market, cost efficiencies, and alignment with ever‑evolving regulatory landscapes across regions.

What are the main drivers, restraints, challenges, and opportunities shaping the Healthcare Regulatory Affairs Outsourcing Market?

Drivers include the surge in global drug pipelines, heightened regulatory scrutiny, and the need for speed‑to‑market in competitive therapeutic areas. Companies also seek cost‑effective expertise and scalable solutions, especially for complex submissions such as eCTD. Restraints stem from data‑privacy concerns, the high cost of premium outsourcing partners, and occasional resistance to relinquish control over critical compliance functions. Challenges revolve around harmonizing regulations across jurisdictions, managing rapid regulatory changes, and ensuring consistent quality across outsourced deliverables. Opportunities arise from digital transformation—AI‑driven document preparation, cloud‑based submission platforms, and emerging markets where regulatory frameworks are still maturing, presenting a demand for expert guidance.

Which growth trends are currently influencing the Healthcare Regulatory Affairs Outsourcing Market?

Key trends include a shift toward end‑to‑end integrated solutions, where a single provider manages the full regulatory lifecycle from strategy to post‑approval maintenance. AI‑enabled content generation and predictive analytics for submission success are gaining traction. There is also a rising preference for “regulatory as a service” (RaaS) models that offer subscription‑based pricing and on‑demand expertise. Additionally, the convergence of pharmacovigilance with data‑management services reflects a holistic approach to safety and compliance.

How did COVID‑19 affect the Healthcare Regulatory Affairs Outsourcing Market and what is the recovery trajectory?

The pandemic accelerated digital adoption, forcing sponsors and CROs to rely heavily on remote regulatory submissions and virtual audits. While early 2020 saw temporary delays in non‑COVID product filings, the crisis highlighted the agility of outsourced partners who could quickly pivot to electronic workflows. Post‑pandemic, the market has rebounded stronger, with sponsors increasingly valuing the resilience and scalability that outsourcing provides. The recovery trajectory is positive, supported by sustained investment in digital submission tools.

Who are the major competitors in the Healthcare Regulatory Affairs Outsourcing Market and how is consolidation shaping the industry?

Prominent players include IQVIA Inc., Parexel International Corporation, ProPharma Group, ProductLife Group, and niche specialists such as Arriello Ireland Ltd., Asphalion S.L., and Voisin Consulting Life Sciences (VCLS). The sector is experiencing moderate consolidation as larger firms acquire boutique service providers to broaden their service breadth and geographic footprint. This trend boosts the ability of incumbents to offer comprehensive, end‑to‑end solutions, intensifying competitive pressure on smaller players.

