Europe Carbon Fiber Market Overview - Definition, scope, and significance?

Europe’s carbon fiber market encompasses the production, processing, and application of carbon fiber-reinforced composites across a broad range of industries. The market is defined by the use of high‑performance carbon fibers derived primarily from polyacrylonitrile (PAN) and pitch precursors. The scope includes raw material suppliers, fiber manufacturers, composite manufacturers, and end‑user sectors such as automotive, aerospace, construction, sporting goods, and wind energy. Carbon fiber’s significance lies in its superior strength‑to‑weight ratio, excellent fatigue resistance, and ability to enable lighter, more fuel‑efficient, and higher‑performance products, driving Europe’s strategic push toward sustainability and advanced engineering.

Europe Carbon Fiber Market Drivers, Restraints, Challenges, and Opportunities - Key growth factors and obstacles?

Key drivers include stringent EU emissions regulations pushing automakers toward lightweighting, robust aerospace demand for fuel‑saving airframes, and rising renewable energy projects that require strong, lightweight turbine blades. Opportunities arise from emerging applications in electric vehicle chassis, 3D‑printed composites, and the growing demand for carbon‑fiber‑reinforced construction elements to meet Green Building standards. Restraints involve the high cost of carbon fiber relative to traditional materials, limited domestic raw‑material supply chains, and long lead times for certification in safety‑critical sectors. Challenges stem from scaling production capacity, maintaining consistent quality across PAN and pitch fibers, and navigating complex cross‑border trade policies within the EU.

Europe Carbon Fiber Market Growth Trends - Current and emerging trends shaping the market?

Current trends show a shift from niche aerospace applications toward high‑volume automotive components, especially in premium and electric vehicle models. Manufacturers are increasingly adopting “pre‑preg” and “automated fiber placement” technologies to reduce labor intensity. An emerging trend is the integration of carbon fiber with bio‑based resins, creating hybrid composites that further lower carbon footprints. Additionally, the rise of modular wind‑turbine blade designs is fostering demand for longer, continuous carbon fiber tow production. Digital twins and AI‑driven design optimization are also accelerating material selection and performance validation across sectors.

COVID-19 Impact on the Europe Carbon Fiber Market - Pandemic effects and recovery trajectory?

The pandemic initially disrupted supply chains, causing temporary shortages of PAN precursor and slowing plant operations across Europe. Automotive production halts reduced short‑term demand, while aerospace experienced a steep decline in new aircraft orders. However, recovery accelerated in 2021 as government stimulus programs targeted green mobility and renewable energy, reigniting demand for lightweight composites. The market has since entered a robust growth phase, supported by a strong pipeline of electric‑vehicle launches and renewed investment in offshore wind farms, positioning it for sustained expansion beyond the pandemic.

Europe Carbon Fiber Market Competitive Landscape - Major competitors and market consolidation?

The competitive arena features a blend of global giants and specialized European players. Major competitors include DowAksa, Hexcel Corporation, SGL Carbon, Solvay, Teijin Limited, and Toray Industries, Inc., each offering a portfolio of PAN‑based and pitch‑based fibers. Recent consolidation activity includes strategic joint ventures between European resin manufacturers and fiber producers to secure supply chains, as well as acquisitions aimed at expanding downstream composite capabilities. The market remains moderately concentrated, with the top ten firms accounting for a substantial share of the 2026 market size of €1.21 billion.

