What is the Plant Protein Market Overview – definition, scope, and significance?

The plant protein market encompasses the production, processing, and distribution of protein derived from plant sources such as soy, wheat, and pea. It includes product types like isolates, concentrates, and protein flour, and serves applications ranging from protein beverages to bakery items. The market is significant because it addresses growing consumer demand for sustainable, health‑focused, and allergen‑friendly protein options, while also reducing reliance on animal‑based proteins.

What are the Plant Protein Market Drivers, Restraints, Challenges, and Opportunities?

Key drivers include rising health awareness, vegan and flexitarian lifestyles, and environmental concerns that favor plant‑based nutrition. Restraints involve supply chain volatility for raw legumes and consumer skepticism about taste and texture. Challenges arise from regulatory scrutiny over novel processing methods and competition from emerging alternative proteins. Opportunities exist in product innovation, clean‑label formulations, and expanding into emerging markets where protein deficiency remains a concern.

What are the current Plant Protein Market Growth Trends?

Trend analysis shows a shift toward high‑purity isolates for sports nutrition, while concentrates dominate mass‑market dairy alternatives. Plant‑based meat extenders are gaining traction as manufacturers blend animal and plant proteins to reduce cost and improve sustainability. Additionally, functional ingredients such as fortified protein bars and ready‑to‑drink beverages are experiencing rapid uptake, driven by on‑the‑go lifestyle preferences.

How has COVID‑19 impacted the Plant Protein Market and what is the recovery trajectory?

The pandemic accelerated demand for shelf‑stable plant protein ingredients as consumers stocked up on pantry staples. Disruptions in logistics briefly slowed raw material availability, but the sector rebounded quickly as health‑focused purchasing persisted. Recovery is now steady, with continued growth supported by post‑pandemic emphasis on immunity‑boosting nutrition and a return to food‑service channels introducing plant‑based menus.

What does the Plant Protein Market Competitive Landscape look like?

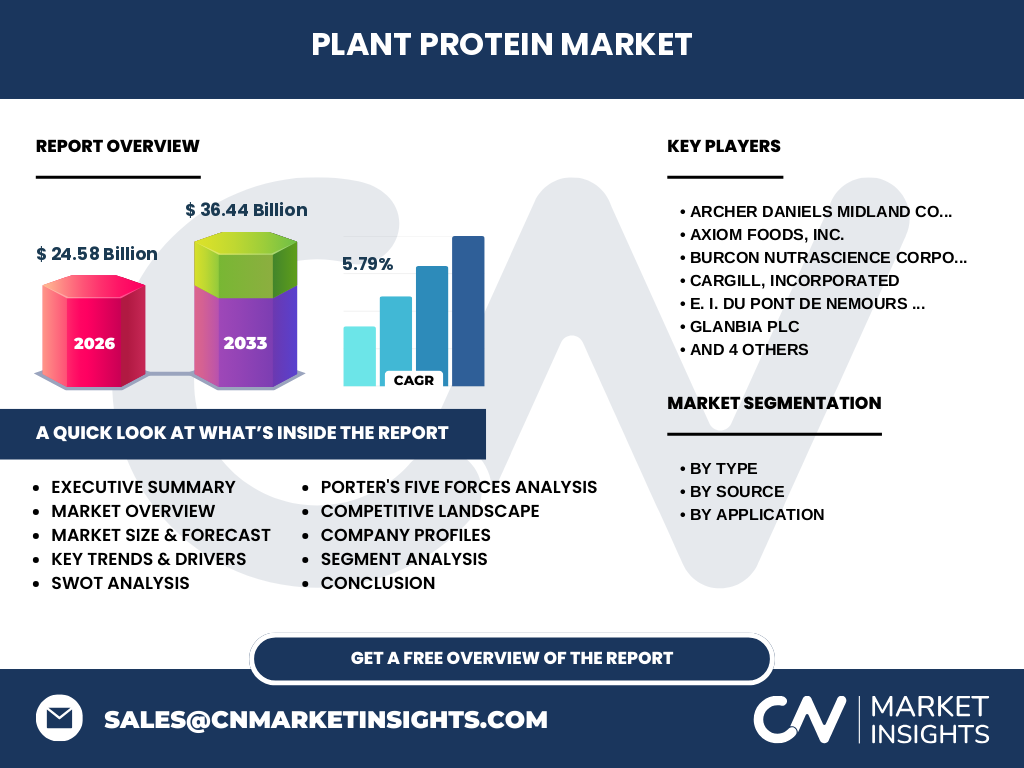

The market is moderately consolidated, featuring global agribusinesses and specialty ingredient firms. Leading players such as Archer Daniels Midland, Cargill, and DSM leverage integrated supply chains, while innovators like Axiom Foods and Burcon NutraScience focus on proprietary extraction technologies. Recent consolidation activity includes strategic partnerships and acquisitions aimed at expanding portfolio breadth across isolates, concentrates, and functional protein flours.

Can you provide an Executive Summary of the Plant Protein Market?

The plant protein market is valued at $24.58 billion in 2026 and is projected to reach $36.44 billion by 2033, reflecting a CAGR of 5.79 %. Growth is driven by health, sustainability, and innovation across isolates, concentrates, and protein flour. Major applications include beverages, dairy alternatives, meat extenders, bars, and bakery. Leading firms are investing in R&D and strategic alliances to capture expanding consumer demand worldwide.

