North America Carbon Fiber Market Overview - Definition, scope, and significance?

The North America carbon fiber market comprises the production, distribution, and application of carbon fiber reinforced materials across multiple industries within the United States, Canada, and Mexico. Carbon fiber is defined as a high‑strength, lightweight material made from precursor fibers such as polyacrylonitrile (PAN) or pitch, which are carbonized at high temperatures. The market’s scope includes raw material supply, intermediate products, and end‑use applications in sectors like automotive, aerospace, construction, sporting goods, and wind energy. Its significance stems from the material’s ability to improve fuel efficiency, reduce emissions, and enable innovative product designs, positioning carbon fiber as a critical enabler of sustainability and performance in North America’s advanced manufacturing landscape.

North America Carbon Fiber Market Drivers, Restraints, Challenges, and Opportunities - Key growth factors and obstacles?

Key drivers include rising demand for lightweight components in automotive and aerospace, increased government incentives for fuel‑efficient technologies, and growing investment in renewable energy infrastructure such as wind turbines. Restraints arise from the high cost of raw materials, limited domestic production capacity, and supply chain bottlenecks for PAN and pitch precursors. Challenges involve stringent regulatory standards for aerospace certification and the need for specialized manufacturing expertise. Opportunities are emerging in additive manufacturing, recycled carbon fiber technologies, and new applications in electric vehicle (EV) chassis and high‑performance sporting equipment, which could unlock additional demand across the region.

North America Carbon Fiber Market Growth Trends - Current and emerging trends shaping the market?

Current trends show a steady shift from niche aerospace use toward mass‑market automotive applications, especially in EV platforms where weight reduction directly extends range. Another notable trend is the integration of carbon fiber composites into wind turbine blades to increase length and efficiency. Emerging trends include the adoption of thermoplastic carbon fiber matrices for faster processing, the development of low‑cost precursor technologies, and collaborations between carbon fiber producers and automotive OEMs to create “design‑for‑manufacturing” frameworks that streamline part integration.

COVID-19 Impact on the North America Carbon Fiber Market - Pandemic effects and recovery trajectory?

The COVID‑19 pandemic caused temporary disruptions in supply chains for PAN and pitch, leading to short‑term inventory shortages and delayed project timelines, particularly in aerospace and construction. However, the market demonstrated resilience as stimulus packages accelerated EV adoption and renewable energy projects, driving a swift rebound. By late 2022, demand recovered to pre‑pandemic levels, and the recovery trajectory has remained upward, supported by robust post‑COVID industrial investment and a clear policy focus on decarbonization.

North America Carbon Fiber Market Competitive Landscape - Major competitors and market consolidation?

The competitive landscape is characterized by a mix of global leaders and regional specialists. Major competitors include DowAksa, Formosa Plastic Corporation, Hexcel Corporation, Hyosung Corporation, Kureha Corporation, Mitsubishi Chemical Corporation, SGL Carbon, Solvay, Teijin Limited, and Toray Industries, Inc. Recent consolidation activity features strategic joint ventures to expand PAN precursor capacity and acquisitions aimed at securing downstream processing capabilities. These moves reflect a broader industry trend toward vertical integration to mitigate supply risks and enhance cost competitiveness.

