1. What is the definition, scope, and significance of the Micro Mobile Data Center Market?

The Micro Mobile Data Center (MMDC) market comprises compact, transportable data center solutions that deliver enterprise‑grade compute, storage, networking, and power in a ruggedized enclosure. Typically ranging from a few rack units to full‑scale deployments, these units are designed for rapid deployment, scalability, and operation in harsh or remote environments. The scope of the market covers hardware platforms, integrated software, cooling and power management systems, and associated services such as installation, monitoring, and maintenance. Significance stems from the growing need for edge computing, disaster‑recovery capabilities, and on‑site processing for latency‑critical applications across industries like telecommunications, finance, healthcare, and manufacturing.

2. What are the key drivers, restraints, challenges, and opportunities shaping the Micro Mobile Data Center Market?

Key drivers include the surge in 5G roll‑outs, increasing demand for edge computing, and the need for rapid, temporary infrastructure during disaster response or large‑scale events. Digital transformation initiatives across BFSI, retail, and healthcare also accelerate adoption. Restraints involve high upfront capital costs and regulatory compliance for power and cooling in certain jurisdictions. Challenges revolve around managing thermal performance in confined spaces and ensuring cybersecurity for mobile assets. Opportunities arise from emerging use cases such as high‑density network hubs, remote office support for distributed workforces, and integration with renewable energy sources to create truly off‑grid solutions.

3. What current and emerging growth trends are influencing the Micro Mobile Data Center Market?

The market is trending toward higher rack‑unit densities, with a noticeable shift from the “Up to 25 RU” segment to the “Above 40 RU” segment as customers demand more compute power per footprint. Modular architecture and software‑defined infrastructure are enabling faster provisioning and easier scaling. Additionally, the convergence of AI workloads at the edge is prompting vendors to incorporate accelerated compute (GPU/FPGA) within mobile units. Another emerging trend is the use of containerized data centers for rapid field deployment in military and humanitarian missions.

4. How has COVID‑19 impacted the Micro Mobile Data Center Market and what is the recovery trajectory?

The pandemic accelerated remote work and highlighted the vulnerability of centralized data centers, driving interest in decentralized, mobile solutions. Demand for temporary capacity to support surged online services and vaccination‑site data processing led to short‑term contract wins for several vendors. Post‑pandemic, the market has continued to grow as organizations retain hybrid work models, maintaining the momentum created during the crisis. Recovery is reflected in robust pipeline projects and a steady pipeline of edge‑centric initiatives.

