1. What is the Asia Pacific Carbon Fiber Market Overview – definition, scope, and significance?

The Asia Pacific carbon fiber market encompasses the production, distribution, and end‑use consumption of carbon fiber and carbon‑reinforced composites across countries such as China, Japan, South Korea, India, and Southeast Asian nations. Carbon fiber is defined as a high‑performance material composed of thin strands of carbon atoms arranged in a crystalline structure, offering superior strength‑to‑weight ratio, stiffness, and corrosion resistance. The market’s scope includes raw material sourcing (PAN and pitch), manufacturing processes, and applications in automotive, aerospace & defense, construction, sporting goods, and wind energy. Its significance lies in enabling lightweight design, fuel efficiency, and emission reductions, aligning with regional sustainability goals and the rapid growth of high‑tech industries.

2. What are the main drivers, restraints, challenges, and opportunities shaping the Asia Pacific Carbon Fiber Market?

Key drivers include rising demand for lightweight components in automotive and aerospace, government incentives for renewable energy (wind turbine blades), and expanding construction projects that require high‑strength materials. Restraints stem from high production costs, limited availability of low‑cost PAN precursors, and price sensitivity in emerging economies. Challenges involve technology transfer barriers, stringent certification requirements, and supply‑chain disruptions. Opportunities arise from advancements in cost‑effective manufacturing (e.g., thermoplastic composites), growing adoption in electric‑vehicle chassis, and strategic partnerships between local manufacturers and global technology leaders.

3. Which growth trends are currently influencing the Asia Pacific Carbon Fiber Market?

Current trends feature a shift toward thermoplastic carbon composites that enable faster molding cycles, increased recycling potential, and lower lifecycle costs. Another trend is the integration of carbon fiber in mass‑market automotive platforms to meet fuel‑efficiency standards. The aerospace sector is increasingly using carbon fiber for secondary structures, while wind‑energy developers are specifying longer, stiffer blades made from carbon‑reinforced composites. Digitalization of the supply chain, such as AI‑driven demand forecasting, is also emerging as a catalyst for market efficiency.

4. How did COVID‑19 affect the Asia Pacific Carbon Fiber Market and what is the recovery trajectory?

The pandemic caused short‑term disruptions in raw‑material logistics and temporary shutdowns of manufacturing plants, leading to a modest dip in demand during 2020‑2021. However, stimulus packages directed at automotive electrification and infrastructure revitalization accelerated post‑pandemic orders. Recovery accelerated in 2022, with demand rebounding faster in China and South Korea due to renewed automotive production. The market is now on a robust growth path, supported by pent‑up demand and the acceleration of green‑technology initiatives.

