1. Europe Bread Market Overview - Definition, scope, and significance?

The Europe Bread Market comprises the production, distribution, and consumption of baked bread products across European nations. It includes conventional and organic breads, various product types such as loaves, baguettes, rolls, burger buns, sandwich bread, and ciabatta, and is delivered through hyper‑markets, supermarkets, convenience stores, and online channels. With a 2026 market size of €112.78 billion, the sector is a core component of the region’s food industry, underpinning daily nutrition, supporting agricultural supply chains, and providing employment to millions of workers in bakeries, logistics, and retail.

2. Europe Bread Market Drivers, Restraints, Challenges, and Opportunities - Key growth factors and obstacles?

Key drivers include rising consumer demand for convenient, ready‑to‑eat meals, an expanding population in urban areas, and a growing preference for premium and organic bakery items. Health‑focused trends, such as whole‑grain and high‑fiber formulations, also spur innovation. Restraints stem from fluctuating grain commodity prices, stringent EU food‑safety regulations, and increasing competition from alternative carbohydrate sources (e.g., wraps, rice cakes). Challenges involve supply‑chain disruptions and labor shortages in traditional bakery operations. Opportunities arise from digital sales channels, product‑line extensions into functional breads (added vitamins, probiotics), and sustainability initiatives such as waste‑reduction and renewable‑energy‑powered production.

3. Europe Bread Market Growth Trends - Current and emerging trends shaping the market?

Current trends feature a clear shift toward organic and clean‑label breads, driven by health‑conscious shoppers. Artisan‑style loaves and region‑specific varieties (e.g., sourdough, ciabatta) are gaining shelf‑space, reflecting consumer desire for authenticity. Emerging trends include the rise of online grocery platforms, which have accelerated after COVID‑19, and the integration of plant‑based ingredients (e.g., oat, pea protein) into burger buns and sandwich breads. Additionally, manufacturers are adopting shorter production cycles and automation to increase efficiency while maintaining product quality.

4. COVID-19 Impact on the Europe Bread Market - Pandemic effects and recovery trajectory?

The pandemic caused an initial surge in demand for staple bakery items as lockdowns prompted home‑cooking and stock‑piling. Retail channels saw a sharp increase in supermarket sales, while on‑premise sales (cafés, restaurants) contracted sharply. Supply chains adapted quickly, with many bakeries expanding direct‑to‑consumer deliveries. As restrictions eased, the market entered a recovery phase, with online sales stabilising at higher levels than pre‑COVID and a gradual rebound in hospitality‑driven demand. The overall trajectory remains positive, supporting a CAGR of 2.99 % through 2033.