What are the Plant Protein Market Forecasts for 2025‑2032?

Based on the provided CAGR of 5.79 %, the market is expected to maintain steady expansion through 2032, moving from the 2026 baseline of $24.58 billion toward the forecast horizon of $36.44 billion by 2033. This trajectory suggests consistent annual growth, underpinned by product innovation and geographic market penetration.

How is the Plant Protein Market Size and Share by Segmentation?

Segmentation by type divides the market into isolates, concentrates, and protein flour, each serving distinct functional needs. By source, soy, wheat, and pea proteins are the primary raw materials, with soy leading due to its high protein yield. Application segmentation includes protein beverages, dairy alternatives, meat alternatives/extenders, protein bars, and bakery, with dairy alternatives and meat extenders showing the fastest adoption rates.

What is the Global Plant Protein Market Size and Share by Region?

The global market is anchored by North America and Europe, where consumer acceptance of plant‑based diets is highest. Growing demand in the Asia‑Pacific region, driven by rising middle‑class incomes and urbanization, adds significant momentum. While specific regional dollar values are not disclosed, the overall market size of $24.58 billion in 2026 reflects contributions from all major geographic zones.

What does the Regional Analysis of the Plant Protein Market reveal?

In North America, strong retail distribution and premium product launches dominate growth. Europe benefits from regulatory support for sustainable food systems, encouraging plant protein integration in traditional food categories. Asia‑Pacific shows rapid expansion as manufacturers adapt local cuisines with plant‑based proteins, while Latin America and the Middle East exhibit emerging opportunities linked to rising health consciousness.

Which companies lead the Plant Protein Market and what are their strategies?

Key companies include Archer Daniels Midland, Cargill, DSM, and Glanbia, which focus on vertical integration and large‑scale production. Specialty firms like Axiom Foods and Burcon NutraScience pursue niche markets through innovative extraction and fermentation technologies. Strategic moves encompass joint ventures for source diversification, acquisition of boutique protein brands, and investment in R&D to develop clean‑label isolates.

How does Porter’s Five Forces analysis apply to the Plant Protein Market?

Threat of new entrants is moderate due to high capital requirements for processing facilities. Bargaining power of suppliers is moderate; raw legume availability can be limited but large agribusinesses mitigate risk. Bargaining power of buyers is growing as retailers demand lower costs and sustainable sourcing. Threat of substitutes includes animal proteins and emerging cultured meat, while competitive rivalry remains intense among established players and innovative newcomers.

What are the SWOT analysis highlights for the Plant Protein Market?

Strengths: Strong consumer trends toward health and sustainability; diversified raw material base. Weaknesses: Sensitivity to crop yields and price volatility. Opportunities: Expansion into emerging markets, development of high‑purity isolates, and formulation of functional foods. Threats: Regulatory changes, competition from alternative protein technologies, and potential consumer fatigue with plant‑based labeling.

How is the Plant Protein Market Value Chain structured?

The value chain starts with agricultural production of soy, wheat, and pea crops, followed by processing into isolates, concentrates, or protein flour. Subsequent stages involve formulation into finished products such as beverages, dairy alternatives, and meat extenders, distribution through wholesale and retail channels, and finally consumer purchase. Key value‑adding activities include purification, fortification, and flavor optimization.

What key investment insights can be drawn for the Plant Protein Market?

Investors should prioritize companies with integrated sourcing and processing capabilities to mitigate raw material risk. Funding innovative technologies like enzymatic extraction and fermentation offers high upside. Strategic allocation toward firms expanding in fast‑growing regions, particularly Asia‑Pacific, aligns with projected demand. Partnerships with consumer brands can accelerate market entry for novel protein applications.

What is the overall conclusion of the Plant Protein Market analysis?

The plant protein market is on a robust growth path, underpinned by a $24.58 billion base in 2026 and a forecasted rise to $36.44 billion by 2033. Health, sustainability, and functional food trends drive expansion across isolates, concentrates, and protein flour. Competitive dynamics favor firms that combine scale, innovation, and geographic reach, positioning the sector for continued relevance in the global protein landscape.

Which research methodology was used for this report?

The study employed a mixed‑method approach, integrating secondary data from industry reports, company filings, and reputable databases with primary insights gathered through expert interviews. Market sizing relied on top‑down and bottom‑up techniques, while trend analysis incorporated forward‑looking indicators such as consumer surveys and investment activity.

What is the scope of this research?

The scope covers global plant protein production, processing, and end‑use applications across isolates, concentrates, and protein flour derived from soy, wheat, and pea. It includes analysis of major geographic regions, competitive landscape, and forward projections to 2033. The report excludes detailed financial breakdowns beyond the provided market size and CAGR figures.

Who are the key companies and what recent developments have they announced?

Leading firms such as Archer Daniels Midland, Cargill, DSM, and Glanbia have launched new high‑purity isolate lines and entered joint ventures with dairy‑alternative brands. Axiom Foods announced a partnership to commercialize pea‑derived protein isolates, while Burcon NutraScience introduced a patented fermentation process for scalable protein production. Recent product launches include fortified protein beverages by Ingredion and specialized bakery protein blends from Kerry Group.