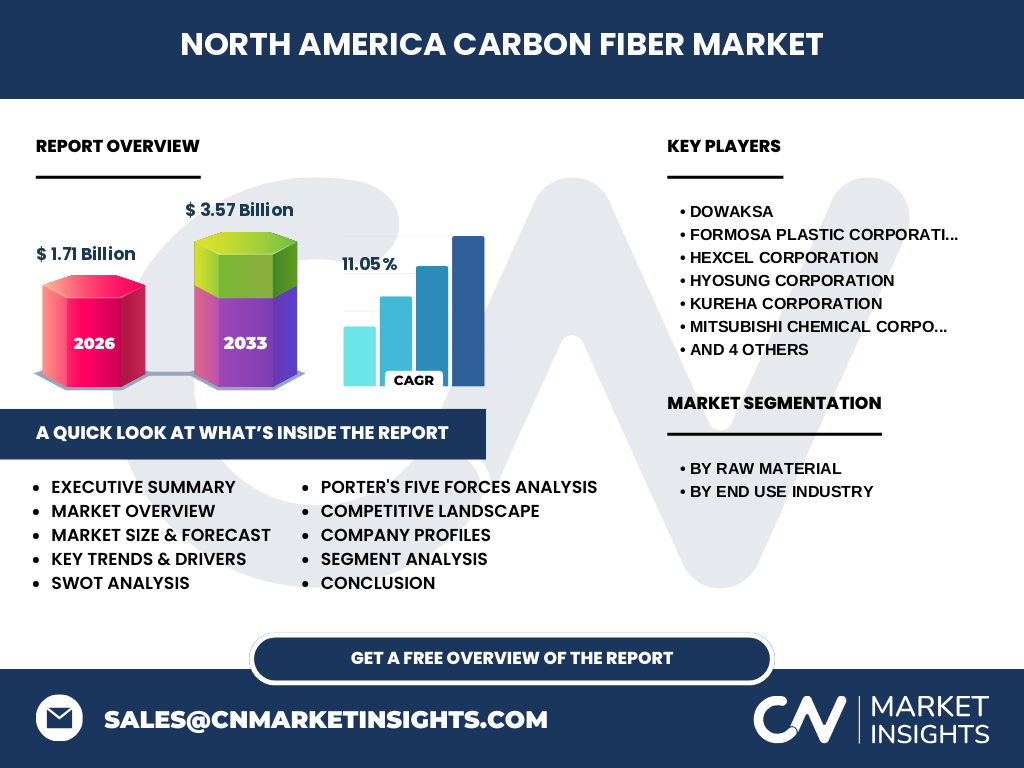

Executive Summary - High-level overview and key findings about North America Carbon Fiber Market?

The North America carbon fiber market was valued at USD 1.71 billion in 2026 and is projected to reach USD 3.57 billion by 2033, translating to a robust CAGR of 11.05 %. Growth is propelled by accelerating lightweighting initiatives in automotive and aerospace, strong governmental support for clean‑energy projects, and expanding applications in construction and sporting goods. While high material costs and supply constraints remain critical challenges, emerging low‑cost precursor technologies and recycling initiatives present significant upside. The market’s outlook is positive, with strong investment interest and ongoing consolidation shaping a more resilient supply chain.

North America Carbon Fiber Market Forecast - Projections for 2025-2032 period?

Based on current growth dynamics, the market is expected to maintain an average annual growth rate of approximately 11 % through 2032. This trajectory will drive the market size from roughly USD 1.5 billion in 2025 to well above USD 3 billion by 2032. The forecast reflects continued expansion of carbon‑fiber‑based components in EVs, increased turbine blade replacements, and rising demand for high‑performance sporting goods. The compound impact of technology improvements, cost reductions, and policy incentives will sustain the upward momentum.

North America Carbon Fiber Market Size and Share by Segmentation - Breakdown by segment?

Segmentation by raw material reveals two primary categories: PAN‑based carbon fiber, which dominates due to its superior performance characteristics, and pitch‑based carbon fiber, which serves niche high‑temperature applications. By end‑use industry, automotive accounts for the largest share, driven by EV lightweighting programs; aerospace and defense follow, reflecting the material’s critical role in airframe and engine components. Construction, sporting goods, and wind energy each represent growing but smaller shares, with wind energy expected to accelerate as turbine blade lengths increase.

Global North America Carbon Fiber Market Size and Share by Region - Geographic distribution?

Within the global context, North America holds a significant share of the carbon fiber market, underpinned by mature aerospace programs, a large automotive manufacturing base, and substantial renewable energy investments. While precise regional percentages are not disclosed, the market’s USD 1.71 billion valuation in 2026 underscores North America’s role as a key demand hub, complemented by strong supply capabilities from both domestic and international manufacturers operating in the region.

Regional Analysis of the North America Carbon Fiber Market - Detailed regional market performance?

The United States leads the regional performance, driven by its extensive aerospace sector, major automotive OEMs, and aggressive EV adoption policies. Canada contributes through its growing renewable energy projects, particularly offshore wind initiatives, while Mexico shows emerging potential in automotive component manufacturing. Each sub‑region exhibits distinct growth drivers: the U.S. focuses on high‑tech aerospace and EVs, Canada on wind energy and green infrastructure, and Mexico on cost‑effective automotive supply chain integration.

Leading Company Profiles in the North America Carbon Fiber Market - Industry players and strategies?

Key players such as DowAksa and Toray Industries focus on expanding PAN precursor capacity and developing high‑modulus fibers for aerospace. Hexcel Corporation emphasizes advanced composite systems for military and commercial aircraft. SGL Carbon and Solvay invest heavily in carbon fiber recycling and thermoplastic composites to address cost pressures. Mitsubishi Chemical and Teijin Limited pursue joint ventures with North American OEMs to co‑develop lightweight structures, while Hyosung and Kureha leverage their chemical expertise to lower raw material costs.