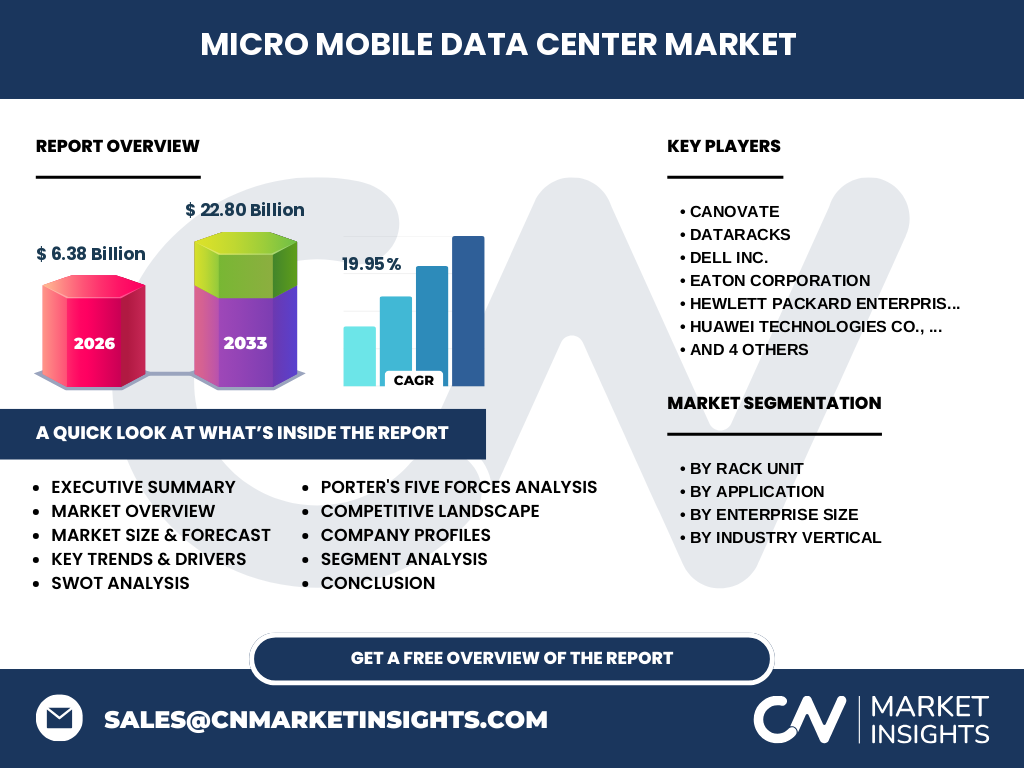

5. Who are the major competitors in the Micro Mobile Data Center Market and what is the state of market consolidation?

Key players include Canovate, Dataracks, Dell Inc., Eaton Corporation, Hewlett Packard Enterprise Development LP, Huawei Technologies Co., Ltd., Panduit, Rittal GmbH and Co. KG, Schneider Electric, and Zella DC. The competitive landscape is characterized by strategic partnerships, joint development of cooling technologies, and acquisitions aimed at expanding edge‑compute portfolios. While no single entity dominates, the market shows moderate consolidation as larger OEMs acquire niche mobile‑centric firms to broaden their edge offerings.

6. What are the high‑level findings and key takeaways from the Micro Mobile Data Center Market Executive Summary?

The market is projected to reach USD 6.38 billion in 2026 and expand to USD 22.80 billion by 2033, reflecting a compound annual growth rate (CAGR) of 19.95 % over the forecast horizon. Growth is driven by edge‑computing adoption, 5G infrastructure expansion, and the need for resilient, on‑site processing. The “Above 40 RU” segment and applications such as High‑Density Networks and Remote Office Support are emerging as high‑growth areas. Competitive dynamics are intensifying, with vendors focusing on modularity, energy efficiency, and integrated security. Opportunities for investors include targeting high‑density, AI‑enabled mobile units and leveraging renewable‑energy integrations.

7. What are the projected market size and growth outlook for the Micro Mobile Data Center Market from 2025 to 2032?

Based on the disclosed CAGR of 19.95 %, the market is expected to maintain a rapid expansion trajectory. Starting from the 2026 base of USD 6.38 billion, the forecast indicates a market value of approximately USD 22.80 billion by 2033. This suggests that the market will more than triple within seven years, underscoring strong demand across all segments and regions. The forecast reflects continued investment in edge infrastructure, especially in high‑density and AI‑driven deployments.

8. How is the Micro Mobile Data Center Market sized and shared across the defined segments?

Segmentation by rack unit reveals three distinct categories: “Up to 25 RU,” “25‑40 RU,” and “Above 40 RU.” While exact monetary shares are not disclosed, the trend indicates a shift toward larger capacity units (“Above 40 RU”) as enterprises seek greater compute density. Application‑wise, the market is divided among Instant DC and Retrofit, High‑Density Networks, Remote Office Support, and Mobile Computing, with High‑Density Networks and Remote Office Support showing the strongest growth potential. Enterprise‑size segmentation shows separate focus on Large Enterprises versus Small and Medium‑Size Enterprises (SMEs), with large enterprises driving the majority of high‑value contracts. Industry verticals include BFSI, Retail, Healthcare, IT and Telecom, and Manufacturing, each leveraging mobile data centers for specific use cases such as secure transaction processing, point‑of‑sale analytics, telemedicine, and production line monitoring.

9. What is the global geographic distribution of the Micro Mobile Data Center Market?

The market exhibits a truly global footprint, with significant adoption in North America, Europe, Asia‑Pacific, and emerging growth in Middle‑East & Africa and Latin America. Although precise regional revenue figures are not provided, the presence of major vendors with worldwide sales networks and the universal need for edge capabilities suggest a balanced distribution, with North America and Asia‑Pacific leading due to early 5G deployments and robust industrial automation initiatives.

10. Can you provide a detailed regional analysis of the Micro Mobile Data Center Market?

In North America, demand is driven by large‑scale enterprise digital transformation, advanced telecom roll‑outs, and stringent disaster‑recovery regulations. Europe’s growth is fueled by sustainability mandates and strong manufacturing sectors seeking mobile edge solutions. Asia‑Pacific shows the fastest adoption, powered by rapid 5G rollout, smart city projects, and a large SME base requiring remote office support. The Middle‑East & Africa region is witnessing investments in oil‑&‑gas remote monitoring, while Latin America is emerging as a market for mobile computing solutions in logistics and retail.