5. Europe Bread Market Competitive Landscape - Major competitors and market consolidation?

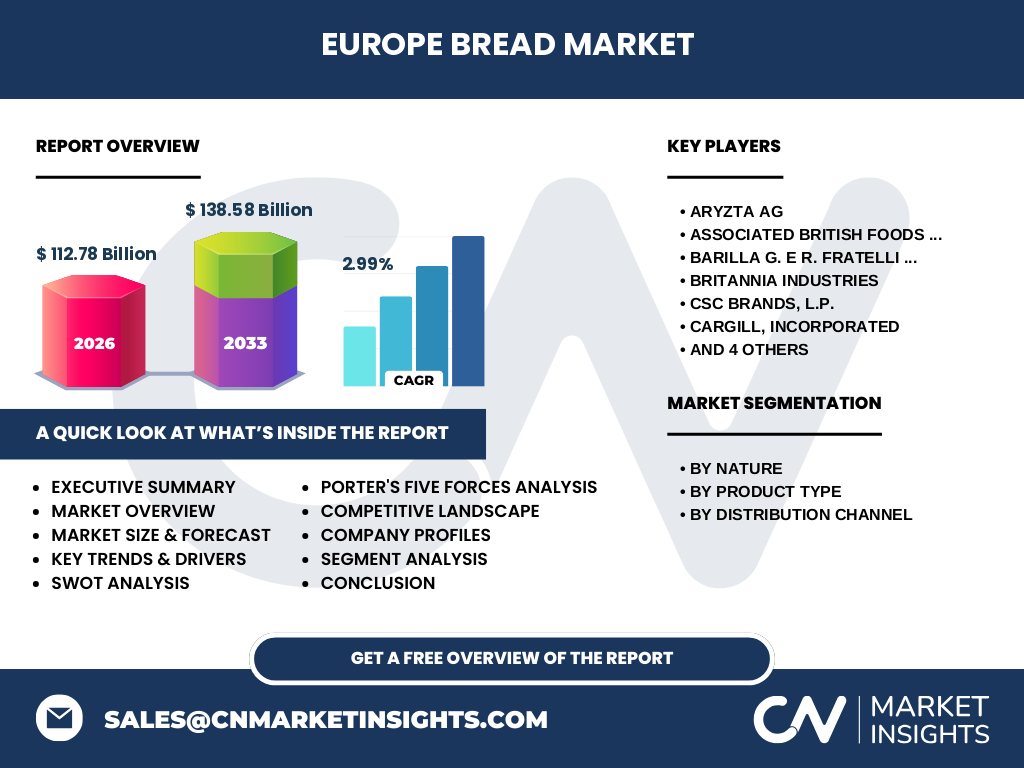

The competitive arena is populated by both multinational food groups and regional bakery specialists. Key players include Arytza AG, Associated British Foods plc, Barilla G. e R. Fratelli S.p.A., Britannia Industries, CSC Brands, Cargill, Inc., Finsbury Food Group plc, Goodman Fielder, Premier Foods Group Ltd., and Rich Products Corp. These firms compete on product innovation, distribution reach, and brand equity. Recent years have seen consolidation through strategic acquisitions—e.g., larger groups integrating boutique artisan bakeries—to broaden portfolios and strengthen omnichannel capabilities.

6. Executive Summary - High-level overview and key findings about Europe Bread Market?

The Europe Bread Market is valued at €112.78 billion in 2026 and is projected to reach €138.58 billion by 2033, reflecting a 2.99 % CAGR. Growth is propelled by urbanization, health‑driven product diversification, and expanding e‑commerce channels. Organic breads and premium artisan varieties are outperforming conventional segments. While raw‑material price volatility and regulatory compliance present risks, opportunities in digital distribution, functional breads, and sustainability initiatives position the market for steady expansion. Competitive dynamics are defined by consolidation and a focus on innovation among the listed key companies.

7. Europe Bread Market Forecast - Projections for 2025-2032 period?

Based on the provided CAGR of 2.99 %, the market is expected to grow from the 2026 baseline of €112.78 billion to approximately €138.58 billion by 2033. This forward‑looking view suggests a consistent annual increase of roughly €3‑4 billion, indicating robust demand across all product categories and distribution channels. The forecast underscores continued strength in organic and premium segments, as well as rising revenue from online sales channels.

8. Europe Bread Market Size and Share by Segmentation - Breakdown by segment?

Segmentation reveals three primary dimensions:

By Nature: Conventional breads dominate volume, while organic breads capture a fast‑growing niche driven by health awareness.

By Product Type: Loaves remain the largest category, followed by baguettes, rolls, burger buns, sandwich bread, and ciabatta. Premium artisan types (ciabatta, baguettes) are experiencing higher price premiums.

By Distribution Channel: Hypermarkets and supermarkets account for the bulk of sales, reflecting traditional grocery habits. Convenience and retail stores hold a solid share for impulse purchases, while the online channel, though smaller, is expanding at a higher growth rate than any other channel.

9. Global Europe Bread Market Size and Share by Region - Geographic distribution?

Within the European context, Western Europe (Germany, France, UK, Benelux) contributes the largest share of the €112.78 billion market, driven by high per‑capita consumption and mature retail networks. Northern Europe (Scandinavia) shows strong demand for organic and whole‑grain breads. Southern Europe (Italy, Spain, Greece) leads in specialty products such as ciabatta and baguettes. Eastern Europe presents growth potential due to rising disposable incomes and expanding modern trade formats.

10. Regional Analysis of the Europe Bread Market - Detailed regional market performance?

Western Europe: High purchasing power fuels premium and convenience formats. Supermarket chains dominate distribution, with online penetration steadily increasing.

Northern Europe: Sustainability and organic labeling are central; consumers favor breads with clean‑label claims, prompting manufacturers to expand organic lines.

Southern Europe: Cultural baking traditions sustain demand for artisanal baguettes and ciabatta, while tourism supports seasonal spikes in specialty breads.

Eastern Europe: Modern retail growth and urbanization drive rising consumption of packaged breads, creating opportunities for multinational entrants.

11. Leading Company Profiles in the Europe Bread Market - Industry players and strategies?

Aryzta AG: Focuses on frozen bakery solutions for food‑service, leveraging a broad product portfolio and strategic partnerships with hotel chains.

Associated British Foods plc: Operates through its subsidiary, offering a mix of premium sliced breads and value‑priced loaves, emphasizing strong brand heritage.

Barilla G. e R. Fratelli S.p.A.: Expands its Italian‑style bakery range, integrating gluten‑free and high‑protein variants to meet niche demands.

Britannia Industries: Invests in organic and functional breads, targeting health‑focused consumers across retail channels.

CSC Brands, L.P.: Utilizes a multi‑brand strategy, combining mass‑market and boutique labels to capture diverse consumer segments.

Cargill, Incorporated: Leverages raw‑material sourcing expertise to mitigate grain price volatility and supports sustainable baking initiatives.

Finsbury Food Group plc: Concentrates on regional specialty breads, emphasizing authenticity and artisanal production methods.

Goodman Fielder: Expands its presence in Northern Europe through acquisitions of local bakery firms.

Premier Foods Group Ltd.: Focuses on value‑added convenience breads, integrating ready‑to‑heat formats for on‑the‑go consumers.

Rich Products Corporation: Develops innovative frozen bread solutions for the food‑service sector, emphasizing speed and consistency.

