What is the North America High‑Flow Nasal Cannula Market Overview – definition, scope, and significance?

The North America High‑Flow Nasal Cannula (HFNC) market encompasses devices that deliver heated, humidified oxygen at flow rates up to 60 L/min through specially designed nasal prongs. The scope includes all components (air‑oxygen blender, nasal cannula, heated inspiratory circuit, active humidifier) and end‑user segments such as ambulatory care centers, hospitals, and long‑term care facilities. HFNC therapy is significant because it provides a non‑invasive alternative for patients with acute and chronic respiratory conditions, improves patient comfort, reduces the need for intubation, and aligns with the region’s focus on advanced respiratory care.

What are the market drivers, restraints, challenges, and opportunities in North America?

Key drivers include rising prevalence of chronic obstructive pulmonary disease (COPD) and acute respiratory failure, increasing adoption of minimally invasive ventilation, and strong reimbursement frameworks in the United States and Canada. Restraints stem from high capital costs of HFNC systems and the need for staff training. Challenges involve competition from conventional oxygen therapy and variability in clinical guidelines across institutions. Opportunities arise from technological advancements such as integrated monitoring, expanding home‑care applications, and partnerships that broaden distribution networks.

What growth trends are currently shaping the North America High‑Flow Nasal Cannula Market?

Current trends feature a shift toward portable HFNC units for outpatient and home settings, integration of digital analytics for real‑time flow and temperature monitoring, and a preference for single‑use consumables to enhance infection control. Emerging trends include the development of AI‑driven decision support tools that optimize flow settings, and increasing clinical research that supports HFNC use in novel indications such as post‑surgical care and neonatal respiratory support.

How did COVID‑19 impact the North America High‑Flow Nasal Cannula Market and what is the recovery trajectory?

The pandemic spurred a rapid increase in HFNC deployment as hospitals sought alternatives to invasive ventilation for COVID‑19 patients with hypoxemic respiratory failure. Demand surged, prompting accelerated production and expanded inventory. Post‑pandemic, the market retains elevated baseline usage because clinicians have recognized the therapeutic benefits of HFNC beyond COVID‑19. Recovery is now a steady growth phase rather than a rebound, with continued procurement driven by long‑term clinical adoption.

Who are the major competitors and what is the consolidation landscape in the market?

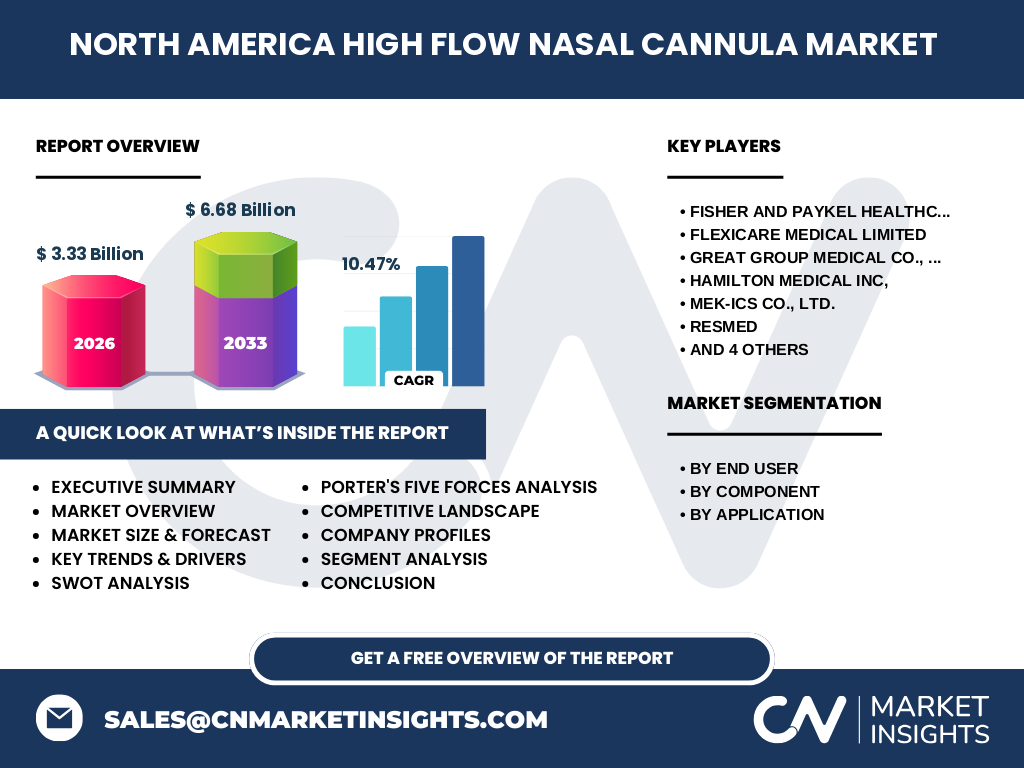

Major competitors include Fisher & Paykel Healthcare Limited, Resmed, Teleflex Incorporated, Vapotherm, Hamilton Medical Inc., Flexicare Medical Limited, Great Group Medical Co., Ltd., Mek‑Ics Co., Ltd., Salter Labs, and TNI Medical AG. The competitive landscape shows a mix of large multinational corporations and specialized niche players. Recent years have seen strategic collaborations, joint ventures, and selective acquisitions aimed at expanding product portfolios and geographic reach, reflecting moderate consolidation while preserving a diverse supplier base.

What are the high‑level findings in the Executive Summary?

The North America HFNC market is valued at USD 3.33 billion in 2026 and is projected to reach USD 6.68 billion by 2033, delivering a CAGR of 10.47 % over the forecast period. Growth is propelled by rising respiratory disease burden, strong reimbursement, and technological innovation. The market is segmented by end‑user, component, and application, with hospitals and long‑term care centers representing the largest end‑user share. Leading firms are investing in product differentiation and expanding into home‑care segments, positioning the market for sustained expansion.