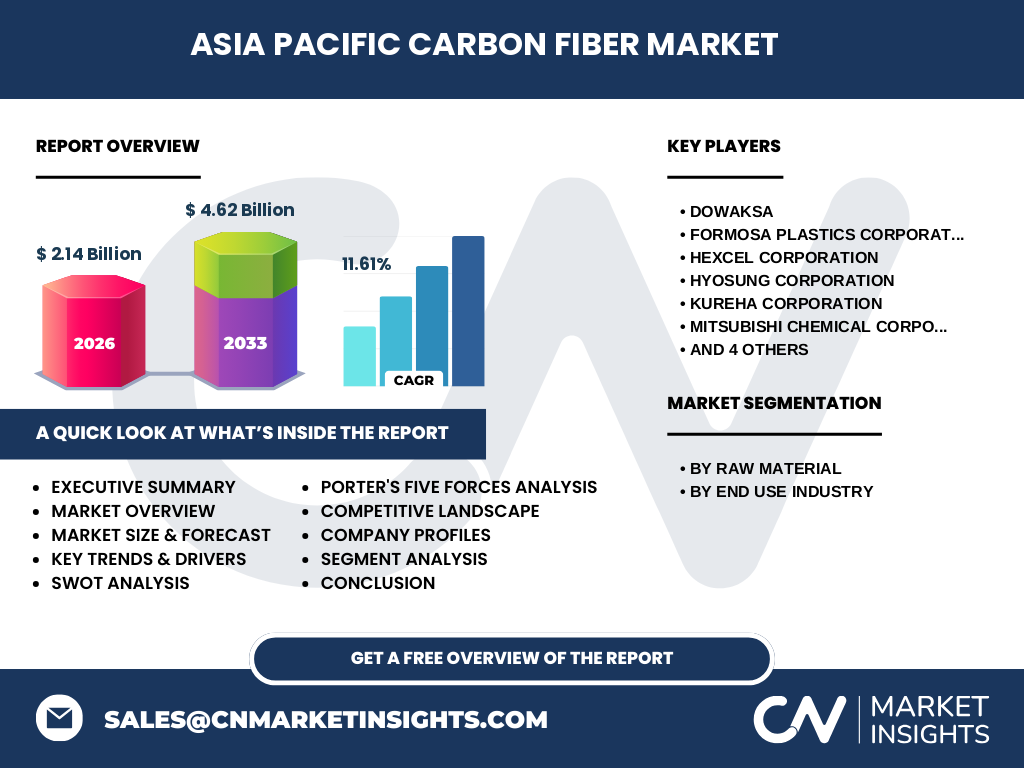

5. Who are the major competitors and what is the competitive landscape of the Asia Pacific Carbon Fiber Market?

The competitive arena is dominated by global incumbents with strong regional footholds, including DowAksa, Formosa Plastics, Hexcel, Hyosung, Kureha, Mitsubishi Chemical, SGL Carbon, Solvay, Teijin, and Toray. These firms compete on technology superiority, product portfolio breadth, and strategic alliances with local OEMs. Recent market consolidation includes joint ventures for PAN precursor production and acquisitions aimed at expanding capacity. Competitive pressure is heightened by new entrants focusing on niche applications such as low‑cost automotive-grade fibers.

6. What are the key findings highlighted in the Executive Summary for the Asia Pacific Carbon Fiber Market?

The executive summary underscores a rapidly expanding market valued at USD 2.14 billion in 2026, projected to reach USD 4.62 billion by 2033, reflecting an 11.61 % CAGR. Growth is propelled by automotive lightweighting, aerospace modernization, and renewable‑energy infrastructure. Regional leaders China and Japan account for the bulk of consumption, while emerging markets such as India and Vietnam show strong upside potential. Strategic partnerships, technology upgrades, and scaling of PAN‑based production are identified as critical success factors.

7. What are the forecast expectations for the Asia Pacific Carbon Fiber Market from 2025 to 2032?

Forecasts anticipate the market to maintain an average annual growth rate of approximately 11.6 % through 2032, driven by sustained automotive electrification, increased air‑frame replacement programs, and expanding wind‑farm projects. By 2032, the market is expected to exceed the 2033 estimate of USD 4.62 billion, with end‑use demand from automotive and renewable energy contributing the largest share. Investment in localized PAN precursor facilities and advanced recycling technologies will further bolster the growth trajectory.

8. How is the Asia Pacific Carbon Fiber Market sized and shared by segmentation?

Segmentation by raw material reveals two primary categories: PAN‑based fibers, which dominate the market due to superior mechanical properties, and pitch‑based fibers, which serve niche high‑temperature applications. By end‑use industry, automotive accounts for the largest slice, followed by aerospace & defense, construction, sporting goods, and wind energy. While precise monetary splits are not disclosed, the hierarchy reflects the relative maturity and volume of each sector, with automotive and aerospace together representing the bulk of the market value.

9. What is the geographic distribution of the Asia Pacific Carbon Fiber Market size and share by region?

The market’s geographic distribution is anchored by China, which leads in both production capacity and consumption, especially in automotive and wind‑energy projects. Japan and South Korea follow, with strong aerospace and high‑performance sporting‑goods demand. Southeast Asian nations, including Singapore, Thailand, and Vietnam, are emerging as new growth hubs due to rising infrastructure investments. Overall, the Asia Pacific region contributes the majority of the global carbon‑fiber market, reinforcing its strategic importance.

10. What does the regional analysis reveal about market performance across Asia Pacific?

Regional analysis shows China’s market expanding at a faster pace than the regional average, driven by government mandates for lightweighting in passenger cars and aggressive wind‑farm expansion. Japan’s growth is steady, anchored by legacy aerospace programs and high‑tech manufacturing. South Korea benefits from strong automotive R&D and a focus on electric‑vehicle platforms. Emerging economies such as India are witnessing early‑stage adoption in construction and automotive, indicating a long‑term upside as infrastructure projects mature.

11. Which companies lead the Asia Pacific Carbon Fiber Market and what are their key strategies?

Leading players include Toray, which leverages its extensive R&D network to launch ultra‑high‑modulus fibers; Mitsubishi Chemical, focusing on integrated PAN precursor production; and SGL Carbon, expanding its footprint through joint ventures in China. DowAksa pursues cost‑reduction via scale‑up of PAN facilities, while Hexcel emphasizes aerospace partnerships. Hyosung and Kureha invest in advanced spinning technologies, and Formosa Plastics expands its pitch‑based product line for high‑temperature markets. Strategic collaborations with OEMs and investments in recycling are common themes.

