1. Europe Cleanroom Air Filter Market Overview - Definition, scope, and significance?

The Europe Cleanroom Air Filter Market encompasses the production, distribution, and application of high‑efficiency particulate air (HEPA) and ultra‑low penetration air (ULPA) filters used to maintain controlled environments—cleanrooms—across a range of high‑tech industries. Cleanrooms are classified according to stringent particle count limits, and the filters are critical for removing contaminants such as dust, microbes, and chemical vapors. The market’s scope covers the entire value chain from filter design and material sourcing to installation, testing, and after‑sales service, serving sectors like electronics, pharmaceuticals, biotechnology, and medical devices. Its significance lies in safeguarding product quality, ensuring regulatory compliance, and protecting patient safety, thereby directly influencing the competitiveness of Europe’s precision manufacturing and life‑science sectors.

2. Europe Cleanroom Air Filter Market Drivers, Restraints, Challenges, and Opportunities - Key growth factors and obstacles?

Key drivers include increasing demand for advanced semiconductor components, expanding biologics production, and tighter regulatory standards for aseptic processing. The push toward Industry 4.0 and automation further fuels the need for reliable contamination control. Restraints stem from high capital expenditure required for cleanroom construction and periodic filter replacement, which can limit adoption among smaller manufacturers. Challenges involve fluctuating raw‑material costs for filter media and the need for skilled technicians to certify filter performance. Opportunities arise from emerging applications such as nanotechnology manufacturing, the rollout of next‑generation HEPA/ULPA media with longer service life, and green‑filter initiatives that reduce energy consumption while maintaining filtration efficiency.

3. Europe Cleanroom Air Filter Market Growth Trends - Current and emerging trends shaping the market?

Current trends show a steady shift from conventional glass‑fiber HEPA media to synthetic nanofiber and electrostatically charged filters that deliver higher efficiency with lower pressure drop. Manufacturers are also integrating IoT‑enabled monitoring systems that provide real‑time filter integrity data, reducing unscheduled downtime. Emerging trends include the adoption of modular cleanroom designs that allow rapid reconfiguration, and increased collaboration between filter suppliers and equipment OEMs to develop fully integrated contamination‑control solutions tailored to specific process flows.

4. COVID-19 Impact on the Europe Cleanroom Air Filter Market - Pandemic effects and recovery trajectory?

The COVID‑19 pandemic initially disrupted supply chains for raw materials and delayed cleanroom construction projects across Europe. However, the crisis also highlighted the critical role of cleanroom filtration in vaccine and diagnostic manufacturing, leading to a surge in orders for high‑performing HEPA and ULPA filters. By 2022, the market began recovering rapidly, supported by government stimulus for biotech R&D and accelerated vaccination campaigns. The recovery trajectory remains positive, with renewed investment in resilient supply chains and a heightened focus on pandemic preparedness driving sustained demand.

5. Europe Cleanroom Air Filter Market Competitive Landscape - Major competitors and market consolidation?

The competitive arena is characterized by a mix of multinational corporations and specialized niche players. Leading companies such as Camfil, Mann+Hummel, Freudenberg SE, and Parker Hannifin Corporation dominate due to extensive product portfolios and strong distribution networks. Recent consolidation activity includes strategic acquisitions aimed at expanding media technology capabilities and geographic reach. While the market remains fragmented, the top ten firms collectively hold a significant share, fostering a competitive environment focused on innovation, service quality, and compliance support.