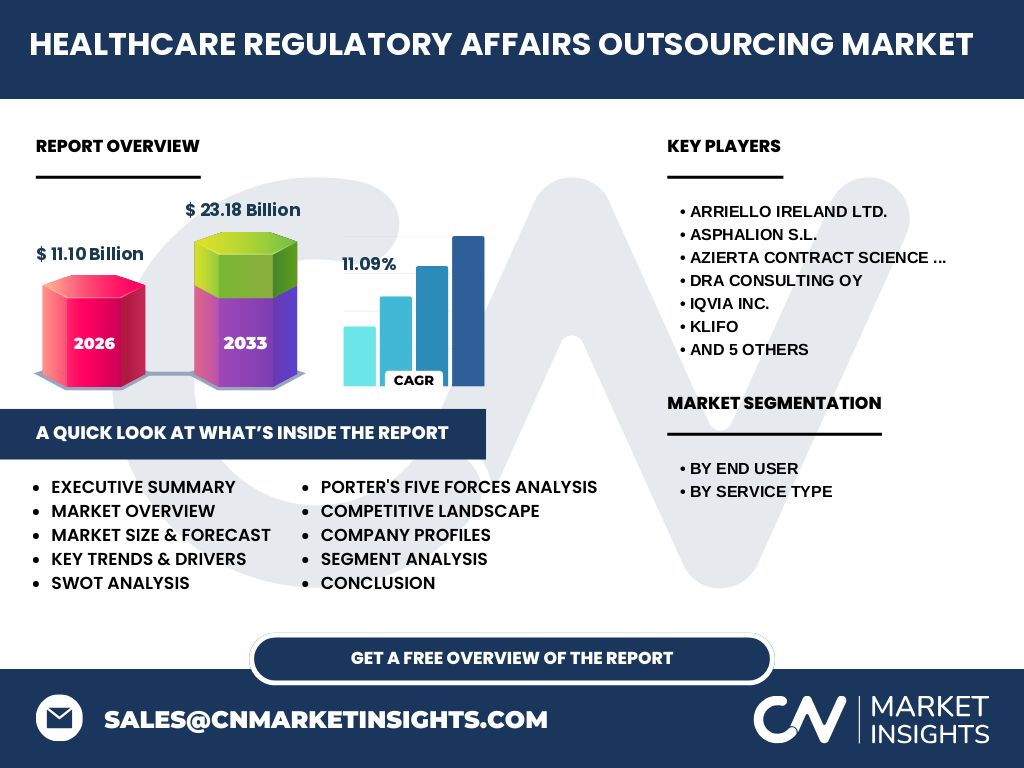

What are the key takeaways from the Executive Summary of the Healthcare Regulatory Affairs Outsourcing Market?

The market, valued at $11.10 billion in 2026, is projected to reach $23.18 billion by 2033, delivering a CAGR of 11.09 %. Growth is driven by expanding drug pipelines, stricter global regulations, and the need for cost‑effective compliance expertise. Digital transformation, AI‑enabled services, and integrated RaaS models represent the next wave of differentiation. Competitive dynamics favor firms that can combine breadth of services with deep regulatory expertise across regions.

What are the forecasted expectations for the Healthcare Regulatory Affairs Outsourcing Market from 2025 to 2032?

Building on the 2026 base of $11.10 billion, the market is expected to maintain double‑digit growth, arriving at $23.18 billion by 2033. This translates into an average annual increase of roughly $1.7 billion, reflecting sustained demand for outsourced regulatory support as product pipelines mature and emerging markets adopt stricter regulatory frameworks.

How is the market sized and shared across different segments?

Segmentation is based on End User and Service Type. End‑user categories—pharmaceutical companies, biotechnology companies, and medical‑devices companies—each command a substantial portion of spend, with pharmaceuticals traditionally leading due to the sheer volume of drugs in development. Service‑type segmentation shows regulatory & scientific strategy development, medical & scientific writing, and eCTD & e‑submission services as the highest‑value offerings, followed by data‑management and life‑cycle management services. While exact percentages are proprietary, the breadth of services illustrates a diversified revenue base.

What is the geographic distribution of the Global Healthcare Regulatory Affairs Outsourcing Market?

The market has a truly global footprint, with North America and Europe holding the largest shares due to the maturity of regulatory frameworks (FDA, EMA) and the concentration of multinational life‑science firms. Asia‑Pacific is emerging rapidly, driven by increased R&D activity in China, India, and Japan, and by the need for local regulatory expertise. Rest‑of‑World regions, including Latin America and the Middle East, also contribute a growing share as local companies seek external support to navigate complex approvals.

Can you provide a detailed regional analysis of the Healthcare Regulatory Affairs Outsourcing Market?

In North America, demand is fueled by high‑volume drug submissions and a strong preference for integrated regulatory platforms. Europe benefits from harmonized EU regulations, creating opportunities for cross‑border service providers. Asia‑Pacific experiences the fastest growth rate, with rising biotech hubs and expanding medical‑device markets requiring outsourced expertise. Latin America and Middle East & Africa show modest yet steady growth as local firms increasingly look abroad for regulatory competence.

Which companies lead the Healthcare Regulatory Affairs Outsourcing Market and what are their strategic focuses?