12. How does Porter’s Five Forces framework assess the Asia Pacific Carbon Fiber Market?

Threat of new entrants is moderate; high capital intensity and technical expertise create barriers, yet niche players targeting low‑cost automotive fibers can enter. Bargaining power of suppliers is relatively high because PAN precursors are limited to a few producers. Bargaining power of buyers is moderate; large automotive OEMs negotiate pricing, but the lack of interchangeable substitutes sustains supplier leverage. Threat of substitutes is low; alternatives such as aluminum or steel cannot match the specific strength‑to‑weight ratio. Industry rivalry is intense, driven by technology race, capacity expansion, and strategic alliances.

13. What are the SWOT elements for the Asia Pacific Carbon Fiber Market?

Strengths: Superior material properties, alignment with sustainability goals, strong demand from high‑growth end uses.

Weaknesses: High production cost, limited low‑cost precursor supply.

Opportunities: Emerging automotive lightweighting standards, renewable‑energy blade demand, recycling technology development.

Threats: Potential trade restrictions, raw‑material price volatility, rapid technological shifts that could favor alternative composites.

14. How is the value chain of the Asia Pacific Carbon Fiber Market structured?

The value chain begins with raw‑material sourcing (PAN and pitch), followed by precursor manufacturing, fiber spinning, surface treatment, and conversion to fabrics or prepregs. These intermediate products are then supplied to composite manufacturers, who integrate them into finished components for automotive, aerospace, construction, sporting goods, and wind‑energy sectors. End‑of‑life recycling and re‑processing are emerging downstream activities, creating circular‑economy value loops.

15. What investment insights can be derived for stakeholders interested in the Asia Pacific Carbon Fiber Market?

Investors should prioritize projects that reduce PAN precursor costs, such as localized production or alternative feedstocks. Funding for recycling infrastructure offers long‑term cost savings and ESG benefits. Partnerships with OEMs—particularly in electric‑vehicle platforms—provide secure demand pipelines. Capital allocation toward thermoplastic carbon composites can capture market share as manufacturers seek faster cycle times. Finally, monitoring policy incentives for lightweighting and renewable energy will help identify high‑return opportunities.

16. What are the concluding takeaways from the Asia Pacific Carbon Fiber Market analysis?

The Asia Pacific carbon‑fiber market is on a high‑growth trajectory, underpinned by robust demand across multiple high‑value industries. With a projected market size of USD 4.62 billion by 2033 and an 11.61 % CAGR, the region offers attractive investment and partnership opportunities. Overcoming cost barriers through supply‑chain integration and recycling, while leveraging government incentives, will be decisive for sustaining momentum. Companies that innovate in low‑cost manufacturing and secure strategic OEM relationships are poised to lead.

17. How was the research for this report conducted?

The study employed a mixed‑method approach, combining primary interviews with industry executives, secondary data extraction from company reports, trade publications, and government statistics, and quantitative modeling to forecast market size. Trend analysis incorporated macroeconomic indicators, policy frameworks, and technology adoption curves. Validation was performed through cross‑referencing multiple sources to ensure reliability of the presented figures.

18. What is the scope of this research and its limitations?

The research covers the Asia Pacific carbon‑fiber market from 2025 to 2032, focusing on PAN and pitch raw materials and six end‑use industries. It includes market sizing, competitive dynamics, and strategic insights. Limitations stem from the reliance on publicly disclosed data and the exclusion of confidential proprietary figures. Consequently, precise market‑share percentages are not disclosed, but the analysis reflects the relative importance of each segment.

19. Which key companies have made recent developments in the Asia Pacific Carbon Fiber Market?

Recent developments include Toray’s launch of a next‑generation ultra‑high‑modulus fiber targeting aerospace applications; Mitsubishi Chemical’s joint venture in Vietnam to produce PAN precursors locally; DowAksa’s announcement of a new expansion plant in China aimed at halving production costs; Hexcel’s strategic partnership with a leading automotive OEM to supply carbon‑fiber composites for electric‑vehicle chassis; and SGL Carbon’s acquisition of a recycling technology firm to enable closed‑loop carbon‑fiber reuse. These moves illustrate the sector’s focus on cost reduction, capacity expansion, and sustainability.