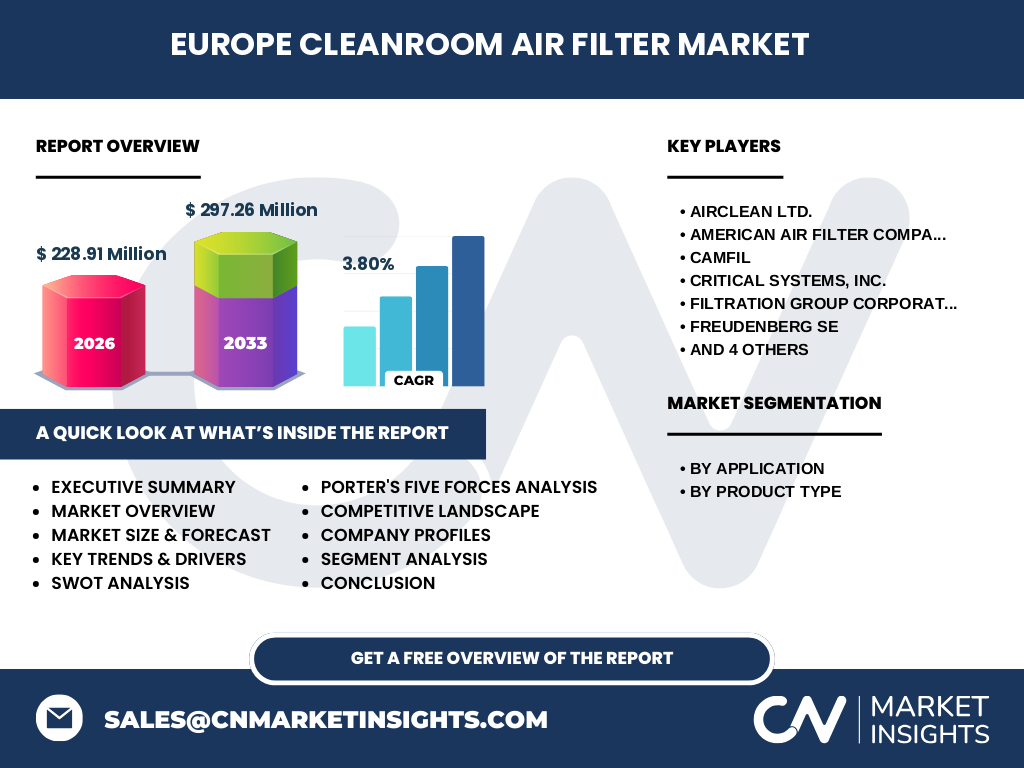

6. Executive Summary - High-level overview and key findings about Europe Cleanroom Air Filter Market?

The Europe Cleanroom Air Filter Market is valued at €228.91 million in 2026 and is projected to reach €297.26 million by 2033, reflecting a compound annual growth rate (CAGR) of 3.80 %. Growth is propelled by robust demand in electronics, pharmaceuticals, biotechnology, and medical devices, alongside regulatory pressures and technological advancements in filter media. The market benefits from strong competitive dynamics, increasing adoption of smart monitoring, and emerging opportunities in green filtration. Despite cost pressures and supply‑chain volatility, the outlook remains favorable, with sustained investment expected across the region.

7. Europe Cleanroom Air Filter Market Forecast - Projections for 2025‑2032 period?

Looking ahead to the 2025‑2032 horizon, the market is expected to maintain a steady upward trajectory, adhering closely to the 3.80 % CAGR identified for the broader 2027‑2033 forecast window. Demand from the electronics sector will be bolstered by 5G infrastructure and advanced packaging, while pharmaceutical and biotechnology growth will be driven by personalized medicine and gene‑therapy production. The medical‑device segment will continue to expand as Europe tightens standards for implantable and diagnostic equipment. These sectoral drivers, combined with incremental price‑elasticity in filter replacement cycles, underpin the projected revenue growth.

8. Europe Cleanroom Air Filter Market Size and Share by Segmentation - Breakdown by segment?

Segmentation by application reveals that the pharmaceutical segment commands the largest share, reflecting stringent sterility requirements and the high volume of biologics manufacturing in Europe. The electronics segment follows, driven by semiconductor and display production. Biotechnology and medical‑device applications each account for a meaningful portion of the market, with steady expansion as new therapies and devices reach commercialization. By product type, HEPA filters dominate due to their broad applicability and cost‑effectiveness, while ULPA filters capture premium pricing in ultra‑clean environments such as advanced research labs and high‑precision semiconductor fabs.

9. Global Europe Cleanroom Air Filter Market Size and Share by Region - Geographic distribution?

Within the European context, the market is concentrated in Western and Central Europe, where the majority of high‑tech manufacturing hubs are located. Countries such as Germany, France, the United Kingdom, and the Netherlands exhibit the highest consumption of cleanroom filters, attributable to dense clusters of pharmaceutical firms, semiconductor fabs, and medical‑device manufacturers. Eastern European nations contribute growing demand, supported by expanding biotech parks and cost‑competitive production facilities.

10. Regional Analysis of the Europe Cleanroom Air Filter Market - Detailed regional market performance?

Germany leads the region, leveraging its strong automotive electronics and precision engineering sectors. France’s market strength is anchored in its world‑renowned pharmaceutical and biotech ecosystem. The United Kingdom shows resilience through its thriving medical‑device industry and continued investment in life‑science research. The Benelux region benefits from high‑density logistics hubs that support rapid distribution of filter products. Scandinavia, while smaller in absolute terms, demonstrates high adoption of energy‑efficient filtration technologies, aligning with regional sustainability goals.

11. Leading Company Profiles in the Europe Cleanroom Air Filter Market - Industry players and strategies?

Camfil focuses on innovative filter media and offers comprehensive service contracts that include on‑site performance testing. Mann+Hummel differentiates through modular cleanroom solutions and digital monitoring platforms. Freudenberg SE leverages its extensive material science expertise to produce high‑durability ULPA media. Parker Hannifin Corporation expands its footprint via strategic partnerships with OEMs in the semiconductor space. Airclean Ltd. and AAF Flanders emphasize custom‑engineered solutions for niche pharmaceutical applications. These firms pursue growth through R&D investment, geographic expansion, and value‑added services.

