What is the SOC as a Service Market Overview – definition, scope, and significance?

The SOC as a Service (Security Operations Center as a Service) market refers to the outsourced delivery of continuous threat monitoring, detection, analysis, and response capabilities through a cloud‑based or remotely managed platform. It enables organizations of all sizes to access advanced security analytics, incident response, and compliance reporting without building an in‑house SOC. The scope encompasses services across network, endpoint, application, and cloud security, as well as prevention, detection, and incident‑response functions. Its significance lies in addressing the escalating cyber‑threat landscape, talent shortages, and the need for rapid scalability, thereby allowing enterprises to protect digital assets while focusing on core business objectives.

What are the main drivers, restraints, challenges, and opportunities in the SOC as a Service Market?

Key drivers include rising ransomware incidents, increasing regulatory compliance requirements, and the global shortage of skilled security analysts. Organizations are also motivated by the cost‑effectiveness of subscription‑based models and the ability to leverage AI‑enabled analytics. Restraints stem from concerns over data sovereignty, integration complexities with legacy systems, and perceived loss of control over security operations. Challenges involve maintaining consistent service quality across multiple geographic locations and ensuring real‑time response in highly distributed environments. Opportunities arise from the growth of cloud adoption, expansion of IoT attack surfaces, and the emergence of advanced threat‑intel sharing ecosystems that can be integrated into SOC‑as‑a‑Service platforms.

What are the current growth trends shaping the SOC as a Service Market?

Current trends include the convergence of SOC services with extended detection and response (XDR) solutions, enabling unified visibility across on‑premise and cloud workloads. Automation and machine‑learning‑driven analytics are being embedded to reduce alert fatigue and accelerate remediation. Another trend is the rise of managed detection and response (MDR) bundles that combine SOC capabilities with proactive threat hunting. Additionally, providers are expanding service portfolios to cover specialized domains such as OT security and zero‑trust network architectures, reflecting evolving customer requirements.

How has COVID‑19 impacted the SOC as a Service Market and what is the recovery trajectory?

The pandemic accelerated digital transformation and remote‑work adoption, leading to a surge in cyber‑attacks targeting dispersed workforces. This heightened demand for outsourced security monitoring, boosting SOC‑as‑a‑Service contracts in 2020‑2021. While the immediate shock subsided, the market retained the momentum gained, with enterprises continuing to prioritize resilient security operations. The recovery trajectory is stable, with ongoing investment in SOC services expected to sustain growth through the forecast period.

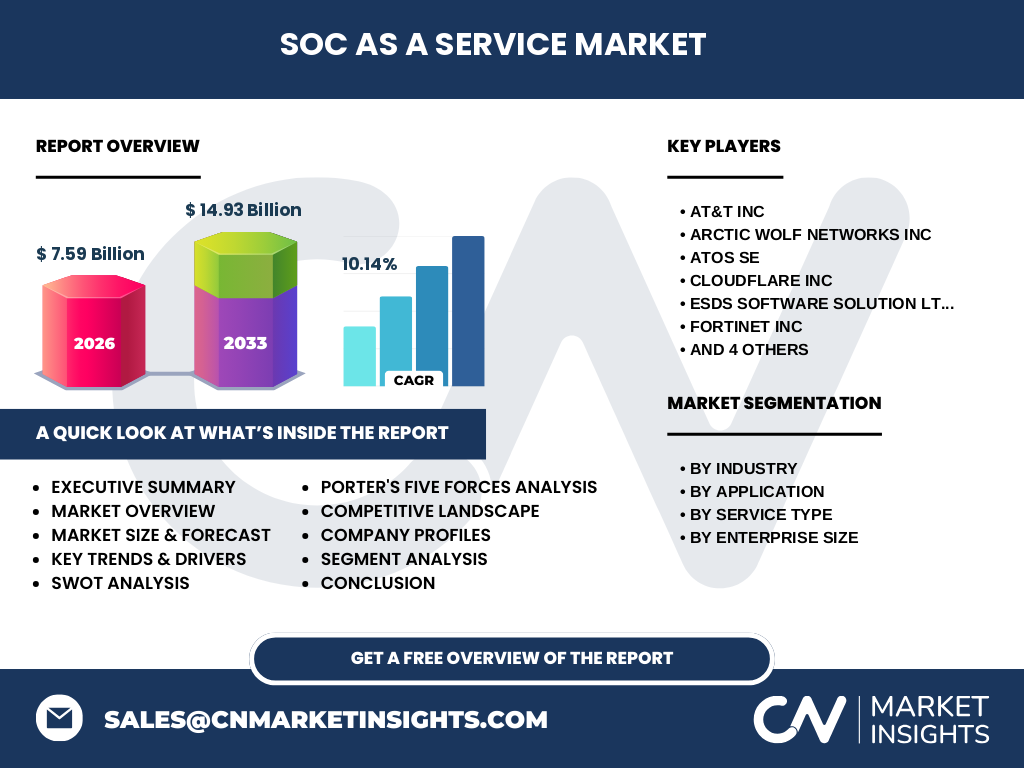

Who are the major competitors in the SOC as a Service Market and what does the competitive landscape look like?