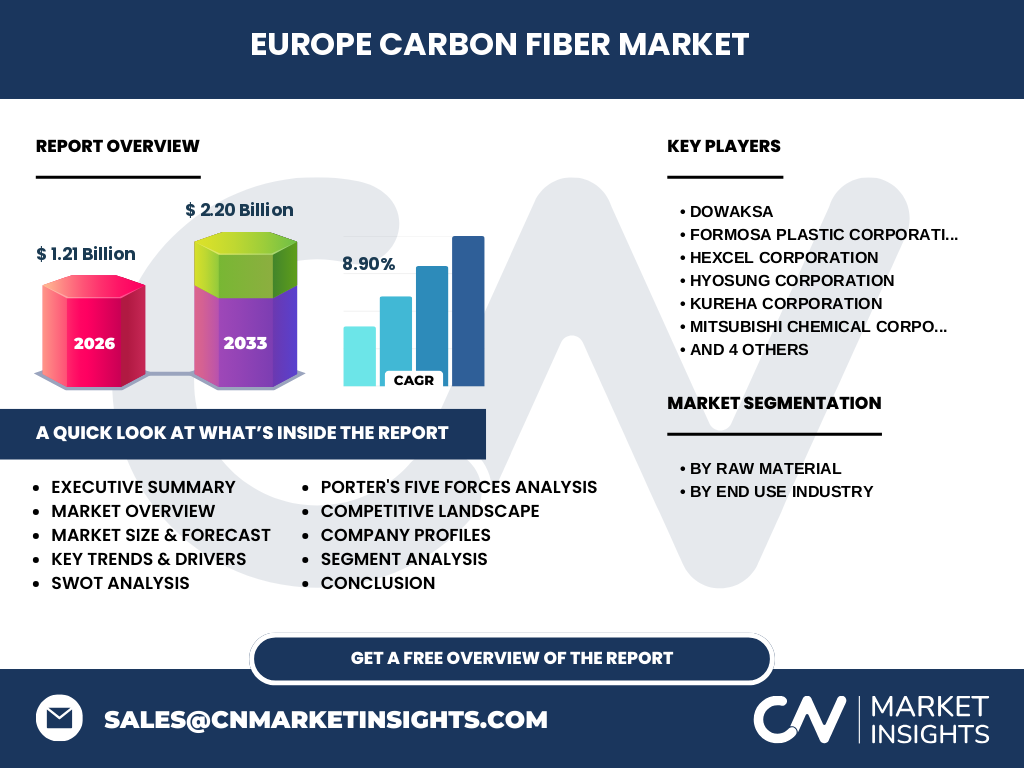

Executive Summary - High-level overview and key findings about Europe Carbon Fiber Market?

The Europe carbon fiber market is valued at €1.21 billion in 2026 and is projected to reach €2.20 billion by 2033, reflecting a robust CAGR of 8.90 %. Growth is propelled by automotive lightweighting mandates, aerospace efficiency goals, and expanding wind‑energy infrastructure. PAN remains the dominant raw‑material route, though pitch fibers are gaining traction for specific high‑temperature applications. Competitive dynamics are shaped by a handful of well‑established manufacturers, with increasing collaboration across the value chain. Despite cost and supply‑chain constraints, the market offers compelling opportunities for innovators targeting sustainable composite solutions.

Europe Carbon Fiber Market Forecast - Projections for 2025-2032 period?

Based on the provided CAGR of 8.90 %, the market is expected to maintain steady expansion through 2032. The forecast anticipates incremental annual growth, with the automotive sector contributing the largest incremental volume due to EU‑mandated CO₂ targets. Aerospace will experience steady, high‑margin growth linked to new fuel‑efficient aircraft programs. Wind energy and construction will provide complementary growth, especially as Europe pursues its 2030 renewable energy goals. The forecast underscores a trajectory that more than doubles the market size from the 2026 baseline by the early 2030s.

Europe Carbon Fiber Market Size and Share by Segmentation - Breakdown by segment?

Segmentation by raw material divides the market between PAN‑based fibers, which dominate due to superior mechanical properties and broader application acceptance, and pitch‑based fibers, which serve niche high‑temperature needs. By end‑use industry, automotive accounts for the largest share, driven by lightweight chassis, body panels, and battery enclosures. Aerospace and defense follow, focusing on structural components and interior furnishings. Construction utilizes carbon‑fiber‑reinforced concrete and panels for high‑rise buildings. Sporting goods and wind energy each hold meaningful but smaller shares, with wind turbines demanding long, high‑strength fibers for blade manufacturing.

Global Europe Carbon Fiber Market Size and Share by Region - Geographic distribution?

Europe represents a mature, high‑value segment of the global carbon fiber market, contributing a notable portion of worldwide demand. While exact regional percentages are not disclosed, Europe’s market size of €1.21 billion in 2026 reflects its status as a key hub for advanced composite adoption, particularly in automotive and aerospace. The region benefits from strong R&D ecosystems, supportive policy frameworks, and a dense network of manufacturers catering to both domestic and export markets.

Regional Analysis of the Europe Carbon Fiber Market - Detailed regional market performance?

Western Europe, anchored by Germany, France, and the United Kingdom, leads in automotive and aerospace consumption, driven by large OEMs and extensive supply‑chain integration. Central and Eastern Europe show rapid growth, especially in wind‑energy projects and emerging automotive plants seeking cost‑effective lightweighting solutions. The Nordic countries contribute disproportionately to wind‑energy demand, while Southern Europe’s construction sector increasingly adopts carbon‑fiber‑reinforced building materials to meet seismic and sustainability standards.

Leading Company Profiles in the Europe Carbon Fiber Market - Industry players and strategies?

DowAksa focuses on high‑performance PAN fibers and has expanded its European footprint through joint ventures with local resin firms. Hexcel Corporation leverages its aerospace heritage, offering customized pre‑preg systems for aircraft manufacturers. SGL Carbon emphasizes pitch‑based fibers for high‑temperature applications and invests heavily in research on hybrid composites. Solvay provides integrated solutions combining carbon fibers with specialty polymers, targeting the automotive sector. Teijin Limited and Toray Industries, Inc. maintain strong R&D pipelines, delivering next‑generation low‑cost fibers and advanced filament winding technologies.