12. Porter's Five Forces Analysis of the Europe Cleanroom Air Filter Market - Competitive forces assessment?

Threat of new entrants is moderate; high capital requirements and technical expertise create barriers, yet niche innovators can enter via specialized media technologies. Bargaining power of suppliers is relatively low because filter manufacturers often source raw materials from multiple vendors, mitigating supply risk. Bargaining power of buyers is moderate to high, as large pharmaceutical and electronics customers negotiate volume discounts and demand rigorous compliance documentation. Threat of substitutes is minimal, given the regulatory necessity of HEPA/ULPA filtration in cleanrooms. Competitive rivalry is intense, driven by product differentiation, service quality, and after‑sales support.

13. SWOT Analysis of the Europe Cleanroom Air Filter Market - Strengths, weaknesses, opportunities, threats?

Strengths: Established base of technologically advanced manufacturers, strong demand from regulated industries, and a clear regulatory framework supporting filter adoption.

Weaknesses: High upfront costs for filter systems, dependency on volatile raw‑material prices, and limited awareness of energy‑saving filter options among some end‑users.

Opportunities: Development of next‑generation nanofiber media, integration of IoT‑based monitoring, and expansion into emerging biotech clusters across Eastern Europe.

Threats: Potential supply‑chain disruptions, tightening environmental regulations that could increase operational costs, and competitive pressure from low‑cost manufacturers outside Europe.

14. Europe Cleanroom Air Filter Market Value Chain Analysis - Industry structure and value flow?

The value chain begins with raw‑material suppliers (glass‑fiber, synthetic polymers, nanofibers) which feed filter manufacturers that design and fabricate HEPA/ULPA products. Next are system integrators that assemble filters into cleanroom modules, followed by distributors and regional sales offices that deliver to end‑users. After‑sales service— including installation, certification, and periodic replacement—adds significant value and creates recurring revenue streams. Feedback loops from end‑users to manufacturers drive continuous improvement in filter performance and sustainability.

15. Key Investment Insights in the Europe Cleanroom Air Filter Market - Strategic investment recommendations?

Investors should prioritize companies with strong R&D pipelines focused on low‑pressure‑drop, high‑efficiency media, as these solutions meet both regulatory and sustainability criteria. Partnerships with OEMs in high‑growth sectors such as semiconductor packaging and gene‑therapy production offer scalable revenue opportunities. Additionally, acquiring or funding firms that provide digital monitoring and predictive maintenance platforms can generate differentiated, high‑margin service offerings. Geographic diversification—especially targeting fast‑growing Eastern European biotech hubs—will enhance portfolio resilience.

16. Europe Cleanroom Air Filter Market Conclusion - Summary and key takeaways?

The Europe Cleanroom Air Filter Market is on a solid growth path, underpinned by a 3.80 % CAGR and a projected market size of €297.26 million by 2033. Demand is broadly distributed across electronics, pharmaceutical, biotechnology, and medical‑device applications, with HEPA filters holding the dominant product share. Competitive dynamics are shaped by innovation in filter media, digital service integration, and strategic consolidation. While cost and supply considerations pose challenges, opportunities in green filtration, IoT‑enabled monitoring, and emerging biotech clusters provide compelling avenues for expansion.

17. Research Methodology - How this research was conducted?

The study combines primary interviews with industry experts, senior engineers, and procurement managers, alongside secondary data collection from company reports, regulatory publications, and reputable market databases. Quantitative data were validated through cross‑checking of vendor disclosures and third‑party financial statements. Qualitative insights were synthesized to generate trend analysis, while forecasting employed a compound annual growth rate derived from historical performance and forward‑looking macro indicators.

18. Research Scope - Coverage and limitations?

The scope encompasses the European region, covering major markets in Western, Central, and Eastern Europe, and includes the full spectrum of cleanroom air filtration applications and product types (HEPA and ULPA). The analysis focuses on the period up to 2033. Limitations arise from the proprietary nature of some company-level financials, which restricts the granularity of market‑share calculations. Nonetheless, the study provides a comprehensive view based on the most reliable data available.

19. Key Companies and Recent Developments in the Europe Cleanroom Air Filter Market - Introduction to top companies and their recent announcements, product launches, partnerships, and strategic developments?

Camfil recently unveiled a nanofiber‑enhanced HEPA line that promises a 20 % reduction in pressure drop. Mann+Hummel announced a partnership with a leading semiconductor fab to co‑develop modular filter cartridges equipped with real‑time contaminant sensors. Freudenberg SE launched an ULPA filter series certified for ISO 1 cleanrooms, targeting advanced research facilities. Parker Hannifin expanded its European service network, adding 15 new field‑service teams to improve turnaround times for filter replacement. Airclean Ltd. introduced a sustainable filter programme that recycles filter media at end‑of‑life, aligning with EU circular‑economy directives. These developments illustrate the market’s focus on performance, digitalization, and environmental responsibility.