The market is fragmented with several global and niche players. Leading competitors include AT&T Inc, Arctic Wolf Networks Inc, Atos SE, Cloudflare Inc, ESDS Software Solution Ltd, Fortinet Inc, NTT Data Corp, Thales SA, Verizon Communications Inc, and ConnectWise LLC. Consolidation activities have been modest, focusing on strategic acquisitions of threat‑intel firms and AI analytics startups to enhance service depth. Competitive advantage is driven by breadth of global delivery centers, integration capabilities with existing IT ecosystems, and proprietary security analytics platforms.

What are the key findings in the Executive Summary of the SOC as a Service Market?

The SOC as a Service market is projected to reach $14.93 billion by 2033, up from $7.59 billion in 2026, reflecting a CAGR of 10.14 % over the forecast horizon. Strong demand across BFSI, IT & Telecom, and Government sectors fuels growth, while cloud‑security services dominate the application segment. Large enterprises and SMEs alike are adopting subscription models, driving diversified revenue streams. The competitive arena is characterized by a mix of telecom giants, cybersecurity specialists, and managed‑service providers, each leveraging AI and automation to differentiate offerings.

What is the forecast for the SOC as a Service Market from 2025 to 2032?

Based on the provided CAGR of 10.14 %, the market is expected to expand from the 2026 baseline of $7.59 billion to approximately $14.93 billion by the end of 2033. This trajectory suggests a steady increase in annual revenues, with peak growth anticipated in the mid‑term (2028‑2030) as cloud adoption and regulatory pressures intensify. The forecast underscores robust demand for integrated prevention, detection, and incident‑response services across multiple industries.

How is the SOC as a Service Market sized and shared by segmentation?

Segmentation by industry shows that BFSI, IT & Telecom, Manufacturing, Retail, Government & Public Sector, and Healthcare each constitute important verticals, with BFSI and IT & Telecom typically leading in adoption due to high compliance mandates. By application, Network Security, Endpoint Security, Application Security, and Cloud Security split the market, with Cloud Security gaining the fastest uptake as workloads migrate to public clouds. Service‑type segmentation highlights Prevention, Detection, and Incident Response services, where Detection often commands the largest share because of continuous monitoring needs. Finally, enterprise size segmentation reveals that both Large Enterprises and SMEs are actively purchasing SOC‑as‑a‑Service, though Large Enterprises tend to consume higher‑value, customized solutions.

What is the geographic distribution of the Global SOC as a Service Market size and share?

The market exhibits a global footprint with strong presence in North America, Europe, and the Asia‑Pacific region. While specific regional dollar values are not disclosed, the overall growth pattern indicates that North America leads in early adoption due to mature cybersecurity frameworks, Europe follows with stringent GDPR‑related compliance, and Asia‑Pacific is emerging rapidly as digital transformation accelerates in countries like India and China.

What does the regional analysis of the SOC as a Service Market reveal?

North America benefits from a high concentration of large enterprises and a mature managed‑service ecosystem, driving sizable contract values. Europe’s market is propelled by regulatory pressures and public‑sector initiatives to secure critical infrastructure. The Asia‑Pacific region presents the highest growth potential, buoyed by expanding cloud services, rapid SME digitalization, and increasing cyber‑risk awareness. The Middle East and Africa, though smaller, are beginning to invest in SOC capabilities as part of broader national cybersecurity strategies.

Which leading companies are profiled in the SOC as a Service Market and what are their strategies?

Key players include:

AT&T Inc – leveraging its extensive telecom network to deliver edge‑based SOC services.

Arctic Wolf Networks Inc – focusing on concierge‑style threat detection and response for SMBs.

Atos SE – integrating SOC offerings with its broader digital transformation portfolio.

Cloudflare Inc – bundling SOC capabilities with its global CDN and DDoS protection.

ESDS Software Solution Ltd – targeting the Indian market with cost‑effective managed security.