What is the market forecast for 2025‑2032?

Based on the provided CAGR of 10.47 %, the market is expected to continue expanding steadily through 2032, surpassing the 2027 forecast level of USD 6.68 billion. The forecast reflects ongoing adoption across acute care settings, growing home‑care adoption, and incremental sales of consumable components such as nasal cannulas and humidifier filters. The trajectory suggests a robust upside potential for manufacturers and investors alike.

How is the market sized and shared by segmentation?

Segmentation is organized into three primary dimensions. By end‑user, the market is split between ambulatory care centers and hospitals/long‑term care centers. By component, it comprises air‑oxygen blenders, nasal cannulas, heated inspiratory circuits, and active humidifiers. By application, the market addresses bronchiectasis, acute respiratory failure, acute heart failure, and COPD. While exact revenue shares are not disclosed, each segment contributes meaningfully to the overall USD 3.33 billion base, with hospitals and acute respiratory failure leading in volume.

What is the geographic distribution of the market size and share?

The market is confined to the North America region, encompassing the United States and Canada. The United States dominates due to its larger healthcare infrastructure, higher per‑capita device adoption, and extensive reimbursement programs. Canada contributes a smaller but growing share, driven by national health system investments in advanced respiratory support. Together, these countries account for the entire market valuation of USD 3.33 billion in 2026.

What does the regional analysis reveal about market performance?

In the United States, market performance is characterized by high procurement rates in tertiary hospitals, rapid integration of portable HFNC units, and strong private‑sector investment. Canadian market performance reflects steady growth aligned with public‑sector budgeting cycles and increased use in long‑term care facilities. Both regions exhibit a consistent shift toward non‑invasive ventilation strategies, reinforcing the upward trend across the North American landscape.

Which companies lead the North America High‑Flow Nasal Cannula Market and what are their strategies?

Fisher & Paykel Healthcare Limited leads with a broad portfolio of integrated HFNC systems and a focus on R&D for next‑generation humidification technology. Resmed leverages its strong respiratory device distribution network to cross‑sell HFNC solutions. Teleflex Incorporated emphasizes modular component design for customizable configurations. Vapotherm focuses on high‑flow precision and exclusive consumables. Other players such as Hamilton Medical Inc. and Flexicare Medical Limited pursue niche market penetration through specialized clinical studies and strategic partnerships.

How does Porter’s Five Forces analysis apply to this market?

Threat of new entrants: Moderate, due to high capital requirements and regulatory hurdles. Bargaining power of suppliers: Low to moderate, as component suppliers are numerous but critical for quality. Bargaining power of buyers: High, especially large hospital systems that demand volume discounts and integrated service contracts. Threat of substitutes: Moderate, with conventional oxygen therapy and non‑invasive ventilation devices offering alternatives. Competitive rivalry: Intense, driven by innovation, product differentiation, and service agreements.

What are the SWOT insights for the North America High‑Flow Nasal Cannula Market?

Strengths: Proven clinical efficacy, growing adoption, strong reimbursement. Weaknesses: High upfront cost, need for specialized training. Opportunities: Expansion into home‑care, AI‑enabled devices, emerging indications. Threats: Competitive pressure from alternative ventilation technologies and potential regulatory changes.

What does the value chain analysis reveal about the market?

The value chain begins with raw‑material suppliers for medical‑grade plastics and electronics, progresses to component manufacturers (blenders, humidifiers), then to system integrators assembling complete HFNC units. Distribution channels include direct sales to large hospital groups, third‑party distributors for ambulatory centers, and online platforms for consumables. After‑sales services, training, and maintenance contracts add value, while end‑users (clinicians and patients) drive final adoption.

What key investment insights can be drawn for stakeholders?

Investors should focus on companies that demonstrate strong R&D pipelines, diversified product lines across components, and robust distribution in both acute and home‑care settings. Partnerships that expand consumable sales and recurring revenue streams are attractive. Given the 10.47 % CAGR, capital allocation toward firms with scalable manufacturing and regulatory expertise is likely to yield above‑average returns.

What are the main conclusions from the market analysis?

The North America HFNC market is on a high‑growth trajectory, underpinned by clinical demand, reimbursement support, and technological innovation. Hospitals remain the primary demand engine, while ambulatory and home‑care segments present emerging growth pockets. Leading manufacturers are consolidating capabilities through product diversification and strategic alliances, positioning the market for continued expansion through 2033.

How was the research methodology designed?

The study employed a mixed‑method approach, combining primary interviews with clinicians, procurement officers, and industry executives, with secondary data from regulatory filings, company reports, and reputable market databases. Quantitative forecasting used the CAGR of 10.47 % applied to the 2026 base of USD 3.33 billion, while qualitative insights were derived from trend analysis and expert opinion.

What is the scope of this research and its limitations?

The scope covers the North America HFNC market, encompassing all major components, end‑users, and applications listed. It excludes detailed country‑by‑country breakdowns beyond the United States and Canada, and it does not provide proprietary sales figures for individual companies. All analysis is confined to the data provided and publicly available sources up to the research date.

Which key companies have recent developments in the market?

Fisher & Paykel Healthcare Limited announced a next‑generation humidifier with faster warm‑up time. Resmed introduced a compact, battery‑operated HFNC unit targeting home care. Teleflex Incorporated launched a modular circuit kit to reduce inventory complexity. Vapotherm released a new line of high‑efficiency nasal cannulas designed for pediatric use. Hamilton Medical Inc. reported a partnership with a major US health system to pilot AI‑driven flow optimization. These developments reflect ongoing innovation and market reinforcement.