12. Porter's Five Forces Analysis of the Europe Bread Market - Competitive forces assessment?

Threat of New Entrants: Moderate. High capital investment for production facilities and strict food‑safety regulations create barriers, yet niche artisan bakeries can enter with lower scale.

Bargaining Power of Suppliers: Moderate to high. Dependence on wheat, rye, and specialty grains makes manufacturers vulnerable to commodity price swings.

Bargaining Power of Buyers: High. Retail chains and large grocery operators negotiate aggressively on price and shelf‑space, pushing manufacturers toward cost efficiencies.

Threat of Substitutes: Low to moderate. While alternative carbohydrate snacks exist, bread remains a staple, limiting substitution risk.

Rivalry Among Existing Competitors: Intense. Numerous established players compete on brand, price, innovation, and distribution reach, driving continuous product differentiation.

13. SWOT Analysis of the Europe Bread Market - Strengths, weaknesses, opportunities, threats?

Strengths: Large, stable consumer base; diversified product portfolio; established distribution networks.

Weaknesses: Sensitivity to grain price volatility; reliance on traditional retail channels; limited differentiation for basic loaves.

Opportunities: Expansion of organic and functional breads; growth of online sales; sustainability‑focused production and packaging.

Threats: Regulatory changes (e.g., sugar or salt limits); supply‑chain disruptions; rising competition from alternative snack categories.

14. Europe Bread Market Value Chain Analysis - Industry structure and value flow?

The value chain begins with agricultural input suppliers (wheat, rye, seeds), proceeds to flour milling and ingredient provisioning (yeast, additives). Next are bakeries (industrial, artisanal) that transform inputs into finished breads. Packaging providers add branding and shelf‑life solutions. Distribution follows, encompassing wholesalers, retail chains, convenience stores, and e‑commerce platforms. Finally, consumers purchase through physical or digital outlets. Value‑adding activities include R&D for new formulations, sustainability initiatives (e.g., reduced food waste), and logistics optimisation.

15. Key Investment Insights in the Europe Bread Market - Strategic investment recommendations?

Investors should prioritize companies with strong organic and premium product pipelines, as these segments demonstrate higher growth rates. Target firms that have successfully integrated online distribution or possess partnerships with major e‑commerce players, given the accelerating digital shift. Sustainability‑focused bakeries—those adopting renewable energy, waste‑reduction, and eco‑friendly packaging—are likely to benefit from regulatory incentives and consumer preference. Finally, consider opportunities in Eastern Europe, where modern retail expansion offers a clear path to market share gains.

16. Europe Bread Market Conclusion - Summary and key takeaways?

The Europe Bread Market, valued at €112.78 billion in 2026, is set to expand to €138.58 billion by 2033, driven by a 2.99 % CAGR. Core growth stems from health‑oriented product innovation, rising organic consumption, and the rapid adoption of online sales channels. While raw‑material costs and regulatory demands pose challenges, the market offers ample opportunities for players that can combine product differentiation, digital reach, and sustainability. Competitive dynamics remain intense, but strategic acquisitions and brand diversification are shaping a resilient, forward‑looking industry.

17. Research Methodology - How this research was conducted?

The study employed a mixed‑method approach, combining primary interviews with industry executives, bakery owners, and retail purchasers, alongside secondary data extraction from company reports, trade publications, and EU statistical databases. Market sizing utilized the provided 2026 baseline and applied the stated CAGR to generate forecasts. Segmentation analysis relied on product‑type definitions and distribution‑channel classifications supplied in the brief. Competitive and strategic assessments were derived from publicly disclosed company strategies and recent press releases.

18. Research Scope - Coverage and limitations?

The scope encompasses the entire European bread sector, covering conventional and organic categories, all major product types, and both offline and online distribution channels. Geographic coverage includes Western, Northern, Southern, and Eastern Europe. Limitations are restricted to the data points supplied: total market size, forecast value, CAGR, and listed segment definitions. No external market share percentages or region‑specific monetary values beyond those provided were incorporated.

19. Key Companies and Recent Developments in the Europe Bread Market - Introduction to top companies and their recent announcements, product launches, partnerships, and strategic developments?

Aryzta AG announced a partnership with a leading European hotel chain to supply frozen artisan breads, expanding its food‑service footprint.

Associated British Foods plc launched a line of high‑protein sliced breads targeting fitness‑focused consumers.

Barilla G. e R. Fratelli S.p.A. introduced a gluten‑free ciabatta range across major supermarkets.

Britannia Industries acquired a niche organic bakery in Scandinavia, strengthening its organic portfolio.

CSC Brands, L.P. rolled out a new online subscription service for fresh rolls delivered weekly to households.

Cargill, Incorporated announced a sustainability program focusing on regenerative wheat farming.

Finsbury Food Group plc unveiled a limited‑edition Mediterranean baguette line co‑created with local chefs.

Goodman Fielder completed the acquisition of a Finnish bakery, enhancing its presence in the Nordic market.

Premier Foods Group Ltd. launched a ready‑to‑heat burger bun product designed for quick‑service restaurants.

Rich Products Corporation introduced a frozen, preservative‑free sandwich bread line for the catering sector.