Fortinet Inc – combining next‑gen firewalls with SOC analytics.

NTT Data Corp – utilizing its global delivery model to serve multinational corporations.

Thales SA – emphasizing high‑assurance encryption and government‑grade SOC services.

Verizon Communications Inc – offering integrated threat intelligence through its security ops.

ConnectWise LLC – focusing on SMBs with a platform that merges PSA, RMM, and SOC functions.

What does Porter’s Five Forces analysis indicate for the SOC as a Service Market?

Threat of new entrants: Moderate – high capital investment in analytics platforms deters many newcomers, but cloud‑native startups can enter with niche AI solutions.

Bargaining power of buyers: High – enterprises can switch providers relatively easily, pushing vendors to enhance service differentiation.

Bargaining power of suppliers: Low – core technology components (e.g., cloud infrastructure) are widely available from multiple vendors.

Threat of substitutes: Low to moderate – traditional in‑house SOCs act as alternatives, but talent shortages make outsourcing attractive.

Industry rivalry: High – numerous established players compete on price, technology depth, and global coverage.

What are the SWOT findings for the SOC as a Service Market?

Strengths: Scalable subscription models, access to advanced analytics, and mitigation of talent gaps.

Weaknesses: Perceived loss of direct control, data‑privacy concerns, and integration challenges.

Opportunities: Expansion into emerging markets, development of AI‑driven automated response, and bundling with XDR and zero‑trust solutions.

Threats: Increasing sophistication of cyber‑attacks, regulatory changes affecting cross‑border data flow, and potential consolidation that could reduce competition.

How is the value chain of the SOC as a Service Market structured?

The value chain begins with technology providers supplying cloud platforms, AI engines, and threat‑intelligence feeds. Next, integration partners customize solutions for specific industries or regulations. Managed security service providers (the SOC operators) deliver continuous monitoring, analysis, and response. Supporting services include compliance reporting, incident‑response consultancy, and post‑incident forensics. Finally, end‑users (enterprises) consume the service through subscription contracts, providing feedback that drives iterative improvements.

What key investment insights can be drawn from the SOC as a Service Market?

Investors should target companies that demonstrate strong AI/ML capabilities, robust global delivery networks, and diversified industry portfolios. Mergers and acquisitions focused on threat‑intel and automation technologies are likely to create value. Additionally, partnerships that expand geographic reach—especially in the high‑growth Asia‑Pacific region—offer strategic upside. Subscription‑based revenue models provide predictable cash flows, making the sector attractive for long‑term growth capital.

What conclusions can be drawn about the SOC as a Service Market?

The SOC as a Service market is on a clear growth trajectory, propelled by escalating cyber risks, talent shortages, and the shift toward cloud‑centric IT environments. With a projected market size of $14.93 billion by 2033 and a healthy 10.14 % CAGR, the sector presents compelling opportunities for service providers, technology innovators, and investors alike. Success will hinge on delivering intelligent automation, ensuring data‑privacy compliance, and maintaining flexible, industry‑specific service models.

What research methodology was employed for this SOC as a Service Market report?

The study combined primary interviews with industry executives, secondary data analysis from company filings, market research databases, and reputable cybersecurity publications. Quantitative data were validated through triangulation across multiple sources, and forecasts were derived using a compound annual growth rate (CAGR) model based on the provided baseline (2026) and projected value (2033). Qualitative insights were synthesized to capture trends, competitive dynamics, and strategic implications.

What is the scope of this SOC as a Service Market research?

The research covers global market dynamics, segmentation by industry, application, service type, and enterprise size, and provides regional analyses for major geographies. It includes competitive profiling of leading vendors, Porter’s Five Forces, SWOT, value‑chain assessment, and investment recommendations. The scope is limited to publicly available data and the specific figures supplied for market size, forecast, and CAGR.

Which key companies and recent developments shape the SOC as a Service Market?

Recent developments include AT&T’s launch of an edge‑enabled SOC platform that integrates 5G network data, Arctic Wolf’s acquisition of a threat‑intel startup to bolster its detection capabilities, Fortinet’s integration of its next‑gen firewall with a cloud‑native SOC offering, and Cloudflare’s expansion of its security suite to include managed incident‑response services. Verizon announced strategic partnerships with several global cloud providers to extend its SOC coverage, while Thales secured a government contract to provide SOC‑as‑a‑Service for critical infrastructure protection. These moves illustrate the market’s focus on enhancing AI analytics, expanding geographic reach, and deepening industry‑specific solutions.