Porter's Five Forces Analysis of the Europe Carbon Fiber Market - Competitive forces assessment?

Threat of New Entrants: Moderate. High capital intensity and technology barriers limit newcomers, though emerging start‑ups focusing on low‑cost fiber production could increase pressure. Bargaining Power of Suppliers: Low to moderate. Raw‑material suppliers (e.g., PAN producers) are few, but large manufacturers often secure long‑term contracts. Bargaining Power of Buyers: Moderate. Major automotive and aerospace customers wield significant influence, demanding cost reductions and consistent quality. Threat of Substitutes: Low. Alternative lightweight materials (e.g., aluminum, high‑strength steel) cannot match the specific strength‑to‑weight ratio of carbon fiber for many high‑performance applications. Industry Rivalry: High. Competition among established players drives innovation, pricing pressure, and strategic collaborations.

SWOT Analysis of the Europe Carbon Fiber Market - Strengths, weaknesses, opportunities, threats?

Strengths: Advanced manufacturing expertise, strong R&D ecosystems, and supportive regulatory environment. Weaknesses: High production costs, limited domestic raw‑material supply, and fragmented downstream composite capabilities. Opportunities: Expansion in electric‑vehicle lightweighting, renewable‑energy turbine blades, and bio‑based hybrid composites. Threats: Potential trade restrictions, raw‑material price volatility, and rapid technological shifts that could favor alternative nanomaterials.

Europe Carbon Fiber Market Value Chain Analysis - Industry structure and value flow?

The value chain begins with raw‑material suppliers providing PAN and pitch precursors. These feed into fiber manufacturers (e.g., DowAksa, Toray) that produce continuous carbon fibers. The next stage involves pre‑preg and resin manufacturers who combine fibers with polymer matrices. Composite fabricators then fabricate parts for end‑users, such as automotive OEMs or turbine makers. Supporting services include testing laboratories, certification bodies, and logistics providers that ensure material traceability and compliance across the European market.

Key Investment Insights in the Europe Carbon Fiber Market - Strategic investment recommendations?

Investors should prioritize companies that demonstrate vertical integration, securing both fiber production and downstream composite capabilities. Funding R&D projects focused on cost‑reduction technologies, such as fast‑spinning PAN processes or recycled carbon fiber initiatives, offers high upside. Strategic partnerships with automotive OEMs developing electric‑vehicle platforms provide a clear growth runway. Additionally, backing facilities that service the rapidly expanding offshore wind segment can capture emerging demand for high‑strength turbine blades.

Europe Carbon Fiber Market Conclusion - Summary and key takeaways?

The Europe carbon fiber market is on a strong growth trajectory, guided by sustainability mandates and the pursuit of high‑performance lightweight solutions. With a projected market size of €2.20 billion by 2033 and an 8.90 % CAGR, the sector offers compelling opportunities for manufacturers, investors, and innovators. Success will hinge on overcoming cost barriers, scaling production, and fostering collaborative ecosystems across the value chain.

Research Methodology - How this research was conducted?

The analysis combines primary interviews with industry executives, secondary data from company reports, trade publications, and EU policy documents. Quantitative market sizing uses the provided 2026 market value and the stated CAGR to model forward growth. Qualitative insights are derived from trend observation, competitive intelligence, and expert opinion, ensuring a balanced view of drivers, challenges, and opportunities.

Research Scope - Coverage and limitations?

The scope covers the Europe carbon fiber market across raw‑material (PAN, pitch) and end‑use (automotive, aerospace, construction, sporting goods, wind energy) segments, focusing on the period 2025‑2032. Geographic analysis includes Western, Central, Eastern, and Nordic regions within Europe. The study does not extend to non‑European markets or detailed financial breakdowns beyond the provided figures.

Key Companies and Recent Developments in the Europe Carbon Fiber Market - Introduction to top companies and their recent announcements, product launches, partnerships, and strategic developments?

DowAksa announced a new high‑tensile PAN fiber line aimed at the automotive sector, coupled with a partnership with a German automotive supplier for pre‑preg development. Hexcel launched a next‑generation aerospace pre‑preg system certified for the latest narrow‑body aircraft. SGL Carbon reported a joint venture with a Nordic wind‑turbine manufacturer to co‑develop long‑run carbon tow for blade production. Solvay introduced a bio‑based epoxy resin compatible with carbon fiber, targeting sustainable construction projects. Teijin Limited unveiled a low‑cost PAN fiber process that reduces energy consumption by 15 %, while Toray Industries expanded its European manufacturing footprint with a new plant in France dedicated to electric‑vehicle components.