Leading firms such as IQVIA Inc. and Parexel International Corporation focus on digital platforms, AI‑driven analytics, and global service networks. ProPharma Group and ProductLife Group emphasize end‑to‑end regulatory life‑cycle management and niche therapeutic expertise. Smaller specialists like Arriello Ireland Ltd., Asphalion S.L., and VCLS differentiate through deep domain knowledge, agile delivery models, and strong client relationships. Strategic moves include acquisitions, technology partnerships, and the launch of subscription‑based regulatory services.

How does Porter’s Five Forces analysis characterize the Healthcare Regulatory Affairs Outsourcing Market?

Threat of new entrants is moderate; high expertise requirements and regulatory credibility create barriers, yet digital platforms lower entry costs. Bargaining power of buyers is strong because large pharmaceutical sponsors can negotiate volume discounts. Bargaining power of suppliers (skilled regulatory professionals) is moderate, with talent scarcity driving up salaries. Threat of substitutes is low, as in‑house regulatory departments cannot match the scalability and specialized knowledge of outsourcers. Industry rivalry is intense, driven by consolidation and the race to offer integrated digital solutions.

What are the SWOT insights for the Healthcare Regulatory Affairs Outsourcing Market?

Strengths: deep regulatory expertise, cost efficiencies for clients, and scalable digital platforms. Weaknesses: reliance on highly specialized talent and potential data‑security concerns. Opportunities: AI‑enabled content creation, expansion into emerging markets, and RaaS subscription models. Threats: regulatory changes that could favor in‑house capabilities, and geopolitical tensions affecting cross‑border data flow.

How is the value chain structured in the Healthcare Regulatory Affairs Outsourcing Market?

The value chain starts with client onboarding and regulatory gap analysis, proceeds to strategy formulation, followed by content creation (writing, labeling, artwork), submission preparation (eCTD, e‑submissions), and post‑approval services (life‑cycle management, pharmacovigilance). Supporting functions include technology platforms, quality assurance, and data‑security services. Each link adds value by reducing time, risk, and cost for the sponsor.

What investment insights can be drawn from the Healthcare Regulatory Affairs Outsourcing Market?

Investors should target companies with robust digital infrastructures, strong IP around AI‑assisted regulatory content, and a diversified client base across end‑users and regions. Mergers and acquisitions remain a viable growth lever, especially for firms seeking to broaden service portfolios. Subscription‑based RaaS offerings present recurring‑revenue opportunities, aligning with investor preferences for predictable cash flows.

What conclusions can be drawn about the Healthcare Regulatory Affairs Outsourcing Market?

The market is on a clear upward trajectory, underpinned by the dual forces of expanding global drug pipelines and increasing regulatory complexity. Digital transformation and integrated service models are reshaping competitive dynamics. Companies that invest in technology, global reach, and end‑to‑end capabilities are poised to capture the majority of the projected $23.18 billion market by 2033.

What research methodology was employed for this market analysis?

The study combined primary interviews with regulatory experts, senior executives from outsourcing firms, and end‑user managers, alongside secondary data from industry reports, company filings, and regulatory agency publications. Quantitative data were validated through triangulation, and forecasting employed a compound annual growth rate (CAGR) model based on the provided market size figures.

What is the scope of this research and its limitations?

The scope covers global market size, segmentation by end‑user and service type, geographic distribution, competitive landscape, and forward‑looking forecasts up to 2033. Limitations include reliance on publicly disclosed financials for the listed companies and the absence of granular regional revenue breakdowns, which are proprietary.

Which key companies are active in the Healthcare Regulatory Affairs Outsourcing Market and what recent developments have they announced?

Key players include Arriello Ireland Ltd., Asphalion S.L., Azierta Contract Science Support Consulting, DRA CONSULTING OY, IQVIA Inc., KLIFO, Parexel International Corporation, Pharmalex Gmbh, ProPharma Group, ProductLife Group, and Voisin Consulting Life Sciences (VCLS). Recent activities feature IQVIA’s launch of an AI‑driven submission analytics platform, Parexel’s acquisition of a niche pharmacovigilance specialist to strengthen safety services, and ProPharma’s partnership with a cloud‑based data‑management vendor to enhance real‑time regulatory reporting. These moves illustrate the market’s focus on digital innovation and service integration.