Porter's Five Forces Analysis of the North America Carbon Fiber Market - Competitive forces assessment?

Threat of New Entrants: Moderate – high capital requirements and technology barriers limit new players. Bargaining Power of Suppliers: High – limited number of PAN and pitch precursor suppliers creates supplier concentration. Bargaining Power of Buyers: Growing – large automotive OEMs can negotiate pricing as volumes increase. Threat of Substitutes: Low – few alternatives match carbon fiber’s strength‑to‑weight ratio. Industry Rivalry: Intense – established global firms compete on technology, cost, and capacity expansion.

SWOT Analysis of the North America Carbon Fiber Market - Strengths, weaknesses, opportunities, threats?

Strengths: Advanced manufacturing ecosystem, strong demand from automotive and aerospace, supportive policy environment. Weaknesses: High raw material cost, limited domestic precursor supply, complex certification processes. Opportunities: Recycling of carbon fiber, development of low‑cost PAN precursors, expansion into wind turbine blades and EV chassis. Threats: Potential trade restrictions on imported precursors, macro‑economic fluctuations affecting capital‑intensive projects, and rapid technological shifts toward alternative lightweight materials.

North America Carbon Fiber Market Value Chain Analysis - Industry structure and value flow?

The value chain begins with raw material procurement (PAN, pitch), followed by precursor fiber production, carbonization, surface treatment, and sizing. Next, intermediate products such as tows and fabrics are manufactured, which are then supplied to composite fabricators and OEMs. Final stages involve part design, molding, and assembly in automotive, aerospace, and wind turbine applications. Value‑added services include material testing, certification, and recycling, increasingly becoming differentiators for market participants.

Key Investment Insights in the North America Carbon Fiber Market - Strategic investment recommendations?

Investors should prioritize companies expanding PAN precursor capacity and those developing recycling technologies, as cost reduction pathways are critical for market expansion. Partnerships with automotive OEMs targeting EV platforms present high‑growth opportunities, while stakes in wind‑energy‑focused carbon fiber manufacturers can capture the renewable‑energy upside. Additionally, funding ventures that integrate thermoplastic matrices can accelerate time‑to‑market and improve profitability, aligning with industry demand for faster, cost‑effective manufacturing solutions.

North America Carbon Fiber Market Conclusion - Summary and key takeaways?

The North America carbon fiber market is on a strong growth trajectory, underpinned by a CAGR of 11.05 % and a projected market size of USD 3.57 billion by 2033. Lightweighting mandates, renewable‑energy investments, and advancements in low‑cost precursor technologies drive demand across automotive, aerospace, and wind sectors. While high material costs and supply constraints persist, ongoing consolidation and innovation are creating a more resilient ecosystem. Stakeholders who focus on cost‑reduction, recycling, and strategic OEM collaborations are positioned to capture the most value.

Research Methodology - How this research was conducted?

The research employed a mixed‑method approach, combining primary interviews with industry experts, OEM engineers, and material suppliers, with secondary data from company annual reports, trade publications, and government databases. Quantitative analysis utilized trend extrapolation based on the provided 2026 market size (USD 1.71 billion) and forecast (USD 3.57 billion) to calculate the 11.05 % CAGR. Qualitative insights were derived from competitor press releases, partnership announcements, and policy documents to validate growth drivers and market dynamics.

Research Scope - Coverage and limitations?

The scope covers the North American carbon fiber market, focusing on raw material types (PAN, pitch) and end‑use industries (automotive, aerospace & defense, construction, sporting goods, wind energy). Geographic coverage includes the United States, Canada, and Mexico. Limitations stem from the use of publicly available financial figures only; proprietary cost structures, exact market share percentages, and confidential R&D expenditures are not disclosed.

Key Companies and Recent Developments in the North America Carbon Fiber Market - Introduction to top companies and their recent announcements, product launches, partnerships, and strategic developments?

Recent developments include DowAksa’s announcement of a new PAN precursor plant in the United States, aimed at reducing supply lead times. Toray Industries signed a strategic alliance with a major U.S. EV manufacturer to co‑develop carbon‑fiber‑reinforced chassis components. Hexcel Corporation introduced a next‑generation high‑modulus fiber for aircraft structures, while SGL Carbon launched a recycled carbon fiber line targeting wind turbine blade manufacturers. Mitsubishi Chemical entered a joint venture with a Canadian renewable‑energy firm to supply carbon fiber for offshore wind projects, and Solvay unveiled a thermoplastic carbon fiber composite system designed for rapid automotive molding.