11. What are the profiles of leading companies in the Micro Mobile Data Center Market and their strategic approaches?

Canovate focuses on modular containerized solutions with integrated cooling. Dataracks specializes in high‑density rack designs for telecom edge sites. Dell Inc. leverages its broader data‑center portfolio to offer turnkey mobile units with embedded management software. Eaton provides power‑management expertise, emphasizing energy efficiency. Hewlett Packard Enterprise Development LP delivers software‑defined infrastructure, enabling rapid orchestration. Huawei combines networking strength with mobile chassis for 5G edge deployments. Panduit supplies cabling and connectivity solutions that complement mobile enclosures. Rittal offers scalable, stackable units with strong thermal engineering. Schneider Electric integrates advanced power‑distribution and monitoring services. Zella DC focuses on ultra‑compact, ruggedized units for remote and military use.

12. How do Porter’s Five Forces affect the Micro Mobile Data Center Market?

• Threat of New Entrants: Moderate – high capital requirements and technology expertise limit entry, but niche innovators can disrupt with specialized cooling or AI integration.

• Bargaining Power of Suppliers: Low to moderate – component suppliers (semiconductors, batteries) have some influence, yet large OEMs can negotiate favorable terms.

• Bargaining Power of Buyers: High – enterprises demand customized solutions, driving vendors to offer flexible pricing and service contracts.

• Threat of Substitutes: Low – traditional stationary data centers cannot match the mobility and rapid‑deployment advantage of MMDCs.

• Industry Rivalry: Intense – multiple global players compete on performance, energy efficiency, and service ecosystems, leading to continuous innovation.

13. What are the SWOT insights for the Micro Mobile Data Center Market?

Strengths: Rapid deployment, edge‑computing enablement, scalability, and resilience.

Weaknesses: High initial cost, limited space for extensive hardware, and dependence on reliable power sources.

Opportunities: Integration with renewable energy, AI‑accelerated workloads, and expansion into emerging markets with limited fixed infrastructure.

Threats: Supply‑chain disruptions for critical components, evolving cybersecurity regulations, and potential saturation in mature regions.

14. How is the value chain structured for the Micro Mobile Data Center industry?

The value chain begins with component suppliers (servers, networking gear, power modules, cooling systems). These feed system integrators who assemble the mobile enclosure, embed management software, and conduct testing. Next, vendors provide sales, financing, and logistics services to deliver the units to end‑users. Post‑sale, service providers deliver installation, remote monitoring, maintenance, and upgrade pathways, creating recurring revenue streams. Partnerships with telecom operators and cloud providers often sit at the top of the chain, enabling end‑to‑end edge solutions.

15. What key investment insights should investors consider when evaluating the Micro Mobile Data Center Market?

Investors should focus on companies with strong modular platforms, proven integration of AI accelerators, and a diversified portfolio across rack‑unit sizes. Firms that have secured long‑term contracts with telecom operators or government agencies present lower risk. Attention to ESG factors—such as renewable‑energy‑compatible designs—can unlock additional capital. Finally, monitoring M&A activity can reveal consolidation signals and potential entry points for strategic investments.

16. What are the concluding remarks and major takeaways for the Micro Mobile Data Center Market?

The MMDC market is on a steep growth curve, projected to expand from USD 6.38 billion in 2026 to USD 22.80 billion by 2033 at a CAGR of 19.95 %. Edge computing, 5G, and the need for resilient, mobile infrastructure are the primary catalysts. While cost and thermal management remain challenges, opportunities in AI, renewable integration, and high‑density networking position the market for sustained expansion. Competitive dynamics are sharpening, making innovation and partnership critical for success.

17. What research methodology was employed to compile this market report?

The study utilized a combination of primary interviews with industry experts, vendor surveys, and secondary data extraction from company filings, press releases, and reputable market databases. Quantitative analysis involved trend extrapolation based on the provided CAGR, while qualitative insights were derived from thematic coding of expert opinions. Cross‑validation ensured consistency across segments and regions.

18. What is the scope of this research and are there any limitations?

The research covers the global Micro Mobile Data Center market from 2025 to 2033, segmented by rack unit, application, enterprise size, and industry vertical, and includes geographic analysis. Limitations are confined to publicly available data and the disclosed financial figures; proprietary sales data and detailed regional revenue breakdowns are not included.

19. Which key companies are highlighted and what recent developments have they announced?

Leading firms such as Dell Inc. and Huawei Technologies have launched next‑generation AI‑ready mobile units with integrated GPU clusters. Schneider Electric announced a partnership with a major telecom operator to deploy battery‑backed MMDCs for 5G edge sites. Rittal introduced a high‑efficiency liquid‑cooling module for units above 40 RU. Canovate secured a multi‑year contract with a disaster‑relief agency for rapid‑deployment data centers. Zella DC unveiled a ruggedized, solar‑compatible chassis targeting remote mining operations. These developments illustrate the market’s focus on performance, energy sustainability, and sector‑specific customization.